|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

|

|

The elder Bush once aptly called "supply side" economics “voodoo economics.” But it's much worse then that. Few people understand that Supply Side Economics is a variant of Generational Theft. The best description of supply side or “trickle down” economics I ever heard was by JK Galbraith:

|

|

“trickle down economics is the idea that if you feed the horse enough oats eventually some will pass through to the road for the sparrows.”

There two main types of people (or more correctly oligarchy stooges pretending to be economics; and stooges is the most polite work I can find -- more proper term would be intellectual prostitutes of financial oligarchy) in this camp:

In a perfect academic world of fairness, honesty and integrity, nobody should resort to calling opponents dishonest. Science is the search for truth and it is easy to chose a wrong road. But "supply-siders" are dishonest in a very exact meaning of this word: they deliberately ignore decades of important economic research because they did not like the fact that conclusions prevent them from getting money from financial oligarchy.

Usually critics of supply-side economics point to the lack of academic economics credentials by movement leaders such as Jude Wanniski and Robert Bartley to imply that the theories were bankrupt. But like in Lysenko case the key here are not economic credentials and level of absurdness of supply economics claims. The movement actually attracted several pretty bright, albeit corrupt people. The key is the usefulness of this pseudoscientific nonsense for the elite as a smoke screen for the brazen attempt of wealth redistribution.

One postulate of supply side economics is the existence of so called Laffer curve:

Laffer is best known for the Laffer curve, a curve illustrating tax elasticity which asserts that in certain situations, a decrease in tax rates could result in an increase in tax revenues. Although he does not claim to have invented this concept (Laffer, 2004), it was popularized with policy-makers following an afternoon meeting with Dick Cheney and Donald Rumsfeld in which he reportedly sketched the curve on a napkin [1] to illustrate his argument (Wanniski, 2005). The term "Laffer curve" was coined by Jude Wanniski (a writer for the Wall Street Journal), who was also present. The basic concept was not new: Laffer himself says he learned it from Ibn Khaldun and John Maynard Keynes.[1]

A simplified view of the theory is that tax revenues would be zero if tax rates were either 0% or 100%, and somewhere in between 0% and 100% is a tax rate which maximizes total revenue. Laffer's innovation was to conjecture that the tax rate that maximizes revenue was at a much lower level than previously believed: so low that current tax rates were above the level where revenue is maximized.

Bottom Line: Supply-side theory is nothing more than a rationale for unchecked greed, propaganda of the law of jungles in pseudoscientific packaging. And people who advocate it are very valuable for financial oligarchy. That's why it is very profitable to be a supply side economist. Intellectual trends, especially those closely related to an ideology, such as economics,are frequently, although not always, rationalizations of attempts by dominant groups to impose their goals on society and extirpate others.

Lee Iococca noted in the early 80's that Reaganomics was "picking our grandchildren's pockets." It is a classic case of generational theft. Initially planned as "gun instead of butter" it changed to "gun, butter and debt" after they encounter resistance in dismantling Social Programs. As one commenter (Erdgeist) to the article by Hale Bonddad Stewart Supply Side Economics and Generational Theft aptly put it:Martin Wolf in his Jul 25, 2010 FT column (The political genius of supply-side economics) noted "The political genius of this idea is evident. Supply-side economics transformed Republicans from a minority party into a majority party":This says it all about the Reagan years -- and the lingering schizophrenia that still lurks in the brains of most Republicans.

"Fiscal policy in the Reagan administration exhibited all the signs of schizophrenia that characterized most of its policies.

An expansionary fiscal policy, led by the militarization of the economy, was not the aim of the administration when it drafted its plan. The increases in national defense spending was supposed to be offset by reductions in the civilian sphere. Congress did not go along with the complete dismantling of the New Deal and the welfare state. Its resistance was bound to lead to trouble, for the administration did not have a mandate to eliminate all the social programs enacted in the past 50 years.

Reagan's victory led the conservatives to labor under the miscomprehension that the public was voting for a complete change in philosophy; what the public voted for was hope--hope that somehow there were easy answers to the economic woes that were besetting the nation. Reagan promised them that, and the voters responded."

Source: The Economy in the Reagan Years: The Economic Consequences of the Reagan Administrations by Anthony S. Campagna (1994).

...My reading of contemporary Republican thinking is that there is no chance of any attempt to arrest adverse long-term fiscal trends should they return to power. Moreover, since the Republicans have no interest in doing anything sensible, the Democrats will gain nothing from trying to do much either. That is the lesson Democrats have to draw from the Clinton era’s successful frugality, which merely gave George W. Bush the opportunity to make massive (irresponsible and unsustainable) tax cuts. In practice, then, nothing will be done. ...

To understand modern Republican thinking on fiscal policy, we need to go back to perhaps the most politically brilliant (albeit economically unconvincing) idea in the history of fiscal policy: “supply-side economics”. Supply-side economics liberated conservatives from any need to insist on fiscal rectitude and balanced budgets. ... It allowed them to promise lower taxes, lower deficits and, in effect, unchanged spending. Why should people not like this combination? Who does not like a free lunch?

How did supply-side economics bring these benefits? First, it allowed conservatives to ignore deficits. They could argue that, whatever the impact of the tax cuts in the short run, they would bring the budget back into balance, in the longer run. Second, the theory gave an economic justification – the argument from incentives - for lowering taxes on politically important supporters. Finally, if deficits did not, in fact, disappear, conservatives could fall back on the “starve the beast” theory: deficits would create a fiscal crisis that would force the government to cut spending and even destroy the hated welfare state.

In this way, the Republicans were transformed from a balanced-budget party to a tax-cutting party. This innovative stance proved highly politically effective...

The ... theory that cuts would pay for themselves has proved altogether wrong. ... Indeed, Greg Mankiw ... has responded to the view that broad-based tax cuts would pay for themselves, as follows: “I did not find such a claim credible, based on the available evidence. I never have, and I still don’t.” Indeed, he has referred to those who believe this as “charlatans and cranks”. ...

So, when Republicans assail the deficits under President Obama, are they to be taken seriously? ...[I]t is not deficits themselves that worry Republicans, but rather how they are caused: deficits caused by tax cuts are fine; but spending increases brought in by Democrats are diabolical, unless on the military. ...

What conclusions should outsiders draw about the likely future of US fiscal policy? First, if Republicans win the mid-terms in November, as seems likely, they are surely going to come up with huge tax cut proposals (probably well beyond extending the already unaffordable Bush-era tax cuts).

Second, the White House will probably veto these cuts, making itself even more politically unpopular.

Third, some additional fiscal stimulus is, in fact, what the US needs, in the short term, even though across-the-board tax cuts are an extremely inefficient way of providing it.

Fourth, the Republican proposals would not, alas, be short term, but dangerously long term, in their impact.

Finally, with one party indifferent to deficits, provided they are brought about by tax cuts, and the other party relatively fiscally responsible (well, everything is relative, after all), but opposed to spending cuts on core programs, US fiscal policy is paralyzed. ...

This is extraordinarily dangerous. The danger does not arise from the fiscal deficits of today, but the attitudes to fiscal policy, over the long run, of one of the two main parties. Those radical conservatives (a small minority, I hope) who want to destroy the credit of the US federal government may succeed. If so, that would be the end of the US era of global dominance. The destruction of fiscal credibility could be the outcome of the policies of the party that considers itself the most patriotic.

In sum, a great deal of trouble lies ahead, for the US and the world.

Where am I wrong, if at all?

The economist John Kenneth Galbraith noted that supply side economics was not a new theory. He wrote, "Mr. David Stockman has said that supply-side economics was merely a cover for the trickle-down approach to economic policy—what an older and less elegant generation called the horse-and-sparrow theory: If you feed the horse enough oats, some will pass through to the road for the sparrows."[39] Galbraith claimed that the horse and sparrow theory was partly to blame for the Panic of 1896.

See Supply-side economics - Wikipedia, the free encyclopedia

Here is a couple of comments from an excellent article by Barry Ritholtz NYT Blaming Bush for the Wrong Things The Big Picture

Bush has created a new hypertext linkage definition of kleptocracy* and massive US financial ponzi scheme to keep the bullshit US economy going where credit must flow like a raging river or America’s house of cards goes bust trumps everything else.

Mission accomplished and BOL to 98 or 99% of Americans for next ? years.

*government by those who seek chiefly status and personal gain at the expense of the governed.

===

As for Clinton, I never saw him as moral, and not even a true progressive. He was/is pure ego with few principles, IMO. As for the rest of the Democrats, many are in the same class as Clinton. In addition, many have been co-opted (like Schumer) by the 28 year long dominance of free-market philosophy; they and Clinton were too weak and too concerned with their own re-elections to stand firmly against that trend.

This situation was very beneficial to "deregulation criminals" like Greenspan

|

|

Switchboard | ||||

| Latest | |||||

| Past week | |||||

| Past month | |||||

May 15, 2020 | www.nakedcapitalism.com

"Lifting all boats" was always a lie. It was simply a way to sell trickle down by claiming that the objectively observable inequality it produced would somehow help everyone, eventually, sort of. There was not and has never been a plan by the Conservative Movement to lift all boats. Only a plan to feign interest in doing so.

Synoia , May 14, 2020 at 11:36 am

The rich were riding on the Boats being lifted by the workers.

orlbucfan , May 14, 2020 at 11:42 am

That pattern has appeared throughout recorded world history. How is it peacefully stopped?

Ed Miller , May 14, 2020 at 7:45 pm

I see the current situation more like the sinking of the Titanic (whether caused by the virus or shady financial dealing, it doesn't matter). The rich passengers get the lifeboats and the rest of the passengers get the ice water. A few survived in the water, so it's time to look to the future. Crony capitalism in a nutshell.

Bsoder , May 14, 2020 at 5:40 pm

Lifting all yachts.

Jul 25, 2010 | blogs.ft.com

The future of fiscal policy was intensely debated in the FT last week. In this Exchange, I want to examine what is going on in the US and, in particular, what is going on inside the Republican party. This matters for the US and, because the US remains the world's most important economy, it also matters greatly for the world.

My reading of contemporary Republican thinking is that there is no chance of any attempt to arrest adverse long-term fiscal trends should they return to power. Moreover, since the Republicans have no interest in doing anything sensible, the Democrats will gain nothing from trying to do much either. That is the lesson Democrats have to draw from the Clinton era's successful frugality, which merely gave George W. Bush the opportunity to make massive (irresponsible and unsustainable) tax cuts. In practice, then, nothing will be done.

Indeed, nothing may be done even if a genuine fiscal crisis were to emerge. According to my friend, Bruce Bartlett , a highly informed, if jaundiced, observer, some "conservatives" (in truth, extreme radicals) think a federal default would be an effective way to bring public spending they detest under control. It should be noted, in passing, that a federal default would surely create the biggest financial crisis in world economic history.

To understand modern Republican thinking on fiscal policy, we need to go back to perhaps the most politically brilliant (albeit economically unconvincing) idea in the history of fiscal policy: "supply-side economics". Supply-side economics liberated conservatives from any need to insist on fiscal rectitude and balanced budgets. Supply-side economics said that one could cut taxes and balance budgets, because incentive effects would generate new activity and so higher revenue.

The political genius of this idea is evident. Supply-side economics transformed Republicans from a minority party into a majority party. It allowed them to promise lower taxes, lower deficits and, in effect, unchanged spending. Why should people not like this combination? Who does not like a free lunch?

How did supply-side economics bring these benefits? First, it allowed conservatives to ignore deficits. They could argue that, whatever the impact of the tax cuts in the short run, they would bring the budget back into balance, in the longer run. Second, the theory gave an economic justification – the argument from incentives - for lowering taxes on politically important supporters. Finally, if deficits did not, in fact, disappear, conservatives could fall back on the "starve the beast" theory: deficits would create a fiscal crisis that would force the government to cut spending and even destroy the hated welfare state.

In this way, the Republicans were transformed from a balanced-budget party to a tax-cutting party. This innovative stance proved highly politically effective, consistently putting the Democrats at a political disadvantage. It also made the Republicans de facto Keynesians in a de facto Keynesian nation. Whatever the rhetoric, I have long considered the US the advanced world's most Keynesian nation – the one in which government (including the Federal Reserve) is most expected to generate healthy demand at all times, largely because jobs are, in the US, the only safety net for those of working age.

True, the theory that cuts would pay for themselves has proved altogether wrong. That this might well be the case was evident: cutting tax rates from, say, 30 per cent to zero would unambiguously reduce revenue to zero. This is not to argue there were no incentive effects. But they were not large enough to offset the fiscal impact of the cuts (see, on this, Wikipedia and a nice chart from Paul Krugman).

Indeed, Greg Mankiw, no less, chairman of the Council of Economic Advisers under George W. Bush, has responded to the view that broad-based tax cuts would pay for themselves, as follows: "I did not find such a claim credible, based on the available evidence. I never have, and I still don't." Indeed, he has referred to those who believe this as " charlatans and cranks ". Those are his words, not mine, though I agree. They apply, in force, to contemporary Republicans, alas,

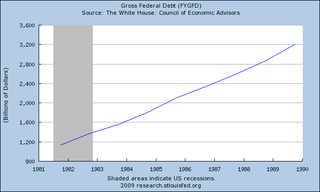

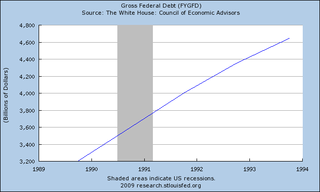

Since the fiscal theory of supply-side economics did not work, the tax-cutting eras of Ronald Reagan and George H. Bush and again of George W. Bush saw very substantial rises in ratios of federal debt to gross domestic product. Under Reagan and the first Bush, the ratio of public debt to GDP went from 33 per cent to 64 per cent. It fell to 57 per cent under Bill Clinton. It then rose to 69 per cent under the second George Bush . Equally, tax cuts in the era of George W. Bush, wars and the economic crisis account for almost all the dire fiscal outlook for the next ten years ( see the Center on Budget and Policy Priorities ).

Today's extremely high deficits are also an inheritance from Bush-era tax-and-spending policies and the financial crisis, also, of course, inherited by the present administration. Thus, according to the International Monetary Fund, the impact of discretionary stimulus on the US fiscal deficit amounts to a cumulative total of 4.7 per cent of GDP in 2009 and 2010, while the cumulative deficit over these years is forecast at 23.5 per cent of GDP . In any case, the stimulus was certainly too small, not too large.

The evidence shows, then, that contemporary conservatives (unlike those of old) simply do not think deficits matter, as former vice-president Richard Cheney is reported to have told former treasury secretary Paul O'Neill . But this is not because the supply-side theory of self-financing tax cuts, on which Reagan era tax cuts were justified, has worked, but despite the fact it has not. The faith has outlived its economic (though not its political) rationale.

So, when Republicans assail the deficits under President Obama , are they to be taken seriously? Yes and no. Yes, they are politically interested in blaming Mr Obama for deficits, since all is viewed fair in love and partisan politics. And yes, they are, indeed, rhetorically opposed to deficits created by extra spending (although that did not prevent them from enacting the unfunded prescription drug benefit, under President Bush). But no, it is not deficits themselves that worry Republicans, but rather how they are caused: deficits caused by tax cuts are fine; but spending increases brought in by Democrats are diabolical, unless on the military.

Indeed, this is precisely what John Kyl (Arizona), a senior Republican senator, has just said:

"[Y]ou should never raise taxes in order to cut taxes. Surely Congress has the authority, and it would be right to -- if we decide we want to cut taxes to spur the economy, not to have to raise taxes in order to offset those costs. You do need to offset the cost of increased spending, and that's what Republicans object to. But you should never have to offset the cost of a deliberate decision to reduce tax rates on Americans"

What conclusions should outsiders draw about the likely future of US fiscal policy?

First, if Republicans win the mid-terms in November, as seems likely, they are surely going to come up with huge tax cut proposals (probably well beyond extending the already unaffordable Bush-era tax cuts).

Second, the White House will probably veto these cuts, making itself even more politically unpopular.

Third, some additional fiscal stimulus is, in fact, what the US needs, in the short term, even though across-the-board tax cuts are an extremely inefficient way of providing it.

Fourth, the Republican proposals would not, alas, be short term, but dangerously long term, in their impact.

Finally, with one party indifferent to deficits, provided they are brought about by tax cuts, and the other party relatively fiscally responsible (well, everything is relative, after all), but opposed to spending cuts on core programmes, US fiscal policy is paralysed. I may think the policies of the UK government dangerously austere, but at least it can act.

This is extraordinarily dangerous. The danger does not arise from the fiscal deficits of today, but the attitudes to fiscal policy, over the long run, of one of the two main parties. Those radical conservatives (a small minority, I hope) who want to destroy the credit of the US federal government may succeed. If so, that would be the end of the US era of global dominance. The destruction of fiscal credibility could be the outcome of the policies of the party that considers itself the most patriotic.

In sum, a great deal of trouble lies ahead, for the US and the world.

Where am I wrong, if at all?

July 25, 2010 4:18pm in Financial crisis , Supply-side economics | 10 comments

Email Share PrintYou need to be signed in to comment. Please sign in or open a free account with FT.com now.

RSS feed

Comments

Open for comments. Click to close Closed. Click to open for commentingSorted by oldest first | Sort by newest first Sorted by newest first | Sort by oldest first

- Report Martin Wolf | July 25 5:04pm | Permalink

| Options

Bruce Bartlett writes "I think my friend Martin is a bit too hard on Reagan, who did try to cut spending and signed 11 major tax increases into law to bring down the deficit. And Bush 41 initiated a budget deal in 1990 that eventually led to budget surpluses. It was Bush 43 and his willing accomplices among the Republicans who controlled Congress that deserve the vast bulk of the blame."This is my response: "Fair comment. But, as you have often noted, his followers have repudiated president Reagan's willingness to raise taxes. Nor are they making any credible commitments to large-scale cuts in public spending. It is also the case that, despite a boom in the 1980s, the end of the Reagan and George H. Bush era saw much higher public debt ratios than the beginning. I think you have to recognise that today's Republicans are Reagan's children and, as is often the case, are more uncompromising than their parents."

- Report ralbin | July 25 6:59pm | Permalink

| Options

Mr. Wolf - Your comment is entirely correct though perhaps incomplete. Implicit, and sometimes explicit, in the supply-side argument was that low taxes wouldn't involve any public sacrifices. The Republicans promised the benefits of the liberal state while arguing that the needed tax revenues wouldn't be needed. This is what made it and continues to make it a successful political strategy. This is an actual Big Lie.Its worth delineating the other Big Lie of Republican political strategy, the the USA is so powerful that it can do anything it wants on the international stage. Add in consistent appeals to racial and religious bigotry (from which the personally decent Mr. Reagan was not immune) and you have almost the whole Republican political strategy of the last 30 years. Very successful and almost all of it based on deception and appeals to the electorate's worst tendencies.

- Report Kent Willard | July 25 7:06pm | Permalink

| Options

Running up the debt in order to default and cut spending is like having a heart attack in order to get serious about diet and exercise. It is crazy, but they will do it, and then blame it on someone else.Any bets on a gov't shutdown attempt next year?

- Report Dana Houle | July 25 7:09pm | Permalink

| Options

I think you're assuming a lot about the results of the November elections that are far from certain. In fact, it's highly, highly unlikely that the Republicans will win the Senate, and not particularly likely they'll win the House. They will certainly pick up seats in the House, maybe a lot, but there are only a handful of Dem-held Senate seats that I would say today are pretty much lost for the Democrats (North Dakota, Arkansas), while there are also up to 8 Republican-held seats that could be in play. Democrats would have to lose 10 seats that they currently hold and not win any seats currently held by Republicans (even though 5 of those are open and Vitter in Louisiana is so scandal-plagued he may not survive). It's just about implausible the Democrats will lose a net of 10 or more seats.Even in the House, Democrats will have to lose almost all the contested seats, at a time when the most recent generic ballot from Gallup shows Democrats nationally with an 8 point advantage and most of the vulnerable Democratic incumbents have huge cash advantages over their Republican challengers.

I agree with your interpretation of the political appeal of supply side economics, but I think you're greatly overestimating the ability of the Republicans to win enough seats in November to fully enact their fiscal will on the White House.

- Report toweypat | July 25 7:42pm | Permalink

| Options

"Second, the White House will probably veto these cuts"I wish I could agree. Given what we have seem from President Obama this past year and a half, I think he is just as likely to go along with them as part of some nebulous plan to angle for concessions from the other side, or simply to burnish his bipartisan credentials.

- Report JoelS | July 25 8:24pm | Permalink

| Options

Thanks for saying out loud what has been apparent: that Republicanism has become fundamentally destructive. I don't think there's any doubt that the empire is coming to an end, as all empires do, with the unwillingness of the populace to bear the costs and burdens. The tax revolt is, at its heart, a cancer destroying American power and prosperity.This is doubly unhealthy because the United States needs a healthy opposition. In its absence, the Democrats are also becoming corrupt. Their electoral appeal has increasingly become: "Vote for us. We're not insane." That's necessary, of course, but hardly sufficient. So we end up with a health care bill with no cost containment, a financial regulatory bill that does not address the speculation and institutional giantism that was at the heart of the collapse, and a stimulus bill half the size that it should have been and heavily tilted against hiring the unemployed in favor of tax cuts. The Republicans would have done worse, but that is small comfort.

Where are you wrong? If anywhere, in having any doubts that we are on the path to destruction, will no reason to think that we will turn back.

- Report Till Schreiber | July 25 9:02pm | Permalink

| Options

A wild card in the events you outline could be the report of the bipartisan commission on reducing the long-term budget deficit. Larry Summers mentioned it in his contribution to the austerity debate. If, and it's a big if, this report is substantive enough, it might provide cover for Republicans, Democrats, and the White House to tackle long-term deficits.In addition, I also feel you are a bit generous in labeling the Democrats relatively fiscally responsible. Certainly, the president's budget had rather high projected deficits over the next decade (and beyond).

Ultimately, according to the CBO a lot comes down to health care costs, particularly Medicare. Reforming Medicare and controlling the explosion of costs currently projected for it is the key. Everything else is secondary.

- Report Edward Hatfield | July 25 9:22pm | Permalink

| Options

At last you have it spot on. There will have to be a crisis because Weston democracies will not vote for wage cuts. May be it could be done if the elite took a big cut first but that will not happen as most of the elite do not see the problem as their fault.You recently replied to one of my emails about thestateBritainis in with the words

"I also don't understand this masochism" Well you surely must now

- Report Barry Thompson | July 25 9:24pm | Permalink

| Options

James Galbraith says you are wrong:"So long as U.S. banks are required to accept U.S. government checks -- which is to say so long as the Republic exists -- then the government can and does spend without borrowing, if it chooses to do so Insolvency, bankruptcy, or even higher real interest rates are not among the actual risks to this system."

The only real risk to the system is inflation. The need for any sovereign government that can issue its own currency to balance its budget is merely a useful fiction, of political importance but not a real economic constraint.

Otherwise, keep up the great work!

- Report Richard W | July 25 9:25pm | Permalink

| Options

' Those radical conservatives (a small minority, I hope) who want to destroy the credit of the US federal government may succeed. If so, that would be the end of the US era of global dominance. The destruction of fiscal credibility could be the outcome of the policies of the party that considers itself the most patriotic. 'That prospect holds no fear for the majority of contemporary Republican thinking in the party and throughout the conservative base. Withdrawal from NATO, UN and the global stage is precisely the plan. The contemporary Republican party is now more than ever aligned with the populist, reactionary and isolationist sentiments of conservative small town America. It will take many years, but I suspect America is on a long slide to an ungovernable failed state and eventual break-up of the union.

Jan 12, 2019 | www.nytimes.com

Socrates Downtown Verona. NJ Jan. 5

To anyone who thinks that the Republican Party knows a thing about economics or business: you're delusional. Republicans know a tremendous amount about greed, theft and selfishness. Arthur Laffer is the idiotic tax-cut patron saint economist of the Grand Old Phonies who helped Ronnie Reagan raid the US Treasury for the uber-wealthy.

George W Bush re-implemented Laffer-economics and drove the nation into a Depression.

Trump and the GOP are in the process of driving America over another bankrupting 0.1% welfare tax-cut cliff -- remember it took Bush-Cheney a good seven years to do it.

And guess who recently helped drive Kansas bankrupt with tax cuts for the rich ?

GOP tax-cut saint Arthur Laffer. He helped former Kansas Gov. Sam Brownback (R) pass tax cuts through the Kansas legislature. In August 2012, Laffer promised a crowd at a small business forum in Kansas that the cuts would produce "enormous prosperity," adding that they'll "make a big difference in a decade." They did make a big difference.

Kansas employment and the Kansas state economy both grew slower than the national rates, and the drastic decline in tax revenue coming into the state's treasury blew a gigantic hole in its budget.

Kansas reversed the destructive tax cuts in order save Kansas. The lesson is plain and simple and happens over and over again. Republicans are economic wrecking balls hellbent on destroying society for corrupt billionaires. D to go forward. R for nationally-assisted suicide.

medium.com

SA is cursed with neo-liberal trickle-down baloney stifling radical economic change Kevin Humphrey, The New Age, Johannesburg, 1 December 2016

South Africa's massive inequalities are abundantly obvious to even the most casual observer. When the ANC won the elections in 1994, it came armed with a left-wing pedigree second to none, having fought a protracted liberation war in alliance with progressive forces which drew in organised labour and civic groupings.

At the dawn of democracy the tight knit tripartite alliance also carried in its wake a patchwork of disparate groupings who, while clearly supportive of efforts to rid the country of apartheid, could best be described as liberal. It was these groupings that first began the clamour of opposition to all left-wing, radical or revolutionary ideas that has by now become the constant backdrop to all conversations about the state of our country, the economy, the education system, the health services, everything. Thus was the new South Africa introduced to its own version of a curse that had befallen all countries that gained independence from oppressors, neo-colonialism.

By the time South Africa was liberated, neo-colonialism, which as always sought to buy off the libera-tors with the political kingdom while keep-ing control of the economic kingdom, had perfected itself into what has become an era where neo-liberalism reigns supreme. But what exactly is neo-liberalism? George Monbiot says: "Neo-liberalism sees competi-tion as the defining characteristic of human relations. It redefines citizens as consumers, whose democratic choices are best exercised by buying and selling, a process that rewards merit and punishes inefficiency. It maintains that 'the market' delivers benefits that could never be achieved by planning."

Never improving

There is consensus between commentators who have studied the effects of neo-liberalism that it has become all pervasive and is the key to ensuring that the rich remain rich, while the poor and the merely well to do continue on a perpetual hamster's wheel, going nowhere and never improving their lot in life while they serve their masters.

Monbiot says of this largely anonymous scourge: "Attempts to limit competition are treated as inimical to liberty. Tax and regulations should be minimised, public services should be privatised. The organisation of labour and collective bargaining by trade unions are portrayed as market distortions that impede the formation of a natural hierarchy of winners and losers. Inequality is recast as virtuous, a reward for utility and a genera-tor of wealth, which trickles down to enrich everyone. Efforts to create a more equal society are both counterproductive and morally corrosive. The market ensures that everyone gets what they deserve."

Nelson Mandela

South Africa's sad slide into neo-liberalism was given impetus at Davos in 1992 where Nelson Mandela had this to say to the assembled super rich: "We visualise a mixed economy, in which the private sector would play a central and critical role to ensure the creation of wealth and jobs. Future economic policy will also have to address such questions as security of investments and the right to repatriate earnings, realistic exchange rates, the rate of inflation and the fiscus."

Further insight into this pivotal moment was provided by Anthony Sampson, Mandela's official biographer who wrote: "It was not until February 1992, when Mandela went to the World Economic Forum in Davos, Switzerland, that he finally turned against nationalisation. He was lionised by the world's bankers and industrialists at lunches and dinners."

This is not to cast any aspersions on Mandela, he had to make these decisions at the time to protect our democratic transition. But these utterances should have been accom-panied by a behind the scenes interrogation of all the ANC's thoughts on how to proceed in terms of the economy delivering socialist orientated solutions without falling into the minefield of neo-liberal traps that lay in wait for our emerging country.

Senior cadres co-opted Unfortunately, history shows that some key senior cadres of the ANC were all too keen to be coopted into the neo-liberal fold and any attempts to put forward radical measures that would bring something fresh to the table to address the massive inequalities of the past were and continue to be kept off the table and we are still endlessly fed the neo-liberal trickle-down baloney.

Now no one dares to express any type of radical approach to our economic woes unless it is some loony populist. Debate around these important issues is largely missing and the level of commentary on all important national questions is shockingly shallow.

Anti-labour, anti-socialist, anti-poor, anti-black The status quo as set by the largely white-owned media revolves around key neo-liberal slogans mas-querading as commentary that is anti-labour, anti-socialist and anti-poor, which sadly translates within our own context as anti-black and therefore repugnantly racist.

We live in a country where the black, over-whelmingly poor majority of our citizens have voted for a much revered liberation movement that is constantly under attack from within and without by people who do not have their best interests at heart and are brilliant at manipulating outcomes to suit themselves on a global scale.

Kevin Humphrey is associate executive editor of The New Age

Sep 27, 2017 | crookedtimber.org

Restating the case against trickle down (updated in response to comments)

by John Quiggin on September 2, 2017 I've just given a couple of talks focusing on inequality, one for the Global Change Institute at UQ, following a presentation by Wayne Swan and the second at a conference organized by the TJ Ryan Foundation (including great talks by Peter Saunders, Sally McManus, and others), where I was responding to a paper by Jim Stanford from the Centre for Future Work. Because I was speaking second in both cases, I didn't prepare a paper or slides, but tailored my talk to complement the one before. That can be a high risk strategy, but in this case, I think it worked very well.

It led me to a new, and I hope improved, statement of the case against 'trickle down' theory. As always, the most important part of a refutation is a clear statement of the theory you propose to refute, so that it can be shown where it falls down. After the talks I wrote this up, and it's over the fold. Comments and constructive criticism much appreciated.

The case against trickle down, restated

The trickle down theory relies on the following claims*

- In the absence of taxes and other government interventions, high market incomes reflect, and elicit, high productivity, investment and effort.

- More effort from highly productive workers and investors increases the productivity of workers in general.

The trickle down argument then starts with the claim that reducing tax on high income earners will lead them to work harder and invest more. Since they are (by claim 1) the most productive members of the community, their efforts will (by claim 2) make everyone else more productive, and will benefit consumers. So, reducing taxes on high income groups will make everyone better off.

Claim 1 is a restatement of the marginal productivity theory which is at the heart of neoclassical economics. In a general equilibrium model of a perfectly competitive economy with full employment, it can be deduced as a theorem. With constant returns to scale,

Claim 2 is generally assumed to be true, although it's not usually spelt out. It is true either if there are external economies of scale such as information externalities (the most productive provide a model for others to copy) or complementarity in production (working with highly productive colleagues and managers makes people in general more productive). With economies of scale, Claim 1 needs to be interpreted carefully, The implication is not that everyone receives a payment equal to their marginal product, but that market incomes are (roughly) proportional to average and marginal productivity.

If Claim 2 doesn't hold then all the benefits of increased effort from highly productive workers and investors is captured by the workers and investors themselves. This means that the there is no 'trickle down' except through the tax system. The policy implication is that tax rates for high income earners should be set at or near the top of the 'Laffer curve' where revenue is maximized, estimated by Piketty, Saez and Stantcheva at around 80 per cent.

The neoclassical model that gives rise to Claim 1 has never been a fully accurate representation of the economy. But it is even less accurate now than in the past. The crucial recent developments, likely to continue in the absence of radical policy change, are:

- (i) wage stagnation, with the result that the link between productivity and incomes has been broken for workers as a group

- (ii) the increasing proportion of profits derived from monopoly power and financial sector speculation

- (iii) the rise of the information economy. Information is a public good, so imposing explicit prices on information or bundling it with undesired advertising reduces its social value

- (iv) the likely emergence of a patrimonial society in which high incomes are derived from inherited wealth

These developments mean that cuts in the top rate of income tax will primarily reward ownership of capital, unproductive activity, or luck in choosing ones parents, rather than increasing productivity. They also undermine the second proposition underlying trickle down theory. The pursuit of monopoly profits ('rent-seeking' in the jargon of free-market economics) reduces rather than increases the productivity of the economy as a whole.

That's the theory. The empirical evidence, which was in dispute for a long time, is now clear-cut, at least for the United States. Decades of pro-rich policies have, unsurprisingly, made the rich much richer. Contrary to the predictions trickle down theory, the result has been to reduce, rather than increase, the productivity and dynamism of the economy. The combination of slower growth and increased inequality implies, as a matter of arithmetic, that the majority of the population must be worse off.

*There are some other versions of trickle down that can be dismissed more easily. Most notably, there's the idea that the spending of the rich will create employment. That's true, but more employment would be generated if income were redistributed to the poor, who save less of their income and consume more.

BruceJ 09.02.17 at 1:51 am ( 1 )

mclaren 09.02.17 at 2:02 am ( 3 )Claim 1 is a restatement of the marginal productivity theory which is at the heart of neoclassical economics. In a general equilibrium model of a perfectly competitive economy with full employment, it can be deduced as a theorem.

Honestly, this makes 'neoclassical economics' sound suspiciously like yet another perpetual motion scheme.

We can also cite the exponential growth of share buybacks to boost stock prices and thus enrich CEOs + corporate officials with stock options. This now seems to be the main corporate use for profits, as opposed to investment. This trend would seem to short-circuit the whole argument in claim 1, since if businesses use profits to buy back shares instead of investing to increase productivity, claim 1 is entirely moot.Wally 09.02.17 at 2:13 am ( 4 )See "Profits Without Prosperity" by William Lazonick, Harvard Business Review, 2014.

"2. More effort from highly productive workers and investors increases the productivity of workers in general."OldClark 09.02.17 at 2:48 am ( 5 )What, people claim this? With a straight face? I work in a factory. I'd say the opposite is true, the harder I work, the more everyone else slacks off!

Tinkle down theory: We must coddle the rich, because if we don't, then they will have a sad and won't work hard. But the poor? Anything they get makes them work less hard.Ian Maitland 09.02.17 at 2:48 amBut maybe: Tax the rich harder and they work harder, because they still want more, more, more. And the poor? Anything they get empowers them, and further motivates them to escape poverty.

John Quiggin 09.02.17 at 3:53 am ( 7 )"The empirical evidence [against trickle down theory], which was in dispute for a long time, is now clear-cut, at least for the United States."I wonder if the clause tacked on to that sentence -- "at least for the United States" -- isn't a dead giveway?

What about the rest of the world? True, globalization enriched corporations and created Third World billionaires, but the most striking development of the two or three decades up to 2007 was the transformation of the situation and prospects of the world's poor. 2015 economics Nobelist Angus Deaton has said: "Life is better now than at almost any time in history. More people are richer and fewer people live in dire poverty. Lives are longer and parents no longer routinely watch a quarter of their children die."

Between 1970 and 2006, the percentage of the world population in poverty has fallen by 80 percent from 27% to 5%. The corresponding total number of poor has fallen from 403 million in 1970 to 152 million in 2006. At the same time, various measures of global inequality have declined substantially and measures of global welfare increased by somewhere between 128% and 145% (Pinkovskiy.& Sala-i-Martin 2009; see also Kinley, 2009: 14-15).

It is amazing how we take for granted what in retrospect will be seen as a golden age. How quickly we have forgotten how, before globalization, much of the Third World had been written off by experts. In the 1960s and 1970s, for example, Peter Singer placed Bangladesh in the "hopeless" category. "We have no obligation to assist countries whose government make our aid ineffective," Singer wrote. Paul Ehrlich wrote in The Population Bomb that, "India couldn't possibly feed two hundred million more people by 1980." He endorsed a system of "triage" that would end food aid to "hopeless" countries such as India and Egypt. (India has gone from being an economic basket case to a bread basket). Garrett Hardin used the lifeboat earth metaphor to argue against helping the world's poorest. That help would lead to unsustainable population growth that would capsize the lifeboat, so they had to be thrown overboard.

Globalization was mostly about the lifting of barriers to trade and investment and liberalizing domestic economies. The era has been called "the age of Milton Friedman" by Andrei Shleifer (2009) because it marked a stride toward a global free market. The miracle of globalization was, accidentally or on purpose, the result of the unleashing of market forces. Instead of planners, foreign aid, high tariffs and import substitution, it was greater market openness that drove this transformation.

I don't know if this qualifies as "trickle down," but I think we should all give thanks for what has been accomplished. Sadly, the Great Recession and the populist revolt have put the brakes on the process.

@6 I've responded to this point before, as follows:Alex SL 09.02.17 at 4:43 am ( 8 )In the wake of the GFC, some advocates of economic liberalism have sought to shift the ground of debate, arguing that, whatever the impact of financial globalisation on developed countries, it has been hugely beneficial for India and China which, between them, account for a third of the world's population.

There are all sorts of problems with this argument.The relatively disappointing economic performance of China and India in the postwar decades certainly provides strong grounds for criticising the economic policies of Mao Zedong and Nehru. But even in the days when some observers saw these policies as providing an appropriate development path for the countries that adopted them, no one seriously proposed their adoption by developed countries. And as more attention has been focused on the irrational aspects of these policies (such as the Great Leap Forward, in which people were made to melt down their cooking pots to provide scrap for backyard smelters, which presumably produced new cooking pots, or the dozens of licenses required to undertake the simplest economic activity in India) it has become easier to understand why their removal or relaxation

At the same time, neither of these rapidly-growing economies come anywhere near meeting the standard description of a free-market economy. China still has a huge state-owned enterprise sector, a tightly restricted financial system and a closely managed exchange rate. India began its growth spurt before the main period of market liberalisation and also retains a large state sector. In both countries, as earlier in Japan and South-East Asia, the state has played a major role in promoting particular directions of development.

In summary, while the development success stories of China and India, and, before them of Japan and the East Asian tigers, may have some useful lessons for countries struggling to escape the poverty trap, they can tell us nothing about the relative merits of economic liberalism and social democracy.

I am not an economist (is IANAE a thing?), but it always seemed to me that the two main problems with trickle-down are the second to last paragraph – empirical disproof – and the idea that, say, lowering taxes from 35% to 25% is some kind of huge incentive that will make people who are affected by that change work harder. I do not find it a priori plausible that somebody would ever say:Matt 09.02.17 at 5:56 am ( 9 )"Hey, if I work harder to earn another $10,000 I will only actually get to take $6,500 home. If that is the case, then I will not work harder and rather lose out on the $6,500, even if I could really do with another $6,500. So there. But if you lower the tax rate so that I get to keep $7,500, now we are talking! Those 10% are so much more relevant than the other 65%." (Add zeroes at the end of those numbers as required.)

This is just not a reasoning that will ever make sense or occur to anybody in real life, i.e. outside of a libertarian think tank, unless we are indeed talking a tax rate of 95%.

I do not find it a priori plausible that somebody would ever say:Bill 09.02.17 at 9:47 am ("Hey, if I work harder to earn another $10,000 I will only actually get to take $6,500 home. If that is the case, then I will not work harder and rather lose out on the $6,500, even if I could really do with another $6,500. So there. But if you lower the tax rate so that I get to keep $7,500, now we are talking! Those 10% are so much more relevant than the other 65%."

for what it's worth, I have thought things at least very similar to that several times, and even acted on them, when, for example, I was already teaching several classes, and I was asked if I'd like to teach one more. At that point, teaching one more would start to have significant impact on my quality of life and ability to do writing. I'd be unhappy. But, I could use the extra money. But each dollar cut off made a bit difference, considering that it would actually be a pretty significant impact on my happiness at that point to teach another class. Even if I could use the money, it had to be a fair amount of money before I'd take the class on. Now, I don't mean to draw any sort of general conclusion from this, or to suggest that it's a problem with the post, or to suggest that my situation suggests anything important about tax policy or whatnot. But, that things like this happens seems pretty clear to me, because they have happened to me.

The two propositions seem at odds. If people earn their marginal productivity (by #1), there should not be the externalities (in #2). The presence of the externalities suggests that incomes are not set according to marginal contributions to the economy. In turn, that calls into question the general equilibrium model.ccc 09.02.17 at 9:54 am ( 11 )"So, reducing taxes on high income groups will make everyone better off."nastywoman 09.02.17 at 10:08 am ( 12 )Even if 1 and 2 hold that "better off" conclusion still does not follow. Or at minimum "better off" must be defined and qualified. How well off social animals like us are arguably depend on both absolute and relative factors. Even if 1 and 2 raise the economic floor for literally everyone they may also increase economic inequality, which can cause health worsening (spirit level type argument) and worse equality of opportunity for the children of those not earning most. Seeing one's child strive but not succeed because of a system of economic inequality is arguably a "being worse off" factor.

"Trickle down" never works if you don't have Rich dudes who don't trickle down enough. But it kind of works if you have a German Mittelstands-dude who has such a high social conscious with an empathetic responsibility for his workers and his community that he pays his workers excellent – insists on NOT firing -(or outsourcing) them and is in economical crisis even willing to sacrifice his own well being for the well being of his community and workers.Collin Street 09.02.17 at 11:21 am ( 13 )And this simple Kindergarten-wisdom (philosophy?) just doesn't apply (anymore?) in THE homeland – even supposedly – and to a certain extend applied when a dude called Ford made sure that his workers could afford the cars they build.

Tim Worstall 09.02.17 at 11:23 am ( 14 )"Trickle down" never works if you don't have Rich dudes who don't trickle down enough.It's better than that: even if trickle-down actually works the way it's supposed to the way it's supposed to work it'll make problems of equality worse, not better, long-term. See, you're giving the money to people with the expectation that they will use it to make "profitable investments". But a profitable investment -- definitionally -- returns more money to its maker than they spend: the result of "trickle down" is profitable investments made by the currently-rich that make them even richer .

"Claim 2 is generally assumed to be true, although it's not usually spelt out. It is true either if there are information externalities (the most productive provide a model for others to copy) or complementarily in production (working with highly productive colleagues and managers makes people in general more productive).bob mcmanus 09.02.17 at 12:03 pm ( 15 )If Claim 2 doesn't hold then all the benefits of increased effort from highly productive workers and investors is captured by the workers and investors themselves. This means that the there is no 'trickle down' except through the tax system. The policy implication is that tax rates for high income earners should be set at or near the top of the 'Laffer curve' where revenue is maximized, estimated by Piketty, Saez and Stantcheva at around 80 per cent."

Well, no, not really. Imagine, just imagine for a moment, that the harder work and greater investment in pursuit of those higher incomes leads to something like that new leukemia drug just approved. $500k a treatment today, that being cheaper than the other treatment, bone marrow transplant. And in 10 or so years time the patent expires and it drops in price again. No, this is not an argument that drug patents are super, rather, do we think that people are incentivised to create new things by the prospects of gaining gazillions?

Are those 600 Americans likely to get this treatment each year made richer by its existence?

We're made richer by being able to consume the greater production of those more highly motivated high productivity people, aren't we?

As to the 80% peak, that suffers from the same problem that the very similar Diamond and Saez one does. It assumes that we've already closed off all avenues of avoidance (D&S using "allowances" to mean this). A residence based tax system, rather than a passport one, is just such an allowance. For you can avoid by leaving the country and we've even got a name for when this happened, the brain drain.

Further, the Staggers gets the NI situation wrong. D&S, certainly, talk about "taxes on income", not "income taxes". They specifically include employer paid taxes on employment income. Meaning adding employers' NI for the UK, not just the residual 2% employees'. At which point, with allowances like residence based, D&S give us something like 54% as the Peak. Or, given NI, somewhere around where we are with income tax alone right now, 45% or so.

IANAE, and no longer reading as much economics as I used to, and this may belong to JQ's last paragraph about trivial trickle-down theories, but I was inspired to visit the Marx-Kalecki three-sector model. (Investment goods, wage goods, luxury goods/capitalist consumption.) Which as usual, approaches the problem from the production side. "Trickle-down" in this case depends on how capitalist spend their increased income, whether on investment or luxury goods.bob mcmanus 09.02.17 at 12:22 pm ( 16 )John Bellamy Foster Monthly Review, 2013. One point here is to refute the "profit-squeeze" theory, which still endures in some Marxian economics. This may be a "what next after refuting trickle-down."

Only for those interested, I am not capable or enthused to defend the whole thing.

"For Kalecki, the power of labor to increase money wages!although present to a minor extent in the normal business upswing!was not a significant economic threat to capital even at full employment due primarily to the pricing power of firms. Hence, if the system neglected consistently to promote full-employment through the stimulation of government spending this was not to be attributed to economic reasons per se, but rather to the political threat that permanent full employment would represent to the capitalist class."

I buy this completely, and the "pricing power of firms" is the main reason I oppose any UBI job guarantee/ELR is much better. But state infrastructure is best. The taxes on capital and capitalists must go to government spending ( socialized worker consumption ) and investment (workers capital?) or it is counterproductive.

Sorry. Two more thingsAlex SL 09.02.17 at 1:11 pm ( 17 )1) The Meidner Plan is back in the news, see Jacobin.

2) Increased taxes on capitalists for redistribution will upset capitalists. You want to drive almost every economist nuts, start talking about state control of pricing . That can done indirectly in ways like gov't housing or Medicare-for-all. The problems with redistribution without socialized pricing are evident in the PPACA.

Matt @9,steven t johnson 09.02.17 at 1:38 pmI may misunderstand, but the way you describe it it seems as if the concern to become overworked would have been the main factor. I must say that if the question is whether we want to lower top tax rates by 10% so that more people work themselves to death and get a heart attack in their 40s I'd say thanks but no thanks.

Maybe even phrasing it as "working harder", as I did in my first comment, is the wrong way of looking at trickle-down economics; the main argument seems to be that an investor or company owner would rather let their money sit around useless and earn a mere 1% in interest than invest in some 'job creating' activity that earns a return of 20% if they only get to keep 13%. Phrased like that I think it would be hard to argue that any even half-rational investor would ever reject the 13% ROI.

The problem might be that there just is no additional, unused opportunity for productive activity that earns a return of 20% on investment if the masses have seen stagnant wages for the last few decades. How would they afford to buy the new product that the investment would be in, except in the sense of a zero sum game where another investment elsewhere becomes less attractive to make up the difference? So if the investor's tax rate is lowered their choices are still money sitting around uselessly or inflating a bubble.

A man digging a ditch with a shovel is working much harder than the dude with a backhoe. It is not clear the guy working harder gets paid more. It's not clear the guy on the backhoe is getting more than minimum wage. The amount of profit expected from the ditch seems to me to depend on a lot more than how hard or productive either worker is. And the last I looked, economics doesn't have an agreed upon theory on the dynamics of the general rate of profit.bob mcmanus 09.02.17 at 2:40 pm ( 19 )All that stuff about marginal revenue productivity etc. seems to me to be unlikely to be much more than ideology.

Last one, because I would like this to be clearer. I am inverting is a little bit from "decreased taxes with increase growth" to "will increased taxes inhibit growth" using a 3-department model because:nastywoman 09.02.17 at 5:35 pm ( 20 )Krugman on Taxing Rents yesterday

Krugzilla: "much corporate taxation probably doesn't fall on returns to physical capital, but rather on monopoly rents."

So question for Quiggin, leaving aside finance and rents

Are increased taxes on physical/fixed capital a good thing, growth and welfare enhancing?

Are increased taxes on corporate returns, profits, good?

Should we end all depreciation allowances?

De we want to tax productive investment?It is about the framing. Too often this is argued as about capitalist income and capitalist consumption, as in Obama taxing private jets.

@13John Quiggin 09.02.17 at 11:17 pm ( 21 )

"See, you're giving the money to people with the expectation that they will use it to make "profitable investments".Or to spend it for a really great watch? – as I happen to know -(and love) these great Swiss Watchmakers who love to have the dough of Rich US-dudes redistributed towards some real cool Craftsmen. -(wherever they are) – as I'm right now spending some time with some really cool US carpenter -(in Iceland) – who loves it too – when he get's flown to Iceland to do some "real cool" work here too.

And isn't that really "fascinating" that so many "Rich Dudes" -(of all nations) seem to have this "thing" about (only) making "profitable investments" in order to return more money to themselves – than they spend – in order to make them even richer BUT when it comes to pay for a "Craftsman" who manufactures a nice well done cabinet -(or a well working golden watch) a "Real Rich Dude" is even willing to throw in a first class airline ticket to Geneve?

Whassup?

Bill @10 This is a good point. I think (1) needs to be modified to say that incomes are proportional to marginal product. Then point (2) requires generalized external economies of scale, which is the central idea in endogenous growth theory. I'll work on this.Ebenezer Scrooge 09.03.17 at 12:27 am ( 22 )Tim @14 The example you give is precisely covered by point 2.

Trickle-down is popular because many people are happy to tug their forelock if they can look down on somebody else. This is more an American disease than a European one.Collin Street 09.03.17 at 1:07 am ( 23 )Phrased like that I think it would be hard to argue that any even half-rational investor would ever reject the 13% ROI.Gareth Wilson 09.03.17 at 7:00 am ( 24 )You think other people are like you. Other people think other other people are like them. What this says about advocates of trickle-down economics is left as an exercise.

There is a problem which is referred to in New Zealand as the three B's. Once people own a boat, a BMW, and a bach (holiday home), there's a tendancy to work less hard, maybe even retire early and sit around doing nothing. Margaret Thatcher herself harshly criticised the British equivalent of this. I share your skepticism that tax rates will help with this, but it is a problem.nastywoman 09.03.17 at 7:45 am ( 25 )– or let's blame it all on the "fashionable American-Anglo culture of "Disruption"?bob mcmanus 09.03.17 at 10:19 am ( 26 )

While in sane and reasonable economical environments the words "trickle down" just don't exist BUT a culture of "Cooperation and Compromises or how do the Germans call it "Mitbestimmung" – and there is no need for "trickle down" in Mitbestimmung as everybody agrees that everybody should get her or his faire share of the "winnings".Okay fineCarlD 09.03.17 at 11:10 am ( 27 )"Capitalist income when directed by policy into productive actually job-creating investment is of general benefit and should be taxed at a lower marginal rate."

is the big trickle-down, the primal, universal trickle-down that enables all the others.

Not capitalist income vs labour income, not capital income share vs labour share, the problem is capital vs labour, " good to increase capital cause jobs " is an assumption so basic I don't even know how to quantify its adversary or opposition. Raw Number of workers? Capital's opposition is made invisible by mainstream economics. And looking at capitalist income or capitalist share of income or marginal productivity etc I think are means to ensure that capital quantity keeps increasing ("cause we can tax the profits or outflow") and capitalist political power (cause we don't want to lose the factory or sports stadium cause jobs) keeps increasing.

No, Marx didn't go here, but then Marx believed that increasing capital quantity would inevitably lead to proletarian revolution. We no longer have that excuse.

Tax not consumption, tax not income, tax capital directly so that we have less of it. The govt can use the income to create socialized investment and production.

"In the absence of taxes and other government interventions,"bob mcmanus 09.03.17 at 12:25 pm (This is always the weasel out. There are always at least some taxes and government interventions on which to blame the failure of markets to work their magic.

Last one again. I may not respond if anyone bothers, because this is at least orthogonal to the OP.faustusnotes 09.03.17 at 12:27 pm ( 29 )How to tax capital? Simple, an example. Declare face value of equities at closing bell on April 15 and tax it. 50%, 10%, 0.1%. Forget realized capital gains or transaction taxes, tax face values. Yes indeed I understand what will happen to face values the day before and the day after. I want to drive NASDAQ to zero, how about Krugman? Why not? (Also bonds and bank assets, of course)

Yes, I know we do tax property at a local level and I spent some time looking for the tax incidence between business wealth and housing values but I suspect it varies wildly along with a maze of capital-protecting laws. I did notice that non- profits are taxed differently if at all, in other words, still looking at property under the lens of income. So the Clinton Foundation provides Chelsea economic security and political power in perpetuity.

Capital is a power relation that shows up in de-facto segregated communities and unequal education spending and outcomes and I would possibly tax houses as I would equities.

And of course all this can be incremental and marginal, we don't need to go fullbore expropriation from the start.

But private property is a socialized power relation, and we want to discourage private investment as much as possible. Otherwise, its still a trickle down economy.

I think it's important to take issue with comment 6, by Ian Maitland, which is a collection of despicable lies. I know it makes no difference to Ian Maitland, who is a lying shill, but it is important for people reading.Layman 09.03.17 at 12:50 pm (First Maitland says (contradictorily) that the proportion of the world population in poverty has fallen to 5%, and that only 152 million people live in poverty. This is untrue. The World Bank estimates that 10.7% of the world's population, or about 790 million people, live in poverty, and that the majority of poverty reduction has only occurred due to China and India (i.e. no change in Africa). Maitland is using dubious numbers from a single shonky 2009 analysis published in that dumpster for shit papers, the NBER.

Second, Peter Singer never wrote the phrase Maitland accuses him of, with respect to the Bangladesh famine. Singer's paper on the famine can be found here and is a discussion of the urgent need to increase aid to "East Bengal", as well as whether people in developed countries are justified in impoverishing themselves in support of starving people in East Bengal (he concludes that they should not impoverish themselves so much that their utility is lower than that of the Bangladeshis they want to help). He discusses and dismisses the idea that people in rich countries should not give aid to East Bengal because the real cause of its famine is population control, and aid without population control won't work: He recommends aid now, and then further aid for population control. He says people should be "working full time" to push both issues with their government, and sneers at the UK government for valuing concorde more than starving Bangladeshis.

The nearest quote to that which Maitland attributes to Singer comes from a later book, Practical Ethics , and is part of a discussion about whether rich people should give money to aid poor countries, and how to judge the best way to do this. Practical Ethics was written in 1979, about the time that now-independent Bangladesh was becoming a success story in health, population control and nutrition despite being much poorer than India. In the sentence before the sentence closest to that which Maitland cites, Singer states that we have an obligation to assist poor countries, but not to waste our money on ways that don't help. This sentence has nothing to do with Bangladesh, and nothing to do with abandoning poor countries to starve – in fact it concerns the best way to do precisely the opposite.

In short, what Maitland wrote here is entirely false, deliberately misleading, and malicious. I know most people on here are aware that Maitland is a lying liar, but just in case anyone is new here and thinks that the failure to challenge his lies is a sign that they're accepted by others as fact, here is the rebuttal: everything at comment 6 is a vicious lie, and people like Maitland should be deeply ashamed of themselves for the deliberate and mendacious lies they tell.

Garett Wilson: "There is a problem which is referred to in New Zealand as the three B's. Once people own a boat, a BMW, and a bach (holiday home), there's a tendancy to work less hard, maybe even retire early and sit around doing nothing. Margaret Thatcher herself harshly criticised the British equivalent of this. I share your skepticism that tax rates will help with this, but it is a problem."Cranky Observer 09.03.17 at 1:03 pm ( 31 )Why is this a problem? Sure, it's an affront to Puritanism, but besides that?

some lurker 09.03.17 at 2:55 pm ( 32 )= = = Once people own a boat, a BMW, and a bach (holiday home), there's a tendancy to work less hard, maybe even retire early and sit around doing nothing. [ ] I share your skepticism that tax rates will help with this, but it is a problem. = = =

Why? Why is it a problem, that is?

I realize that many global cultures based on English, Scots, and closely-related Northern European cultures have adopted the neo-Puritan attitude that mankind deserves to be punished and that 60-100 hours/week of grinding labor from age 16 to 80 is a necessary part of that punishment. I'm less sure why the rest of us should accept that, particularly given the trend toward automation of production of the necessities of life.

The devil is, as always, in the details. These arguments always ignore the inconvenient facts of tax brackets (you mean the 90% tax rate for high earners doesn't apply to the first dollar earned?) or deductions/exemptions. My rule of thumb is that top earners pay an effective tax rate of around a third of the actual rate. George Romney was assessed a 70-90% rate in the 60s and paid something in the 30s: his son Willard would have been assessed a 39.6% rate and paid something in the teens, probably not too far off what most of the CT commentariat pay.Tim Worstall 09.03.17 at 5:11 pm ( 33 )Economics is theoretical politics just as politics is applied economics: it all made more sense when it was called "political economy." Then you knew that economists were trying to write policy and that politicians were trying to hide their schemes behind some academic fig leaf.

And +1 to the "tinkle-down" variant I'll be sure to use that.

"Tim @14 The example you give is precisely covered by point 2."RD 09.03.17 at 5:18 pm ( 34 )Umm, how? If there's a consumer surplus then the workers and inventors and capitalists etc simply aren't gaining all of he value. I don't we generally think that there is usually a consumer surplus?

GW @ 24bruce wilder 09.03.17 at 6:07 pm ( 35 )A rich guy on holiday at the beach notices a local fisherman sitting on the beach strumming a guitar and sipping a beer at 1400 hours. He inquires as to why he is not still at work.

Local; "I've caught enough fish for today!"

Rich Guy; "But if you work harder and longer, 6 or 7 days a week, 12 hours a day, you will be able to buy another fishing boat, employ more fisherman, buy 2 more boats, then 4 boats."

Local:" What for?"

Rich Guy: " So you can retire and sit on the beach strumming your guitar and drinking beer!"

. . . the marginal productivity theory . . . is at the heart of neoclassical economics. In a general equilibrium model of a perfectly competitive economy with full employment, it can be deduced as a theorem. . . . The neoclassical model . . . has never been a fully accurate representation of the economy.Howard Frant 09.03.17 at 7:55 pm ( 36 )Way to go out on a limb with classic understatement. Never a " fully accurate representation"!

It seems to me we are back in Lesson 1 / Lesson 2 economics, wondering whether Lesson 2 is going to be an explanation of how Lesson 1 is wrong and wrong in every conceivable respect and implication, . . . or an explanation of how Lesson 1 is right, but not quite right.

In some respects, you seem to want to turn the claims for trickle-down economics topsy-turvy and show how pretty much the opposite of what the advocates of trickle-down predicted and recommended has turned out to be true and ought to be recommended.

But, in other respects, you seem to want to defend neoclassical economics, as a merely imperfect representation, which has, perhaps become less accurate as the further development of the economic system has unfolded.

The rhetorical turn, "it is even less accurate now than in the past" leads to a narrative in which epiphenomena are transformed into their own causal forces, perhaps to avoid the contradiction in your analysis. Wage stagnation is an outcome that disproves the neoclassical economics that recommended the policies that created wage stagnation, but some instinct holds you back from saying that, so now wage stagnation is itself a reason to believe that neoclassical economics is "less accurate" a representation. Did wage stagnation cause itself? Did the recommendations or expectations of orthodox neoclassical economics have anything to do with it?

I guess we do not need to answer and we should not wonder if the recommendations themselves were innocent misunderstandings of the economy or a fraudulent apology for policy that in fact targeted the consequent upward redistribution of income and wealth.

Is neoclassical economics simply a rhetoric engine for generating these frauds or did neoclassical economists know what the powers-that-be were doing as well as how to sell what the powers-that-be were doing? It is a classic conundrum in economics. The doctrines of economics provide the styling for the outward apology and (importantly false) rationale (see the discussion of the allegedly Machiavellian roles of James M Buchanan and Milton Friedman in the other thread) for policy, but also the operating manual for policy. Somewhere, someone has to have some idea of what they are doing, in pulling the levers and operating the machinery of the economic system. Even granted that there might be important limits -- the serious people have been known to run the economy off the edge of a cliff. It is just hard to know even then -- when we are enveloped in a crisis of crisis capitalism -- if the powers-that-be are doing it by mistake (1930) or on purpose (2008).

I cannot tell from the OP whether you think economic theory and the intuitions it cultivates, for better and worse, should matter or not. Is neoclassical economics wrong? Or misused?

I sort of question whether it's even worth engaging with trickle-down at this level, as opposed to just saying "Well, it doesn't work." Are there still serious ecenomists who are saying it does?J-D 09.03.17 at 8:48 pm ( 37 )JQ@7

The dramatic increase in income and reduction in poverty in the Third World go far beyond China and India. China is the most extreme, but it's pretty much everywhere, except Africa.

Alex SL@8

People are always tempted to respond to economists' assertions by saying,"Well, *I* wouldn't do that!" Unfortunately, introspection generally doesn't work, because the assertions usually are not about what a typical person would do, but about what people on the margin would do, i.e., people who are close to indifferent beween doing it and not doing it.

steven t johnson@18

Two things you can be sure of (both in line with neoclassical theory): 1) The guy operating the backhoe will be making more than the guy wielding the shovel 2) The guy operating the backhoe will be making (a lot) more than the minimum wage.

Gareth WilsonF 09.03.17 at 9:30 pm ( 38 )

How is it a problem? a problem for whom?14 is also addressed quite well and in detail by Michael Pettis' latest .Peter T 09.04.17 at 12:05 am ( 40 )1) The guy operating the backhoe will be making more than the guy wielding the shovel 2) The guy operating the backhoe will be making (a lot) more than the minimum wage.Tabasco 09.04.17 at 12:20 am ( 41 )At the level of: a lot of guys wielding shovels will move less dirt than a lot of guys driving back-hoes, and so be less productive and have less to share, this is true.

At the level of the work-crew digging ditches it's not. Three guys dig a ditch – one marks the line, one drives the back-hoe, one shovels the odd bits that the back-hoe can't do. Every so often they change places, because they all know all the jobs, and shovelling is hard work. Or old Joe drives the back-how while young Dave does the shovel, because that's fairer given Joe's got a bad back. Joe gets paid a bit more because he's senior. And Ramjit gets paid most because he's in charge and is responsible for seeing that the ditch goes where it's supposed to.

You can't devolve cooperative production down to individual productivity.

Gareth Wilson 09.04.17 at 12:24 am ( 42 )"The dramatic increase in income and reduction in poverty in the Third World go far beyond China and India."No one talks much about South Korea, but a generation ago they were very poor. Now they are as rich as Japan, with income distribution like the Scandinavians. Of course this all happened with a great deal of heavy handed government intervention, to the disapproval of free market fundamentalists in the West, but it was still capitalism.

It's a problem because the man with the three B's could be producing more wealth and improving everyone's standard of living, but he isn't.J-D 09.04.17 at 5:49 am ( 43 )Gareth WilsonScott V 09.04.17 at 1:46 pm ( 44 )