|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

| Economics of Peak Energy | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 |

|

|

Switchboard | ||||

| Latest | |||||

| Past week | |||||

| Past month | |||||

|

|

December 23, 2013 The Guardian

Jump to comments (330)Industry expert warns of grim future of 'recession' driven 'resource wars' at University College London lecture

A former BP geologist speaks out on the danger of peak oil. Photograph: Ben Stansall/AFP/Getty Images

A former British Petroleum (BP) geologist has warned that the age of cheap oil is long gone, bringing with it the danger of "continuous recession" and increased risk of conflict and hunger.

At a lecture on 'Geohazards' earlier this month as part of the postgraduate Natural Hazards for Insurers course at University College London (UCL), Dr. Richard G. Miller, who worked for BP from 1985 before retiring in 2008, said that official data from the International Energy Agency (IEA), US Energy Information Administration (EIA), International Monetary Fund (IMF), among other sources, showed that conventional oil had most likely peaked around 2008.

Dr. Miller critiqued the official industry line that global reserves will last 53 years at current rates of consumption, pointing out that "peaking is the result of declining production rates, not declining reserves." Despite new discoveries and increasing reliance on unconventional oil and gas, 37 countries are already post-peak, and global oil production is declining at about 4.1% per year, or 3.5 million barrels a day (b/d) per year:

"We need new production equal to a new Saudi Arabia every 3 to 4 years to maintain and grow supply... New discoveries have not matched consumption since 1986. We are drawing down on our reserves, even though reserves are apparently climbing every year. Reserves are growing due to better technology in old fields, raising the amount we can recover – but production is still falling at 4.1% p.a. [per annum]."

Dr. Miller, who prepared annual in-house projections of future oil supply for BP from 2000 to 2007, refers to this as the "ATM problem" – "more money, but still limited daily withdrawals." As a consequence: "Production of conventional liquid oil has been flat since 2008. Growth in liquid supply since then has been largely of natural gas liquids [NGL]- ethane, propane, butane, pentane - and oil-sand bitumen."

Dr. Miller is co-editor of a special edition of the prestigious journal, Philosophical Transactions of the Royal Society A, published this month on the future of oil supply. In an introductory paper co-authored with Dr. Steve R. Sorrel, co-director of the Sussex Energy Group at the University of Sussex in Brighton, they argue that among oil industry experts "there is a growing consensus that the era of cheap oil has passed and that we are entering a new and very different phase." They endorse the conservative conclusions of an extensive earlier study by the government-funded UK Energy Research Centre (UKERC):

"... a sustained decline in global conventional production appears probable before 2030 and there is significant risk of this beginning before 2020... on current evidence the inclusion of tight oil [shale oil] resources appears unlikely to significantly affect this conclusion, partly because the resource base appears relatively modest."

In fact, increasing dependence on shale could worsen decline rates in the long run:

"Greater reliance upon tight oil resources produced using hydraulic fracturing will exacerbate any rising trend in global average decline rates, since these wells have no plateau and decline extremely fast - for example, by 90% or more in the first 5 years."

Tar sands will fare similarly, they conclude, noting that "the Canadian oil sands will deliver only 5 mb per day by 2030, which represents less than 6% of the IEA projection of all-liquids production by that date."

Despite the cautious projection of global peak oil "before 2020", they also point out that:

"Crude oil production grew at approximately 1.5% per year between 1995 and 2005, but then plateaued with more recent increases in liquids supply largely deriving from NGLs, oil sands and tight oil. These trends are expected to continue... Crude oil production is heavily concentrated in a small number of countries and a small number of giant fields, with approximately 100 fields producing one half of global supply, 25 producing one quarter and a single field (Ghawar in Saudi Arabia) producing approximately 7%. Most of these giant fields are relatively old, many are well past their peak of production, most of the rest seem likely to enter decline within the next decade or so and few new giant fields are expected to be found."

"The final peak is going to be decided by the price - how much can we afford to pay?", Dr. Miller told me in an interview about his work. "If we can afford to pay $150 per barrel, we could certainly produce more given a few years of lead time for new developments, but it would break economies again."

Miller argues that for all intents and purposes, peak oil has arrived as conditions are such that despite volatility, prices can never return to pre-2004 levels:

"The oil price has risen almost continuously since 2004 to date, starting at $30. There was a great spike to $150 and then a collapse in 2008/2009, but it has since climbed to $110 and held there. The price rise brought a lot of new exploration and development, but these new fields have not actually increased production by very much, due to the decline of older fields. This is compatible with the idea that we are pretty much at peak today. This recession is what peak feels like."

Although he is dismissive of shale oil and gas' capacity to prevent a peak and subsequent long decline in global oil production, Miller recognises that there is still some leeway that could bring significant, if temporary dividends for US economic growth - though only as "a relatively short-lived phenomenon":

"We're like a cage of lab rats that have eaten all the cornflakes and discovered that you can eat the cardboard packets too. Yes, we can, but... Tight oil may reach 5 or even 6 million b/d in the US, which will hugely help the US economy, along with shale gas. Shale resources, though, are inappropriate for more densely populated countries like the UK, because the industrialisation of the countryside affects far more people (with far less access to alternative natural space), and the economic benefits are spread more thinly across more people. Tight oil production in the US is likely to peak before 2020. There absolutely will not be enough tight oil production to replace the US' current 9 million b/d of imports."

In turn, by prolonging global economic recession, high oil prices may reduce demand. Peak demand in turn may maintain a longer undulating oil production plateau:

"We are probably in peak oil today, or at least in the foot-hills. Production could rise a little for a few years yet, but not sufficiently to bring the price down; alternatively, continuous recession in much of the world may keep demand essentially flat for years at the $110/bbl price we have today. But we can't grow the supply at average past rates of about 1.5% per year at today's prices."

The fundamental dependence of global economic growth on cheap oil supplies suggests that as we continue into the age of expensive oil and gas, without appropriate efforts to mitigate the impacts and transition to a new energy system, the world faces a future of economic and geopolitical turbulence:

"In the US, high oil prices correlate with recessions, although not all recessions correlate with high oil prices. It does not prove causation, but it is highly likely that when the US pays more than 4% of its GDP for oil, or more than 10% of GDP for primary energy, the economy declines as money is sucked into buying fuel instead of other goods and services... A shortage of oil will affect everything in the economy. I expect more famine, more drought, more resource wars and a steady inflation in the energy cost of all commodities."

According to another study in the Royal Society journal special edition by professor David J. Murphy of Northern Illinois University, an expert in the role of energy in economic growth, the energy return on investment (EROI) for global oil and gas production - the amount of energy produced compared to the amount of energy invested to get, deliver and use that energy - is roughly 15 and declining. For the US, EROI of oil and gas production is 11 and declining; and for unconventional oil and biofuels is largely less than 10. The problem is that as EROI decreases, energy prices increase. Thus, Murphy concludes:

"... the minimum oil price needed to increase the oil supply in the near term is at levels consistent with levels that have induced past economic recessions. From these points, I conclude that, as the EROI of the average barrel of oil declines, long-term economic growth will become harder to achieve and come at an increasingly higher financial, energetic and environmental cost."

Current EROI in the US, Miller said, is simply "not enough to support the US infrastructure, even if America was self-sufficient, without raising production even further than current consumption."

In their introduction to their collection of papers in the Royal Society journal, Miller and Sorrell point out that "most authors" in the special edition "accept that conventional oil resources are at an advanced stage of depletion and that liquid fuels will become more expensive and increasingly scarce." The shale revolution can provide only "short-term relief", but is otherwise "unlikely to make a significant difference in the longer term."

They call for a "coordinated response" to this challenge to mitigate the impact, including "far-reaching changes in global transport systems." While "climate-friendly solutions to 'peak oil' are available" they caution, these will be neither "easy" nor "quick", and imply a model of economic development that accepts lower levels of consumption and mobility.

In his interview with me, Richard Miller was particularly critical of the UK government's policies, including abandoning large-scale wind farm projects, the reduction of feed-in tariffs for renewable energy, and support for shale gas. "The government will do anything for the short-term economic bounce," he said, "but the consequence will be that the UK is tied more tightly to an oil-based future, and we will pay dearly for it."

Dr Nafeez Ahmed is executive director of the Institute for Policy Research & Development and author of A User's Guide to the Crisis of Civilisation: And How to Save It among other books. Follow him on Twitter @nafeezahmed

12/6/2013adornosghost:

dilbert dogbert wrote:

Horses fed.

Need to feed the the horses and llamas, and probably break the ice on the trough.

"Bakken news this morning, not enough for a new post so I will just post it at the top of this one.

Snow, cold temps slow oil production

DICKINSON, N.D. --Even booming Bakken oil production can't stand up to North Dakota's crippling winters.

By hindering transportation to wells and slowing the hydraulic fracturing process, severe winter weather slows production.

The No. 1 cause of the slowdown in winter months is difficulties for fracking, North Dakota Department of Mineral Resources Director Lynn Helms said. Ice and snow make it harder to get water to a site, it takes longer to heat fluids and keep them warm, and flowback water can freeze and delay the process, he said....

Between 400 and 500 wells are expected to be shut down from about now until spring, Helms said.

"There are a lot of wells out there that produce very little oil and gas," he said, "and it doesn't pay to keep the roads plowed or try to get trucks in and out to keep the wells pumping.

"It's pretty significant when you think about 400 or 500 wells being shut off for three to four months," Helms said.

And from the Wall Street Journal concerning oil production in Texas

Snow, cold temps slow oil production

Bitter winds that blew sleet across Texas just before Thanksgiving led to power outages, frozen equipment and icy roads throughout the prolific oil fields of the Permian Basin, including Midland, Texas. Some energy companies are warning that their oil output-and earnings-are being affected.

Winter weather adds another dimension to the situation when you have low producing wells where the oil is hauled out by truck."

-Ron

November 17, 2013 | Econbrowser

Here are some numbers I put together, based on Steven Kopits' excellent work*.

The cumulative increase in global crude oil (Crude + Condensate) production, in the seven year period from 1998 to 2005, in excess of what we would have produced at the 1998 production rate of 67.0 mbpd (million barrels per day, EIA), was 6.3 Gb (billion barrels).

Steven Kopits estimated that cumulative global upstream (oil exploration and production) capital costs were $1.5 Trillion in the seven year period from 1998 to 2005. So, the total capital cost per net cumulative barrel of increase in production from 1998 to 2005 (relative to 1998) was about $300 per barrel.

Of course, the total upstream capital expenditures were used to both offset declines from existing production and to show a net increase in production, but I am primarily interested in the difference between the 1998 to 2005 increase in global crude oil production versus the 2005 to 2012 increase in global crude oil production.

The cumulative increase in global crude oil production, in the seven year period from 2005 to 2012, in excess of what we would have produced at the 2005 production rate of 73.6 mbpd (million barrels per day, EIA), was 0.3 Gb.

Steven Kopits estimated that cumulative global upstream capital costs were $3.5 Trillion in the seven year period from 2005 to 2012. So, the total capital cost per net cumulative barrel of increase in production from 2005 to 2012 (relative to 2005) was about $11,700 per barrel.

Note that cumulative upstream capital costs increased by 133% from the 1998 to 2005 time period to the 2005 to 2012 time period, but the corresponding increase in cumulative production (relative to 1998 and 2005 respectively) fell by 95%.

Therefore the global upstream capital costs necessary to offset production declines from existing wells and to add one new barrel of cumulative production in the 2005 to 2012 time period was 39 times what was necessary to offset production declines from existing wells and to add one new barrel of cumulative production in the 1998 to 2005 time period--in terms of capital costs per barrel of new cumulative production.

And note that annual Brent crude oil prices rose at an average rate of about 15%/year from 1998 to 2012.

A critically important point to remember is that the post-2005 decline in US petroleum consumption, and the post-2008 increase in US crude oil production, caused our demand for net oil imports to decline, but this had no impact on the global supply of net oil exports.

We have seen a material post-2005 decline in Global Net Exports of oil (GNE**), with developing countries, led by China, so far at least consuming an increasing share of a post-2005 declining volume of GNE.

The reality facing the US and most other developed net oil importing countries is that are gradually being priced out of the global market for exported oil, via price rationing. At the 2005 to 2012 rate of decline in the ratio of GNE to Chindia's Net Imports (GNI), the GNE/CNI ratio would approach 1.0 in only 17 years, which implies that the Chindia region alone would theoretically consume 100% of Global Net Exports of oil:

http://i1095.photobucket.com/albums/i475/westexas/Slide1_zps9ff3e76d.jpg

*Data Source: Barclays Capital

**GNE = Combined net exports from (2005) Top 33 net oil exporters, total petroleum liquids + other liquids (EIA)

From what I have seen, total oil supply has been moving up since 2005 and significantly since the most recent recession. Corn prices are also at three-year lows, and corn is the main input for fuel ethanol. And also, the EPA is now considering a reduction in the ethanol mandate, though I do not know if refiners will chose to use a different oxygenator (like MTBE) for their blends.

There is also supply reduction in countries like Libya (war) and Iran (politics). Venezuela is turning into a failed state. Mexico is reforming its oil industry to offer incentives (like production sharing agreements) to boost production.

It looks like there are more factors which could lower oil prices than raise them, over the next few years.

Luke,

Following is a link to normalized production and net exports numbers for 2002 to 2011, and partially to 2012:

http://i1095.photobucket.com/albums/i475/westexas/Slide1-29_zps42ffc9bc.jpg

2005 values in the above chart were set equal to 100%. GNE remained at 96% (of 2005 rate) in 2012, while ANE (Available Net Exports, or GNE less CNI) fell to 85% (of 2005 rate).

Regarding Libya and Iran, production and export disruptions certainly had an effect, but there are always some kind of production problems around the globe at any given point in time.

Regarding Mexico, based on the 2004 to 2012 rate of decline in their ECI ratio, they would approach zero net oil exports in about six years, by the end of 2019. Overall Western Hemisphere net oil exports* fell from 5.9 mbpd in 2004 to 5.0 mbpd in 2012.

*Seven major net exporters in the Americas in 2004, total petroleum liquids + other liquids, EIA

And here is an excerpt from an essay I wrote regarding the prospect for the US becoming a net oil exporter:

For a concrete example of how the Export Capacity Index (ECI) concept works, consider two countries that are widely considered to be critically important sources of future crude oil production: Brazil and Iraq. If we extrapolate the 2008 to 2012 rate of decline in Brazil + Iraq's combined ECI ratio (the ratio of liquids production* to consumption), they would collectively approach zero net oil exports in about 20 years.

Given Brazil's status as a net oil importer in 2012, even if we count biofuels, it's instructive to consider what the conventional wisdom was just a few years ago regarding Brazil. In April, 2009 Bloomberg published a column discussing the prospect for Brazil continuing "to take market share away from OPEC."

We should keep case histories like this in mind when we read in the media about the "Fact" that the US will soon be a net oil exporter, and while there are always uncertainties in forecasting future trends, we can be certain of three objective facts: (1) All oil fields, sooner or later, peak and decline; (2) Global crude oil production is the sum of discrete oil fields that peak and decline and (3) Given an ongoing production decline in an oil exporting country, it is an mathematical certainty that unless domestic consumption in that oil exporting country falls at the same rate as the rate of decline in production, or at a faster rate, the resulting net export decline rate will exceed the production decline rate and the net export decline rate will accelerate with time.

*EIA data, production = total petroleum liquids + other liquids (mostly biofuels in the other liquids category)

Lower gasoline prices are more to do with lack of demand growth rather than supply increases. World oil demand is rising by less than 1%. Chinese oil demand was 8.4 mpd in 2005. In 2013 they are consuming at rate of 9.75 mpd which is mere 1.9% growth componded from 2005 while their economy has grown at over 9% average. So is East European and CIS oil demand where oil demand growth has lagged economic growth rates.

They consume lot less oil than countries with similar per capita income. Can anyone explain this anomaly?

baffling

perhaps our inability to impact world crude prices and thus gasoline suggests the economy should attack energy in a different way? reduce demand for oil and gasoline with renewable energy sources and electric/hybrid cars.

you can change the supply-demand curve two ways. why not shift the demand curve if we are ineffective with the supply curve?

Jeffrey, excellent work, as always. Have you considered adjusting your data for population to show the per-capita levels and rates? If so, you will have already discovered that the world extraction per capita now resembles that of the US in the mid- to late 1970s, implying that the global growth of industrialization has peaked along with real GDP per capita.

Also, what you and Steven are describing WRT to costs at the trend investment and extraction rates is the so-called "Seneca Cliff" (or effect), i.e., the acceleration rate of decline is much faster than the rise to the peak. The phenomenon is also analogous to the so-called "Red Queen Race" (also prevalent in the high-tech industry) in which a faster rate of growth of investment, net energy, and profit is required to avoid deceleration and then contraction of extraction/production.

To all:

Real final sales per capita and wage and salary disbursements to the price of gasoline:

http://research.stlouisfed.org/fredgraph.png?g=owD

To working-class wages:

http://research.stlouisfed.org/fredgraph.png?g=owE

Brent to real GDP levels for China to '11), US (real final sales per capita), Japan, and the EU:

http://research.stlouisfed.org/fredgraph.png?g=owF

Change rates (China has decelerated from 9% to 7%):

http://research.stlouisfed.org/fredgraph.png?g=owG

Change rates of US real final sales per capita and Brent to real final sales per capita:

http://research.stlouisfed.org/fredgraph.png?g=owK

The decelerating rate of Brent to final sales with the yoy rate of US real final sales below 1% is recessionary historically.

https://app.box.com/s/txig5u69mz0pbgsj3qn5

IOW, the prices of oil and gasoline have fallen recently because US and global demand is at or near an historical recessionary rate worldwide.

There has recently been headlines about the Monterey shale reserves in CA with recoverable reserves estimated at 15 billion bbl by the EIA, which is about 2 years' worth of current US consumption and ~18 months for the US and China combined. What is rarely discussed when these issues are reported is the price of oil, cost per bbl, sustainable rate of extraction, and rate of real GDP per capita is required to sustain profitable extraction and the demand to justify the costs of extraction.

@bmz, the US cannot become "energy independent" in the way it is generally understood (sold) at the trend level and rate of real GDP per capita AND at the current price of oil. Rather, we would need the constant US$ price of oil below $40 at a 30-35% lower level of oil consumption (including net oil imports) OR a near doubling of US extraction in the meantime.

However, real GDP per capita cannot grow with the sustained price of oil above $40-$50, but a price of oil at or above $85-$100 is required for crude substitutes to be profitable to extract.

We can't afford to increase profitable crude substitute extraction AND grow real GDP per capita at the current price of oil.

Therefore, we are left with an indefinite period ahead of little or no growth of real GDP per capita with steadily declining US oil consumption and imports per capita, and the likelihood of the average price of oil falling to levels that do not permit growth of profitable extraction of crude substitutes.

IOW, Peak Oil and the "Limits to Growth".

Re: Satish

I don't know if it's an explanation, other than an explanation for high oil prices, but here is a chart showing normalized liquids consumption (2002 = 100%) for China, India, (2005) Top 33 net oil exporters and the US from 2002 to 2012, versus annual Brent crude oil prices:

http://i1095.photobucket.com/albums/i475/westexas/Slide14_zpsb2fe0f1a.jpg

The $64 Trillion question is what happens from 2012 to 2022. As noted above, the current trajectory would put China and India consuming 100% of Global Net Exports of oil in 17 years.

Posted by: Jeffrey J. Brown at November 17, 2013 01:57 PM

Re: Jimmy,

Of course, there is the alternative explanation--that the global supply of net oil exports available to importers other than China & India (what I call ANE) fell from 41 mbpd in 2005 to 35 mbpd in 2012.

Posted by: at November 17, 2013 02:06 PM

Nov 13, 2013 | FT Alphaville

Oil prices continue to decline, with WTI currently leading the charge:

So where are the oil bulls of 2008 now?

Hard to say. But long-standing oil market watcher Stephen Schork, of the Schork Report, offers some colourful views on the topic this Wednesday. They come in the shape of a somewhat self-congratulatory nostalgic yarn, but it is worth the read, in so much as it really takes you back to how things were back in those scary September days.

Here he goes:

Back in September 2008 we were in Vienna giving a presentation to our friends at OPEC. In between copious amounts of Sachetorte and Grüner Veltliner, we had the opportunity to sit down with one of the largest hedge fund managers in Austria. At the time, crude oil on the NYMEX was imploding. That is to say, after peaking at a record $147 that July, the market was in the midst of the correction and was trading around $110 that September.

We told this fund manager the same thing we told Dr. Alipour-Jeddi's group at OPEC the day before, i.e. we thought oil was heading back to at least $75, which was the spot whence the 2008 bubble began. After we finished our bearish screed, the fund manager stood up, snickered and shot us a look of haughty derision. He then walked over to his bookshelf, took out a book and slid the book across the desk. The book was Matt Simmons' Twilight in the Desert.

Then, while still maintaining that air of superiority, he told us that this (pointing to Mr. Simmons' book) was the reason why we would never see oil below $100 a barrel again. We sat there. We took in what he just told us and we contemplated a measured response. After some thought, we told him that we thought he was a fool (that was our exact word).

Needless to say, we didn't get his business. It can also go without saying that this guy is no longer one of Vienna's largest fund managers. Our expressed skepticism was (and still is) based on common economic sense that high prices are indeed the cure for high prices. The mirror of this economic axiomatic is… low prices are the cure for low prices, which in the case of our Viennese fund manager, led him to the false messiah of peak oil. The reason why no new significant oil deposits were discovered in the 1980s and 1990s is because… at $20 a barrel it did not make any economic sense to go out and try and discover new oil. In hindsight, you drive oil to $147 barrel and lo and behold, five years hence the world is swimming in oil. It really is that simple.

All of which happens to be a lead up to the following observation about the latest from the IEA's world energy outlook 2013:

This now brings us to yesterday's release of the IEA's World Energy Outlook 2013. Of particular interest were these two bullets:

- "Global energy trade is re-oriented from the Atlantic basin to the Asia-Pacific region. China is becoming the largest oil- importing country; India becomes the largest importer of coal by the early 2020s. Improved energy efficiency and a boom in unconventional oil and gas production help the United States to move steadily towards meeting almost all of its energy needs (in energy equivalent terms) from domestic resources by 2035.

- Oil supply rises from 89 mb/d in 2012 to 101 mb/d in 2035 in the New Policies Scenario. Key components of the increase are unconventional oil (up 10 mb/d) and natural gas liquids (NGLs) linked to the increase in global gas output (up 5 mb/d). Conventional crude oil's share in total oil production falls, from 80% in 2012 to two-thirds in 2035. The role of OPEC in quenching the world's thirst for oil is temporarily reduced over the next ten years, notably as US light tight oil and Brazilian deepwater output step up, but the share of OPEC countries in global output rises again in the 2020s, as they remain the only large source of relatively low-cost oil. Iraq is the largest single source of oil production growth, followed by Brazil, Canada and Kazakhstan. The United States is the world's largest oil producer for much of the period to 2035."

Hmm, from Twilight in the Desert to the U.S. being the world's go-to oil producer for the next two decades. Isn't it amazing what can happen when you let markets respond to the needs of people? Case in point… weather aside, where would you rather live, Bismarck or Caracas?

A triumph for market adjustability, ingenuity and just holding out for the right incentive.

(He's not the peak oil messiah, he's a very naughty boy – Ed.)

Related links:

- International Energy Agency warns of future oil supply crunch – FT

- Welcome to Saudi America – FT Alphaville

This entry was posted by Izabella Kaminska on Wednesday November 13th, 2013 09:41.

markopolo

Apart from the bigger problem that we have to deal with the consequences of burning all this carboniferous fuel, the 'price of oil' is a distraction. We all know there's lots out there. What matters is how much energy is required to produce each unit of new energy - so called EOEI. This ratio is deteriorating and therefore growth becomes increasingly expensive. QED.

meteorquake

"Continues to decline"??? someone really can't read a graph. Looks very much like returning after a few-month excursion to me... d

Nobby

Alternative sources of oil such as tar sands and shale have perhaps put a collar around oil prices. There is currently plenty of supply when crude is above $100, but if prices fall much below that level, much of the marginal output is no longer economically viable.

As for the long era of US oil supremacy, the assumptions being made are quite controversial as not all the experts agree on the life expectancy of the new finds.

One other thing is that too much is being written about the changing dynamics of supply in the US market and not enough about the changing dynamic of demand. As far as I can see from the data, US oil consumption has declined by a greater amount than production has increased - demand is down around 2m barrels a day from the peak, whereas output is up around 1m.

Andao

Question about the "US energy self sufficiency " forecasting: does this take into account the fact that Americans will likely buy more inefficient vehicles if domestic gasoline prices are lower? If the US is awash in oil, then gas is cheap and everyone wants an SUV. Research into energy efficiency has been driven by expensive oil. Just like no one wants to search for new oil at $20/barrel, no one wants to invest in electric cars at this level either.

Perhaps the drop in oil price is a lagging indicator.. the benefits of recent research into fuel efficiency are still being felt, while current investment is slowing or halting. People buy fewer electric cars = lower investment in battery technology/factories = more expensive batteries and electric cars. Ten years from now we might all be looking at electric cars as just a fad, sort of like how GM treated the EV-1 in the mid 1990s

Doly

"Peak oil" was always misunderstood. People weren't necessarily saying "oil prices will go up and up and never come back". What they said is: "Oil will be getting harder and harder to get, and the time of cheap oil is over." Which, as far as I can tell, is still correct. New tech and everything, this new oil is still harder to get than anything tried before. We are nowhere near the prices of 10 years ago, are we?

And technically, it's true that the cure of high prices is in high prices... if all you worry about is prices. If you happen to worry about what else high prices might bring (like, contributions to a Great Recession that never feels quite over), then your view may be that the cure didn't cure as much as you would wish.

BlkScholes88

I think that Stephen Stork is missing the point completely here. He disregards the fact that 'low prices solve low prices' but the in the very next sentence agrees with it…

"The reason why no new significant oil deposits were discovered in the 1980s and 1990s is because… at $20 a barrel it did not make any economic sense to go out and try and discover new oil."

It is true the run up in crude prices led to large investment which spurred the growth we are seeing today. During this period however, the backend of oil curves were also moving – which is where investment decisions are largely based off. Today we seem to be in a false sense of security and the backend of oil curves are largely stable – could this be another case of the 80s/90s?

Peak oil isn't an issue now given advances in non-conventional production - though I think its an exaggeration to say the 'world is swimming in oil'. However, it's a major leap (and error) to translate this into lower prices. All this new production comes at a price – the cheap oil is gone.

You can see it in the returns for a lot the Majors, their Return on Equity etc measures peaked in '05 when oil was trading $50 a barrel. They are spending increase amount of CAPEX but if anything their reserves and production is decreasing. Breakevens on new fields like Kasahgan back this up. So I agree with the Austrian fund Manager, Peak oil isn't an issue but I don't see oil trading at $75 for any sustained period – but I guess that just makes me a fool.

the River Lea

And the 2009-09 recession had nothing to do with the collapse of the oil price? Despite the drop in demand growth, oil prices climbed back up to $100/bbl and have stayed around there ever since.

Greasy wheel

For the oil price to come down - and stay down for a long period of time (>3 years) - the cost structure of the industry has to change. Anything can happen over a period of less than 3 years given that's a pretty standard timeframe for a major project.

That could be enough crude flooding out of Iraq, Iran, Venezuela to push out the more expensive barrels and make the current long-run marginal cost of $90-$100 become $80. Or waning demand (substitution, economic effects, delayed demand responses to high prices) having a similar effect.

It could be Asian NOCs looking at assets differently and applying lower costs of capital, a pretty big effect when looking at the Oil Sands.

It could be the waning of demand for oil services unwinding some of the inflation that has built in to the sector, even if the actual activity per barrel produced doesn't change much. Labour (particularly labour), equipment, the supply chain - these could all change to make today's $90/bbl breakeven project the $70/bbl breakeven project of tomorrow...

Bob Buhr

Of course, if governments are going to limit CO2 generation to achieve a climate target of limiting the rise in global temperatures to 2oC, as was agreed at the Cancun meetings in 2010, there will absolutely have to limits placed on how much oil can be consumed-otherwise, this target won't be achievable. So having access to all this oil (and commentators are correct-it won't necessarily be cheap oil) isn't actually going to help all that much. What happens to the valuations of all these companies (not to mention market indices) then? And if we don't observe the 2oC target and bust through it, becuase, you know, free markets and all, we're looking at a pretty bad set of scenarios. Not really a triumph for anyone, actually.

r j sigmund

strange, the article i read just minutes before this said the IEA report said the Shale Boom is Only Temporary, and We'll Soon be Relying on the Middle East Again

think maybe we read the report ourselves to get past the spins...

deraesthet

little typo: it's Sachertorte not Sachetorte. And I hope they didn't drink the Grüner Veltliner while eating the cake. Not a good match. I really can't think of a "large" hedge fund in Austria.

steve from virginia

Good grief!

Peak oil hasn't gone anywhere, just buried under an avalanche of Wall Street lies and self-promotion ... including the IEA's latest 'report'.

Keep in mind:

- - Prices are low because the customers cannot earn by burning fuel, they must borrow instead. Because of credit 'problems' -- hundreds of trillion$ of dollars in unpayable debt on the books already -- there are more stringent borrowing constraints; customers are broke and unable to bid fuel prices higher.

- - Fuel extraction rate has been largely flat since 2005, new 'output' is balanced by depletion in old fields.

- - It is easier to put cars on the road than pull oil out of the ground (ocean). New fuel demand is from countries like the Philippines that are bankrupts.

- - When customers are required to bid for scarce supplies, they quickly exhaust their credit and the result is a 'crisis' somewhere. @ $106/barrel Brent, there is no immediate crisis. @ $118 a few months ago there were ugly noises about a China credit crash! Keep in mind the price that broke the market in 2008 was +$130/barrel: the market-breaking price is lower every day.

- - Because of past consumption success, there is less fuel available and the marginal cost of each next barrel relentlessly increases to the hapless driller. If the driller's customer cannot borrow the driller is out of business, period.

- - At some near point the price needed by drillers will be unaffordable to straitened customers. Then what? Greece is a good place to look because, a) it is bankrupt, b) it has no value to offer in exchange for the fuel it wastes every day, and, c) it has no fuel of its own like the rest of Europe. Because it is insolvent, Greece also cannot borrow any more. Syria and Egypt are also good places to look, where the 'drive to drive' comes against hard limits and the citizens take up machine guns so that they too might be able to sit in traffic jams like their American Cousins.

Izzy, marginal costs are inescapable and you know it, your chortling is whistling past the graveyard.

steve from virginia

This following is just wishful thinking, Hitler's phantom armies coming to rescue him in April, 1945:

" ... Key components of the increase are unconventional oil (up 10 mb/d) ... "

Unconventional is at- or near peak output in the US (Bakken and Eagle Ford). Canadian (Low EROI bitumen) is available only as long as the Alberta natural gas holds out. The gas is used to cook the bitumen. Meanwhile, unconventional plays in China, Poland ... and in the US itself ... are failures.

" ... and natural gas liquids (NGLs) linked to the increase in global gas output (up 5 mb/d)."

NGLs aren't motor fuel and gas output requires distribution infrastructure, it is local rather than global (which is why the gas price crash in the US, absence of expensive distribution infrastructure). BTW: chilling natural gas to ship it in tankers wastes 25% of the gas; energy $$$ thrown away for nothing.

" ... Conventional crude oil's share in total oil production falls, from 80% in 2012 to two-thirds in 2035."

As such, our ongoing energy crash is the easiest crisis to predict since the collapse of the US real estate bubble in 2008. The wails from businessmen aren't hard to hear now: "We never saw it coming ...!"

' ... as US light tight oil and Brazilian deepwater output step up,"

Best US light tight plays are already exploited and depleting @ 60% per well, per year, Don't believe me, check Shell Oil/Eagle Ford. Also check North Dakota Bureau of Mines and Minerals. Brazil is experiencing terminal decline as deepwater drillers fail to find any real oil (only hype oil).

- http://www.ft.com/...-00144feab7de.html

- http://www.ft.com/...-00144feabdc0.html

" ... but the share of OPEC countries in global output rises again in the 2020s, as they remain the only large source of relatively low-cost oil. Iraq is the largest single source of oil production growth ..."

Iraq's production has never met expectations and the country is in a civil war. Q: Why would any country sell a valuable item just to see it wasted? ... to put a bigger number on a rich man's computer? Why not keep it and sell it for much more (risk adjusted) later? This is Hotelling's Rule and coming to an OPEC country near you.

" ... followed by Brazil, Canada and Kazakhstan. The United States is the world's largest oil producer for much of the period to 2035."

Yes, and I pitch the seventh game of the 2014 World Series and win for the Nationals w/ a two-hit shutout. This is the nonsense that passes for analysis in the richest nations on Planet Earth in 2013. Birol and company should be taken out and shot.

June 6, 2004 | NYT, Page B07

If you're wondering about the direction of gasoline prices over the long term, forget for a moment about OPEC quotas and drilling in the Arctic National Wildlife Refuge and consider instead the matter of Hubbert's Peak. That's not a place, it's a concept developed a half-century ago by a geologist named M. King Hubbert, and it explains a lot about what's going on today at the gas pump. Hubbert argued that at a certain point oil production peaks, and thereafter it steadily declines regardless of demand. In 1956 he predicted that U.S. oil production would peak about 1970 and decline thereafter. Skeptics scoffed, but he was right.

It now appears that world oil production, about 80 million barrels a day, will soon peak. In fact, conventional oil production has already peaked and is declining. For every 10 barrels of conventional oil consumed, only four new barrels are discovered. Without the unconventional oil from tar sands, liquefied natural gas and other deposits, world production would have peaked several years ago.

Oil experts agree that hitting Hubbert's Peak is inevitable. The oil laid down by nature is finite, and almost half of it has already been extracted. The only uncertainty is when we hit the peak. Pessimists predict by 2010. Optimists say not for 30 to 40 years. Most experts expect it in 10 to 20 years. Lost in the debate are three much bigger issues: the impact of declining oil production on society, the ways to minimize its effects and when we should act. Unfortunately, politicians and policymakers have ignored Hubbert's Peak and have no plans to deal with it: If it's beyond the next election, forget it.

To appreciate how vital oil is, imagine it suddenly vanished. Virtually all transport -- autos, trucks, airplanes, ships and trains -- would stop. Without the fertilizers and insecticide made from oil, food output would plunge. Manufacturing output would also drop. Millions in colder regions would freeze.

Fortunately, oil production does not suddenly stop at Hubbert's Peak; rather, it declines steadily over time. But because production cannot meet demand, the price of oil will rapidly and continuously escalate, degrading economies and living standards. People complain now about gasoline at $3 per gallon. After Hubbert's Peak, $7 per gallon will seem cheap. Spending $150 to fill up the SUV? Ouch!

How to minimize the impact of declining oil production? Conservation and new finds can help. Higher mileage standards for autos and trucks could cut U.S. oil use by 20 percent or more. New oil fields continue to be discovered, but they are small. No giant Saudi Arabia-type fields have been found in 30 years. The small fields contribute ever diminishing amounts of oil. But while conservation and new oil can delay Hubbert's Peak and ease its impact, they cannot prevent it. Moreover, even if the United States conserves oil, other countries might not. A practical long-term, non-oil solution to the problem of Hubbert's Peak is needed.

We need new technologies, especially for transportation, which accounts for two-thirds of U.S. oil consumption. Possible options are synthetic fuels from coal, hydrogen fuel from nuclear and renewable power sources, and electrified transport: light rail, rail and maglev. Processes for synthetic gasoline, diesel and jet fuel are well developed but expensive. The environmental problems from coal -- mining, carbon dioxide emissions and other pollutants -- are serious and require more attention. Hydrogen fuel produced by electrolysis from renewable power sources is environmentally clean, but it has serious technical problems. Producing the hydrogen equivalent in energy to the oil now used in U.S. transport would require 10 trillion kilowatt hours of electric energy; we would have to triple our electric generation capacity.

A more practical approach would be the electrification of transport. Switching half the truck and personal auto miles to electrified transport would require an increase in electric generation capacity of only 10 percent. Electrified transport is clean, non-polluting and energy-efficient. Light rail and rail systems are already in wide use. First- generation maglev systems are operating, and lower-cost second-generation systems are being developed.

As oil production declines, the combination of electrified transport and synthetic fuels from coal can meet the challenge. Hydrogen fuel is probably not practical, but research and development on it should continue in the hope of a breakthrough.

Whatever non-oil transport technologies prove best, making the transition from our present systems will take many years. It took decades for the first automobiles and airplanes to evolve into effective systems, and decades to build the interstate highway network. We can't afford to wait until Hubbert's Peak occurs. We should begin now to plan and implement the new, non-oil technologies. If we don't, our economy and living standard will be in serious trouble.

James C. Jordan is an energy and environment policy consultant and a former energy program director for the Navy. James R. Powell, a former senior scientist at Brookhaven National Laboratory, was a co-recipient, with Gordon Danby, of the 2000 Benjamin Franklin Medal in Engineering, for their invention of superconducting maglev technology. He is a director of Maglev 2000 of Florida Corp.

8/25/2013 | Hoocoodanode

westexas:And then there is the global oil supply situation.

While currently increasing US crude oil (crude + condensate) production is very helpful on a number of fronts, it is very likely that we will continue to show the post-1970 "Undulating Decline" pattern that we have seen in US crude oil production, as new sources of oil have come on line, and then inevitably peaked and declined (US crude oil production, which will probably average about 7.5 mbpd in 2013, is currently about 25% below the 1970 peak rate of 9.6 mbpd).

For example, EIA data show that crude oil production from Alaska increased at 26%/year from 1976 to 1985, which contributed to a secondary, but lower, post-1970 US crude oil production peak of 9.0 mbpd in 1985 (up from a low of 8.1 mbpd in 1976), versus the 1970 peak rate of 9.6 mbpd. Because of the strong rate of increase in Alaskan crude oil production from 1976 to 1985, the US was actually on track, in the mid-Eighties, to become crude oil self-sufficient in about 10 years, but then the inevitable happened, and the rate of increase in Alaskan crude oil production slowed, and then started declining in 1989, resulting in a post-1970 "Undulating Decline" pattern. Note that the 1976 to 1985 rate of increase in annual Alaskan crude oil production (26%/year) exceeded the estimated 2008 to 2013 rate of increase in combined annual crude oil production from Texas + North Dakota (20%/year).

The very slow increase in global crude oil production since 2005 (and the average annual post-2005 global crude oil production rate is below the 2005 rate of 74 mbpd), combined with a material post-2005 decline in Global net oil exports, have resulted in high crude oil prices that have provided considerable incentives for US oil companies to make money in tight/shale plays. But I think that the assertion by many in the Cornucopian camp that shale plays will result in a virtually infinite rate of increase in global crude oil production is wildly unrealistic.

We are facing high--and increasing--overall decline rates from existing oil wells in the US. At a 10%/year overall decline rate, which in my opinion is conservative, the US oil industry, in order to just maintain the 2013 crude oil production rate, would have to put online the productive equivalent of the current production from every oil field in the United States of America over the next 10 years, from the Gulf of Mexico to the Eagle Ford, to the Permian Basin, to the Bakken to Alaska. Or, at a 10%/year decline rate from existing wells, we would need the current productive equivalent of 10 Bakken Plays over the next 10 years, just to maintain current production.

On the natural gas side, a recent Citi Research report (estimating a 24%/year decline rate in US natural gas production from existing wells), implies that the industry has to replace virtually 100% of current US gas production in four years, just to maintain a dry natural gas production rate of 66 BCF/day. Or, at a 24%/year decline rate, we would need the productive equivalent of the peak production rate of 30 Barnett Shale Plays over the next 10 years, just to maintain current production.

The dominant pattern that we have seen globally, at least through 2012, is that developed net oil importing countries like the US were gradually being forced out of the market for exported oil, via price rationing, as the developing countries, led by China, consumed an increasing share of a declining post-2005 volume of global net oil exports.

For more information on net oil exports, you can search for: ASPO + Export Capacity Index.

bearly

Stagflationary Mark[Even after the 28.1% in 2012, the 780 thousand housing starts in 2012 were the fourth lowest on an annual basis since the Census Bureau started tracking starts in 1959]

We've passed peak IP, peak oil peak on-and-on.... so it wouldn't be much of a stretch to say we have passed peak homebuilding.

The future is still bright? What's the word "still" doing there? It's either bright or it isn't, right?

Alternative CredAbility Consumer Distress Index

As seen in the following chart, I have chosen to use the median instead of the average. Why? A few good apples can't purify the barrel!

Hey! Just opinions.

arthur_dent

Kauai_Kahuna wrote:

Well, if you listen to the posters here your most likely living in a bunker and have missed the best bull market in my lifetime.

not sure how old you are but to put things in context. If we are at the end of a secular Bear market, then the comparison is it is now 1946 or 1983. Just scratched the surface of the Bull to come. If on the other hand we are still in the grips of a Bear then there is also plenty of time. Think of the extra-ordinary measures that have been taken to date and the growth the US and the world has experienced in the last 5 years. If historical growth does not materialize soon, this Bull is dead.

bearly

km4Rob Dawg wrote:

What new reader would even bother long enough to discover the ignore button.

What I am beginning to wonder is whether this blog is doing a service by cheerleading for this abysmal economy and leadership.

StagMark's posts are far more representative as a barometer of what is going on, and continuing down this path of destroying productive capacity, stripping capital out of this nation to build elsewhere unfettered is hardly Rose Colored Glasses

The future looks Dooooooooooooooom!!!

Sure The Future is still Bright! if you're in the 2% club33 Shocking Facts Which Show How Badly The Economy Has Tanked Under Obama | Zero Hedge

My top picks ( hard to choose )

2) Since Obama has been president, seven out of every eight jobs that have been "created" in the U.S. economy have been part-time jobs

4) It is hard to believe, but an astounding 53 percent of all American workers now make less than $30,000 a year.

7) During the first four years of Obama, the number of Americans "not in the labor force" soared by an astounding 8,332,000. That far exceeds any previous four year total.

8) According to the U.S. Census Bureau, the middle class is taking home a smaller share of the overall income pie than has ever been recorded before.

9) When Obama was elected, the homeownership rate in the United States was 67.5 percent. Today, it is 65.0 percent. That is the lowest that it has been in 18 years.

14) The poverty rate has shot up to 16.1 percent. That is actually higher than when the War on Poverty began in 1965.

16) When Barack Obama entered the White House, there were about 32 million Americans on food stamps. Today, there are more than 47 million Americans on food stamps.

20) Health insurance costs have risen by 29 percent since Barack Obama became president, and Obamacare is going to make things far worse.

22) According to economist Tim Kane, the following is how the number of startup jobs per 1000 Americans breaks down by presidential administration... Bush Sr.: 11.3 Clinton: 11.2 Bush Jr.: 10.8 Obama: 7.8

24) According to one recent survey, 76 percent of all Americans are living paycheck to paycheck.

30) At the end of 2008, the Federal Reserve held $475.9 billion worth of U.S. Treasury bonds. Today, Fed holdings of U.S. Treasury bonds have skyrocketed past the 2 trillion dollar mark.

31) When Barack Obama was first elected, the U.S. debt to GDP ratio was under 70 percent. Today, it is up to 101 percent.

32) During Obama's first term, the federal government accumulated more new debt than it did under the first 42 U.S presidents combined.

33) When you break it down, the amount of new debt accumulated by the U.S. government during Obama's first term comes to approximately $50,521 for every single household in the United States. Are you able to pay your share?bearly

JPSaturn_ls1 wrote:

whether the economic signals grind upward

The signal that matters to just about anyone that matters is the stock market. The apparent path to correcting the economic problems is to use all the apparatus & every means possible to move the stock market indices higher.

It cost a lot to move the needles. And at some point there won't be enough ammunition available to keep kicking the stock market to new highs and we still have all the underlying problems. Wasted ammo.

Then what ?

The Gentlemen's Book of Etiquette and Manual of Politeness: Being a Complete ... - Cecil B. Hartley - Google Books

Steve Weston

I am your greatest admirer and have said so in my book. HOWEVER:

- This is the 20 teens, not the 90's

- You did not mention the economic impact of the price of gasoline and crude oil in your forecast.

- You did not mention the impact of China on the US manufacturing base.

- You did not mention the declining demand for US products in the EU.

I wish you would comment on the impact of the above issues and why, in light of the above, you're so optimistic

Steve Weston SalesSuperiority.com

Aug 24, 2013 | Zero Hedge

For roughly forty years (since the report was published in 1972), technology has pulled one magic rabbit after another out of the hat, making a mockery of the claims that there were limits on consumption and resource extraction: the green revolution and fossil-fuel fertilizers expanded food production, new supergiant oil fields and improved drilling technologies opened up vast new energy reserves, and improved technologies led to more efficient use of resources. The success of the past four decades in pushing back looming limits has created a widespread confidence that technology can solve any apparent limits. For example, if the seas have been stripped of fish, then aquaculture will fill the desire for fresh fish. Presto-magico. But what if the technological improvements are entering a terminal phase of diminishing returns? What if the "solutions" don't really replace what has been destroyed? For example, the ecology of the open ocean is not restored by aquaculture; rather, it is further harmed by poor aquaculture practices.

goldfish1

what if the technological improvements are entering a terminal phase of diminishing returns

"what if" done already happened.

adornosghost

Lurking Lawyer wrote:

Inflation is always under-reported.

"Capex compression is a term we use to describe the reduction of upstream spending by the oil companies when their exploration and production costs are rising faster than their oil revenues. That's what's happening today. Hess is divesting oil producing properties to increase profits; BP has shelved the deepwater Mad Dog Phase 2 project in the Gulf of Mexico. This is occurring because oil prices haven't been increasing, and costs have. So oil companies are looking at their portfolio of projects and deciding to postpone or cancel some of them. Were the oil supply rising quickly and oil prices falling, this sort of capital restraint would be normal-the usual boom-bust cycle of the industry. But oil is still in short supply, and very few of the large oil companies have been able to hold oil production over the last few years-even as they were investing massively in oil exploration and production. Now, they are actually reducing investment in upstream projects, even in the face of historically high oil prices and falling production. That's capex compression."

August 9, 2013 | charles hugh smith

There are real-world consequences to over-issuing credit and currency.

Creating credit is the same as printing money when interest rates are zero. If I borrow $1 billion at 0% from the Federal Reserve (because I'm a Too Big to Fail bank, for example), it is functionally equivalent to printing $1 billion in cash currency because the credit costs nothing.

Let's say there is a .25% interest rate cost and printing cash also costs .25%. The carrying costs of both are trivial.

As a result, those with access to cheap credit have the equivalent of a printing press. I illustrated this recently with an example of three traders entering a trading fair: Trader 1 only has cash that has been earned and saved; Trader 2 has access to leveraged credit (i.e. borrowing $100 based on $10 of cash collateral) and Trader 3 has a printing press that creates cash currency. The Financial System Doesn't Just Enable Theft, It Is Theft (July 31, 2013)

As a result, Traders 2 and 3 could buy a lot more real-world goods at the fair than Trader 1, enabling the two traders with essentially unlimited credit/cash to reap enormous profits on carry-trades and other speculative trading.

Longtime contributor Harun I. recently pointed out an even more destructive consequence: resource wars.

Not only can trader 2 and 3 purchase more goods than trader 1. Trader 2 and 3 have no limit on what they can bid and therefore can price trader 1 out of the market completely. This can and does lead to economic warfare and control over states that have to import the majority of their food and/or energy.This is a profound insight. Let's take two states, both of which issue credit and currency. The first is the U.S., and the second is a beleaguered state (State 2) with too much public and private debt and little collateral (for example, gold reserves) to back its currency.

The second state can issue as much currency and credit as it chooses, but the value of that capital falls in direct proportion to the quantity issued. Those sellers who accept this credit or cash as payment for real-world goods have little trust that the money issued by State 2 will retain its current purchasing power in the future. As a result, there is a huge risk premium priced into the trade, and relatively few traders will accept the risk of trading a potentially worthless currency for their scarce resources.

For whatever reason (and there are more than one), the trader trusts that the U.S. dollar will retain its purchasing power long enough for the trader to trade it for some other asset or form of capital, or even hold it as collateral for future loans.

Harun's point is the U.S. can outbid State 2 for oil or any other resource because it's essentially free for the U.S. to issue credit and cash. The price for the resources in U.S. dollars will soar in a bidding war, and while the U.S. can simply issue more credit/cash, State 2 is rapidly impoverished as the cost of essential resources rises.

Eventually this leads to a bidding war for trust: Whose credit/cash will be trusted to retain its purchasing power? There is a grand irony here, of course; as issuers of credit/cash attempt to debase their currency to boost their exports, their debased currency buys fewer real-world resources.

In a global credit crisis created by the over-issuance of credit/debt, which currencies will lose trust and which will gain trust? Those which retain or gain trust will enrich the issuer and those who lose trust will impoverish the issuer.

Nations that lose this bidding war for trust may reckon it's "cheaper" to wrest control of the needed resources by force rather than go through the arduous steps necessary to rebuild lost trust in their credit and currency.

In sum: there are real-world consequences to over-issuing credit and currency.

azurite wrote on Tue, 8/6/2013 - 8:55 am

"More than 35 percent of public transportation buses in the United States now use alternative fuels such as CNG or hybrid (electric-diesel) systems, according to the American Public Transportation Association, whose figures for early 2011 showed that 18.6 percent of transit buses nationwide ran on CNG, liquefied natural gas and blends."Miami-Dade Transit may convert buses to natural gas - Miami-Dade - MiamiHerald.com

By Rob Wile, Business Insider

Some surprising people, including the CEO of Exxon (XOM), think true American energy independence is actually a bad idea.

Add Berkshire Hathaway (BRK-B) Vice-Chairman Charlie Munger's name to that list.

Munger recently spoke at the Committee of 100 U.S.-China relations conference (via Farnam Street Blog's Shane Parrish notes and Tim Harford).

The moderator asked Munger a basic question about which sectors Berkshire believes are ripe for growth.

He responded by begging off that question and launched instead into a critique of America's energy policy, especially the continued insistence on independence.

Related: Oil Tops $100 Again, Here's the 1 Thing Energy Investors Need to Watch

But unlike other commentators who've refuted the concept, Munger approached the question from a more apocalyptic angle:

Here's Parrish's transcript:

If energy independence was such a good thing, let's just imagine that we go back to 1930 or something like that and we were hell bent to have total energy independence from all the foreigners. And we just drill and use every technique we can and we produce our hydrocarbon reserves which are absolutely certain to be limited.

Well, by now have way less in reserve and are way less energy independent. In trying to get energy independence we would have destroyed our safety stock of oil within our own borders.

Oil and gas are absolutely certain to become incredibly short and very high priced. And of course the United States has a problem and China has a worse problem.

And China has the correct solution. Imported oil is not your enemy it's your friend.

Every barrel that you use up that comes from somebody else is a barrel of your precious oil which you're going to need to feed your people and maintain your civilization.

And what responsible people do with a Confucius ethos is they suffer now to benefit themselves, their families, and their countrymen later. And the way to do that is to go very slow on producing your own (domestic) oil. You want to produce just enough so that you keep up on all of the technology. And don't mind at all paying prices that look ruinous for foreign oil. It's going to get way worse later.

Every barrel of foreign oil that you use up instead of using up your own - you're going to eventually realize you were doing the right thing.

Energy is one of the unique areas, he continued, where free-market policies end up causing more problems than they solve. In the case of energy, he said, governments should step in and encourage imports (it should be noted, of course, that this situation already partially exists, since exporting U.S. crude has been banned since the '70s):

Why are the policy makers in both countries so stupid on this single issue because they are not stupid generally? I think that it's partly the economists who have caused the problem. Because they have this theory that if people react in a free market that it's much better than any type of government planning but there is a small class of problems where it's better to think the things through in terms of the basic science and ignore these signals from the market.

Now if I'm right in this, there are a whole lot of lessons that logically follow:

- Foreign oil is your friend not your enemy;

- You want to produce your own assets slow; …

- The oil in the ground you're not producing is a national treasure; … running out of hydrocarbons is like running out of civilization. All this trade, all these drugs, fertilizers, fungicides, etc. … which China needs to eat with a population so much, they all come from hydrocarbons.

And it is not at all clear that there is any substitute. When the hydrocarbons are gone, I don't think the chemists will be able to simply mix up a vat and there will be more hydrocarbons. It's conceivable, of course, that they could but it's not the way to bet. I think we should all be quite conservative and we should pay no attention to these silly economics and politicians that tell us to become energy independent.

So what should we be doing instead?

Munger believes we need to shift resources away from producing whatever is left in the ground and save it for his purported day of reckoning. Rather, we should be investing in all the other forms of energy out there:

We have a brain block on this issue. We should behave now to do on purpose what we did by accident: we conserved some of our oil because we were not aggressive enough and smart enough to get it out faster, that was accidentally doing the right thing. Now we should do on purpose what we formally did by accident. We should conserve and subsidize new forms of energy … we should suppose these big national grids.

Posted by Gail the Actuary on April 15, 2013 - 6:02am

Recently, I explained how high oil prices can bring on financial collapse for oil importers. In this post, I'll discuss the flip side of the situation: how oil exporters reach financial collapse.

Topic: Economics/Finance

Tags: egypt, financial collapse, fsu, oil exports, oil prices, syria, venezuela, list all tags]Unfortunately, we have many examples of countries that were oil exporters, but are dealing with collapse situations. Egypt, Syria, and Yemen all have had political disruptions since 2011. These may not be called financial collapse, but they all took place as the country's oil exports decreased and as the price of imported food rose. Another example is the Former Soviet Union (FSU). It collapsed in 1991, after a period of low oil prices, in what looks very much like a financial collapse.

There are several dynamics at work in the financial collapse of oil exporters:

- Oil exporters are often dependent on oil export revenue to fund government programs.

- The need for government programs grows as population grows and as the price of food rises.

- The amount of oil that can be extracted in a given year often declines over time, as initial stores are depleted.

- Exports often decline even more rapidly than oil supply, because of rising oil consumption as population grows.

In general, high oil prices are good for oil exporters (except the effect on food prices). At the same time, oil importers strongly prefer low oil prices. As a result, we end up with a price tug of war between oil importers and oil exporters.

One additional issue is declining Energy Return on Energy Invested. Countries often have the option of reducing their rate of decline by adding production in areas which are more expensive to drill (say deeper, smaller locations offshore Norway) or by using enhanced oil recovery methods. Such approaches add costs (and energy use), and further add to the price that oil exporters need for their product.

Egypt, Syria, and Yemen

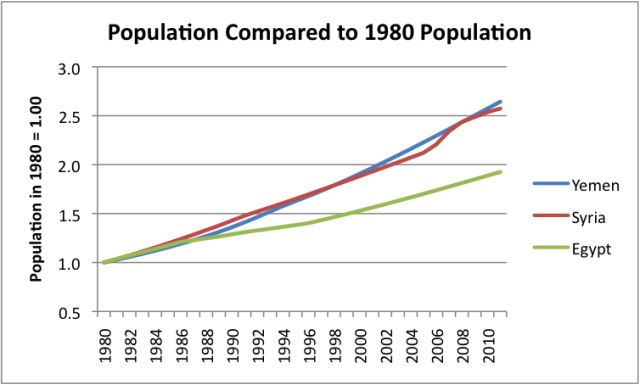

Egypt, Syria, and Yemen are three countries that the press would say are suffering from the continuing impact of the Arab Spring revolutions, which began in 2011, or of civil war. The similarity of the oil production and consumption charts for the three countries (shown below) suggests that declining oil exports likely played a major role as well.

In all three countries, oil production rose and then began to fall (Figures 1, 2, and 3). At the same time, oil consumption rose. The two lines–production and consumption–come very close to meeting in 2011, indicating that oil exports are at that point dropping to 0.

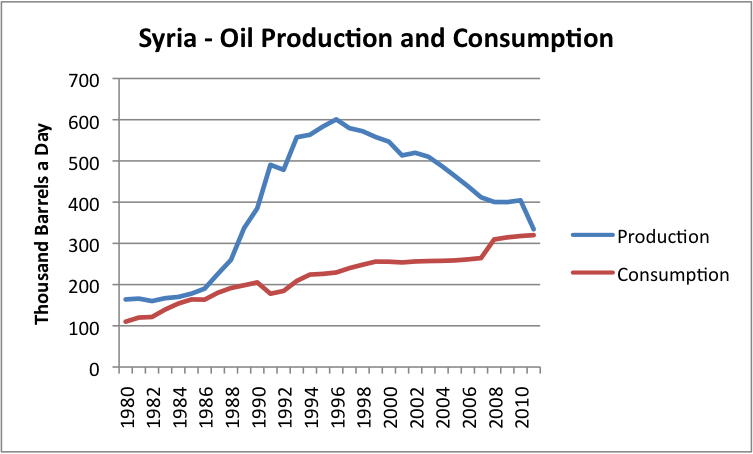

Figure 1. Oil production and consumption for Syria, based on EIA data. (Both are on an "all liquids" basis.)

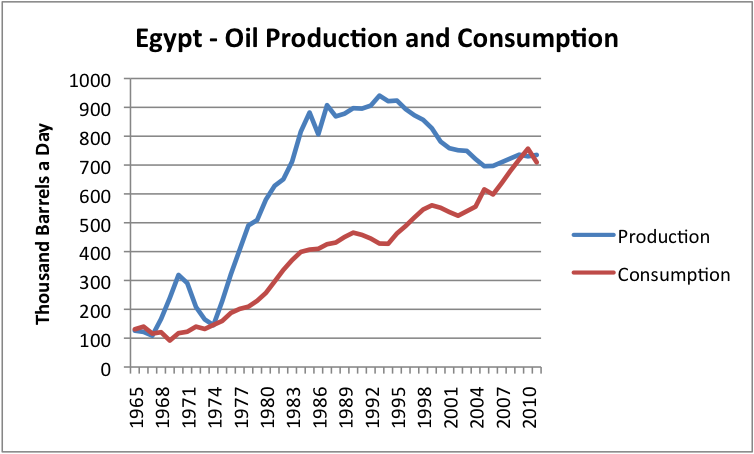

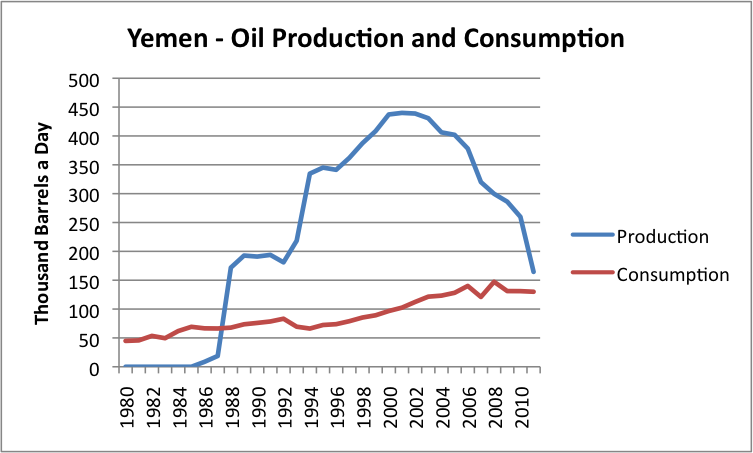

Figure 2. Oil production and consumption for Egypt, based on BP's 2012 Statistical Review of World Energy.

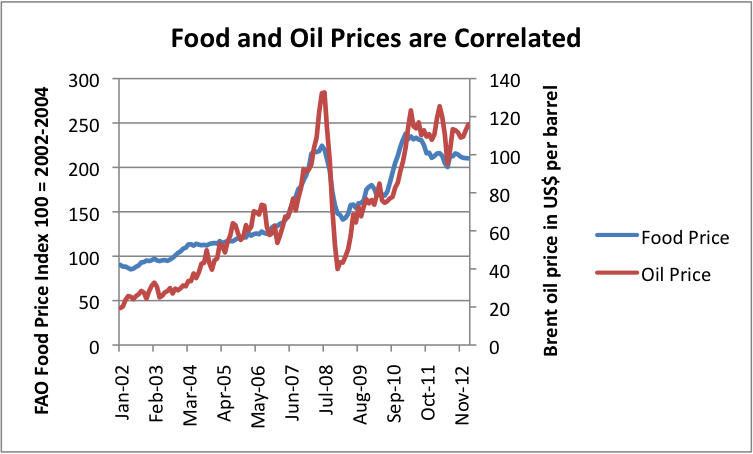

Figure 3. Oil production and consumption for Yemen, based on EIA data. (Both are on an "all liquids" basis.) To make matters worse, the three countries are in an arid part of the world, where a large share of food must be imported. Oil prices and food prices tend to rise at the same time (Figure 4, below). By 2011, both food and oil prices were high. In fact, both prices have tended to stay high. Now, these countries find themselves with the unpleasant problem of paying for the higher cost of imported food (grown and transported with oil), so indirectly they are becoming an oil importer instead of an oil exporter.

Figure 4. Food and oil prices tend to rise at the same time. Based on data of the FAO and the EIA. Faced with less revenue from oil exports, and higher prices of food imports, these countries find themselves with a permanent mismatch between revenue and expenses. Part of the revenue mismatch relates to subsidies offered to poor residents. With higher food and oil prices, the funding needed for subsidies rises rapidly, even as oil exports drop to close to zero.

One issue that makes the situation worse is the huge rise in population that came with increased prosperity. Population has nearly doubled since 1980 in Egypt, and has more than doubled in both Syria and Yemen (Figure 5, below).

Figure 5. Ratio of population in later years to population in 1980, based on EIA data. All in all, the situation is very bad. These countries admittedly do have other resources, such as grazing land for animals, food crop production, and in some cases natural gas exports, but the loss of oil exports puts a hole in their budgets. If oil production continues to drop in the future, both jobs and local oil consumption are likely to be affected as well. (This is a link to a post I wrote about the Egyptian situation two years ago.)

I tried to put together an index of the relative dependence of various countries on oil exports, by comparing the value of oil exports to Gross National Income. Based on exports before the recent drop-off, Yemen's index is around 30%; Syria and Egypt are a little under 10%. The index no doubt understates the role of oil, because it does not include the oil the country uses itself, or the impact of any natural gas industry. It also excludes indirect jobs, like that of grocery store owner or taxi driver.

If Egypt and Syria are indeed collapsing with what seems like low dependence on oil exports, it makes one wonder about the impact if Saudi Arabia's (index over 70%) or Libya's (index about 60%) oil extraction would drop.

The Collapse of the Former Soviet Union

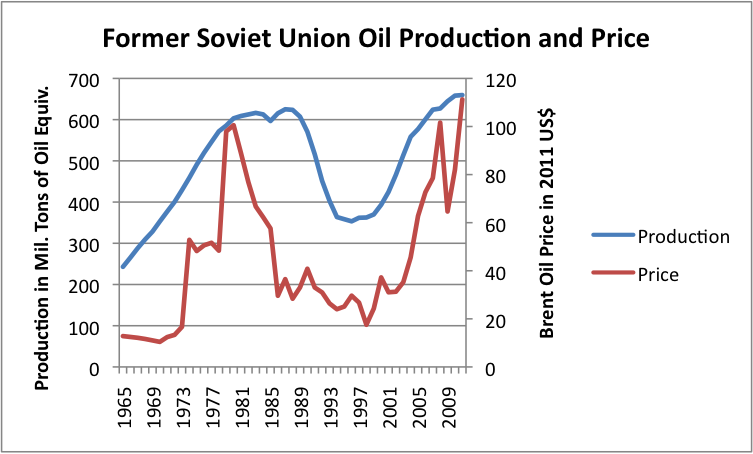

The Soviet Union was an oil exporter and a major world power, prior to its collapse in 1991. While there are many views as to what led to this collapse, one issue seems to be a drop in oil price in the early 1980s.

Figure 6. Former Soviet Union oil production and price in 2011$, based on data from BP's 2012 Statistical Review of World Energy. The drop in oil prices did not lead to an immediate decline in oil production (Figure 6), most likely because the cost of maintaining production on a field that has recently developed, is low for a few years. What is expensive is the up-front cost of bringing new fields on line. These were not added, causing a decline in production, after a few years.

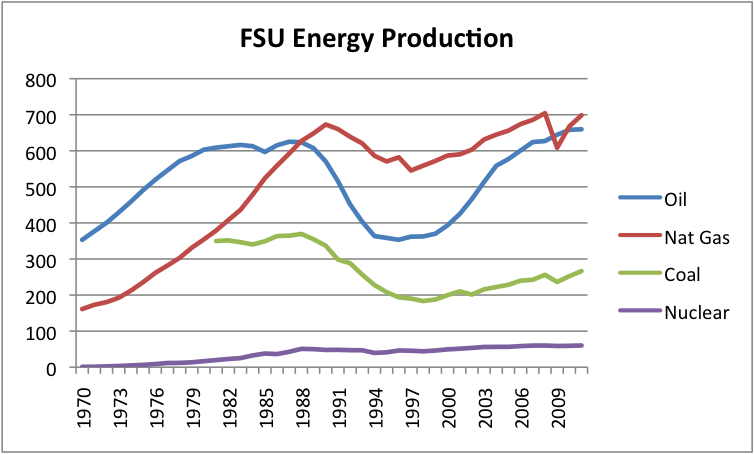

Russia's energy data shows the marks of the financial collapse building, prior to 1991. Revenue from oil exports dropped in the mid 1980s, because of the lower oil price. Oil production started declining in 1987, four years before the collapse. Other types of energy production started declining as well, as if a recession were underway, pulling the economy down in all areas.

Figure 7. Former Soviet Union Energy production by type (hydroelectric omitted), based on BP's 2012 Statistical Review of World Energy. Every type of energy production (except hydropower, not shown) dropped back during this period, even coal and nuclear, with decreases beginning prior to 1991. Population growth started slowing prior to 1991 as well. Eventually, the government collapsed, after continuing recession.

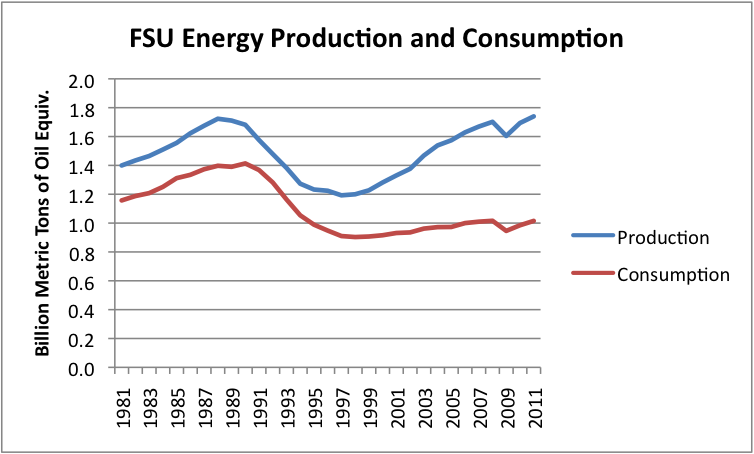

Figure 8. Former Soviet Union energy production and consumption, based on BP's 2012 Statistical Review of World Energy. The FSU never regained its former stature as a manufacturing country, even when oil production rose, after oil prices rebounded. With little manufacturing, energy consumption has remained far below its pre-1991 levels (Figure 8).

I visited Russia in 2012, and saw for myself a little of the current situation. One problem is that its cost structure (based primarily on oil and gas which is now high-priced, and workers who need wages to pay for these fuels) is not competitive with the low-cost structure of the Chinese and Indians. Another issue is the poor condition of Russia's infrastructure (roads, bridges, water pipelines, etc.) due to neglect during the time of its collapse. With the high cost of oil, it is expensive to make repairs and add new infrastructure.

In terms of my index, Russia's oil exports now amount to a little less than 20% of Gross National Income.

Collapse in Countries with Declining Exports

Egypt, Syria, and Yemen are examples of countries whose exports have pretty much disappeared, causing great crisis. But how about countries with earlier declines in production? To some extent, there were not many problems in the 2003 to 2008 period, because declines in oil exports could often be offset by increases in oil prices.

One country that stands out, though, is Argentina, with problems both before and after the 2003-2008 period.

Figure 9. Oil and Gas Production of Argentina, based on EIA data (total liquids). Argentina's oil production hit a peak in 1998, and began dropping in 1999. Oil prices were at an unusually low level in the 1998 to 2002 period. This timing coincided precisely with it first economic crisis, which came in 1999 to 2002. Oil prices rose in the 2003 to 2008 period, and Argentina's problems seemed to disappear.

Now Argentina's oil exports are very low, and in 2012 and 2013, the country is again having financial problems. Argentina's economy is well diversified, so a person wouldn't think that oil would play a big role. (My index of the role of oil exports was only about 2%, as of 2008.) But oil problems overlay any other problems a country may have. If a country has a tendency to overspend its income, or over-promise subsidies, any reduction in oil income will tend to magnify this effect. When making plans, it is easy to overlook the fact that the benefit from oil income is temporary.

Target Break-Even Brent Oil Prices

Many large oil exporters include revenue from oil exports in a country's annual budget. This is quite different from the cost of pulling the oil out of the ground. It is the money governments collect, as taxes or revenue sharing agreements or leases, to support their programs. With rising population, and often with declining exports, oil exporters find that they need higher prices each year, just to make their budgets balance.

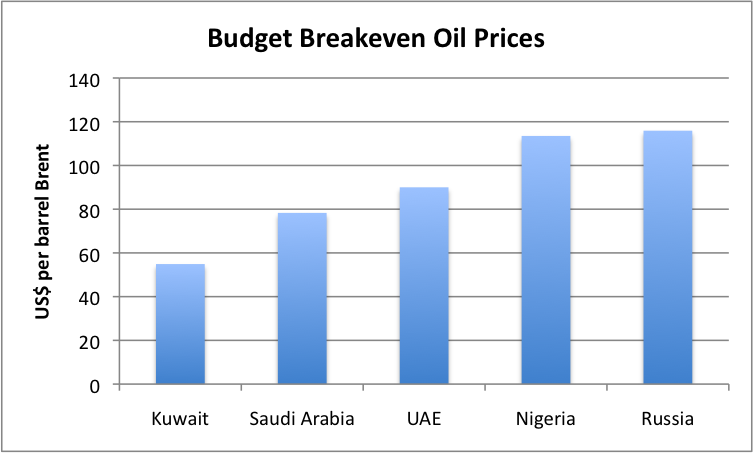

Figure 10 provides some Deutche Bank estimates of budget break-even oil prices.

Figure 10. Budget breakeven oil prices, based on a Deutche Bank analysis provided in a presentation by Mark Lewis. Note that the indicated break-even prices for Nigeria and Russia are above current Brent price levels. (The current Brent Crude oil price is $106.) An estimate from Energy Policy Information Center (EPIC) shows Venezuela's break-even price to be a little higher than Russia's, and Iran's between that of Nigeria and Russia. According to EPIC, Iraq's break-even is in the $80 to $100 barrel range. The Saudi Arabian oil minister was quoted on January 16, 2013 as saying that the country needs oil prices averaging $100 barrel.

One concern is that these break-even prices will keep rising. Another concern is that countries "at the margin" will find it difficult to reach their price targets.

One country of concern is Venezuela. It has a very high break-even price, and recently underwent a leadership change. It also has a tendency to spend oil revenue, even before the oil is pulled from the ground, through loan programs from the Chinese.