|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

| Jan | Feb | Mar | Apr | May | June | July | Aug | Sep | Oct | Nov | Dec |

|

|

|

|

Daron Acemoglu and James Robinson

It is well-known that who you know and who you are connected to matters greatly for your business success in many countries. This is nicely documented in several papers that show how connections to powerful politicians have a huge value in countries with weak institutions.

For example, in a famous paper Ray Fisman used an event study methodology exploiting rumors about the health of the Indonesian dictator President Suharto to show how close connections to Suharto were greatly valuable: these adverse news reduce the stock market value of the firms connected to him.

Similar results were found, among other places, in Malaysia by Simon Johnson and Todd Mitton and in Pakistan by Asim Khwaja and Atif Mian.

But the consensus view has been that such connections don't matter in countries with strong institutions such as the United States.

In fact, Larry Summers used this as the basis for his argument for why the response to financial crises should be different in the United States in his Ely Lecture to the American Economic Association: strong US institutions imply that policies that should not be tried in Indonesia or Malaysia because of concerns about cronyism and corruption could be adopted with little worry in the United States.

This view was supported by work that applied similar methodology to the United States. For example, other work by Ray Fisman, together with co-authors, found that the value of connections to Dick Cheney were small or nonexistent.

So US institutions do seem to work as they are supposed to.

Recent work by Daron, Simon Johnson, Amir Kermani, James Kwak and Todd Mitton finds something quite different, however.

Focusing on the announcement of Timothy Geithner as President-elect Obama's nominee for Treasury Secretary in November 2008, they report robust and large returns to financial firms with connections to Geithner. Connections here are defined either from Timothy Geithner's meetings with financial firm executives during the previous two years when he was the President of the Federal Reserve Bank of New York, or from his overlap on non-profit boards with these executives. What's going on?

One possibility is that this just reflects the fact that firms that had such connections are also those that would have actually benefited from the safe pair of hands that Timothy Geithner would bring to the job of Treasury Secretary. Though plausible, this explanation does not receive any support from the data: controls for characteristics that could capture such benefits do not change the results, and in fact the results hold when comparing firms of very similar size, profitability and leverage, and similar risk and stock market return profiles.

Another possibility is that the same sort of shady dealings that went on in Indonesia, Malaysia or Pakistan are also present in the United States - or at the very least were thought to be present by stock market participants. But this seems very unlikely, and there is no evidence to support this. Timothy Geithner appears to be an honest technocrat, with no interest in doing favors in order to get campaign contributions or financial gain.

Instead, the paper suggests a different hypothesis: "social connections meets the crisis".

Namely, the excess returns of connected firms may be a reflection of the perception of the market (and likely a correct perception) that during turbulent times there will be both heightened policy discretion and even more of the natural tendency of government officials and politicians to rely on the advice of a small network of confidants. For Timothy Geithner this meant relying on, and appointing to powerful positions, financial executives from the firms he was connected to and felt comfortable with. But then, there is no guarantee that these people would not give advice favoring their firms, knowingly or perhaps subconsciously (for example, they may be under the grips of a worldview that increases the perceived importance of their firm's survival for the health of the US economy).

So Larry Summers is probably right that strong US institutions preclude the sort of dealings that went on in Indonesia under Suharto or in Malaysia under Mahathir Mohamad. But this does not mean that connections don't matter or that we should not worry and be vigilant about them, particularly during turbulent times when important decisions have to be made quickly and the usual mechanisms for scrutinizing important policy decisions are weakened or suspended.

|

|

Switchboard | ||||

| Latest | |||||

| Past week | |||||

| Past month | |||||

12/28/2013 | Zerohedge

With equity markets reacting enthusiastically to the Fed's historic policy change announced last week, PIMCO's Mohamed El-Erian notes many have rushed to declare victory. Whether in asserting investor comfort with the policy regime shift or in declaring the definitive end of dependence on quantitative easing ("QE"), they believe that the markets' short-term reaction can indeed be extrapolated into the longer-term. While most Fed officials will welcome the markets' favourable reaction – and especially so after the May-June shock – El-Erian suspects that they are much more cautious. Indeed, in this FT Op-Ed, he lays out four reasons why such caution is understandable.

December 24, 2013 | Econbrowser

Bruce at December 24, 2013 08:58 AM

Speaking of optimism, stock market bullishness is at an extreme, with one bearish sentiment indicator at the lowest level in its history going back 25 years, and at the lowest level since before the 1987 Crash.

http://3.bp.blogspot.com/-T1i9qwajt3U/UpwvpV5mxSI/AAAAAAAASb0/dnUwMhROJn4/s1600/II+Bears.png

http://www.aaii.com/sentimentsurvey

http://blogs.marketwatch.com/thetell/2013/12/12/investor-bullishness-looks-horrifying-according-to-this-chart/

http://greedometer.tumblr.com/post/69625602145/advisors-hit-new-all-time-record-for-bullishness

www.investorschronicle.co.uk/r/.../IC/Assets/.../Sentiment%20Tactics.pdf

http://stockcharts.com/h-sc/ui?s=$CPC&p=D&yr=3&mn=0&dy=0&id=p83181309503

http://stockcharts.com/h-sc/ui?s=$CPCE&p=D&yr=3&mn=0&dy=0&id=p33456923405

Reported earnings and revenues have been flat for over two years, whereas the S&P 500 is up 60-65%, and the P/E has expanded 50%. The only two times in the 142-year history of the S&P 500 when a similar situation occurred with real reported earnings having contracted yoy along the way was in 1986-87 and 1928-29.

Shiller's 10-year average P/E is above the levels historically when secular BULL MARKETS PEAKED (1881, 1929, and 1966-68) and thereafter experienced secular bear markets lasting 15-16 to 20 years. Even a best case scenario implies a ~0% real total 10-year return (before fees and taxes) and cyclical drawdowns of 35-50%+ in the meantime.

The speculative leveraged meltup we have seen since summer-fall 2012 (Fed's "all in") is one for the history books, if not one for which the history books must be rewritten.

http://stockcharts.com/h-sc/ui?s=$NYHILO&p=W&yr=3&mn=0&dy=0&id=p40612045936

http://stockcharts.com/h-sc/ui?s=$NYSI&p=W&yr=3&mn=0&dy=0&id=p80316387638

Fewer stocks are participating in the meltup.

Despite Wall St. (that depends upon inflating bubbles), Fed officials (who work for the TBTE banks and Wall St.), and establishment economists (who serve the TBTE banks, the Fed, and Wall St.) claiming that there are no bubbles anywhere (or they are incapable of seeing, or are not permitted to see, bubbles), there are bubbles ABSOLUTELY EVERYWHERE (because the Fed/TBTE banks intended there to be bubbles):

Stocks

Non-financial corporate debt to GDP

Real estate, including in China, Asian city-states, Canada, Australia, parts of Europe, and the oil emirates

Wealth and income concentration to the top 0.01-0.1% to 1-10%

Equity market cap to GDP

Q ratio

Trophy properties

Farmland

Teslas

IPOs

NYSE margin debt

Stock buybacks

Derivatives to GDP

Total debt to GDP

Art

Vintage cars

Student loans and college tuition

Subprime auto loans

Bank reserves

Bank assets to GDP

Fed balance sheet to GDP

Professional athlete and CEO compensation

Professional sports franchise prices

Tight oil extraction and exportsThere is also a bubble in the number of people claiming that there are no bubbles anywhere.

The bubbles are global and cumulatively far larger than anything experienced in history, even larger in scale globally than in 1999-2000 and 2006-07.

The bubbles, Fed printing, bank cash hoarding, and the resulting EXTREME wealth and income concentration to the top 0.1-1% to 10% is contributing to money velocity plunging and the pricing of Millennials out of the housing market, causing household formation to collapse.

Bears have been in hibernation for so long (as in 1999-2001 and 2007-08) that no one remembers where their caves are or if they are any still alive. The bulls have only themselves left to trample in the next stampede out the exits (when, not if, it occurs) when the TBTE bankers finally decide to pull the plug on (or deflate) the bubble, as they always do.

Reason for optimism or unreasonable optimism by the top 0.01-0.1% to 1%?

Ricardo at December 24, 2013 09:04 AM

A friend sent me the following email.

The inability to see that the current monetary policy does not work in any mechanically rational way is embedded in the culture of the professional and academic community. There is an orthodoxy of thought in all the elite institutions of learning and then in all the government and private applications of that learning. This group think will not change, as Schumpeter explained, until all the old heads of academic economic departments die and a new generation can impose a new orthodoxy. Professors and Central Bankers, who have spent their whole lives writing papers and books from an Aggregate Demand, Quantity Theory of Money point of view, are not capable of mentally confronting the possibility that everything they learned and taught for their whole lives might be wrong.

All the cherished beliefs of a generation that low interest rates stimulate economic activity, that increasing the quantity of money will increase bank loans and inflation, or that the economy's growth can be judged by the level of government spending and consumption, are exposed as intellectually bankrupt myths, are not effective in structuring policy, but the current orthodoxy makes it culturally and professionally impossible to admit that.

Anonymous

"2013Q3 q/q GDP growth has been revised up to 4.1% SAAR; higher consumption is part of the reason."

Yes, higher consumption of healthcare and gasoline.

Or is zerohedge lying again?

XO: My earlier assessment still stands; it's just that there are some reasons to believe the output gap will actually shrink.

Regarding the secular stagnation thesis, well I still wonder whether this is merely a reflection of the lack of political will to sustain government spending and transfers at levels sufficient to push the equilibrium real rate above zero.

Ricardo: Sounds like a poor imitation of Kuhn. Suggest you read his Structure of Scientific Revolutions.

Anonymous: I think zerohedge usually reproduces numbers correctly, but the interpretation is usually -- to me -- a bit iffy. In this case, those nominal numbers seem correct. But the figures that I focused on are real magnitudes. I believe upward revision in real health expenditures did account for an important share of the upward revision in overall consumption.

Ricardo, brilliant. Thank you and thank your friend for his/her clarity in succinctly stating the obvious that obviously cannot be admitted by establishment economists.

The focus on public debt by many academics creates a political debate that obscures the structural drag effects of demographics, "globalization"/"trade" (neo-imperial "trade" regime), PRIVATE debt to wages and GDP, and the resulting end of the reflationary effects on the growth of economic activity when the cumulative imputed compounding interest claims of private debt on wages and GDP are so large as to no longer permit growth of private economic activity.

Neither supply-side nor Keynesian policies can resolve the secular Long Wave debt cycle we currently face after 32 years of falling nominal interest rates and the reflationary effects from increasing debt to wages and GDP. More private debt (debt-money lending/deposits) to wages and GDP to increase supply does not work when there is too much private debt to service.

(Total rentier income [interest, dividends, and capital gains)] received disproportionately by the top 0.1-1%, and total gov't receipts combine for an equivalent of 51% of GDP, 120% of public and private wages, and 145% of private wages. The hyper-financialized economy and local, state, and federal gov't spending at 35% of GDP is resulting in a private sector so burdened by debt service, i.e., "rentier taxes", and gov't taxation that it cannot grow.)

Nor is more public debt to wages and GDP successful in increasing gov't spending to encourage private sector growth when the private sector is burdened with unprecedented debt.

By definition, secular highs in debt to GDP coincide with bubbly asset values to GDP, which in turn is reflected by extreme wealth and income concentration, as the top 1-10% receive 20-50% of income and hold 40-85% of all financial wealth.

The secular debt constraint to real GDP per capita precludes further supply-side expansion of debt, whereas extreme wealth and income concentration and runaway central bank reserve expansion causes asset bubbles, further hoarding at no velocity by the top 1-10%, and plunging money multiplier and velocity.

Historically, high debt/GDP, asset bubbles, and extreme wealth and income concentration are unambiguous indications of sub-optimal incentives, gross price distortions, misallocation of flows, and precursor conditions to decelerating real GDP per capita, financial panics, currency crises, structurally high labor underutilization, social instability, political reaction, and war.

Then add the structural ("permanent"?) drag effects from peak Boomer demographics AND Peak Oil (and net energy per capita), and the effects of debt and inequality are exacerbated (reinforced).

The median household income per capita for the bottom 80-90% of US households is equivalent today to the country GDP per capita in eastern Europe and the wealthier areas of Central and South America. The bottom 50-60% now have household income per capita of Mexico, poorer South and Central Americans, and South Africa.

The typical American male under age 35 receives an income of 60% of that of his generational predecessor in 1970-73 after taxes, inflation, and the effects of higher costs to income for energy, housing, education, and medical services.

The typical college grad today (the 50% who are employed or not underemployed or unemployable) receives a salary similarly adjusted at the equivalent purchasing power of the minimum wage in 1970.

We should thus not be surprised why Millennials are staying home, or moving back in, with Mom and Dad (or Mom or Dad); why household formation is collapsing; why Millennials' headship rate is at a record low; why Millennials are not marrying; and why the birth rate for Caucasian females is converging with that of Europeans, Japanese, Singaporeans, and Taiwanese.

In spite of all of this, or because of it, the stock market is melting up and the top 0.1-1% have virtually disengaged from what remains of the productive sectors of the economy on which the rest of us depend for paid employment and purchasing power.

Now the owners of most of the financial wealth and the means of production of goods and services and the managerial caste that facilitates economic activity intend to accelerate automation of paid employment, expand "trade" via an Asian NAFTA, increase immigration to the US, further increase surveillance-state capabilities, and impose "austerity" on the 50% "takers".

In the context of such conditions, it's no wonder economists spend most of their time focused on attempting to determine how many angels can dance on the head of the proverbial pin. No one gets paid nor receives tenure, a department endowment fund, and a pension by looking out of the window of the ivy-covered tower at the real world and telling his peers to do the same and write about it.

Ricardo

Menzie,

Kuhn focused on the populism of fads overwhelming rational thought such as Keynes' political populist return to mercantilism overwhelming the reason of free market economics.

Zero Hedge

...This section highlights the following potential threats:

• the risk of runs and asset fire sales in repurchase (repo) markets;

• excessive credit risk-taking and weaker underwriting standards;

• exposure to duration risk in the event of a sudden, unanticipated rise in interest rates;

• exposure to shocks from greater risk-taking when volatility is low;

• the risk of impaired trading liquidity;

• spillovers to and from emerging markets;

• operational risk from automated trading systems, including high-frequency trading; and

• unresolved risks associated with uncertainty about the U.S. fiscal outlook.

Zero Hedge

The markets are in a perilous condition today.

We've been noting for months that the markets were displaying signs of a top. Among other items, we recently noted:

- Margin debt (when investors borrow money to buy stocks) has hit new all time highs.

- The number of bearish investors has hit an all time low.

- Market leaders have peaked or are peaking.

- Market breadth (the number of stocks that are rallying) is falling.

- Earnings are falling at key economic bellweathers.

- Stocks have diverged dramatically from earnings and revenues.

Of course, market tops always take longer than one expects. The weakness of the S&P 500 over the last few weeks isn't too promising.

Dec 10, 2013 | naked capitalism

Yves here. While I agree with the general thrust of Ilargi's argument, some small caveats are in order. First, the idea of progress, which is the foundation of the internalized belief in rising incomes and improving living standards, is a child of the Industrial Revolution. And that is despite the fact that the first generation, in fact, nearly two generations of the Industrial Revolution brought worse living standards for ordinary people in England (see here for details).

Second, we've had considerable periods even in the modern era where living standards have stagnated and people didn't have good reason to be optimistic about the future. Consider the 1920s in England and Europe through the reconstruction after World War II. The UK didn't get fully off WWII rationing for well more than a decade after the war ended. The US didn't get whacked by the post Great War malaise, but the period from 1929 to 1945 was no party, and the later half of the 19th century had America going from the Civil War into the Long Depression. So the idea of more or less continuous improvement in living standards is an artifact of the 1980s and 1990s (and a lesser degree the first few years of the new century, although I'd argue that was projecting previous experience onto deteriorating fundamentals) projected backwards (the 1970s were an economically lousy, anxious decade, until you compare it to our current malaise).

By Raúl Ilargi Meijer, editor-in-chief of The Automatic Earth, Cross posted from Automatic Earth

What worries me most about the world today, in the last weeks before Christmas and New Year's Day 2014, is that all the plans we make for our futures and more importantly our children's futures are DOA. This is because nobody has a clue what the future will bring, and that's more than just some general statement. Is the future going to be like the past or present? We really don't know. But we do exclusively plan for such a future. And that's not for a lack of warning signs.

One might argue that in the western world over the past 50 years or so, we've not only gotten what we hoped and planned for, but we've even been to a large extent pleasantly surprised. In a narrow, personal, material sense, at least, we've mostly gotten wealthier. And we think this, in one shape or another, will go on into infinity and beyond. With some ups and downs, but still.

While that may be understandable and relatively easy to explain, given the way our brains are structured, it should also provide food for thought. But because of that same structure it very rarely does.

The only future we allow ourselves to think about and plan for is one in which our economies will grow and our lives will be better (i.e. materially richer) than they are now, and our children's will be even better than ours. If that doesn't come to be, we will be lost. Completely lost. And so will our children.

The ability of the common (wo)man to think about the consequences of a future that doesn't include perpetual growth and perpetually improving lives (whatever that may mean), is taken away from her/him on a daily basis by ruling politicians and "successful" businessmen and experts, as well as the media that convey their messages. It's all the same one-dimensional message all the time, even though we may allow for a distinction between on the one hand proposals, and their authors, that are false flags, in that their true goal is not what is pretended, and on the other hand ones that mean well but accomplish the same goals, just unintended.

This all leads to a nearly complete disconnect from reality, and that is going to hurt us even more that reality itself.

We extrapolate the things we prefer to focus on in today's world, with our brains geared for optimism, into our expectations for the future. But what we prefer to focus on is, by definition, just an illusion, or at best a partial reality. We don't KNOW that there will be continuing economic growth, or continuing sufficient energy supplies, or continuing plenty food. Still, it's all we plan for. Not every single individual, of course, but by far most of us.

The last generation in the western world old enough to live through WWII fully aware, i.e. the last who knew true hardship – as a group -, is now 75 or older. Everyone younger than 70 or so have lived their entire lives through a time of optimism, growth and prosperity. That this could now be over is therefore something the vast majority of them either fail to recognize or refuse to.

They stick to their acquired possessions and wealth, which they view wholly as entitlements, and fail to see even the risk that they can continue to do so only by preying on their children, their children's children, and the weaker members of the societies they live in. That notion may be tough to understand, even tougher to process mentally, and for that reason provoke a lot of resistance and denial, no doubt about it, but that doesn't make it less true. The more wealth you want to retire with, the less your children and grandchildren will have to retire with, and even to live on prior to retirement. That is because there is a solid chance that the pie is simply no longer getting bigger.

As societies we must find a way to deal with these issues as best we can, or our societies will implode. If trends from the immediate past continue, then, when the entire baby boomer generation has retired, 10-15 years from now, income and wealth disparities between generations will have become so extreme that younger people will simply no longer accept the situation.

That is what should arguably be the number one theme in all of our planning and deliberations. It is not; indeed, there is nobody at all who talks about it in anything resembling a realistic sense. Every single proposal to deal with our weakened economies, whether they address housing markets, budget deficits, overall federal and personal debt, or pensions systems, is geared towards the same idea: a return to growth. It doesn't seem to matter how real or likely it is, we all simply accept it as a given: there will be growth. It is as close to a religion as most of us get.

And while it may be true that in finance and politics the arsonists are running the fire station and the lunatics the asylum, we too are arsonists and loonies as long as we have eyes for growth only. That doesn't mean we should let Jamie Dimon and his ilk continue what they do with impunity, it means that dealing with them will not solve the bigger issue: our own illusions and expectations.

We allow the decisions for our future to be made by those people who have the present system to thank for their leading positions in our societies, and we should really not expect them to bite the hand that has fed them their positions. But that does mean that we, and our children, are not being prepared for the future; we're only being prepared, through media and education systems, for a sequel of the past, or at best the present. That might work if the future were just an extrapolation of the past, but not if it's substantially different.

If there is less wealth to go around, much less wealth, in the future, what do we do? How do we, and how do our children, organize our societies, our private lives, and our dealings with other societies? Whom amongst us is prepared to deal with a situation like that? Whom amongst our children is today being educated to deal with it? The answer to either question is never absolute zero, but it certainly does approach it.

Obviously, you may argue that we don't know either that the future will be so different from the past. But that is only as true as the fact that neither can we be sure that it will not. So why do we base our entire projections of the future on just one side of the coin, the idea that we will have more of the same – and then some more -, without giving any thought to what will be needed when more of the same will not be available? That looks a lot like the "everything on red" behavioral pattern of a gambling addict. But who amongst us is ready to admit they're gambling with their children's future?

I see the future as completely different than a mere continuation from the 20th century past and the 21st century present. I even see the latter as very different from the former, since all we've really done in the new millennium is seek ways to hide our debts instead of restructuring them. You can throw a few thousand people out of their homes, but if you label the by far biggest debtors, the banks, as too big to fail, and hence untouchable, nothing significant is restructured. But that doesn't mean it's going to go away by itself, the by far biggest debt in the history of mankind. At some point it must hit us in the form of a massive steamroller of dissolving and disappearing credit. In a world that can't function without it.

And if we refuse to consider even the possibility that the debt will crush us under its immense weight, and profoundly change our societies when it does, then we will be left unprepared. And lost. That should perhaps scare us into action, not denial. Denial simply doesn't seem very useful. Is there a risk that business as usual will no longer be available? Yes, and that risk is considerable. But we plan our futures as if it's non-existent. That is a huge gamble. Not to mention the worst possible kind of risk assessment.

The best, or most, that people seem to be able to think of doing, even if they feel queasy about their economic prospects, is to stuff as much manna as they can into their pockets. That is the sort of approach that may have worked in the past, but it offers no guarantees for the future. It's just another gamble.

We love to tell ourselves how smart we are. It's time we walk that talk.

Read more at http://www.nakedcapitalism.com/2013/12/ilargi-all-the-plans-we-make-for-our-futures-are-delusions.html#uKUR4M87ZGp3Z20g.99

Zero Hedge

Submitted by Adam Taggart of Peak Prosperity,Gail Tverberg, is a professional actuary who applies classic risk assessment procedures to global resources: studying issues such as oil & natural gas depletion, water shortages, climate change, etc. She is widely known in the Peak Cheap Oil space for her reports issued across energy websites over the years under the penname "GailTheActuary".

In this week's podcast, Chris asks Gail to assess the merits of the shale oil "revolution". Does it usher in a new Golden Age of American oil independence?

With her actuarial eyeshade firmly in place, Gail quickly begins discounting the underlying economics behind the shale model:

We have to ask: At what price is the oil available? Is this shale oil available because prices are high and in fact, because interest rates are low, as well? Or is it available if it were cheap oil with interest rates at more normal levels?

I think what we have is a very peculiar situation where it is available ,but it is available only because of this peculiar financial situation we are in right now with very high oil prices and very low interest rates.

...

The shale oil plays are going to be probably much less than a 10-year flash in the pan. They are very dependent on a lot of different things, including low interest rates and the ability to keep borrowing - which could turn around very quickly. Lower oil prices would tend to do the same thing. But even if you hypothesize that we can keep the low interest rates and that the oil price will stay up there, under the best of circumstances, the Barnett data says they probably will not go for very long.

You know, when you take how long the payout really is on those wells, I think the companies drilling these plays have been very optimistic as to how long those wells are going to be economic. There was a recent study done saying just that: 10 years or 5 years; but certainly not 40 years.

And so these companies put together optimistic financial statements that have the benefit of these extremely low interest rates. They keep adding debt onto debt onto debt. How long can they continue to get more debt to finance this whole operation? It's not a model that anybody who is very sensible would follow.

Similar to many energy experts Chris has interviewed prior, Gail looks at the math and concludes that humans (especially those in the West) have been living on an energy subsidy that is beginning to run out. We have been living outside of our natural budget, and will be forced to live within what remains going forward. As a result, she expect great changes in store for the next several decades: socially, politically and lifestyle-wise.

Click the play button below to listen to Chris's interview with Gail Tverberg (38m:07s):

Zero Hedge / The Burning Platform blog,

They say those who forget the lessons of history are doomed to repeat them.

As a student of market history, I've seen that maxim made true time and again. The cycle swings fear back to greed. The overcautious become the overzealous. And at the top, the story is always the same: Too much credit, too much speculation, the suspension of disbelief, and the spread of the idea that this time is different.

It doesn't matter whether it was the expansion of railroads heading into the crash of 1893 or the excitement over the consolidation of the steel industry in 1901 or the mixing of speculation and banking heading into 1907. Or whether it involves an epic expansion of mortgage credit, IPO activity, or central-bank stimulus. What can't continue forever ultimately won't.

The weaknesses of the human heart and mind means the swings will always exist. Our rudimentary understanding of the forces of economics, which in turn, reflect ultimately reflect the fallacies of people making investing, purchasing, and saving decisions, means policymakers will never defeat the vagaries of the business cycle.

So no, this time isn't different. The specifics may have changed, but the themes remain the same.

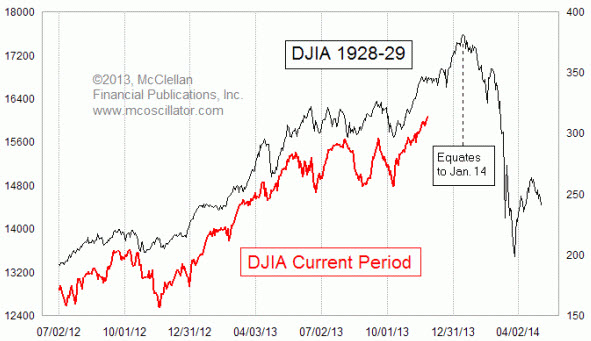

In fact, the stock market is right now tracing out a pattern eerily similar to the lead up to the infamous 1929 market crash. The pattern, illustrated by Tom McClellan of the McClellan Market Report, and brought to his attention by well-known chart diviner Tom Demark, is shown below.

Excuse me for throwing some cold water on the fever dream Wall Street has descended into over the last few months, an apparent climax that has bullish sentiment at record highs, margin debt at record highs, bears capitulating left and right, and a market that is increasingly dependent on brokerage credit, Federal Reserve stimulus, and a fantasy that corporate profitability will never again come under pressure.

On a pure price-analogue basis, it's time to start worrying.

Fundamentally, it's time to start worrying too. With GDP growth petering out (Macroeconomic Advisors is projecting fourth-quarter growth of just 1.2%), Americans abandoning the labor force at a frightening pace, businesses still withholding capital spending, and personal-consumption expenditures growing at levels associated with recent recessions, we've past the point of diminishing marginal returns to the Fed's cheap-money morphine.

All we're doing now is pushing on the proverbial string. Trillions in unused bank reserves are piling up. The housing market has stalled after the "taper tantrum" earlier this year caused mortgage rates to shoot from 3.4% to 4.6% between May and August. The Treasury market is getting distorted as the Fed effectively monetizes a growing share of the national debt. Emerging-market economies are increasingly vulnerable to a currency crisis once the taper finally starts.

The Fed knows it. But they're trapped between these risks and giving the market - the one bright spot in the post-2009 recovery - serious liquidity withdrawals.

But the specifics of the run up to the 1929 crash provide true bone-chilling context for what's happening now.

The Bernanke-led Fed's enthusiasm for avoiding the mistakes that worsened the Great Depression-- a mistimed tightening of monetary conditions - has led him to repeat the mistakes that caused it in the first place: Namely, continuing to lower interest rates via Treasury bond purchases well into an economic expansion and bull market justified by low-to-no inflation.

(Side note here: As economist Murray Rothbard of the Austrian School wrote in America's Great Depression, prices dropped then, as now, because of gains in productivity and efficiency.)

Here's the kicker: The Fed (mainly the New York Fed under Benjamin Strong) was knee deep in quantitative easing in the late 1920s, expanding the money supply and lowering interest rates via direct bond purchases. Wall Street then, as now, was euphoric.

It ended badly.

Fed policymakers felt like heroes as they violated that central tenant of central banking as outlined in 1873 by Economist editor Walter Bagehot in his famous Lombard Street: That they should lend freely to solvent banks, at a punitive interest rate in exchange for good quality collateral. Central-bank stimulus should only be a stopgap measure used to stem panics, a lender of last resort; not act as a vehicle of economic deliverance via the printing press.

It's being violated again now as the mistakes of history are repeated once more. Bernanke will be around to see the results of his mistakes and his misguided justification that quantitative easing is working because stock prices are higher, ignoring evidence that the "wealth effect" isn't working.

Strong died in 1928, missing the hangover his obsession with low interest rates and credit expansion caused after bragging, in 1927, that his policies would give "a little coup de whisky to the stock market."

The level of governmental influence in the financial markets is different today than it was during 1929 – it's *much* greater now. Therefore, I'm thinking the USG will probably do a significant amount of meddling in the future to prevent a crash like 1929. (It probably already has.) I agree that a crash will eventually hit, but this time it will likely include a more sudden drop than in 1929, because the upcoming crash will signal that the USG has lost control, and electronic trading systems will quickly reflect reality. The only way there will be a "relatively slow" crash like 1929, is if the USG decides to purposely orchestrate it.

CounterPunch

So, let's recap: The Fed has managed to spark another surge in risky lending (that "exceeds precrisis levels") that threatens to blow up in investors faces leaving them less prepared for retirement than they are today.

Check.

And there's more. Take a look at the recent stock buyback frenzy, which is where companies buy their own stock to goose the price instead of investing in plants, equipment, hiring, or any other type of useful, productive activity. This is from Bloomberg:

"Multiple expansion through share buybacks have been driving indeed the stock market higher greater than earnings have. …. Buybacks rose by 18% Quarter-over-quarter to $118 billion in 2013, up 11% year-over-year to $218 billion." (Bloomberg)

Even so, Greenspan sees no bubble. Stock prices are based on good old fundamentals, like earnings. What could be more fundamental than earnings, right?

Take a look at this from the Testosterone Pit:

"Corporate earnings will grow this year at their lowest level since 2009. Revenue growth at public companies is almost non-existent. Companies are buying back stock at a record pace to boost per-share earnings." ("What Really Bothers Me About this Stock Market", Michael Lombardi, Testosterone Pit)

Huh? So earnings aren't so hot either?

Apparently not. And that means the fundamentals are actually weak, which makes sense since the economy is in the crapper.

Then we ARE in a bubble, after all?

Yep. And when it bursts it's going to cost a lot of people a lot of money. Just like last time.

Former Idealist:

Don't expect any negative numbers until after Christmas.

These psycho paths are printing their freaking asses off and yet this sucker is still sinking....blub blub blub.

Have a nice holiday, suckers!

KarmaPolice wrote on Fri, 12/6/2013 - 7:25 am (in reply to...)

Former Idealist wrote:

Don't expect any negative numbers until after Christmas.

These psycho paths are printing their freaking asses off and yet this sucker is still sinking....blub blub blub.

Have a nice holiday, suckers!Former Idealist wrote on Wed, 10/9/2013 - 7:58 am

Can't believe the amount of time I wasted reading this shitty blog.

ta taSuckers...indeed!

"Many thousands are in want of common necessaries; hundreds of thousands are in want of common comforts, sir."

"Are there no prisons?"

"Plenty of prisons."

"And the workhouses." demanded Scrooge. "Are they still in operation?"

"Both very busy, sir."

"Those who are badly off must go there."

"Many can't go there; and many would rather die."

"If they would rather die," said Scrooge, "they had better do it, and decrease the surplus population."

While it may appear at first glance that the first chart below shows just one data series, what we have shown are two data sets: one presents, on an inverted axis, the Civilian Employment-to-Population rate, which unlike the unemployment rate as a fraction of the labor force (most recently printing at just 7%), has barely budged since the Lehman collapse. The other data set shows what an implied unemployment rate as calculated by Zero Hedge would be assuming a long-term average of 65.8% worker labor participation rate.

As we reported earlier, according to the BLS this number most recently was 63.0%: a 20 bps rebound from the 35 year low posted in October, but still woefully wrong. The chart shows much more accurately what the real unemployment rate would be when looking at the overall noninstitutional population instead of the ever rising amount of Americans who for one reason or another are not in the labor force.

... ... ...

In short: applying a realistic labor force participation rate to the unemployment rate series, shows that the real US unemployment rate is now 11.5%, a 4.5% difference from the reported number, and the second highest ever, only better compared to October's 4.7%.

Of course, don't inform the Fed of this discrepancy: if aware, the Fed's monetary mandarins would likely never taper. Then again, if indeed the Fed never does taper as many suggest (since it is the flow, not the stock), we will know just which series of unemployment data the Fed is looking at.

hedgeless_horseman

Chocolate rations have been increased to 20 grams.

prains

....from 30 grams

It is well-known that who you know and who you are connected to matters greatly for your business success in many countries. This is nicely documented in several papers that show how connections to powerful politicians have a huge value in countries with weak institutions.

For example, in a famous paper Ray Fisman used an event study methodology exploiting rumors about the health of the Indonesian dictator President Suharto to show how close connections to Suharto were greatly valuable: these adverse news reduce the stock market value of the firms connected to him.

Similar results were found, among other places, in Malaysia by Simon Johnson and Todd Mitton and in Pakistan by Asim Khwaja and Atif Mian.

But the consensus view has been that such connections don't matter in countries with strong institutions such as the United States.

In fact, Larry Summers used this as the basis for his argument for why the response to financial crises should be different in the United States in his Ely Lecture to the American Economic Association: strong US institutions imply that policies that should not be tried in Indonesia or Malaysia because of concerns about cronyism and corruption could be adopted with little worry in the United States.

This view was supported by work that applied similar methodology to the United States. For example, other work by Ray Fisman, together with co-authors, found that the value of connections to Dick Cheney were small or nonexistent.

So US institutions do seem to work as they are supposed to.

Recent work by Daron, Simon Johnson, Amir Kermani, James Kwak and Todd Mitton finds something quite different, however.

Focusing on the announcement of Timothy Geithner as President-elect Obama's nominee for Treasury Secretary in November 2008, they report robust and large returns to financial firms with connections to Geithner. Connections here are defined either from Timothy Geithner's meetings with financial firm executives during the previous two years when he was the President of the Federal Reserve Bank of New York, or from his overlap on non-profit boards with these executives. What's going on?

One possibility is that this just reflects the fact that firms that had such connections are also those that would have actually benefited from the safe pair of hands that Timothy Geithner would bring to the job of Treasury Secretary. Though plausible, this explanation does not receive any support from the data: controls for characteristics that could capture such benefits do not change the results, and in fact the results hold when comparing firms of very similar size, profitability and leverage, and similar risk and stock market return profiles.

Another possibility is that the same sort of shady dealings that went on in Indonesia, Malaysia or Pakistan are also present in the United States - or at the very least were thought to be present by stock market participants. But this seems very unlikely, and there is no evidence to support this. Timothy Geithner appears to be an honest technocrat, with no interest in doing favors in order to get campaign contributions or financial gain.

Instead, the paper suggests a different hypothesis: "social connections meets the crisis".

Namely, the excess returns of connected firms may be a reflection of the perception of the market (and likely a correct perception) that during turbulent times there will be both heightened policy discretion and even more of the natural tendency of government officials and politicians to rely on the advice of a small network of confidants. For Timothy Geithner this meant relying on, and appointing to powerful positions, financial executives from the firms he was connected to and felt comfortable with. But then, there is no guarantee that these people would not give advice favoring their firms, knowingly or perhaps subconsciously (for example, they may be under the grips of a worldview that increases the perceived importance of their firm's survival for the health of the US economy).

So Larry Summers is probably right that strong US institutions preclude the sort of dealings that went on in Indonesia under Suharto or in Malaysia under Mahathir Mohamad. But this does not mean that connections don't matter or that we should not worry and be vigilant about them, particularly during turbulent times when important decisions have to be made quickly and the usual mechanisms for scrutinizing important policy decisions are weakened or suspended.

Society

Groupthink : Two Party System as Polyarchy : Corruption of Regulators : Bureaucracies : Understanding Micromanagers and Control Freaks : Toxic Managers : Harvard Mafia : Diplomatic Communication : Surviving a Bad Performance Review : Insufficient Retirement Funds as Immanent Problem of Neoliberal Regime : PseudoScience : Who Rules America : Neoliberalism : The Iron Law of Oligarchy : Libertarian Philosophy

Quotes

War and Peace : Skeptical Finance : John Kenneth Galbraith :Talleyrand : Oscar Wilde : Otto Von Bismarck : Keynes : George Carlin : Skeptics : Propaganda : SE quotes : Language Design and Programming Quotes : Random IT-related quotes : Somerset Maugham : Marcus Aurelius : Kurt Vonnegut : Eric Hoffer : Winston Churchill : Napoleon Bonaparte : Ambrose Bierce : Bernard Shaw : Mark Twain Quotes

Bulletin:

Vol 25, No.12 (December, 2013) Rational Fools vs. Efficient Crooks The efficient markets hypothesis : Political Skeptic Bulletin, 2013 : Unemployment Bulletin, 2010 : Vol 23, No.10 (October, 2011) An observation about corporate security departments : Slightly Skeptical Euromaydan Chronicles, June 2014 : Greenspan legacy bulletin, 2008 : Vol 25, No.10 (October, 2013) Cryptolocker Trojan (Win32/Crilock.A) : Vol 25, No.08 (August, 2013) Cloud providers as intelligence collection hubs : Financial Humor Bulletin, 2010 : Inequality Bulletin, 2009 : Financial Humor Bulletin, 2008 : Copyleft Problems Bulletin, 2004 : Financial Humor Bulletin, 2011 : Energy Bulletin, 2010 : Malware Protection Bulletin, 2010 : Vol 26, No.1 (January, 2013) Object-Oriented Cult : Political Skeptic Bulletin, 2011 : Vol 23, No.11 (November, 2011) Softpanorama classification of sysadmin horror stories : Vol 25, No.05 (May, 2013) Corporate bullshit as a communication method : Vol 25, No.06 (June, 2013) A Note on the Relationship of Brooks Law and Conway Law

History:

Fifty glorious years (1950-2000): the triumph of the US computer engineering : Donald Knuth : TAoCP and its Influence of Computer Science : Richard Stallman : Linus Torvalds : Larry Wall : John K. Ousterhout : CTSS : Multix OS Unix History : Unix shell history : VI editor : History of pipes concept : Solaris : MS DOS : Programming Languages History : PL/1 : Simula 67 : C : History of GCC development : Scripting Languages : Perl history : OS History : Mail : DNS : SSH : CPU Instruction Sets : SPARC systems 1987-2006 : Norton Commander : Norton Utilities : Norton Ghost : Frontpage history : Malware Defense History : GNU Screen : OSS early history

Classic books:

The Peter Principle : Parkinson Law : 1984 : The Mythical Man-Month : How to Solve It by George Polya : The Art of Computer Programming : The Elements of Programming Style : The Unix Hater’s Handbook : The Jargon file : The True Believer : Programming Pearls : The Good Soldier Svejk : The Power Elite

Most popular humor pages:

Manifest of the Softpanorama IT Slacker Society : Ten Commandments of the IT Slackers Society : Computer Humor Collection : BSD Logo Story : The Cuckoo's Egg : IT Slang : C++ Humor : ARE YOU A BBS ADDICT? : The Perl Purity Test : Object oriented programmers of all nations : Financial Humor : Financial Humor Bulletin, 2008 : Financial Humor Bulletin, 2010 : The Most Comprehensive Collection of Editor-related Humor : Programming Language Humor : Goldman Sachs related humor : Greenspan humor : C Humor : Scripting Humor : Real Programmers Humor : Web Humor : GPL-related Humor : OFM Humor : Politically Incorrect Humor : IDS Humor : "Linux Sucks" Humor : Russian Musical Humor : Best Russian Programmer Humor : Microsoft plans to buy Catholic Church : Richard Stallman Related Humor : Admin Humor : Perl-related Humor : Linus Torvalds Related humor : PseudoScience Related Humor : Networking Humor : Shell Humor : Financial Humor Bulletin, 2011 : Financial Humor Bulletin, 2012 : Financial Humor Bulletin, 2013 : Java Humor : Software Engineering Humor : Sun Solaris Related Humor : Education Humor : IBM Humor : Assembler-related Humor : VIM Humor : Computer Viruses Humor : Bright tomorrow is rescheduled to a day after tomorrow : Classic Computer Humor

The Last but not Least Technology is dominated by two types of people: those who understand what they do not manage and those who manage what they do not understand ~Archibald Putt. Ph.D

Copyright © 1996-2021 by Softpanorama Society. www.softpanorama.org was initially created as a service to the (now defunct) UN Sustainable Development Networking Programme (SDNP) without any remuneration. This document is an industrial compilation designed and created exclusively for educational use and is distributed under the Softpanorama Content License. Original materials copyright belong to respective owners. Quotes are made for educational purposes only in compliance with the fair use doctrine.

FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to advance understanding of computer science, IT technology, economic, scientific, and social issues. We believe this constitutes a 'fair use' of any such copyrighted material as provided by section 107 of the US Copyright Law according to which such material can be distributed without profit exclusively for research and educational purposes.

This is a Spartan WHYFF (We Help You For Free) site written by people for whom English is not a native language. Grammar and spelling errors should be expected. The site contain some broken links as it develops like a living tree...

|

|

You can use PayPal to to buy a cup of coffee for authors of this site |

Disclaimer:

The statements, views and opinions presented on this web page are those of the author (or referenced source) and are not endorsed by, nor do they necessarily reflect, the opinions of the Softpanorama society. We do not warrant the correctness of the information provided or its fitness for any purpose. The site uses AdSense so you need to be aware of Google privacy policy. You you do not want to be tracked by Google please disable Javascript for this site. This site is perfectly usable without Javascript.

Last modified: March, 12, 2019