|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

|

|

|

|

The essence of Great condensate con was aptly formulated by Jeffrey Brown in this

econbrowser.com post (

http://econbrowser.com/archives/2016/01/world-oil-supply-and-demand#comment-194595My premise is that US (and perhaps global) refiners hit, late in 2014, the upper limit of the volume of condensate that they could process, if they wanted to maintain their distillate and heavier output–resulting in a build in condensate inventories, reflected as a year over year build of 100 million barrels in US C+C (Crude + Condensate) inventories.

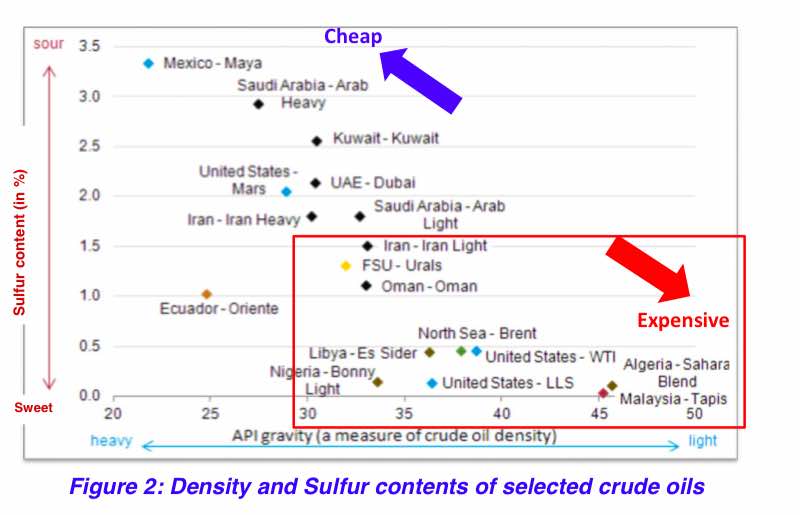

Therefore, in my opinion the US and (and perhaps globally) C+C inventory data are fundamentally flawed, when it comes to actual crude oil inventory data. The most common dividing line between actual crude oil and condensate is 45 API gravity, although the distillate yield drops off considerably just going from 39 API to 42 API gravity crude, and the upper limit for WTI crude oil is 42 API. . . .

Note that (in 2015) 22% of US Lower 48 C+C production consists of condensate (45+ API gravity) and note that about 40% of US Lower 48 C+C production exceeds the maximum API gravity for WTI crude oil (42 API).

Similar observations can be found in

http://www.reuters.com/article/2015/03/23/us-usa-refiners-trucks-analysis-idUSKBN0MJ09520150323In a pressing quest to secure the best possible crude, U.S. refiners are increasingly going straight to the source.

Firms such as Marathon Petroleum Corp and Delek U.S. Holdings are buying up tanker trucks and extending local pipeline networks in order to get more oil directly from the wellhead, seeking to cut back on blended crude cocktails they say can leave a foul aftertaste. . . .

Many executives say that the crude oil blends being created in Cushing are often substandard approximations of West Texas Intermediate (WTI), the longstanding U.S. benchmark familiar to, and favored by, many refiners in the region.

Typical light-sweet WTI crude has an API gravity of about 38 to 40. Condensate, or super-light crude that is abundant in most U.S. shale patches, ranges from 45 to 60 or higher. Western Canadian Select, itself a blend, is about 20.

While the blends of these crudes may technically meet the API gravity ceiling of 42 at Cushing, industry players say the mixes can be inconsistent in makeup and generate less income because the most desirable stuff is often missing.

The blends tend to produce a higher proportion of fuel at two ends of the spectrum: light ends like gasoline, demand for which has dimmed in recent years, and lower-value heavy products like fuel oil and asphalt. What’s missing are middle distillates like diesel, where growing demand and profitability lies.

The distinction between crude and condensate is a matter of opinion. One standard the energy industry uses to compare different types of oil is called API gravity – a measure of how heavy or light petroleum is relative to water. Lighter crudes have higher gravity. For instance, West Texas Intermediate – known as WTI – is a predominant U.S. light crude and has traditionally measured an API gravity of 39 degrees on this scale. Anything above 45 degrees API can be considered condensate, depending on who you ask. Some of the stuff pouring out of wells in Texas, North Dakota, and Colorado is coming in at a range of 50 to 60 degrees API.

In the USA condensate is extracted in large quantities as a byproduct of gas producing wells from Texas to Pennsylvania. When underground condensate is mostly a gas, but it condenses into a liquid when pumped to the surface. Condensate was the natural gas production boom’s redheaded stepchild. Until natural gas production started to ramp up in U. S. shale formations, the distinction between crude and condensate didn’t matter much, and the small amounts of condensate pumped from the ground were left mixed in the crude. Now as much as 12% of daily U.S. crude production might qualify as condensate, according to energy investment bank Simmons & Co. International.

Condensate contains only around 60 – 70% of the energy content of crude oil in the same volume.

Natural-gas condensate - Wikipedia, the free encyclopedia

Natural-gas condensate is a low-density mixture of hydrocarbon liquids that are present as gaseous components in the raw natural gas produced from many natural gas fields. It condenses out of the raw gas if the temperature is reduced to below the hydrocarbon dew point temperature of the raw gas.condensate - Schlumberger Oilfield GlossaryThe natural gas condensate is also referred to as simply condensate, or gas condensate, or sometimes natural gasoline because it contains hydrocarbons within the gasoline boiling range. Raw natural gas may come from any one of three types of gas wells:[

- Crude oil wells — Raw natural gas that comes from crude oil wells is called associated gas. This gas can exist separate from the crude oil in the underground formation, or dissolved in the crude oil. Condensate produced from oil wells is often referred to as lease condensate.[3]

- Dry gas wells —These wells typically produce only raw natural gas that does not contain any hydrocarbon liquids. Such gas is called non-associated gas. Condensate from dry gas is extracted at gas processing plants and, hence, is often referred to as plant condensate.[3]

- Condensate wells —These wells produce raw natural gas along with natural gas liquid. Such gas is also called associated gas and often referred to as wet gas.

There are many condensate sources worldwide and each has its own unique gas condensate composition. However, in general, gas condensate has a specific gravity ranging from 0.5 to 0.8, and is composed of hydrocarbons such as propane, butane, pentane, hexane, etc. Natural gas compounds with more carbon atoms (e.g. pentane, or blends of butane, pentane and other hydrocarbons with additional carbon atoms) exist as liquids at ambient temperatures.[4] Additionally, condensate may contain additional impurities such as:[5][6][7][8]

- Hydrogen sulfide (H2S)

- Thiols traditionally also called mercaptans (denoted as RSH, where R is an organic group such as methyl, ethyl, etc.)

- Carbon dioxide (CO2)

- Straight-chain alkanes having from 2 to 12 carbon atoms (denoted as C

2 to C

12)- Cyclohexane and perhaps other naphthenes

- Aromatics (benzene, toluene, xylenes, and ethylbenzene)

A low-density, high-API gravity liquid hydrocarbon phase that generally occurs in association with natural gas. Its presence as a liquid phase depends on temperature and pressure conditions in the reservoir allowing condensation of liquid from vapor. The production of condensate reservoirs can be complicated because of the pressure sensitivity of some condensates: During production, there is a risk of the condensate changing from gas to liquid if the reservoir pressure drops below the dew point during production. Reservoir pressure can be maintained by fluid injection if gas production is preferable to liquid production. Gas produced in association with condensate is called wet gas. The API gravity of condensate is typically 50 degrees to 120 degrees.

Chemical composition of condensate is different then gasoline produced by cracking and it has a lower octane number than conventional commercial distilled gasoline (Natural gasoline - Wikipedia, the free encyclopedia):

Natural gasoline is a natural gas liquid with a vapor pressure intermediate between natural gas condensate (drip gas) and liquefied petroleum gas and has a boiling point within the range of gasoline. The typical gravity of natural gasoline is around 80 API.This hydrocarbon mixture is liquid at ambient pressure and temperature. It is volatile and unstable but can be blended with other hydrocarbons to produce commercial gasoline.

The natural gas hydrocarbons mixture is mostly pentanes and heavier (smaller amounts of C6 and C6+), extracted from natural gas, that meets vapor pressure, end-point, and other specifications for natural gasoline set by the Gas Processors Association.[1] Includes isopentane which is a saturated branch-chain hydrocarbon, (C5H12), obtained by fractionation of natural gasoline or isomerization of normal pentane.[2]

Natural gasoline is often used to denature ethanol produced for E85. Natural gasoline has a lower octane content than conventional commercial distilled gasoline, so it cannot normally be used by itself for fuel for modern automobiles. However, when mixed with high concentrations of ethanol such as mid-level blends, like E50 or E85, the octane content is raised high enough to be used easily in flex-fuel vehicles. It may be sourced from production of natural gas wells (see "drip gas") or may be produced by extraction processes [3] in the field, as opposed to refinery cracking of conventional gasoline.

http://www.reuters.com/article/2015/03/23/us-usa-refiners-trucks-analysis-idUSKBN0MJ09520150323

In a pressing quest to secure the best possible crude, U.S. refiners are increasingly going straight to the source.

Firms such as Marathon Petroleum Corp and Delek U.S. Holdings are buying up tanker trucks and extending local pipeline networks in order to get more oil directly from the wellhead, seeking to cut back on blended crude cocktails they say can leave a foul aftertaste. . . .

Many executives say that the crude oil blends being created in Cushing are often substandard approximations of West Texas Intermediate (WTI), the longstanding U.S. benchmark familiar to, and favored by, many refiners in the region.

Typical light-sweet WTI crude has an API gravity of about 38 to 40. Condensate, or super-light crude that is abundant in most U.S. shale patches, ranges from 45 to 60 or higher. Western Canadian Select, itself a blend, is about 20.

While the blends of these crudes may technically meet the API gravity ceiling of 42 at Cushing, industry players say the mixes can be inconsistent in makeup and generate less income because the most desirable stuff is often missing.

The blends tend to produce a higher proportion of fuel at two ends of the spectrum: light ends like gasoline, demand for which has dimmed in recent years, and lower-value heavy products like fuel oil and asphalt. What’s missing are middle distillates like diesel, where growing demand and profitability lies.

|

|

Switchboard | ||||

| Latest | |||||

| Past week | |||||

| Past month | |||||

May 08, 2021 | peakoilbarrel.com

JEAN-FRANÇOIS FLEURY IGNORED RON PATTERSON IGNORED 05/01/2021 at 8:38 pm

Jean, I cannot get into the heads of the EIA analysis and figure out why they make the predictions they do. That is, do they really believe the shit they predict? Or do they do it as some kind of propaganda campaign to keep the shale Ponzi scheme afloat as long as possible because they think it is their civic duty to do so? I just don't know but I would imagine it is a little of both.

But we must look at the history of all the peak oil predictions. It all started around 2005 when almost everyone thought peak oil had arrived. But it did not happen. Then many thought it had arrived every couple of years since then. But the peak oil prognosticators became fewer and fewer. Now because all the predictions have been wrong in the past, it is just naturally assumed that peak oil will never happen.

So, even though almost every major producer has peak, including the three largest, the US, Russia, and Saudi Arabia, people cannot bring themselves to believe that peak oil has finally arrived, or did arrive a couple of years ago. So all we can do is shake our heads as they continue to predict that oil production will keep going up and almost forever.

But I find it rather fun to watch as finally someone else's predictions are going up in flames. 😉

There is something I don't understand. How EIA can project that the world oil production will be almost at the level of April 2020 in December 2022? If I am not wrong. KSA has apparently so much difficulties to maintain its production that they decreased their production of 1Mb/d in February to announce after a plan to decrease the domestic oil consumption of 1Mb/d to increase the amount of oil for export. And currently, they are at 8 Mb/d : in March 2020, their production was at 10 Mb/d. Russia is in oil production decline and the goal of increasing the production to the level of March 2020 (11 Mb/d) is and will be a goal for a long time as most the oil produced to compensate the loss of production (1Mb/d) will come from EOR (costly) and fracking (even more costly). For the US, I don't know how the DUC which are currently changed into completed wells and fracked will produce but as the growth of the number of operated rigs is slowing in Permian fields, I don't know how the decline of the current operated rigs will be compensated in the near future (in 6 or 12 months). I am not speaking of Baker, Eagle Ford and Niobara which are in decline. As the lower 48 states conventional oil production is in decline, as the Alaska oil production is in decline and as the GOM oil production is fairly stable, I don't know what will be the increase of US oil production in future. But I have a hunch that it won't be as glorious as the EIA can imagine (predict). Between now and December 2022, there are 6 Mb/d to compensate. If it is not coming the three main oil producers of the world, from where this will come? Iraq : no. They are sparing their oil ressources. Brazil? With pre-salt formations, they will be able to add only a maximum of 500 kb /d. Canada? They are at 5 Mb/d. I am not sure of their possibilities of production growth and even at their production growth rate, they will only add 290 kb/d or so in December 2022. Guyana will produce at most 750 kb/d in 2026. Assuming a constant rate of increase, this will give an additional 120 kb/d in December 2022. The rest of non-opec producer are, at best, only able to maintain their production. Among the rest of OPEC producers ,all are in production decline. There is only Iran which could increase its production but only 1,5 Mb/d at most. With all of this, we are a long way from increasing global oil production by 6 Mb/d until December 2022. HOLE IN HEAD IGNORED 05/02/2021 at 1:35 am

Ron , simple answer . "It is difficult to get a man to understand something, when his salary depends on his not understanding it." . –Upton Sinclair

Mar 07, 2021 | oilprice.com

Canadian Natural Resources, Suncor Energy, and Syncrude will all idle an upgrader each, taking off 250,000 bpd, 130,000 bpd, and 70,000 bpd, respectively, from total oil sands production.

... The oil sands cut will be temporary but, according to the industry itself, even when the three companies resume operations at their upgraders, there is little upward production growth pressure in Canadian oil sands. It seems emission reduction is a bigger priority for oil sands operators than production growth.

Apr 21, 2020 | www.moonofalabama.org

juliania , Apr 21 2020 15:43 utc | 61On the previous thread, Piotr Berman @ 417 did bring up the subject of this post by b, and had the following final comment: "...Actually, the most acute pain is among the clever folk who provided the so-called hedges, namely who sold the obligations to buy oil at a certain price. They are losing hundreds of billions -- my guess. Now they are forced to buy AND store, hence the negative price."

Thanks, Piotr. Some of what is happening makes a bit more sense to me as far as the strange dealings in the stock market are concerned.

Also, just above at 416, karlof1 had this to say: "...Was the West ever on the path to making its goal the improvement of the Common Man as advocated by Wallace and his political allies?..." His answer is NO (exclamation point.)

My answer is YES (exclamation point.) Even if you only progress as far as the creation of the UN, with the leadership of Eleanor, that is an important pivotal moment for mankind which we cannot ignore. But I will state uncategorically that the JFK administration had similar idealistic goals and would have carried them out, had it not been for divisive powers plotting against it. That such dastardly powers succeeded does not negate the previous effort.

And even the example of China proves that this is not an impossible dream for mankind in general. As also is the example of Russia. We are fortunate in this generation to have two role models instead of one.

I don't have the Frost poem at hand so I will thusly mangle the last lines (sorry)

Two paths lay in the woods, and I

Took the one less travelled by

And that has made all the difference.I've mangled it, but the meaning is there, I think. (I'll go find the correct version, and point of reference, I was a college student when Robert Frost came to Johns Hopkins and I heard him read his poems. He did so also at Kennedy's inaugural.)

gm , Apr 21 2020 10:36 utc | 8

What -$37/bbl oil means to you:arby , Apr 21 2020 12:10 utc | 17Oil futures paper contracts market (in normal times of stable->rising oil prices and plenty of tank storage capacity a simple safe "buy low, hold, sell high" investment vehicle used heavily by investment banks, hedge funds, ETFs and teachers', municipal employees', etc, retirement/pension funds) explained in 5 minutes by Chris Martenson starts at ~minute 35:00:

Emily, We may still be at or around peak oil. That does not mean that all of the heavily indebted countries and oil companies won't pump what's left as fast and hard as they can.William Gruff , Apr 21 2020 12:10 utc | 18Now you have to stir in a massive plunge in demand to the equation. Seems to me that all newer oil discoveries are deep sea or shale. All of which require much more energy to produce then say thirty years ago.

When it takes the equivalent of one barrel of energy to produce one barrel of energy it will be lights out.

dan of steele @2Emily , Apr 21 2020 12:56 utc | 24The petrodollar was not in and of itself the mechanism that the US used to "export debt" and enrich itself off global trade. Rather, the petrodollar was the mechanism used to lock-in the US$ as the global reserve currency. If you wanted oil, you needed US$. After that it was just convenient to use US$ for other internationally traded commodities as well. Of course, this made even more sense way back in the distant past of the middle of last century because most of the international trade in manufactured goods was for American products, for which you'd have to use dollars to buy anyway.

The empire fanbois will cook up all kinds of explanations for why the dollar will remain the Global Reserve Currency in order to reassure themselves of the empire's continued hegemony, but the fact is that all of the "locks" locking other countries into that regime are now gone. Countries can choose to walk away now whereas in the past that would mean giving up access to oil and no longer importing all of those awesome things that the US used to make. That is not a barrier anymore.

Arby 17.gm , Apr 21 2020 13:19 utc | 27

Thank you for taking the time to reply.

But something to ponder

Forbes

https://www.forbes.com/sites/michaellynch/2018/06/29/what-ever-happened-to-peak-oil/

Yergin

https://www.technologyreview.com/2011/09/22/191161/peak-oil-debunked/

Well good news for those of us who agree with Edgar Cayce.

'Russia is the hope of the world'.

Russia has 60 years worth left and thats with its known reserves.

Hasn't touched the Arctic yet.....

https://www.worldometers.info/oil/russia-oil/US/Western financial markets are a "musical chairs" game, where right now more chairs are being pulled out from the game faster than the FED and the central banks can 'digitally print' new chairs to keep the game going.Peter AU1 , Apr 21 2020 14:27 utc | 39Looks like energy dominance will get a bail out.juliania , Apr 21 2020 14:36 utc | 41

"We will never let the great US Oil & Gas Industry down. I have instructed the Secretary of Energy and Secretary of the Treasury to formulate a plan which will make funds available so that these very important companies and jobs will be secured long into the future!" Trump said via Twitter.

https://sputniknews.com/us/202004211079043543-trump-instructs-treasury-energy-depts-to-devise-plan-to-fund-us-oil-gas-industry/Is this a result of all the lockdowns? A sort of automotive general strike occasioned by the virus, aided and abetted by government enforcement of restrictions on industry, travel, general hulabaloo?Trisha , Apr 21 2020 15:27 utc | 56Peace has descended upon a weary world. Nature has commanded us to cease and desist from gigantic insults upon the earth. Stop digging! she says, Leave it in the ground! Cease and desist making war for oil!

What does it profit a man? It profits him nothing! I have no idea where this leads, but it is a delicious moment. Look, see the power we have to bring everything to a standstill, even when we only do it because we are forced to! What if we did it willingly?

Where are your trillions now, moghuls?

The earth has spoken. We should all listen. Me, I am going out to plant potatoes.

Peak shale has arrived. The energy inefficiency of fracking - directly related to the economic efficiency of producing shale - killed it off. This would have happened even without COVID-19.The same will (eventually) happen with oil. The global economy - already teetering - has now been pushed over the edge by COVID-19. The demand side of capitalist growth has been temporarily (and in some cases permanently) crushed - which is a good thing for the planet - as workers are idled for the foreseeable future, and many out of a job forever.

Bottom line is that we live on a finite world which capitalism treats as an infinite resource.

Dec 21, 2019 | peakoilbarrel.com

Survivalist x Ignored says: 12/19/2019 at 3:44 pm

Energy crisis looms as forecasts ignore US shale oil qualityFreddy Gulestø x Ignored says: 12/20/2019 at 4:30 amGood article, I believe it will not only be related to US shale oil quality but also a more or less collapse in US shale , to use the shale pioneer Mark Papas words from 2019 " the best in US shale is behind " but the investors choose to not believe him as it not fits with what the shale producers had presented them. Perhaps this time wall street will learn a lesson that might be quite exspensive. I am waiting for how much Exxon will write down of their assets in Permian, that might be higher than Chevron have annonsed.Dennis Coyne x Ignored says: 12/20/2019 at 10:24 amTight oil output will not increase as much as forecast by IEA and OPEC so it is not likely a refining wall at the World level will be be reached. As to demand outrunning supply, when that occurs oil prices will rise to a level that demand is destroyed to the point that supply will equal consumption as it must over the long term. Demand (consumption) cannot be higher than supply (output) for very long as stocks cannot be less than zero plus pipeline fill and minimum storage tank levels needed to keep the overall refinery and distribution system functioning. Oil prices will rise from 2020 to 2030, of that we can be sure, unless a severe World recession occurs (I expect this to begin in 2030+/-2 years and last for 2 to 4 years if World economists remember their Keynesian economics, otherwise it could be 5 to 7 years, if nonsense like fiscal austerity in the face of severe recessions is recommended and we are foolish enough to forget the lessons of 1929-1933.)Watcher x Ignored says: 12/20/2019 at 2:05 pmOil quality is not the way to address or label the issue. Quality is a word traditionally used in oil to describe sulphur content, not a scarcity of middle distillates in the yield. Needs a different word.Further, from the article, diesel is not the consumption growth heavy constituent. It's jet fuel. Up 3.7% last year. Gasoline was up almost 1%.

Dec 21, 2019 | peakoilbarrel.com

TonyEriksen x Ignored says: 12/18/2019 at 6:49 pm

EIA weekly supply estimates released, declining from the last two weeks of Nov at 12.9 mbd down to 12.8 mbd for the first two weeks of Dec.TonyEriksen x Ignored says: 12/20/2019 at 5:05 pm

https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=WCRFPUS2&f=WHFIR is showing a US peak for 2019 in November of 12.7 mbd.

https://twitter.com/HFI_Research/status/1207413992848674816IHS stated that "The new IHS Markit outlook for oil market fundamentals for 2019-2021 expects total U.S. production growth to be 440,000 barrels per day in 2020 before essentially flattening out in 2021. Modest growth is expected to resume in 2022."

https://news.ihsmarkit.com/prviewer/release_only/slug/energy-base-decline-rate-oil-and-gas-output-permian-basin-has-increased-dramatically-bEIA STEO says US oil production in 2019 is 12.25 mbd. That means that IHS is forecasting 12.69 mbd in 2020. This 0.44 mbd growth is assumed to come from the 7 US shale regions on EIA DPR. In 2019, shale region production was 8.60 mbd. 2020 shale region production is forecast to be 9.04 mbd, after 0.44 mbd growth. EIA DPR says that Jan 2020 shale region production is 9.14 mbd which is greater than 9.04 mbd which means that IHS 0.44 mbd 2020 growth implies that a US peak oil is happening about now.

IHS says that modest growth is expected in 2022, but they don't quantify how much growth. I believe this sentence was added because IHS does not want to be accused of implying US oil production has peaked. Dan Yergin, vice chair of IHS, founded CERA in 1982 which is now owned by IHS. Dan Yergin "clearly doesn't care about converting peak oilers. He really wants to influence Washington." In other words, IHS says modest growth in 2022, to please Washington politicians. US shale growth might increase in 2022, even with higher oil prices, but I'm guessing it won't.

http://transitionvoice.com/2011/09/whos-afraid-of-daniel-yergin/Given decreasing money available to shale oil, declining frac spread counts and falling rig counts, I now guess that US peak oil month is Nov 2019. Permian oil production should continue increasing slowly but it's not enough to offset falling production from other shale basins and other conventional oil basins.

North American shale is expected to hit an inflection point in 2020. Our expert, Raoul LeBlanc, VP of Unconventionals, shared his insights on what's ahead for North American #shale markets.

https://ihsmarkit.com/research-analysis/video-north-american-shale-hits-an-inflection-point-in-2020.html

Aug 22, 2019 | peakoilbarrel.com

Freddy x Ignored says: 08/19/2019 at 11:08 am

Thanks for valuable informstion Guy, in my mind from what I have read the shail oil have change some caracter espesialy in 2019. It have become more light that means lower quality. If quality goes down this will mean less profit if any at all to drill new wells after all exspensives, loan balones are payed. The good thing is it seems now low sulfur diesel demand increase because new IMO rules and prices, refinery margins in Asia increases. But it might be this will have minor Impact for WTI price as they demand more heavey oil , brent i.e for their marine diesel..

May 13, 2019 | peakoilbarrel.com

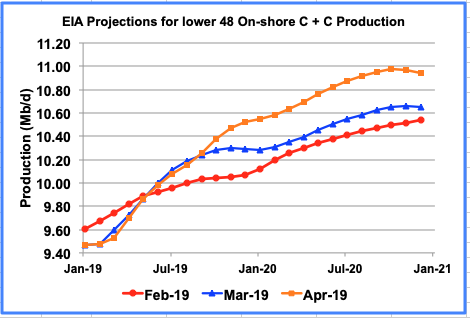

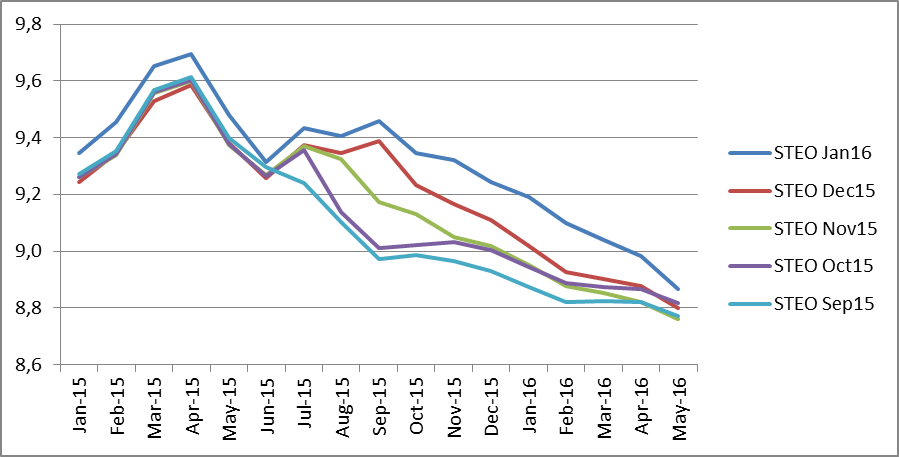

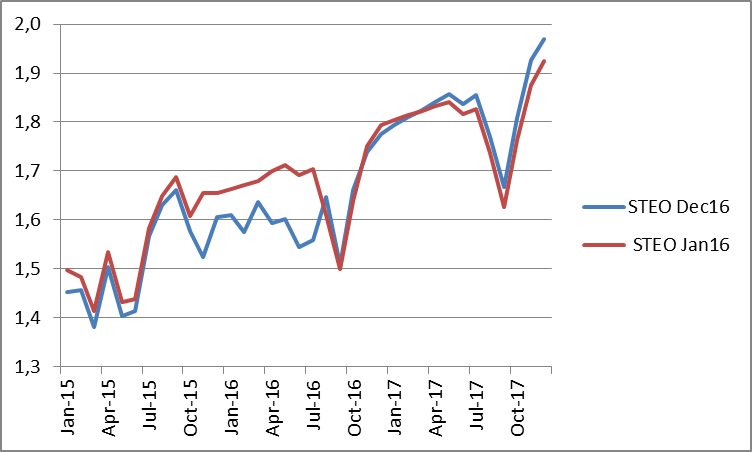

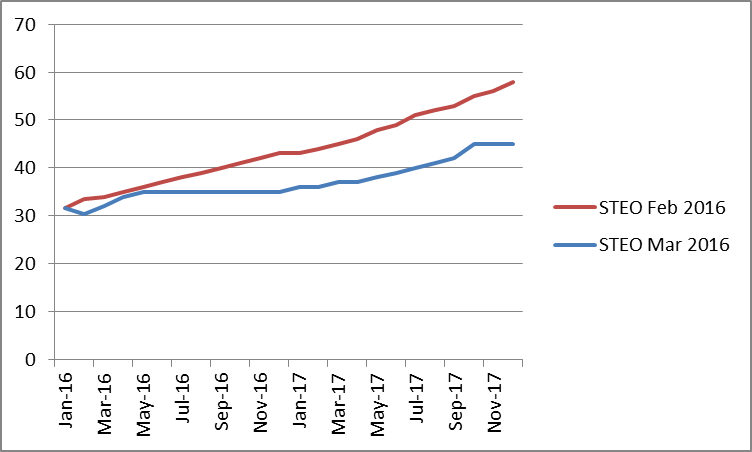

Ignored says: 05/07/2019 at 5:04 pm Attached are the changing monthly STEO projections for February, March and April for the lower 48 production. Today's projection, April, has added 230 kb/d day by year end 2019 to the March projection and close to 300 kb/d in 2020. The April projection also shows an increase of 960 kb/d from Dec 18 to Dec 19. For Dec 19 to Dec 20, the increase is only 420 kb/d, less than half of the 18 to 19 increase. Any speculation/ideas for the lower increase for 19 to 20. The G of M drops by 70 kb/d from Dec 19 to Dec 20.

Ron Patterson x Ignored says: 05/07/2019 at 5:37 pm

Thanks, Ovi.GuyM x Ignored says: 05/07/2019 at 6:27 pmYou notice that the April 19 STEO has the lowest production numbers for Jan. Feb. and April 2019 but the highest numbers as they move into the second half of 2019 and all of 2020.

I don't know what to make of this except that I find it rather amusing.

I found it insulting to my intelligence (not an exceptionally difficult task), but now that you mention it, I can imagine some Lewis Carroll feel to it.

Apr 27, 2019 | peakoilbarrel.com

Mike x Ignored says: 04/26/2019 at 2:30 pm

It should, don't you think? Ninety nine out of 100 people in America believe the USGS "discovered" 50 billion more barrels of oil last year in West Texas. Neither it nor the EIA go to near enough lengths to qualify these type of "surveys;" accordingly they are misleading and confusing to an uneducated public, including but not limited to, politicians in charge of implementing America's energy policies.The USGS mean average EUR in the Delaware Basin does not come close to paying out a $9MM well. How then can operators drill 244K more wells in the Delaware costing nearly $2.4 trillion dollars to recover 46.2 billion more barrels of oil? What earthly good does it do anybody to make an assessment of remaining resources over 8,000 square miles "if economics are not considered?" As stupid as the shale oil industry is, even its smart enough to know better than that.

My comment was directed at using so called unlimited, cheap shale oil resources as a foreign policy tool, not getting in a pissing match about the USGS.

Apr 11, 2019 | peakoilbarrel.com

GuyM: 04/11/2019 at 8:44 am

EIA's projections can be taken with a grain of salt. What is happening in the US shale is becoming more apparent. Exxon and Chevron plan to gear up to supply the new additions that they will supply to their new refinery additions that will accept LTO. However, I do not see them in a massive growth campaign that will increase exports.That leaves the independents who are very much under the gun to fix financials per investors, investments firms, and the press.

I read EOG's fourth quarter discussion with the public, which was cut short due to repetitive questions on whether EOG will increase dividends.

Prices will probably rise, but I don't expect much growth, this year, from the majority of the producers, which are the independents.

At least, for this year. As the years go by, more will be gobbled up by the majors, thus providing more limits in growth.

Apr 06, 2019 | peakoilbarrel.com

Energy News x Ignored says: 04/05/2019 at 11:19 am

Canada produced 4,524 kb/day of crude oil & equivalent products in January down -278 m/m

Exports of crude oil & equivalent products totaled a record 3,860 kb/day in January, up 9.1% from January 2018

Chart for production: https://pbs.twimg.com/media/D3ZukJvX4AASI8p.png

Chart for crude oil inventory https://pbs.twimg.com/media/D3ZuEauWsAIsGcD.png2019-04-05 Statistics Canada, press release https://www150.statcan.gc.ca/n1/daily-quotidien/190405/dq190405b-eng.htm

Mar 27, 2019 | peakoilbarrel.com

Carlos Diaz x Ignored says: 03/24/2019 at 6:38 am

EIA projections are profoundly flawed, being the only question if they are aware of it or if they actually believe their own shit.Increased production is driven by relatively high or increasing oil prices that signal increased demand, OR by the need of producers to maintain income at the expense of other producers when prices fall as it happened between mid-2014 to late 2015.

The second case is difficult to take place when oil prices are relatively low, as now, and when there are agreements between producers to limit production to sustain prices, as now. Therefore EIA is projecting an oil price increase amid general economic weakness, a trade war, Chinese ongoing slowdown, and so on. The economy is not signaling any urgency about oil supply after the Iran sanctions have taken place without much effect. Prices are not going to sustain an increase in oil production unless something unforeseen takes place, and such event cannot be included in EIA forecast.

According to Art Berman presentation about the 2018 price collapse the markets are signalling $60/b oil for 2019-2020 with $10 price excursions. If he is correct we will not see an increase in oil production, and might even see a slight decrease as Venezuela continues its fast descent to near zero oil production. Everybody knows that a country that came to depend almost exclusively on oil will implode when its oil production collapses, the only question being how the implosion will look and what will be the final death toll.

Mar 17, 2019 | www.rigzone.com

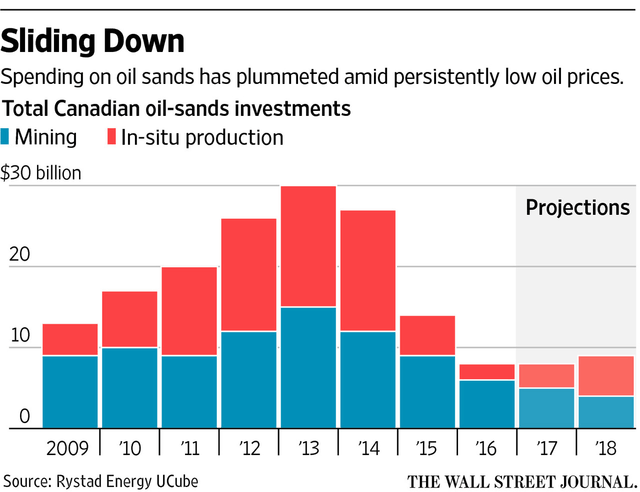

(Bloomberg) -- Exxon Mobil Corp. is delaying a C$2.6 billion ($1.9 billion) oil-sands project in Canada by at least a year as the nation's energy industry grapples with a shortage of pipeline space and government-mandated production cuts.

Exxon's Canadian subsidiary, Imperial Oil Ltd., had originally planned to bring the 75,000-barrel-a-day Aspen project online in 2022, but is now slowing the pace of development at the site in northern Alberta. Any decision to resume normal activity will depend on future government actions and general market conditions, Imperial said Friday.

The delay is another blow to Canada's oil-sands industry, which suffered from record low prices last year after a wave of new production overwhelmed the region's pipeline capacity. That spurred the government of Alberta, where most oil-sands projects are located, to mandate production cuts to drain a glut of crude in storage and revive prices.

The move also reflects Exxon's increased focus on projects off Guyana's coast and in the Permian Basin in Texas. The company last week increased its target for Permian production to 1 million barrels a day by 2024 and expanded its estimate for the size of its Guyana discovery to 5.5 billion barrels.

New RisksImperial, which owns refineries that were benefiting from the cheaper feedstock, has been one of the loudest critics of the curtailment policy and cited the plan again in its explanation for the Aspen delay.

"We cannot invest billions of dollars on behalf of our shareholders given the uncertainty in the current business environment," Imperial Chief Executive Officer Rich Kruger said in a statement. "That said, our goal is to ensure the work we do this year will enable us to effectively and efficiently resume planned activity levels when the time is right."

Imperial hinted at a possible slowdown at Aspen last month, saying it was re-evaluating the project after the forced production cuts introduced new risks. The company also has said previously that the curtailment policy, by boosting Canadian heavy oil prices too high, has made shipping crude by rail uneconomical, forcing Imperial to dial back its rail shipments to almost nothing last month.

Imperial sanctioned the Aspen project in November. The operation would use an extraction method called a steam-assisted gravity drainage, in which steam is pumped underground to heat up sludgy oil-sands bitumen, allowing it to flow through another pipe to the surface.

Imperial was slated to spend about C$700 million on the project this year, and the extra free cash flow stemming from the delay may be used to buy back more shares, which would be a positive for the stock, Dennis Fong, an analyst at Cannaccord Genuity, said in a note.

Imperial rose 0.5 percent to C$36.95 at 10:20 a.m. in Toronto. Exxon fell 0.3 percent to $80.21 in New York.

To contact the reporter on this story: Kevin Orland in Calgary at [email protected] To contact the editors responsible for this story: Simon Casey at [email protected] Joe Carroll

Feb 26, 2019 | peakoilbarrel.com

nikbez x Ignored says: 02/25/2019 at 6:10 pm

Looks like a glut of condensates has developed and is getting worse.Another thing to ponder about shale oil: falling capex, but solid production growth And that's after three bad years (2015, 2016 and 2017) and low current prices.

Do the US shale oil producers want to establish some kind of "world record" and then "The last one out please turn off the lights."

How can such a miracle happen?

The US oil production is really Alice in Wonderland phenomenon.

May 15, 2013 | rbnenergy.com

By Al Troner, President Asia Pacific Energy Consulting (APEC)U.S. production of field (lease) condensates is growing like crazy, especially in the Eagle Ford. There is way too much of this material for it to be absorbed into traditional crude blending markets. At the same time the production of plant condensate, a.k.a. natural gasoline, is also increasing along with the yield of all other products from natural gas processing plants. A glut of condensates has developed and is getting worse. Clearly this is an opportunity for new market development, and the bizdev community is hard at work coming up with concepts, projects and proposals to use all of this material in the U.S. and in export markets. But there is a problem. Condensate markets in different geographies seem to have little in common with each other. It's like walking through the looking glass. One term can have several meanings. One meaning can be ascribed to several terms. Today we launch a RBN blog series to make sense of it all.

First, let's consider a fundamental question. Are condensates in the natural gas liquids (NGL) family? Like everything about this topic, it depends. In U.S. usage, a "plant condensate" is the equivalent of products classified as "pentanes+" and natural gasoline, and these are considered NGLs. On the other hand, U.S. usage typically does not consider "field or lease condensate" as an NGL, instead classifying these commodities as crude oil. There are a variety of reasons for this distinction in the U.S. market, some rational some not so rational that we will explore a little later in this blog.

However, no such distinction exists in international markets, which consider both plant and field condensates the same thing, with both classified as natural gas liquids – since they are both liquids that come from natural gas. Of course, to further confuse things, international markets have their own labeling problems, calling some of these products "naphthas", when any refiner will tell you that term ought to be reserved for products that have been through a crude distillation tower. Are you starting to get a sense for the problem? Because all of these terms are so mixed, mingled and intertwined, the only thing we can do is "Begin at the beginning" as Alice was told in Wonderland -- and that is with the general category of products called natural gas liquids – NGLs.

NGLs, LPGs and Purity Products

NGLs seem to exist in the twilight zone between black oil, or crude, the basis of all petroleum products, and natural gas (methane) the low carbon footprint, suddenly abundant (in the U.S.) fuel source. NGLs are neither here nor there – they possess, to differing extents, characteristics of both oil and gas and have values and market drivers both similar to and distinctly separate from oil and gas.

Yet it would appear that the key factor that unites all NGLs is that they are derived from gas and that most NGLs need special containment to remain liquids. Then, "What is in a name?"

"When I use a word," Humpty Dumpty said in rather a scornful tone, "it means just what I choose it to mean -- neither more nor less." "The question is," said Alice, "whether you can make words mean so many different things." (Lewis Carroll, Through the Looking Glass, Chapter 6 )

In fact, NGLs carry ambiguity in their very name. Ethane, propane, normal butane, isobutane and (as the product is commonly called in the U.S.), natural gasoline are all found in natural gas, but are liquid hydrocarbon molecules suspended within gas. This is equally true for lease condensates, hence the classification of lease condensates as NGLs in international markets. In this survey of the products alternatively called by names such as NGLs, condensates, pentanes plus and various other monikers, we will explore the wide range of terms used to label these products and how, at times, these different labels define each NGL somewhat differently.

The products we call crude oil and natural gas are base materials – oil is the precursor of petroleum products; gas is primarily valued on its ability to create heat, i.e. calorific value. NGLs are many things simultaneously and can be defined as end-products; petrochemical feedstocks or semi-finished intermediates used to create finished oil products. This very variability - this wide range of flexibility of NGL utilization - leads to much uncertainty. To avoid confusion, it is important to define the terms used and to understand how US market terminology and definitions differ from those abroad.

- NGLs are liquid hydrocarbons suspended as particles in gas, under conditions of subterranean pressure and temperature. As noted above, in the U.S. the term NGL is usually reserved for these products produced through some form of processing (natural gas processing plants or refineries), while in international markets it also includes field or lease condensates.

- Y-Grade, also called mixed NGLs or 'raw make' is an unfractionated blend of the various purity products (see definition below) that make up the NGL product family. A Y-grade stream is typically produced by a natural gas processing plant and transported by pipeline to a central fractionation facility to be split into purity products.

- NGL Purity Products – As this term is used in the U.S., the five purity NGL products are ethane (C2), propane (C3), normal butane (NC4), isobutane (IC4) and natural gasoline (C5+). The numbers indicate how many carbon atoms are contained in each NGL molecule. While butane and isobutane both have four carbon atoms, they differ somewhat in molecular structure. As a general rule, when at least 90% of the NGL stream has only one type of carbon molecule, this NGL, whether ethane or butane, is defined as a purity product.

- Liquefied Petroleum Gas, or LPG, is a subset of the NGL family. In the U.S. the term includes propane, normal butane and isobutane and is often associated with refinery production and demand for these products. The term is also used to refer to the international trade for propane and butanes.

- Pentane+ or C5+ designations include the products that we also call condensates. We'll talk about that plus sign and the many varieties of condensates in the section below.

- Heavier NGLs: In the US market, the term Heavy NGLs refers to natural gasoline and butane/isobutane, but this definition is not universal and certainly can be misleading. The only "heavy" NGL that can be separated, stored and transported without special containment is condensate (natural gasoline), a point which we will detail further below. The term Heavy NGLs is rarely used in foreign NGL markets, and when it is occasionally used, it refers solely to condensate.

- Ethane/Propane Mix: In the US market, ethane and propane are sometimes sold as a mixed stream for use as a petrochemical feedstock. The most common is called E/P Mix, consisting of 80% ethane/20% propane. In some cases the buyers want a custom blend that differs in the proportion of these two NGLs. E/P Mix is sold in European NGL markets and is the basis of Mideast Gulf ethylene cracker feedstock supply, but is virtually unknown in Asia.

Note that most NGLs originate from gas production, whether associated with crude or solely on its own non-associated gas production. When NGLs are contained within a gas stream, it is said that they are in "vapor phase".

All natural gas contains some NGLs. Sometimes there are enough NGLs to be recovered economically, sometimes not. Sometimes NGLs must be removed (whether economic or not) for the 'residue' natural gas to meet BTU and other specifications for the take-away natural gas pipeline or LNG liquefaction facility. Regardless, for natural gas produced at the wellhead to be sold and transported in pipeline systems, various impurities like sulfur and water must be removed. When required by downstream specifications, or economically advantageous or both, the NGLs are separated from the gas in a natural gas processing plant. The mixed stream or Y-grade NGLs are then transported to a fractionator for separation into purity products. That fractionator may be at the processing plant location, but in the U.S. is usually some distance away. As discussed on many occasions in RBN blogs, by far the largest NGL fractionation center in the U.S. is at Mont Belvieu, Texas.

The table below from the Baker Institute shows NGL products, their characteristics and their markets.

Source: Baker Institute (Click to Enlarge)

Condensates, Pentanes Plus and Natural Gasoline

Now that we've cleared up NGLs, we need to turn to the far more convoluted world of condensates, and natural gasoline. But that's not the only labels we need to include. There is also naphtha, Pentanes Plus and even A-180. Each of these terms may have a slightly different meaning in different markets.

An Example of the Name Game: Pentanes Plus . For example, Pentanes Plus, as defined in the United Arab Emirates (Abu Dhabi National Oil Company, or ADNOC) produces a condensate stripped directly from the gas stream. It is a light, highly paraffinic naphtha equivalent and therefore best suited for ethylene cracking. It excludes ethane and LPG and is sold as a naphtha grade. So, this material is called pentane, which is a condensate that is sold as paraffinic naphtha. Got it?

And there still is another Pentanes Plus, this one defined by the Energy Information Agency (EIA), a unit of the US Department of Energy (DOE). EIA describes Pentanes as "a mixture of hydrocarbons, mostly pentanes and heavier, extracted from natural gas. (It) includes iso-pentane, natural gasoline, and plant condensate." Note that it excludes lease condensate, which EIA inconveniently lumps into their crude oil production statistics. Obviously ADNOC's "Pentanes Plus" is not the same stuff as EIA's Pentanes Plus.

To access the remainder of Through the Looking Glass: NGLs, Condensates and Pentanes Part 1 – U.S. versus the World you must be logged as a RBN Backstage Pass™ subscriber.

Full access to the RBN Energy blog archive which includes any posting more than 5 days old is available only to RBN Backstage Pass™ subscribers. In addition to blog archive access, RBN Backstage Pass™ resources include Drill-Down Reports, Spotlight Reports, Spotcheck Indicators, Market Fundamentals Webcasts, Get-Togethers and more. If you have already purchased a subscription, be sure you are logged in For additional help or information, contact us at [email protected] or 888-613-8874.

Related Content

- Like A Box of Chocolates – The Condensate Dilemma

- Fifty Shades of Condensates – Which One Did You Mean?

- Whole Lotta Splittin' Going On – The Market for US Gulf Naphtha from Condensate Splitters

- Whole Lotta Splittin' Going On – Gulf Coast Condensate Splitter Economics

- Whole Lotta Splittin' Going On- Processing Gulf Coast Condensate

- 1-2-3- MPLX's Plan for Moving Northeast Condensate and Natural Gasoline

- Neither Fish nor Fowl – Condensates Muscle in on NGL and Crude Markets

- Fifty Shades Lighter – The Lease Condensate Export Problem

- Blinded by the Lights- Finding Markets for U.S. Field and Plant Condensate

- With or Without Splitting? Changing Lease Condensate Export Definitions

Feb 22, 2019 | peakoilbarrel.com

dclonghorn x Ignored says: 02/21/2019 at 10:16 pm

Doc,likbez x Ignored says: 02/22/2019 at 12:57 amYou need to look at more of the report.

http://ir.eia.gov/wpsr/overview.pdf

Crude imports on line 5 as 7,522 kbpd, crude exports on line 9 are 3,607 kbpd for net crude imports on line 4 of 3,915 kbpd.

Other supply includes products and natural gas liquids. It shows net imports on line 21 of -2,809 kbpd. Total net imports of Crude and Petroleum Products on line 33 are 1,106 kbpd.This is somewhat questionable math as one barrel of oil and one barrel of condensate have different energy content (condensate is around 60% of oil).So condensate input into the USA energy balance should be multiplied by approximately 0.5 to get a more clear picture.

The USA imports heavy oil and exports condensate. Not the same liter for liter things.

www.bp.com

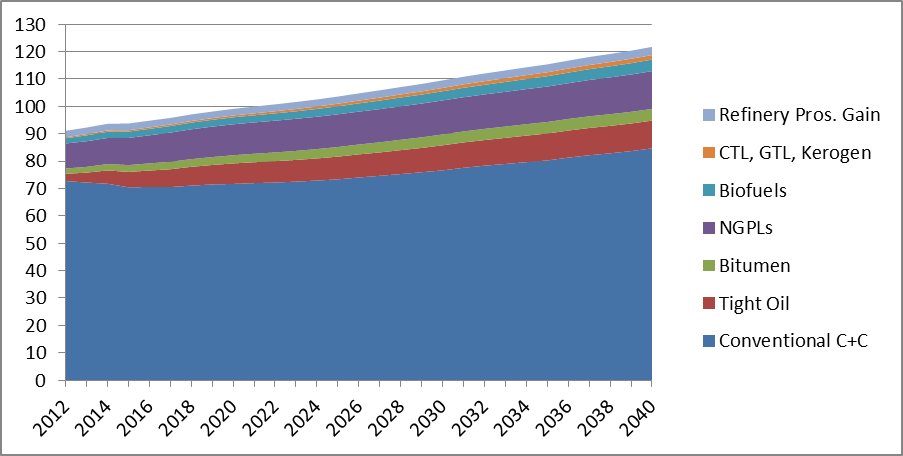

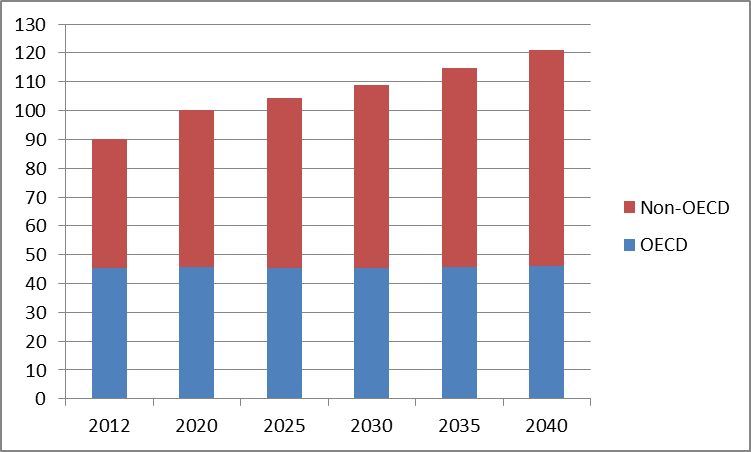

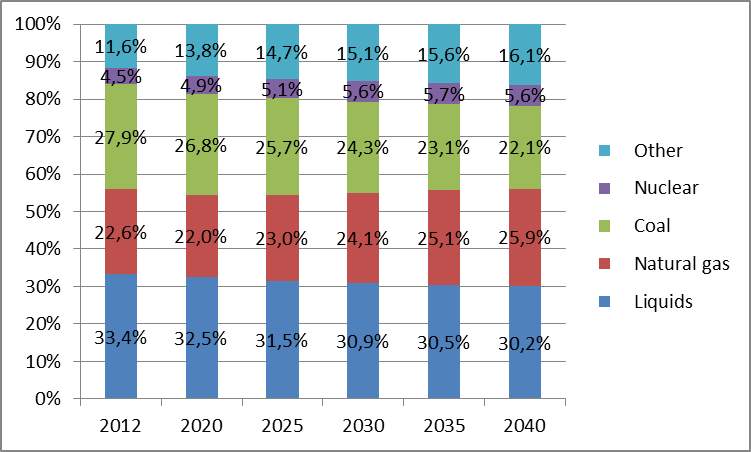

In the ET scenario, global demand for liquid fuels – crude and condensates, natural gas liquids (NGLs), and other liquids – increases by 10 Mb/d, plateauing around 108 Mb/d in the 2030s.

All of the demand growth comes from developing economies, driven by the burgeoning middle class in developing Asian economies. Consumption of liquid fuels within the OECD resumes its declining trend. The growth in demand is initially met from non-OPEC producers, led by US tight oil. But as US tight oil production declines in the final decade of the Outlook, OPEC becomes the main source of incremental supply. OPEC output increases by 4 Mb/d over the Outlook, with all of this growth concentrated in the 2030s. Non-OPEC supply grows by 6 Mb/d, led by the US (5 Mb/d), Brazil (2 Mb/d) and Russia (1 Mb/d) offset by declines in higher-cost, mature basins.

Consumption of liquid fuels grows over the next decade, before broadly plateauing in the 2030s

Demand for liquid fuels looks set to expand for a period before gradually plateauing as efficiency improvements in the transport sector accelerate. In the ET scenario, consumption of liquid fuels increases by 10 Mb/d (from 98 Mb/d to 108 Mb/d), with the majority of that growth happening over the next 10 years or so. The demand for liquid fuels continues to be dominated by the transport sector, with its share of liquids consumption remaining around 55%. Transport demand for liquid fuels increases from 56 Mb/d to 61 Mb/d by 2040, with this expansion split between road (2 Mb/d) (divided broadly equally between cars, trucks, and 2/3 wheelers) and aviation/marine (3 Mb/d). But the impetus from transport demand fades over the Outlook as the pace of vehicle efficiency improvements quicken and alternative sources of energy penetrate the transport system . In contrast, efficiency gains when using oil for non-combusted uses, especially as a feedstock in petrochemicals, are more limited. As a result, the non-combusted use of oil takes over as the largest source of demand growth over the Outlook, increasing by 7 Mb/d to 22 Mb/d by 2040.

The outlook for oil demand is uncertain but looks set to play a major role in global energy out to 2040

Although the precise outlook is uncertain, the world looks set to consume significant amounts of oil (crude plus NGLs) for several decades, requiring substantial investment. This year's Energy Outlook considers a range of scenarios for oil demand, with the timing of the peak in demand varying from the next few years to beyond 2040. Despite these differences, the scenarios share two common features. First, all the scenarios suggest that oil will continue to play a significant role in the global energy system in 2040, with the level of oil demand in 2040 ranging from around 80 Mb/d to 130 Mb/d.

In all scenarios, trillions of dollars of investment in oil is neededSecond, significant levels of investment are required for there to be sufficient supplies of oil to meet demand in 2040. If future investment was limited to developing existing fields and there was no investment in new production areas, global production would decline at an average rate of around 4.5% p.a. (based on IEA's estimates), implying global oil supply would be only around 35 Mb/d in 2040. Closing the gap between this supply profile and any of the demand scenarios in the Outlook would require many trillions of dollars of investment over the next 20 years.Growth in liquids supply is initially dominated by US tight oil, with OPEC production increasing only as US tight oil declines

Growth in global liquids production is dominated in the first part of the Outlook by US tight oil, with OPEC production gaining in importance further out. In the ET scenario, total US liquids production accounts for the vast majority of the increase in global supplies out to 2030, driven by US tight oil and NGLs. US tight oil increases by almost 6 Mb/d in the next 10 years, peaking at close to 10.5 Mb/d in the late 2020s, before falling back to around 8.5 Mb/d by 2040. The strong growth in US tight oil reinforces the US's position as the world's largest producer of liquid fuels. As US tight oil declines, this space is filled by OPEC production, which more than accounts for the increase in liquid supplies in the final decade of the Outlook.

The increase in OPEC production is aided by OPEC members responding to the increasing abundance of global oil resources by reforming their economies and reducing their dependency on oil, allowing them gradually to adopt a more competitive strategy of increasing their market share. The speed and extent of this reform is a key uncertainty affecting the outlook for global oil markets (see pp 88-89).

The stalling in OPEC production during the first part of the Outlook causes OPEC's share of global liquids production to fall to its lowest level since the late 1980s before recovering towards the end of the Outlook.

Low-cost producers: Saudi Arabia, UAE, Kuwait, Iraq and Russia

Oil demand †

Download chart and data Download this chart pdf / 64.6 KB Download this data xlsx / 10.1 KB† Excluding GTLs and CTLs

The abundance of oil resources, and risk that large quantities of recoverable oil will never be extracted, may prompt low-cost producers to use their comparative advantage to expand their market share in order to help ensure their resources are produced.

The extent to which low-cost producers can sustainably adopt such a 'higher production, lower price' strategy depends on their progress in reforming their economies, reducing their dependence on oil revenues.

In the ET scenario, low-cost producers are assumed to make some progress in the second half of the Outlook, but the structure of their economies still acts as a material constraint on their ability to exploit fully their low-cost barrels.

The alternative 'Greater reform' scenario assumes a faster pace of economic reform, allowing low-cost producers to increase their market share. The extent to which low-cost producers can increase their market share depends on: the time needed to increase production capacity; and on the ability of higher-cost producers to compete, by either reducing production costs or varying fiscal terms.

The lower price environment associated with this more competitive market structure boosts demand, with the consumption of oil growing throughout the Outlook.

Growth in liquid fuels supplies is driven by NGLs and biofuels, with only limited growth in crude oil production

The increase in liquid fuels supplies is set to be dominated by increases in NGLs and biofuels, with only limited growth in crude.

Feb 12, 2019 | Oil Sands Magazine

Global shortage of medium to heavy sour crude: Cuts from OPEC, Canada and potentially Venezuela have increased the price of medium and heavy crude oils. The Mars benchmark, a medium, sour crude produced in the Gulf of Mexico, has moved to above par with Light Louisiana Sweet.

Western Canadian Select (WCS) prices in the Gulf Coast also rose above par with the West Texas Intermediate (WTI) benchmark at the end of January. WCS trades at a US$10/bbl discount to WTI in Alberta, but now sells at a US$1.50 premium in Houston.

A similar effect is being seen globally, as several medium to heavy sour crude grades produced in the Middle East are now trading at a premium to Brent.

Feb 15, 2019 | peakoilbarrel.com

Watcher: 02/15/2019 at 4:24 am

I have been suspicious for some time that production numbers can be corrupted by fuzzy definitions. Iran is being sanctioned, but Iran shares that enormous gas field under the Persian Gulf with Qatar. Gas production yields condensate and it yields NGLs.likbez: 02/15/2019 at 7:27 pmHigh vapor pressure NGLs get labeled liquefied petroleum gas, and that is used for transportation fuel in India. Pentane Plus is used or called something akin to natural gasoline.

You can see how the definitions are going to blur and they're going to allow declaring oil production numbers to be anything that they want them to be. Iran is using this to dodge sanctions, or they did use it when condensate was not restricted. Don't recall if that loophole was closed in the current sanctions. That would be a good thing to know.

The same thing can happen with shale. We hear all sorts of talk about how much gas is being flared and how much gas is being captured, and you know perfectly well there has to be condensate involved. There was an article a year or so ago about NGL capture in the Bakken, but I don't recall any follow-up. It shouldn't take too much of a stretch on the part of state regulators to find a way to count the high vapor pressure portion of NGL as oil.

You can see how the definitions are going to blur and they're going to allow declaring oil production numbers to be anything that they want them to be.

Exactly. And this, in turn, allows Wall Street to suppress the price of "prime oil" using fake production numbers, fake storage glut (which is essentially condensate glut) and similar tricks. Please note that the US refineries consume mainly "prime oil" while the USA mainly produces (and tries to export at a discount) "subprime oil."

Pretty polished and sophisticated racket. It might well be that shale oil companies are partially financed from those Wall Street profits as nobody in serious mind expect those loans to be ever repaid.

So OPEC cuts are the only weapon that OPEC countries have against this racket.

In any case, I think all those nice charts now need to be split into "prime oil" and subprime oil parts and analyzed separately. In the current conditions, treating "heavy oil" and condensate as a single commodity looks to me like pseudoscience.

Feb 14, 2019 | oilprice.com

...OPEC+ production cuts could erase the supply surplus in the near future. Saudi Arabia has promised to cut more than required, lowering output in January by 350,000 bpd while also promising another 500,000 bpd cut by March.

"[C]ore-OPEC producers are adopting a 'shock and awe' strategy and exceeding their cut commitment," Goldman Sachs said in a note, predicting that Brent oil prices will average $67.50 per barrel in the second quarter.

Feb 14, 2019 | oilprice.com

To accommodate steadily rising barrels of light oil, OPEC and its non-OPEC partners have backed out their own supplies in order to prevent a crash in prices. But many OPEC members produce medium and heavier blends.

The quantity of global supply may not be vastly different, but the quality of the crude slate has changed dramatically. Refiners cannot easily swap out one type for another. The upshot is that the world is seeing a glut of light oil at a time when supply of medium and heavier barrels are relatively tight.

... ... ...

U.S. sanctions against Venezuela and Iran are magnifying this trend, knocking even more medium and heavier barrels off of the market.

... ... ...

The IEA said that these quality differences could cause some problems this year. "In quantity terms, in 2019 the US alone will grow its crude oil production by more than Venezuela's current output," the agency wrote in its Oil Market Report published Wednesday. "In quality terms, it is more complicated. Quality matters."

Feb 13, 2019 | news.yahoo.com

The "call" on OPEC crude is now forecast at 30.7 million bpd in 2019, down from the IEA's last estimate of 31.6 million bpd in January.

U.S. sanctions on Iran and Venezuela have choked off supply of the heavier, more sour crude that tends to yield larger volumes of higher-value distillates, as opposed to gasoline. The move has created disruption for some refiners, but has not led to a dramatic increase in the oil price in 2019.

"In terms of crude oil quantity, markets may be able to adjust after initial logistical dislocations (from Venezuela sanctions)", the Paris-based IEA said.

"Stocks in most markets are currently ample and ... there is more spare production capacity available."

Venezuela's production has almost halved in two years to 1.17 million bpd, as an economic crisis decimated its energy industry and U.S. sanctions have now crippled its exports.

Brent crude futures have risen 20 percent in 2019 to around $63 a barrel, but most of that increase took place in early January. The price has largely plateaued since then, in spite of the subsequent imposition of U.S. sanctions.

"Oil prices have not increased alarmingly because the market is still working off the surpluses built up in the second half of 2018," the IEA said.

"In quantity terms, in 2019, the U.S. alone will grow its crude oil production by more than Venezuela's current output. In quality terms, it is more complicated. Quality matters."

dlider909, 7 hours ago Story will change in 30 days.Robert, 7 hours ago ... ... ...

What this report fails to do is to pay the appropriate homage to American oilfield roughnecks...

ralf

7 hours ago Nonsense. I see military action against Venezuela soon, just because of our thirst for oil.

Talk about shale is like talk about Moon conquests, not supported by hard facts.

Feb 02, 2019 | www.bloomberg.com

Texas and other shale-rich states are spewing a gusher of high-quality crude -- light-sweet in the industry parlance -- feeding a growing glut that's bending the global oil industry out of shape.

Refiners who invested billions to turn a profit from processing cheap low-quality crude are paying unheard of premiums to find the heavy-sour grades they need. The mismatch is better news for OPEC producers like Iraq and Saudi Arabia, who don't produce much light-sweet, but pump plenty of the dirtier stuff.

The crisis is Venezuela, together with OPEC output cuts, will exacerbate the mismatch. The South American producer exports some of the world's heaviest oil and Trump administration sanctions announced this week will make processing and exporting crude far more difficult. American refiners are scrambling for alternative supplies at very short notice.

"We still have some holes in our supply plan" over the next 30 days, Gary Simmons, a senior executive at Valero Energy Corp., the largest refiner in the U.S., told investors on Thursday. "We are not taking anything from Venezuela."

Crude isn't the same everywhere: the kind pumped from the shale wells of West Texas resembles cooking oil -- thin and easy to refine. In Venezuela's Orinoco region, it looks more like marmalade, thick and hard to process. Density isn't the only difference -- the sulfur content is also important, dividing the market into sweet and sour crude. Heavy crude tends to have more sulfur than light crude.

As Saudi Arabia, Russia and Canada cut production, and American sanctions force Venezuelan and Iranian exports lower, the market for low-quality crude is feeling the impact.

"The strength in the physical crude market continues, led by sour crude shortages," Amrita Sen, chief oil analyst at consultant Energy Aspects Ltd. in London, said echoing a widely held view within the market

Jan 13, 2019 | finance.yahoo.com

In an attempt to combat a ballooning oil glut and dramatically plummeting prices, the premier of Alberta Rachel Notley introduced an unprecedented measure at the beginning of December when she is mandating that oil companies in her province cut production. This directive was particularly surprising in the context of Canada's free market economy, where oil production is rarely so directly regulated.

Canada's recent oil glut woes are not due to a lack of demand, but rather a severe lack of pipeline infrastructure. There is plenty of demand, and more than enough supply, but no way to get the oil flowing where it needs to go. Canada's pipelines are running at maximum capacity, storage facilities are filled to bursting, and the pipeline bottleneck has only continued to worsen . Now, in an effort to alleviate the struggling industry, Alberta's oil production has been cut 8.7 percent according to the mandate set by the province's government under Rachel Notley with the objective of cutting out around 325,000 barrels per day from the Canadian market.

Even before the government stepped in, some private oil companies had already self-imposed production caps in order to combat the ever-expanding glut and bottomed-out oil prices. Cenovus Energy, Canadian Natural Resource, Devon Energy, Athabasca Oil, and others announced curtailments that totaled around 140,000 barrels a day and Cenovus Energy, one of Canada's major producers, even went so far as to plead with the government to impose production caps late last year.

So far, the government-imposed productive caps have been extremely successful. In October Canadian oil prices were so depressed that the Canadian benchmark oil Western Canadian Select (WCS) was trading at a whopping $50 per barrel less than United States benchmark oil West Texas Intermediate (WTI). now, in the wake of production cuts, the price gap between WCS and WTI has diminished by a dramatic margin to a difference of just under $13 per barrel.

Related: The Natural Gas Crash Isn't Over

While on the surface this would seem to be a roundly glowing review of the production caps in Alberta, production cuts are not a long-term solution for Canada's oil glut woes. The current production caps in Canada are only intended to last through the middle of this year, at which point Canadian oil companies will be permitted to decrease their cutbacks to just 95,000 barrels per day fewer than the numbers from November 2018's production rates. The cuts are a just a treatment, not a cure, for oversupply in Alberta. The problem needs to be addressed at its source--the pipelines.

Unfortunately, the pipeline shortage in Alberta has no quick and easy fix. While there are multiple major pipeline projects underway, the two largest, the Keystone XL pipeline and the Trans Mountain pipeline, are stalled indefinitely thanks to legal woes and seemingly endless litigation. The Enbridge Line 3 pipeline, intended to replace one of the region's already existing pipelines, is currently under construction and projected to be up and running by the end of the year, but will not go a long way toward fixing the bottleneck.

Even if the Albertan government re-evaluates the present mid-2019 expiration date for the current stricter production cuts, extending the production caps could have enduring negative consequences in the region's oil industry. Keeping a long-term cap on production in Alberta would potentially discourage investment in future production as well as in the infrastructure the local industry so sorely needs. According to some reporting , the cuts will not be able to control the gap between Canadian and U.S. oil for much longer anyway, just another downside to drawing out what should be a short-term solution. The government will need to weigh the possible outcomes very carefully as the expiration date approaches, when the and the pipeline shortage is still a long way from being solved and the price of oil remains dangerously variable.

By Haley Zaremba for Oilprice.com

Dec 27, 2018 | peakoilbarrel.com

shallow sand x Ignored says: 12/24/2018 at 2:33 pm

WTI $42.58GuyM x Ignored says: 12/24/2018 at 3:08 pmWTI Midland $34.34

Flint Hills posting ND Light Sweet $16.75.

Seems the break even is pretty low, as EIA has predicted about a million bpd increase out of shale in 2019Adam B x Ignored says: 12/24/2018 at 5:53 pmIt doesn't matter whether you provide storage or increase the number of refineries, shale production is relatively dead at these prices. The prices just need to stay ridiculously low for awhile to stop the EIA and IEA from producing more imaginary oil, and face reality. Yeah, that would affect my wells, but I would hope for a better price, later.

Less than $17 a barrel? Bakken is done for awhile. And there is NOBODY in the Permian breaking even at $34. Remember what happened in 2015? Yeah, production dropped by over a million barrels. These prices are as bad as 2015, and we have a bigger drop potential. Those pipeline builders gotta be really worried. But, they should be anyway. How are you going to keep the pipeline flowing if you can't take what's in there out, because there is nowhere to put it? How many mentally challenged people are working in the Permian?

The amazing part is, this time there is no glut, at all. Inventories will drop, but just let it happen. We have to forever eradicate the Permian and shale production will save the world song. It's a thousand times more irritating than listening to Bing Crosby's white Christmas on January1st. There ain't no fritzing Santa Clause, EIA!

Seems like a lot of year end liquidation of oil futures perhaps. That's the only explanation I've got for how oil is this low. Probably will bounce back to the low 50's WTI by late January. It will be interesting to see December through February US production data to see what effect this price dive has done.Financier x Ignored says: 12/25/2018 at 4:24 pmHi GuyM,GuyM x Ignored says: 12/25/2018 at 4:43 pm"Those pipeline builders gotta be really worried. But, they should be anyway."

What do you think the issues are that the pipeline companies are worried about

right now? I would appreciate your thoughts on this.Two thoughts, immediately. The price is such now, that if it stays anywhere close to that for awhile, completions won't be as expected, and there won't be enough oil to fill them. The second is, that if the E&Ps had the right price, and did produce, there is probably not enough shipping until late 2020 or 2021 to handle 2.5 million bpd extra. No place to store it, and refineries can't use high API. Unless, I am missing something. Pipelines can't make much money because a pipeline is filled, it has to be flowing.Dennis Coyne x Ignored says: 12/24/2018 at 5:47 pmIts gonna go to zero. Just kidding.GuyM x Ignored says: 12/24/2018 at 6:03 pm

Doubt these prices will be sustained.Maybe not zero, but could be a lot more. It's reacting to the stock market, now. Dow down 15% and still going. This is no simple correction, as that stops at around 10%, usually. Been a long, long time since the last bear market, and is past due. Everything dives, until they come to grips that commodities are a different animal. That may take months, or longer depending on how bad it gets. Who knows, each bear market has a different generation, and it's always new to them.Adam B x Ignored says: 12/24/2018 at 9:04 pm

Especially this one, as it has been so long. New ball game.

I think it was EN who posted how rate hikes can cause this on a historical basis. Based on that chart, we could be in a significant bear market. Bubbles are going to pop. Not sure what the derivative markets are looking like, but they can't be healthy. The derivative markets are many times bigger than the regular stock markets. Think Lehman Brothers, and margin call. Lehman didn't fail over bad home loans, they failed over the derivatives of home loans. This time, it won't be housing, but something will give. They made a big effort to control the banks after the last fiasco in 2008, but made NO effort in regulating derivatives. Brilliant. Some of the weaker oil companies may be in trouble. JMO.Right on the move from 18,000 to 27,000 in the Dow was just hot air as we are seeing now. Investors realize there isn't a fed put and are freaking out, how far will it sink before Powell and company call off the dogs and say no more rate hikes and stop quantitative tightening..cause it's on "autopilot" according to them. All I want is 4% on an 18 month CD, fat chance now.GuyM x Ignored says: 12/24/2018 at 10:07 pmThe autopilot is also the monthly selling of Bonds held by the Fed, which also acts as interest rate increases.Watcher x Ignored says: 12/24/2018 at 7:19 pmhahahahahahaahahahaGuyM x Ignored says: 12/24/2018 at 7:27 pmThe inventory nazis will be out soon with a surprise discovery that there was more in storage than they ever suspected.

Don't you worry none. In the finest traditions of capitalism and free markets, various govts will be taking action soon. To do something.

Yeah, they are convening as we speak. Never fear. Trust in your government, not your 401k.🤪TechGuy x Ignored says: 12/24/2018 at 10:20 pmA Minsky moment, day, week, month or year(s). Aka margin call on highly leveraged margin is probably the cause. Hence, duck it's hitting the fan.

https://seekingalpha.com/amp/article/4229895-something-happeningIn other words, if you have to sell those paper barrels for margin calls, and there is too few to buy, because they are selling, also; then price goes down, because there are too many paper barrels, and not enough buyers. Probably, the original paper sellers lose their butt, and have to sell something to cover their margins. Everyone now is paying homage to the margin god. Because, there was never any real money to cause the stock market to soar like an eagle.

Which reverses itself later, because when it is time to sell new paper barrels, less are sold, enabling the price to go up (if anyone has any money left). Everyone else is busy ducking Guido, because the value of what they had left in their portfolio was not enough to cover margin. Er, I think

Anyway, that's Guy's course negative 101, on the current status of oil prices.

We come full circle back to the Jan. 2009 Lows! Lowest was Jan 16 at $36.GuyM x Ignored says: 12/24/2018 at 10:35 pm

Folks, I think we hit a recession!Recession usually lags 9 months after the market crash, but, yeah. We are basically there.Dennis Coyne x Ignored says: 12/25/2018 at 7:30 amRecession is based on GDP not the stock market or price of oil.GuyM x Ignored says: 12/25/2018 at 7:47 amhttps://www.bea.gov/data/gdp/gross-domestic-product

Q3-2018 was 3.4% GDP growth. Very good for an advanced economy.Of course. But traditionally, crashes take from cash/growth after a period of time. Nine months to a year, and growth in GDP precedes bull markets by the same. It's not a fritzing law, but it's logical, and normal. Has been since I started following it in the 60's. Last crash was different, in that the GDP growth declined before the crash, due to housing. But, if the crash persists, my bet would be a lack of cash, eventually, to support growth. There are huge losses, we don't see that are happening now in the derivative market, besides the stock markets. There was something like 384 trillion just in interest rate bets in derivatives,that half are losing right now.HHH x Ignored says: 12/25/2018 at 8:04 amThis is no traditional crash. FED can stop hiking interest rates and market might pause an consolidate before going lower but lower they go. Until FED stops allowing it's balance sheet to shrink, down is the direction for markets. Back when QE was full blown stuff like gov. shutdown and trade wars were the very thing that made markets go higher because it meant more QE for longer.GuyM x Ignored says: 12/25/2018 at 8:12 amThere is nothing organic about the recovery of markets since 2008-2009. All assets and markets are mispriced. Price discovery wasn't allowed to happen after 2008-2009. Truth is true price discovery won't be allowed to happen this time either.

Fed is manufacturing a market crash so they can do the next round of QE. Fact is QE works but you can't end it and you sure as hell can't reverse it. QE creates the illusion that everything is fine. There is a credibility issue if you can't ever end QE though. That's where the Fed finds itself now.

Your right. Each crash is different. This one is just a slow meltdown. And, since I have been following it, there has never been anything organic about market growth, it's always BS. There was nothing organic about the first big market crash in the early part of last century, it was purely speculative. The tulip crash, before established markets was speculative.HHH x Ignored says: 12/25/2018 at 8:46 am

Growth in GDP and markets are two separate animals. Although, as the previous crash proves, GDP decline can affect the market, as well as market crashes affecting GDP.The stock market, and now especially derivatives, are nothing other than a gigantic Las Vegas casino. Elves in the market strive to maintain that there is a relation, but in the end, it doesn't pan out.

Well the Dow has had its largest monthly loss ever recorded this December unless market recovers some of that between now and the end of the year. Slow meltdown maybe not. It's currently at about -4,200 which tops the largest monthly drop during 2008-2009 by about 1,000 points.GuyM x Ignored says: 12/25/2018 at 8:53 amJust further to drop than the previous ones. Half would be about 10k more points. But, there is nothing magical about half, it could stop well before that.HHH x Ignored says: 12/25/2018 at 9:01 am

The analysis of the drop is still being speculated. The ones that make sense, so far, is that there was a lot of market fear (tariffs, ad nauseum). Sell offs happened, snow balling into covering margin calls. If so, that is a normal scenario, but I think the Fed raising interest rates, and continuing to unravel QE is also a major, if not the major reason. There are a bunch of other reasons that don't make a lot of sense. One blaming oil price. I think that is yet to come, but not this time.Unwinding of FED's balance sheet is also on autopilot. They don't have to have a Fed meeting to vote on it like a rate hike. Much easier to deflect the blame elsewhere for the resulting market decline.Ron Patterson x Ignored says: 12/25/2018 at 1:09 pm-4,200 which tops the largest monthly drop during 2008-2009 by about 1,000 points.GuyM x Ignored says: 12/25/2018 at 2:19 pmHey, it it's the precentage drop that counts. What was the largest monthly percentage drop in the 2008-2009 crash? I would wager it was far greater than the percentage drop this December.

This article is about the huge 1,175 one day drop last February, but the point still holds.

Dow Jones Suffers Worst Point Drop Ever, But Percentage Loss Is Not Historic