|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

| Jan | Feb | Mar | Apr | May | June | July | Aug | Sep | Oct | Nov | Dec |

|

|

|

|

Yahoo! Finance

Investing in a 401(k) plan allows you to defer paying income tax on the money you save for retirement, helps automate your decision to save for retirement by having the money withheld from your paycheck and often allows workers to get valuable employer contributions. However, investing in a 401(k) plan isn't always worth it, especially if your plan has high fees, poor investment choices and no employer contributions. Here's how to tell if your employer is providing a subpar 401(k) plan:

No immediate eligibility. Ideally, you should start saving in a 401(k) plan with your first paycheck, but many employers won't let you. Only 54 percent of 401(k) plans offer immediate eligibility, according to a recent Vanguard analysis of 2,000 401(k) plans with 3 million participants. And 16 percent of 401(k) plans require workers to be with the company for an entire year before they are able to put their money in the plan. "It's sort of a legacy of when record keeping was more manual," says Jean Young, a senior research analyst for the Vanguard Center for Retirement Research. "You want to make sure that somebody is going to be with your organization before you enroll them."

[Read: 10 Trendy 401(k) Plan Perks.]

No employer contributions. Most Vanguard 401(k) plans (91 percent) offer an employer contribution. The best 401(k) plans immediately provide employer contributions to workers, but the majority of 401(k) plans impose a waiting period before new employees are eligible for a match or other company contributions. Many 401(k) plans require between one and six months (27 percent) or even an entire year of service (28 percent) before employees become eligible for a 401(k) match.

A very small match. The maximum possible match employees can get is a median of 3 percent of pay among all Vanguard 401(k) plans. The bottom quarter (24 percent) of 401(k) plans offer a maximum possible employer match of less than 3 percent. The top 15 percent of plans provide employer matches worth 6 percent or more of pay.

A match that is difficult to take advantage of. Employer contributions vary considerably by employer, with Vanguard alone administering 401(k)s with more than 200 different match formulas. Almost half (48 percent) of 401(k) plans require employees to contribute 6 percent of their pay to the 401(k) plan to capture the maximum possible 401(k) match. Other employers require workers to save between 3 and 5 percent of pay (37 percent) or at least 7 percent (11 percent) to get the entire match offered.

The exact match formula plays a role in how easy it is for employees to actually take advantage of company 401(k) contributions. The most common 401(k) match is 50 cents for each dollar contributed up to 6 percent of pay, and 24 percent of 401(k) plans use this match formula. Another 14 percent of 401(k) plans offer a multi-tier match formula such as $1 for each dollar saved on the first 3 percent of pay and 50 cents for every dollar contributed on the next 2 percent of pay. And 7 percent of plans cap the maximum amount of employer contributions workers can get.

Match formulas have the biggest impact on workers who can only afford to save a small amount. Consider a worker who is able to save 3 percent of her salary in a 401(k) plan. If her employer matches 50 cents for each dollar contributed up to 6 percent of pay, she would get 1.5 percent of her pay as a 401(k) match instead of the maximum possible match of 3 percent. If her employer instead matched dollar for dollar the first 3 percent of pay, she would be able to take advantage of the entire match offered with the same maximum potential cost to her company.

[Read: 10 Things You Should Know About Your 401(k) Plan.]

No nonmatching contributions. Some employers contribute to a 401(k) plan on behalf of employees without them having to save anything on their own, contributing a median of 4.2 percent of pay. The most generous 401(k) plans (16 percent) provide employer contributions worth 10 percent or more of worker salaries.

Long vesting schedule. Employees who leave a job before they are vested in the 401(k) plan could forfeit some or all of their employer's contributions. Only 44 percent of 401(k) plans offer immediate vesting, which means you will get to keep all of your employer's contributions whenever you leave the company. Some 401(k)s have cliff vesting schedules in which you don't get to keep any of your employer's 401(k) contributions until you have been employed by the company for a specific number of years. "If you are likely to change jobs a lot because of the nature of your career, and the company has a generous match but that is subject to a three- or five-year cliff vesting schedule, it's not likely to benefit you," says David Loeper, author of "Stop the Retirement Rip-off: How to Avoid Hidden Fees and Keep More of Your Money." Other employers have graded vesting schedules in which you get to keep a gradually increasing proportion of your employer's contributions based on your years of service - typically getting to keep the entire 401(k) match only after five or six years of service. "The employer doesn't want to invest in the employee and then have the employee up and take off," says Christopher Carosa, a retirement plan consultant and chief contributing editor of FiduciaryNews.com. "From the employee's standpoint, it's better to have immediate vesting."

Poor investment choices. The average Vanguard 401(k) plan offered 27 investment options in 2012, up from 16 in 2003, many of which were recently added target-date funds. "If you have more than 20 options it's probably not going to be a user-friendly plan," Carosa says. "It's going to put too much of the burden of deciding what to invest in on the employee." However, almost half of Vanguard 401(k) plans now offer at least four low-cost index funds that invest in U.S. equities, international equities, bonds and cash, up from a quarter in 2004. "The index core is going to have the lowest cost typically, and costs have been demonstrated to be very important in terms of predicting future outcomes," Young says.

[Read: 10 Secrets of Successful Retirement Savers.]

High fees. Most 401(k) plans charge a variety of fees ranging from record-keeping costs to expense ratios on each investment option. You want to make sure that the expenses aren't excessively high. "An easy to remember rule of thumb is to look and see who is selling the fund to the plan. If the fund is being sold by a broker or an insurance company that is working in a non-fiduciary capacity there is a good chance that you will have these excess fees," Carosa says. "You want to make sure that none of the options in the plan have 12b-1 fees or revenue sharing."

401(k) plans are now required to give all investors information explaining the fees associated with each investment option in the plan, due to new U.S. Department of Labor rules. Make sure you look at these quarterly and annual 401(k) statements, and keep costs in mind when making investment decisions. "The fee is 100 percent certain; the return is not guaranteed," Loeper says. He recommends aiming to pay no more than 75 basis points for most investments, and less than 20 basis points for index funds. "If you are paying more than three-quarters of a point," he says, "somebody is making excess profits or is gambling with your money."

whenever the average price of a gallon of gasoline in the U.S. has risen above $3.80 during the past three years, a stock market decline has always followed.

#4 New home prices just experienced their largest two month drop since Lehman Brothers collapsed.

#5 During the last financial crisis, the mortgage delinquency rate rose dramatically. It is starting to happen again.

#6 Prior to the financial crisis of 2008, there was a spike in the number of adjustable rate mortgages. It is happening again.

#7 Just before the last financial crisis, unemployment claims started skyrocketing. Well, initial claims for unemployment benefits are rising again. Once we hit the 400,000 level, we will officially be in the danger zone.

#8 Continuing claims for unemployment benefits just spiked to the highest level since early 2009.

#9 The yield on 10 year Treasuries is now up to 2.60 percent. We also saw the yield on 10 year U.S. Treasuries rise significantly during the first half of 2008.

#10 According to Zero Hedge, "whenever the annual change in core capex, also known as Non-Defense Capital Goods excluding Aircraft shipments goes negative, the US has traditionally entered a recession". Guess what? It is rapidly heading toward negative territory again.

#11 Average hourly compensation in the United States experienced its largest drop since 2009 during the first quarter of 2013.

#12 In the month of June, spending at restaurants fell by the most that we have seen since February 2008.

#13 Just before the last financial crisis, corporate earnings were very disappointing. Now it is happening again.

#14 Margin debt spiked just before the dot.com bubble burst, it spiked just before the financial crash of 2008, and now it is spiking again.

#15 During 2008, the price of gold fell substantially. Now it is happening again.

#16 Global business confidence is now the lowest that it has been since the last recession.

#17 Back in 2008, the U.S. national debt was rapidly rising to unsustainable levels. We are in much, much worse shape today.

#18 Prior to the last financial crisis, Federal Reserve Chairman Ben Bernanke assured the American people that home prices would not decline and that there would not be a recession. We all know what happened. Now he is once again promising that everything is going to be just fine.

"Minsky moment" -- a sudden fall in asset values bloated by credit.

Blackhalo

Cinco-X wrote:

Telegraphing your punches is almost always a bad idea.

The market is now the Fed's adversary? I think Ben's practice of giving the market at least 6 months notice, is one of the smarter things he does.

"Is the explanation as to why markets fell - a drop of 2% or worse is something that has happened literally 1000s of times previously - accurate? Was the 675th worst one day (2.34%) Dow selloff in history all about the Fed's taper of their bond purchases?"

Employers have long hoped that simpler 401(k) plans would entice more workers to save. But for more-savvy investors, that may not be good news.Many companies have pruned the number of investment options in their plans to keep workers from feeling overwhelmed by too much choice. General Motors Corp. and Delphi Corp., for instance, recently cut these options by nearly half. Meanwhile, other companies have loaded up their plans with a slew of target-date funds -- one-stop shopping for retirement savers -- while shrinking the variety of other funds.

But simple isn't always better. In paring choices, companies may be reducing workers' ability to diversify their assets, leaving them exposed to the downdrafts that sometimes roil stocks and bonds simultaneously.

|

|

Switchboard | ||||

| Latest | |||||

| Past week | |||||

| Past month | |||||

| 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 |

"The US economy desperately needs less of our bloated, unproductive and increasingly parasitic banking system … The banking system has become an agent of destruction for the gross domestic product and of impoverishment for the middle class." David Stockman, |

|

| Government by organized money is just as dangerous as Government by organized mob.

FDR, 1936 "The trouble with capitalism is capitalists; they're too damn greedy." Herbert Hoover |

Employers have long hoped that simpler 401(k) plans would entice more workers to save. But for more-savvy investors, that may not be good news.Many companies have pruned the number of investment options in their plans to keep workers from feeling overwhelmed by too much choice. General Motors Corp. and Delphi Corp., for instance, recently cut these options by nearly half. Meanwhile, other companies have loaded up their plans with a slew of target-date funds -- one-stop shopping for retirement savers -- while shrinking the variety of other funds.

But simple isn't always better. In paring choices, companies may be reducing workers' ability to diversify their assets, leaving them exposed to the downdrafts that sometimes roil stocks and bonds simultaneously.

WSJ.com

Conventional wisdom usually advises older investors and retirees to balance a portfolio of bonds, stocks and annuities to squeeze the most from their savings during the third stage of life.

But recent events on Wall Street and in Washington, including a booming stock market and Federal Reserve warnings about "tapering" its easy-money policy, suggest those investors may need to junk conventional wisdom and think again.

... ... ...

Stocks may be too expensive, while bonds are likely to fall as the Fed pulls back and interest rates rise.

The best asset for many investors right now may simply be cash-money-market funds or short-term certificates of deposit. That's especially true for retirees, who rely on their low-risk investments for both income and capital preservation.

But rising stock prices produce risks as well as gains. At current levels, U.S. stocks offer a paltry dividend yield of just about 2.1%-meaning a retiree investing $100,000 in the S&P 500 will earn just $2,100 a year in dividends.

Stock prices are now at very high levels compared with average corporate earnings for the preceding decade, or compared with the replacement cost of corporate assets-two indicators that many economists note have in the past been very good predictors of stock-market returns. When shares have been this expensive on such measures in the past, they have usually turned out to be a poor investment.

The interest rates on bonds have picked up from the historic lows seen earlier this year, but they remain very low by long-term standards.

The 10-year Treasury note offers a yield of just 2.5%, and the Barclays index of corporate bonds isn't much better at 3.2%. Inflation-protected Treasury bonds are so expensive they offer a guaranteed loss of purchasing power for the next seven years.

The picture is little better for immediate annuities, insurance products that allow retirees to convert a lump sum into a guaranteed income stream for life. According to Hersh Stern, an industry expert and the head of ImmediateAnnuities.com, a comparison website, payout rates on annuities remain little improved on the record lows seen a few months ago.

Thomas Burke

Good job of telling the truth....the bond-equity conundrum makes things very challenging....I hold more cash today, both % and $$, than I have in years....taking a buy-on-weakness and DCA approach, on top of flight-to-quality and "don't fight the tape".

The above notwithstanding, the recent bail-out of bonds, coupled with the huge inflow to stock mutual funds, suggest some contrarian thinking might be in order.

Time for some additions to foreign, European, and emerging markets?

Irvine Mcquarrie

Holding individual T-Notes/Bonds is never a bad idea. As long as they're held to maturity, they can't "fall in value." You'll get 100% of your investment back. Holding T-Note/Bond mutual funds is another matter entirely, since whenever you need that money it could be worth less than what you paid in, much less.

Frank Dickof

Cash may be king......but your retirement kitty will get eaten up as it is earning ZERO return. Retirees need to take a long ball view of their funds. Split it into 3 buckets .....

1. Money you need in the next five years (cash or short term bond ladder maturing 1 to 5 years),

2. Money you need 5-10 years down the road (ETF's with about 75% bonds/25% stock balance),

3. Money needed greater than 10 years (ETF's almost all in stocks). For the last bucket you can dollar cost average into it over a year or so to smooth out the effects of the market. Rebalance as the years go by.

Gerard Muller

I don't think you've understood what this article was about.

The formulation you describe was just fine when bonds were providing historical returns and equities weren't being inflated artificially by an, admittedly, transient Fed policy. But as it is, if someone were to follow your prescription today they would be buying bonds whose current pathetic returns would be driven even lower when QE ends and equities whose value would also drop to an unsupported level. In other words they would likely lose their wealth big time.

The author's analysis is correct as things stand today. We are poised to soon see a return to un-stimulated economic times. What those times will look like is something that retirees should find more attractive than the bucket formulation you prescribe now, if they don't they'll at least have most of their, admittedly somewhat eroded, wealth intact.

James Drake

The Japanese experience of prolonged cheap money may well be our experience. In which case, planning to spend the principal and die broke a suitable option.

Michael H Mitchell

"if you assume a 5% return and 3% inflation " Key word there is ASSUME!!! If your assumption is wrong, and it could well be if the Fed bungles this unprecedented monetary expansion, 70's type inflation will kill you.

john boyer:

As a general rule of life I have said the longer you wait to make a decision the better. It gives me more time to wait for facts and information to come to me. We know for an almost certainty that bonds will fall. I am not so certain for stocks as they are not so monolithic as the bond market unless you go for an index fund or mutual fund. Having a pile of cash lets me sleep at night while I contemplate my next move. I have more control over my expenses so I know how quickly I will be bleeding out my cash. Investment decisions will be made but not just now. Though from almost any measure I could retire now I continue to work for a modest income as I know I may need it some day. Continuing to work does not cost me anything other than the chance to be simply idle. As has been posited by Mr. Taleb of Black Swan fame and Antifragile it is all about the cheapest option. Right now staying in cash seems to be the cheapest option for the highest return.

whenever the average price of a gallon of gasoline in the U.S. has risen above $3.80 during the past three years, a stock market decline has always followed.

#4 New home prices just experienced their largest two month drop since Lehman Brothers collapsed.

#5 During the last financial crisis, the mortgage delinquency rate rose dramatically. It is starting to happen again.

#6 Prior to the financial crisis of 2008, there was a spike in the number of adjustable rate mortgages. It is happening again.

#7 Just before the last financial crisis, unemployment claims started skyrocketing. Well, initial claims for unemployment benefits are rising again. Once we hit the 400,000 level, we will officially be in the danger zone.

#8 Continuing claims for unemployment benefits just spiked to the highest level since early 2009.

#9 The yield on 10 year Treasuries is now up to 2.60 percent. We also saw the yield on 10 year U.S. Treasuries rise significantly during the first half of 2008.

#10 According to Zero Hedge, "whenever the annual change in core capex, also known as Non-Defense Capital Goods excluding Aircraft shipments goes negative, the US has traditionally entered a recession". Guess what? It is rapidly heading toward negative territory again.

#11 Average hourly compensation in the United States experienced its largest drop since 2009 during the first quarter of 2013.

#12 In the month of June, spending at restaurants fell by the most that we have seen since February 2008.

#13 Just before the last financial crisis, corporate earnings were very disappointing. Now it is happening again.

#14 Margin debt spiked just before the dot.com bubble burst, it spiked just before the financial crash of 2008, and now it is spiking again.

#15 During 2008, the price of gold fell substantially. Now it is happening again.

#16 Global business confidence is now the lowest that it has been since the last recession.

#17 Back in 2008, the U.S. national debt was rapidly rising to unsustainable levels. We are in much, much worse shape today.

#18 Prior to the last financial crisis, Federal Reserve Chairman Ben Bernanke assured the American people that home prices would not decline and that there would not be a recession. We all know what happened. Now he is once again promising that everything is going to be just fine.

WSJ.com

Conventional wisdom usually advises older investors and retirees to balance a portfolio of bonds, stocks and annuities to squeeze the most from their savings during the third stage of life.

But recent events on Wall Street and in Washington, including a booming stock market and Federal Reserve warnings about "tapering" its easy-money policy, suggest those investors may need to junk conventional wisdom and think again.

... ... ...

Stocks may be too expensive, while bonds are likely to fall as the Fed pulls back and interest rates rise.

The best asset for many investors right now may simply be cash-money-market funds or short-term certificates of deposit. That's especially true for retirees, who rely on their low-risk investments for both income and capital preservation.

But rising stock prices produce risks as well as gains. At current levels, U.S. stocks offer a paltry dividend yield of just about 2.1%-meaning a retiree investing $100,000 in the S&P 500 will earn just $2,100 a year in dividends.

Stock prices are now at very high levels compared with average corporate earnings for the preceding decade, or compared with the replacement cost of corporate assets-two indicators that many economists note have in the past been very good predictors of stock-market returns. When shares have been this expensive on such measures in the past, they have usually turned out to be a poor investment.

The interest rates on bonds have picked up from the historic lows seen earlier this year, but they remain very low by long-term standards.

The 10-year Treasury note offers a yield of just 2.5%, and the Barclays index of corporate bonds isn't much better at 3.2%. Inflation-protected Treasury bonds are so expensive they offer a guaranteed loss of purchasing power for the next seven years.

The picture is little better for immediate annuities, insurance products that allow retirees to convert a lump sum into a guaranteed income stream for life. According to Hersh Stern, an industry expert and the head of ImmediateAnnuities.com, a comparison website, payout rates on annuities remain little improved on the record lows seen a few months ago.

Thomas Burke

Good job of telling the truth....the bond-equity conundrum makes things very challenging....I hold more cash today, both % and $$, than I have in years....taking a buy-on-weakness and DCA approach, on top of flight-to-quality and "don't fight the tape".

The above notwithstanding, the recent bail-out of bonds, coupled with the huge inflow to stock mutual funds, suggest some contrarian thinking might be in order.

Time for some additions to foreign, European, and emerging markets?

Irvine Mcquarrie

Holding individual T-Notes/Bonds is never a bad idea. As long as they're held to maturity, they can't "fall in value." You'll get 100% of your investment back. Holding T-Note/Bond mutual funds is another matter entirely, since whenever you need that money it could be worth less than what you paid in, much less.

Frank Dickof

Cash may be king......but your retirement kitty will get eaten up as it is earning ZERO return. Retirees need to take a long ball view of their funds. Split it into 3 buckets .....

1. Money you need in the next five years (cash or short term bond ladder maturing 1 to 5 years),

2. Money you need 5-10 years down the road (ETF's with about 75% bonds/25% stock balance),

3. Money needed greater than 10 years (ETF's almost all in stocks). For the last bucket you can dollar cost average into it over a year or so to smooth out the effects of the market. Rebalance as the years go by.

Gerard Muller

I don't think you've understood what this article was about.

The formulation you describe was just fine when bonds were providing historical returns and equities weren't being inflated artificially by an, admittedly, transient Fed policy. But as it is, if someone were to follow your prescription today they would be buying bonds whose current pathetic returns would be driven even lower when QE ends and equities whose value would also drop to an unsupported level. In other words they would likely lose their wealth big time.

The author's analysis is correct as things stand today. We are poised to soon see a return to un-stimulated economic times. What those times will look like is something that retirees should find more attractive than the bucket formulation you prescribe now, if they don't they'll at least have most of their, admittedly somewhat eroded, wealth intact.

James Drake

The Japanese experience of prolonged cheap money may well be our experience. In which case, planning to spend the principal and die broke a suitable option.

Michael H Mitchell

"if you assume a 5% return and 3% inflation " Key word there is ASSUME!!! If your assumption is wrong, and it could well be if the Fed bungles this unprecedented monetary expansion, 70's type inflation will kill you.

john boyer:

As a general rule of life I have said the longer you wait to make a decision the better. It gives me more time to wait for facts and information to come to me. We know for an almost certainty that bonds will fall. I am not so certain for stocks as they are not so monolithic as the bond market unless you go for an index fund or mutual fund. Having a pile of cash lets me sleep at night while I contemplate my next move. I have more control over my expenses so I know how quickly I will be bleeding out my cash. Investment decisions will be made but not just now. Though from almost any measure I could retire now I continue to work for a modest income as I know I may need it some day. Continuing to work does not cost me anything other than the chance to be simply idle. As has been posited by Mr. Taleb of Black Swan fame and Antifragile it is all about the cheapest option. Right now staying in cash seems to be the cheapest option for the highest return.

Jul 25, 2013 | WSJ.com

"A positive correlation between treasury yields and equities implies that bonds would act as a hedge for equities and can justify higher allocation to Treasuries in spite of their lower expected returns," Barclays's Maneesh Deshpande, Rohit Bhatia, Ashish Goyal and Arnab Sen wrote in a research note. But with that correlation gone, Treasurys are no longer a viable hedge.

So the Barclays analysts there have asked "What gives?"

They note that some have explained this shifting relationship by saying it's a function of investor expectations about the outlook for Federal Reserve policy, others, a flight to safety dynamic.

But Barclays suggests another reason. "The most credible explanation is simply that the interest rate equity correlation is systematically inversely related to the level of interest rates."

In other words, when interest rates are exceptionally low stocks and bonds are likely to be positively correlated. In high rate environments, stocks should be negatively correlated with interest rates.

Here's the key takeaway:

During low interest rate periods, risks to the equity market are more from deflationary pressures than from inflationary pressures. Any rise in interest rates would be considered good news by the equity market as it would reflect higher expected inflation (and thus lower deflationary risk) in the future. Thus, in a low rate environment, equities should be positively correlated with interest rates. In contrast, during high interest rate periods, a bigger concern for the market is a further increase in inflation. In this environment, any rise in interest rates would likely reflect higher inflationary expectations in the future and consequently be taken negatively by the equity markets, as higher inflation makes longterm planning more difficult and also raises the spectre of stagflation. Hence in high interest rate regimes, equities should exhibit negative correlation with interest rates.

Another factor, they note, can be unexpected moves by the Fed. "In the short term, surprises in Fed policy can actually lead to lower correlation," four strategists wrote in the note.

"Correlation is expected to be low or negative in periods when the Fed appears more dovish or hawkish than the market expects," they wrote. "These periods of low correlation are usually short in nature as the market quickly resets to the Fed's new stance."

The Barclays strategists don't see the near-zero correlation lasting long. "We believe correlation is likely to become positive going forward once the uncertainty over the Fed policy is removed," they wrote.

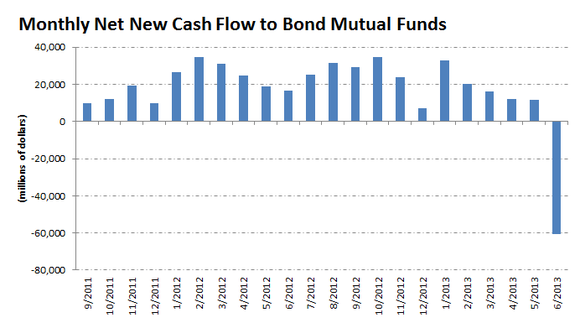

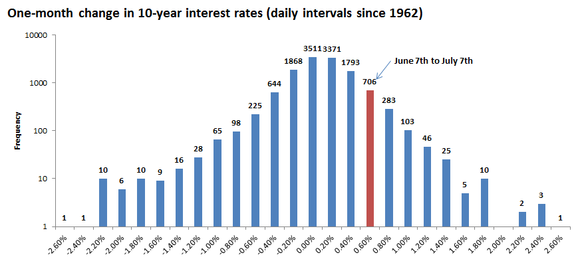

By Morgan Housel | More Articles | Save For Later

July 9, 2013 | Comments (5)Take a look at this chart. It shows the monthly flows to bond mutual funds over the last two years. See if you can spot the outlier:

Source: ICI.

Suddenly, nobody wants bonds.

That's understandable. Interest rates are rising, and for the first time in years, bonds are losing money. The PIMCO Total Return Fund is down 5.6% since April. The Vanguard Long Term Corporate Bond ETF (NASDAQ: VCLT ) is off nearly 10% in the last three months. The popular iShares Barclays 20 Year Treasury Bond ETF has lost more than 11% in the last 90 days.

But what's interesting -- maybe scary -- to think about is that the rise in interest rates over the last month isn't that large, historically. Interest rates on 10-year Treasury bonds have increased by about 60 basis points in the last month, according to data from the Federal Reserve. In percentage terms, that's a lot. But interest rates are so low right now that percentage gains can be deceptive -- a doubling of interest rates from last summer's lows would mean a gain of only a little more than one percentage point.

In absolute terms, the rise in interest rates over the last month isn't that impressive:

Source: Federal Reserve, author's calculations.

If bond investors have panicked at what has been a pretty mild rise in interest rates, what will they do when rates really start to rise?

It won't be pretty. My guess is there will be a few more outliers on that first chart.

On July 09, 2013, at 5:22 PM, SkepikI wrote:

"But what's interesting -- maybe scary -- to think about is that the rise in interest rates over the last month isn't that large,"

Scary indeed Morgan. Thank you for writing this article destined to be consigned to obscurity and ignored by those who need it most. It saves me from my own nagging urge to write one.

And if you readers think THAT'S scary, think about this: rates were so low and still are so low, the mild decline in prices have completely wiped out the interest earnings for the last 6 or 8 months! You Bond owners and fund investors are NOT being paid for the fearsome risks you are running from oppressed interest rates and artificially inflated bond prices.

What ought to be stark terror of inevitable return to normalcy is significantly absent for Bond investors. Just consider this thought experiment: What happens to the price of your bond funds with duration near 10 (as many long term are like Vanguard) when interest rates adjust up by a mere 1%? Price down 10%...lost every bit of interest earned in the past, what 4 years? UGLY! (simulate panic here)

And that's only a 1% change. How much do YOU think interest rates are depressed by?

Report this Comment On July 10, 2013, at 3:30 PM, StockGamingCom wrote:

Bonds seem over-sold. However, in the long run, there's a higher probability that interest rates will go up than down. Therefore, one can play the bounce but the long term viability is a big question mark.

Report this Comment On July 10, 2013, at 10:53 PM, KKoleto wrote:

I had always read to go with intermediate bond funds. Maybe that "set it and forget it" approach is a mistake. What I can't get past is when equities tanked a few years back I just stiffened my lip and waited it out, doing some shopping along the way.

So why am I so nervous with these bond funds going South? Anyway, I am now looking at building a short bond ladder with the thought that rates will rise over time.

Funny, my first mortgage in 1970 was for 7.9. I was told I'd never see rates that low again!

Report this Comment On July 12, 2013, at 11:36 AM, Grimsyke wrote:

I'm new to making comments and perhaps I am in the group of people that the government feels do not understand basic finances but I read today that the government announced it is going to continue their economic stimulus for the next while and the news says the stock markets soared on this good news.

According to my understanding, their "stimulus" is done by spending $85 Billion a month to buy their own debt issues and they are doing this with extra money that they are printing. That is a Trillion dollars a year and they have been doing this for a few years now. Maybe I'm wrong but that seems like a recipe for massive inflation and increases in interest rates if I ever saw one. This seems crystal clear to me.

What I don't understand is why the media and experts are raving that this is a good thing and celebrating??

Report this Comment On July 13, 2013, at 8:20 PM, Zeppelin6880 wrote:

If you've recently bought bonds (i.e. in the last year or so), yes you've taken a hit. If you've had bonds since 2007 like myself you are still up HUGE when taking into account capital gains due to decreasing interest rates. So a one month rise in interest rates does not concern me, and the Fool should know this best as they advocate for a long-term investing approach.

Also, people have been saying for years rates have nowhere to go but up. They've been wrong. I still think the 1.4% or so the 10 yr Treasury hit will again be breached once Europe blows up this year or next (not literally, but financially, just in case the NSA is reading this). The European crisis is anything but over. Greece, Portugal, Italy, Spain, et al are just a precursor to what will occur when investors realize FRANCE is the real risk. Once that situation boils over again money will come across the Atlantic again driving down our rates here. You could see a 1% 10 yr Treasury, which 5 or 6 years ago would have been an impossible thought.

Just a warning, but interest rates can stay low and remain there much longer than seems possible. Just look at Japan. Many a money manager's career has been ruined by betting on a rise in Japanese interest rates.

Cash may be best right now, as the risk/reward ratio for both stocks and bonds seems bad. Stocks are priced at a premium when looking at Shiller P/E (CAPE, cyclically adjusted P/E). Once corporate profit margins revert to the mean (and they ALWAYS have), stocks will get hammered. When this will happen is anyone's guess, but you've been warned.

Stay in short-term bond funds so you can re-invest at higher yields as they rise. Buy gold/silver (5-10% of your portfolio) as insurance.

At these all-time-high prices, just how much riskier stocks are than alternatives like bonds, cash or gold depends largely on how you define "risk." William Bernstein, an investment manager at Efficient Frontier Advisors in Eastford, Conn., and the author of several books on investing and and financial history, says risk takes two basic forms-and understanding the difference can help investors figure out what they should be afraid of.

What Mr. Bernstein calls "shallow risk" is a temporary drop in an asset's market price; decades ago, the great investment analyst Benjamin Graham referred to such an interim decline as "quotational loss."

Shallow risk is as inevitable as weather. You can't invest in anything other than cash without being hit by sharp falls in price.

"Shallow" doesn't mean that the losses can't cut deep or last long-only that they aren't permanent. "Deep risk," on the other hand, is an irretrievable real loss of capital, meaning that after inflation you won't recover for decades-if ever.

BigW wrote:

The world is not quite as simple as this makes it sound. If I buy stock in an individual company and that company makes bad decisions or is overwhelmed by events beyond its control, then I will lose money. I won't magically get that money back later because investing in the stock market represents "shallow risk". Even a broad index fund is subject to the decisions made by the companies it contains. There is no magic here – the best remedy to risk is diversification. Understand that you aren't going to make perfect decisions with imperfect knowledge of the future. Some things will work out, some things won't. But no single or even group of decisions you make will sink you. Before making any investment – I always ask one question – what happens to me if I never see a DIME of the money again? When the answer to that question becomes something like – I won't be able to retire, I will lose my house, then that means it is ALWAYS a bad investment, no matter how attractive it may appear at the time.

12:37 pm July 27, 2013

James Bucholtz wrote:There is nothing new in this book. The author has simply taken old concepts and wrapped them in a new outer coat. Seriously you can summarize the article as simply saying that at times downturns are mild and at others they are persistent and severe. What would have been useful would be a way to predict which was which however predicting the future state of a non linear dynamical system is impossible.

11:53 am July 27, 2013

Ray Zemon wrote:One must remember, ex post you know the state you were in, but ex ante you only know a subjective probability distribution of future states.

In late 2008, there was a real possibility of a "deep risk" state (deflation). I believe that's why the market dropped as much as it did and, as the likelihood of a "deep risk" state declined, came back so quickly,10:24 am July 27, 2013

Lee Zehrer wrote:I would think time would be a factor in evaluating risk?

Or are we actually talking about volatility?

7:50 pm July 26, 2013

Anonymous wrote:BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY BUY.

Thanks,

Wall Street

arthur_dent

for those who think QE and financial repression have not been a fantastic bonanza and giveaway to corporate America, you might want to read this, from Reuters,

Analysis: How much is Fed aid to U.S. corporate profits worth?

just keep repeating to yourself, the Fed is doing it to create jobs and Janet Yellin will create even more jobs.

blinkered )

arthur_dent wrote:

for those who think QE and financial repression have not been a fantastic bonanza and giveaway to corporate America, you might want to read this, from Reuters,

As much as I abhor artificially low rates and their unintended consequences, I can tell you at my fortune 500 company, there has been no austerity because of the robust profits so there is a little truth to the jobs benefit. Is that the best way to help jobs? I sure hope not.

July 24, 2013

Tim Duy:

save_the_rustbelt said...Shock and Awe(ful), by Tim Duy: Yesterday's hot story from Ezra Klein that Larry Summers was the lead candidate for the top spot at the Federal Reserve was greeted with shock and awe(ful). I wish I could say that I was surprised, but at the end of last month I tweeted:

I often think we have prematurely declared Janet Yellen the front runner. We forget that politics will be in play. http://t.co/ghIPnl0kjj

My concerns were only reinforced when news broke last week of the campaign against current Vice Chair Janet Yellen. From Ezra Klein:

The favored parlor game of the political-economic complex right now is guessing who will replace Ben Bernanke as chairman of the Federal Reserve. The clear front-runner is Federal Reserve Vice Chairman Janet Yellen. But she's by no means a sure thing.

One important reason she's not - and I don't know another way to say this - is sexism, as evidenced by the whispering campaign that's emerged against her.

Yesterday, Klein declared Summers the front-runner:

People dismissed Summers's chances a month or two ago, but he's increasingly viewed as the leading candidate today - and opinions on this, for reasons I don't fully understand (though I suspect have to do with a bunch of elite trial balloons going up at the same time), have really hardened in the last 72 hours.

Klein lists a variety of reasons in favor of Summers, most important of which I think is that President Obama and his staff know and like Summers, while Yellen is a virtual unknown in White House circles. This is also the message of Washington Post reporter Zachary Goldfarb's tweet yesterday:

Larry Summers visited White House 14 times in past 2yrs. Janet Yellen visited once, records show. pic.twitter.com/ufFuVbrH7V

- Zachary A. Goldfarb (@Goldfarb) July 23, 2013Reaction was swift and fierce from some quarters of the blogosphere. Cardiff Garcia begins with a defense of Summers:

...Some of the mistakes of his past, such as his role in deregulating derivatives (the Brooksley Born episode) or the Harvard interest rate blowup, don't really tell us much about his capacity to guide macroeconomic stabilisation policy.

His more recent mistakes, specifically his failure to better advise Obama on the stimulus (should have been bigger) and housing policy (should have done more for people in foreclosure and underwater homeowners), included political considerations that are hard to untangle from his actual views.

before launching into his reasons for supporting Yellen, beginning with the most important:

The simplest reason is that she is more conventionally qualified for the job, boasting a much longer entry in her CV as a monetary policymaker.

Like him or hate him, Summers lacks Yellen's depth of exposure to monetary policy. If relative experience with monetary policy is a requirement for the job, Yellen clearly has the upper hand. Felix Salmon, not exactly a fan of Summers to begin with, sums up the situation:

...if Obama picks Summers, it won't be on the merits; instead, it will be on the grounds that Obama likes Summers, and is in awe of his intelligence. (Summers is, to put it mildly, not good at charming those he considers to be his inferiors, but he's surprisingly excellent at cultivating people with real power.)

Salmon then launches into an attack on Summers:

What's more, the move would be a calculated snub to bien pensant opinion. Never mind the utter shambles that Summers made of Harvard, or the way he treated Cornell West, or his tone-deaf speech about women's aptitude, or the pollution memo, or the Shleifer affair, or the way he shut down Brooksley Born at the CFTC, or his role in repealing Glass-Steagal, or his generally toxic combination of ego and temper - so long as POTUS likes Larry, and/or so long as Summers is good at working key Obama advisors like Geithner, Lew, and Rubin, that's all that matters.

Evidently, Salmon holds a grudge a bit longer than Garcia. Now, if only President Obama would shift his focus from Summers and Yellen to Ben Stein, then we would see some real fireworks from Salmon.

Mark Thoma has a more succint reaction:

Larry Summers is the Front-Runner? WTF?

Perhaps not all is lost. Back to Klein:

That's not to say Summers is anywhere near a sure thing. His confirmation would be far tougher than Yellen's, as Republicans will make him answer for the stimulus and the bailouts, and progressive Democrats have a list of grievances going back to financial deregulation in the Clinton-era. There's also the simple fact that appointing Yellen would break a significant glass ceiling - and do so in an administration that hasn't always been great about appointing women to top economic positions. And Summers continues to be a polarizing figure: Those who like him love him, but those who don't like him really don't like him.

That said, one gets the feeling that this is not a sudden decision. Instead it is one that has been building for weeks, at least since June 29, when I began to get nervous about the assumption of Yellen as a front-runner. I suspect that if the position has hardened within the White House as Klein suggests, it is because Obama has made his choice and it is time for everyone to get on board.

I have to say that if Yellen is not the pick, I will be disappointed. I think she the best qualified candidate for the job, and agree with the pro-Yellen arguments of Garcia, Salmon, and Bill McBride. I am very concerned about Summer's disposition to be a de-regulator, especially after we see that the Federal Reserve, in its infinite wisdom, gave permission for investment banks to openly manipulate commodity markets. Does anyone see Summers pushing back at that kind of regulation, or getting on board? I don't think that he is the kind of person to take the words of Adam Smith to heart:

The interest of the dealers, however, in any particular branch of trade or manufactures, is always in some respects different from, and even opposite to, that of the public. To widen the market and to narrow the competition, is always the interest of the dealers. To widen the market may frequently be agreeable enough to the interest of the public; but to narrow the competition must always be against it, and can serve only to enable the dealers, by raising their profits above what they naturally would be, to levy, for their own benefit, an absurd tax upon the rest of their fellow-citizens. The proposal of any new law or regulation of commerce which comes from this order ought always to be listened to with great precaution, and ought never to be adopted till after having been long and carefully examined, not only with the most scrupulous, but with the most suspicious attention. It comes from an order of men whose interest is never exactly the same with that of the public, who have generally an interest to deceive and even to oppress the public, and who accordingly have, upon many occasions, both deceived and oppressed it.

Bottom Line: Nothing is certain until the announcement is made and the Senate takes its turn, but it is looking like the White House is pushing to make Larry Summers the next Federal Reserve Chairman. The curse of the Vice Chair would then live on.

Just give the job to Robert Rubin and cut out Larry the middle man.

anne said...

I am very concerned about Summer's disposition to be a de-regulator, especially after we see that the Federal Reserve, in its infinite wisdom, gave permission for investment banks to openly manipulate commodity markets....

-- Tim Duy

[ http://www.nytimes.com/2013/07/21/business/a-shuffle-of-aluminum-but-to-banks-pure-gold.html

July 20, 2013

A Shuffle of Aluminum, but to Banks, Pure Gold

By DAVID KOCIENIEWSKIRegulators have allowed banks to buy companies that trade in commodities, resulting in huge profits for the banks and billions in higher costs for consumers. ]

anne said in reply to anne...Any Federal Reserve executive could have argued against this policy, but to my knowledge no executive including Janet Yellen so much as discussed the policy publicly.

Mark A. Sadowski said in reply to anne...

Yellen last spoke about commodity prices in April 2011. She did not specifically address that policy.

http://www.federalreserve.gov/newsevents/speech/yellen20110411a.htm

beezer said...

Darryl FKA Ron said in reply to beezer...Nice Adam Smith quote. Smith has a bunch of these sprinkled throughout the Wealth of Nations. Conservatives, of course, don't remember them very often.

That was a great Adam Smith quote. I got me interested WoN, where I had not been before. Sounds like Smith would have disagreed with Schumpeter on consolidating firms into monopoly rent seeking behemoths.

pgl said...

It could be worse. Had Romney won last year - the discussion would be whether it would be Glenn Hubbard or John Taylor.

Mark A. Sadowski said in reply to pgl...

Peter K. said in reply to Mark A. Sadowski...Romney also had Greg Mankiw on his short list:

The difference is that all three potential Republican nomineees actually believe monetary policy is effective unlike Summers.

And Mankiw has written about NGDP targeting in the past:

http://www.nber.org/chapters/c8329.pdf

So it's possible he would have pursued a more expansionary rules based policy.

So if you think putting someone who believes monetary policy is ineffective in charge of the nation's monetary policy (what I would call the James G. Watts candidate) is better than candidates who believe it is effective but two of whom are hawks and one who is essentially a dove, then you are right but I'm not so sure.

I usually agree with you but you're wrong about Mankiw. He would have pursued a Republican policy, probably overly tight. He has written a lot of nonsense over the past 4 years all in the service of Team Republican. He's a loyal soldier.

Mark A. Sadowski said in reply to Peter K....

"He would have pursued a Republican policy, probably overly tight."

Under a Republican President? Don't be so sure.

don said in reply to Mark A. Sadowski...

pgl said in reply to Mark A. Sadowski...I was at an NBER conference where Greg presented an argument for eliminating the inheritance tax. He presented a model in which bequest was the motive for amassing wealth. I asked him how is analysis squared with quotes by two other authors: Keynes, who said something like "As I look about me, I see English industry is a little stupid - too much dominated by third generation men" and Adam Smith, who said the purpose of amassing wealth was neither consumption nor bequests, but "the parade of riches." I wonder if Greg really believes that the inheritance tax is inferior to the income tax.

On the other hand, if Greg followed his dictates for monetary policy, with explicit future inflation targeting, it might have been more effective than the current QE policy.

Mark A. Sadowski said in reply to pgl...I think most Keynesians would tell you that monetary policy is very effective under normal conditions but when we are in a liquidity trap fiscal policy becomes the more effective tool. Bernanke believes that. Yellin believes that. Summers believes that. Summers has been screaming for fiscal stimulus true but so has Bernanke. OK, Congress refuses to listen. Maybe Yellin puts more faith in QE and all that but how's that been working of late? Larry Summers is not a 1950's fiscalist. OK?

"I think most Keynesians would tell you that monetary policy is very effective under normal conditions but when we are in a liquidity trap fiscal policy becomes the more effective tool. Bernanke believes that."

How does one define "more" in this context.

"Bernanke believes that. Yellin believes that. Summers believes that. Summers has been screaming for fiscal stimulus true but so has Bernanke."

Bernanke and Yellen have both correctly noted that fiscal policy has been a huge economic drag. But both still strongly believe that monetary policy is highly effective at the zero lower bound. Take Yellen's speech on monetary policy from April 2012:

http://www.federalreserve.gov/newsevents/speech/yellen20120411a.htm

Or Bernanke's speech at Jackson Hole from last year:

http://www.federalreserve.gov/newsevents/speech/bernanke20120831a.htm

Nobody currently in the Board of Governors of the Federal Reserve really believes in the "liquidity trap". Nor would I want anyone who believes that monetary policy is totally impotent to be placed in charge of the nation's monetary policy.

Reply Wednesday, July 24, 2013 at 01:05 PM

Mark A. Sadowski said in reply to pgl...

"Maybe Yellin puts more faith in QE and all that but how's that been working of late?"

Well enough.

The big four advanced currency areas that are currently at or near the zero lower bound in policy interest rates are the U.S., the eurozone, Japan and the U.K.

One proxy for the amount of QE done is monetary base expansion. This isn't perfect of course since it also measures other policy responses such as "credit easing". The ECB has done credit easing but no QE for example. But let's not make things too complicated for the moment.

As of May the BOE's monetary base is up by 348% since August 2008, the Federal Reserve's up by 260%, the BOJ's up by 75% and the ECB's up by 48%:

http://thefaintofheart.files.wordpress.com/2013/06/sadowski3_1.png

Since aggregate demand (AD) is the appropriate measure of the effectiveness of macroeconomic policies whose ultimate purpose is in fact to stimulate AD, perhaps we should look at the relative AD performance of the four large advanced currency areas since the Great Recession. But before we do that, we should take a look at the other main policy tool for stimulating AD, namely fiscal policy.

In my opinion the most objective way of measuring fiscal policy stance is the change in the general government cyclically adjusted balance, particularly the cyclically adjusted primary balance (CAPB). The cyclically adjusted balance takes into account any changes in the general government budget balance due to the business cycle. Thus changes in the cyclically adjusted balance are mostly due to discretionary fiscal policy, and consequently may be taken as a proxy for the degree of fiscal stimulus. The CAPB goes a step further, factoring out changes in net interest on government debt and thus ensuring that practically all of the changes in fiscal balance are discretionary in nature. The following is a graph of the changes in CAPB by currency area over the calendar years 2009-13. All data comes from the April 2013 IMF Fiscal Monitor.

http://thefaintofheart.files.wordpress.com/2013/06/sadowski3_10.png

The first thing you should note is that Japan has had the most expansionary fiscal policy every year without exception. And although all of the currency zones adopted a much less expansionary fiscal policy stance in 2010, it was the U.K. that took the lead in fiscal consolidation, having the most contractionary fiscal policy in both 2010 and 2011. The U.S. has had the most contractionary fiscal policy starting with calendar year 2012.

Now, let's take a look at relative AD performance. To be technical, AD is nominal GDP (NGDP) when inventory levels are static (i.e. nominal Final Sales of Domestic Product). Thus for all intents and purposes AD is virtually identical to NGDP. The following is a graph of the NGDP of the four big advanced currency areas with NGDP indexed to 100 in 2008Q2, that is, before large scale monetary base expansion started in September 2008.

http://thefaintofheart.files.wordpress.com/2013/06/sadowski3_11.png

Note that the U.K. led in relative NGDP growth from 2009Q3 through 2011Q3 with the sole exception of 2011Q2. The U.K. also led in relative monetary base growth from June 2009 through January 2011. And as previously noted the U.K. had the most contractionary fiscal policy in 2010 and 2011.

The U.S. has led in relative NGDP growth since 2011Q4. The U.S. also led in relative monetary base growth from February 2011 through January 2012. And as previously noted the U.S. has had the most contractionary fiscal policy starting with calendar year 2012.

Japan has ranked last in relative NGDP growth throughout. Japan has also ranked last in relative monetary base growth with the exception of March through August 2011 and since April 2013. And as previously noted Japan has had the most expansionary fiscal policy throughout.

Bloix said in reply to pgl..."It could be worse." The motto of the Obama administration.

kharris said...This is at least in part an outgrowth of the Republican war on women. If women voters had anywhere else to go, snubbing a well qualified woman for an arguably less well qualified guy would be stupid politics. As it is, the White House can turn its thoughts to political considerations other than women's votes in making this choice. In this way, the Republican war on women may succeed, producing a major casualty.

Zero Hedge

The secular low in bond yields has yet to be recorded. This assessment for a continuing pattern of lower yields in the quarters ahead is clearly a minority view, as the recent selling of all types of bond products attest. The rise in long term yields over the last several months was accelerated by the recent Federal Reserve announcement that it would be "tapering" its purchases of Treasury and mortgage-backed securities. This has convinced many bond market participants that the low in long rates is in the past. The Treasury bond market's short term fluctuations are a function of many factors, but its primary and most fundamental determinate is attitudes toward current and future inflation. From that perspective, the outlook for long term Treasury yields to fall is most favorable in light of:a) diminished inflation pressures;

b) slowing GDP growth;

c) weakening consumer fundamentals; and

d) anti-growth monetary and fiscal policies.

InflationSustained higher inflation is, and has always been, a prerequisite for sustained increases in long term interest rates. Inflation's role in determining the level of long term rates was quantified by Irving Fisher 83 years ago (Theory of Interest, 1930) with the Fisher equation. It states that long term rates are the sum of inflation expectations and the real rate. This proposition has been reconfirmed in numerous sophisticated statistical studies and can also be empirically observed by comparing the Treasury bond yield to the inflation rate (Chart 1). On an annual basis, the Treasury bond yield and the inflation rate have moved in the same direction in 80% of the years since 1954.

Additional factors restraining inflation are the appreciation of the dollar and the decline in commodity prices. The dollar is currently up 14% from its 2011 lows. A rise in the value of the dollar causes a "collapsing umbrella" effect on prices. A higher dollar leads to reduced prices of imports, which have been deflating at a 1% rate (ex-fuel) over the past year. When importers cut prices, domestic producers are forced to follow. Commodity prices have dropped more than 20% from their peak in 2011. This drop in commodity prices has also contributed to lower rates inflation.

Sustained higher inflation is not currently evident, and the forces that create inflation are absent. Thus, a period of sustained higher long term rates is improbable.

GDP

GDP growth, whether if measured in nominal or real terms, is the slowest of any expansion since 1948. From the first quarter of 2012 through the first quarter of 2013, nominal GDP grew at 3.3%. This is below the level of every entry point of economic contraction since 1948 (Chart 3). Real GDP shows a similar pattern. For the past four quarters real economic growth was just 1.6%, which was even less than the 1.8% growth rate in the 2000s and dramatically less than the 3.8% average growth rate in the past 223 years. These results demonstrate chronic long term economic underperformance.

Over the past year, the Treasury bond yield rose as the nominal growth in GDP slowed. The difference between the Treasury bond yield and the nominal GDP growth rate (Chart 4) is important in two respects. First, when the bond yield rises more rapidly than the GDP growth rate, monetary conditions are a restraint on economic growth. This condition occurred prior to all the recessions since the 1950s, as indicated in the chart. This condition also signaled the growth recessions in 1962 and 1966-67. Second, the nominal GDP growth rate represents the yield on the total economy, a return that embodies greater risk than a 30 year Treasury bond. Thus, the differential is a barometer of cyclical value for investors in Treasury bonds versus more risky assets.

On two occasions in the 1990s the Treasury bond/GDP differential rose sharply. Neither a quasi- nor outright recession ensued, but in both cases bonds turned in a stellar performance over the next year or longer. This economic indicator simultaneously casts doubt on the prevailing pessimism on Treasury bonds and the optimism over U.S. economic growth.

Consumer

Consumers have not yet healed from the great recession. Their income and employment situations have languished. Based on the standard of living, as measured by the real median household income, this entire recovery has bypassed the consumer sector. The standard of living has contracted regularly in recessions, but this is the first time deep into an expansion that it has continued to erode. The current standard of living is unchanged from 1995 (Chart 5).

In spite of job gains in the first half of 2013, the downward pressure on the standard of living actually intensified. Approximately three quarters of the increases in jobs were in four of the lowest paying industries – retail trade; the temporary help services component of professional and business services; hospitality and leisure; and the nursing and residential care facilities component of the medical category. These increases may reflect efforts of firms to minimize the increase in health care costs associated with full time employment under the Affordable Care Act. Part time jobs averaged increases of 93,000 per month in the first half of 2013, while full time jobs averaged increases of only 22,000 per month. Full time employment as a percentage of the adult population is currently 47%, which is near the lows of the last three decades.

Historically, when taxes are increased, the initial response of households results in a lower saving rate rather than an immediate reduction in spending. For some consumers, recognition of the tax changes in their income is a problem, particularly for those whose earnings are dependent on commissions, bonuses or seasonal work. This explains the sharp drop in the personal saving rate to 2.7% in the first five months of this year, a level at or below the entry points of all the economic contractions since 1929. The 2013 slump in the saving rate is a precursor of the painful adjustments that lie ahead, and an additional restraint on economic growth. (Note: In late July the Bureau of Economic Analysis is expected to release a benchmark revision to the National Income and Product Accounts. As a result of the revision the personal saving rate may be raised by up to 1.5%. This is due to the change in consumer ownership of defined benefit pension plans. This revision will no t change the trend of the saving rate, nor will this higher figure indicate a source of funds for immediate spending since consumers will only receive such pension benefits when they retire.)

The drop in the saving rate in 2013 also serves to explain why the primary drain from higher taxes occurs with a lag after the taxes take effect. Based on various academic studies there is a two or three quarter lag in curtailed spending after the tax increase. Thus, the main drag on growth will fall in the third and fourth quarters of this year, with negative residual influences persisting through the end of 2015. Approximately $140 billion of the tax increase constitutes what might be termed a reduction in permanent income, or its equivalent life cycle income. In addition to working with a lag, over a three year period this portion will carry a negative multiplier of between two and three.

Monetary & Fiscal

Astronomical sums of money have been expended by both monetary and fiscal authorities since the crisis. With the benefit of hindsight it is clear their efforts have not aided economic growth, but rather the balance of their actions has been counter productive. The Fed has maintained the Fed Funds rate at near-zero levels, and it has tried to lower longer term rates through a series of quantitative easings. The effect of each of the quantitative easings was the opposite of the Fed's intentions. During every period of balance sheet expansion long rates rose, yet when securities purchases were discontinued yields fell (Chart 6). The Fed cannot control long rates because long rates are affected by inflation expectations, not by supply and demand in the market place. This is extremely counter intuitive. With more buying, one would assume that prices would rise and thus yields would fall, but the opposite occurred. Why? When the Fed buys, it appears that the existing owners of Treasuries (now amounting to $9.5 trillion) decide that the Fed's actions are inflationary and sell their holdings, raising interest rates. When the Fed stops this program, inflation expectations fall creating a demand for Treasuries, bringing rates back down. The Fed's quantitative policies have been counter productive to growth as interest rates have risen during each period of quantitative easing. During QE1 and QE2, commodity prices rose, the dollar fell and inflation rose temporarily. Wages, however, did not respond. Thus, the higher interest rates during all QEs and the fall in the real wage income during QE 1 & 2 served to worsen the income and wealth divide. This means many more households were hurt, rather than helped, by the Fed's efforts.

In terms of government spending, fiscal policy has not, and will not, have a major affect on economic growth. The increased spending immediately following the financial crisis did little to encourage the economy to grow faster. Likewise, the decrease in spending associated with the "sequester" will unlikely be a drag on growth after the initial and lagged effects are fully exhausted. The research on government spending multipliers suggests that the multiplier on spending is very close to zero.

The impact of tax changes is not nearly as harmless. It has been argued that an expired "temporary payroll tax cut" would not effect spending as the initial increase in income was not seen as permanent. The facts seem to counter this opinion. The average monthly year-over-year growth rate of real personal income less transfer payments for 2011 was 3.4%, and in 2012 it was 2.2%. This year, with the payroll tax change in effect, the average is 1.8% through May. The slower income has resulted in a slowdown in spending. Like income, real personal consumption expenditures has trended lower, with average monthly year-over-year growth rates of 2.5% for 2011, 1.9% for 2012 and 1.8% through May of this year. This trend is expected to continue for some time.

A Final Consideration Favoring Bonds

In the aftermath of the debt induced panic years of 1873 and 1929 in the U.S. and 1989 in Japan, the long term government bond yield dropped to 2% between 13 and 14 years after the panic. The U.S. Treasury bond yield is tracking those previous experiences (Chart 7). Thus, the historical record also suggests that the secular low in long term rates is in the future.

Similar Articles You Might Enjoy:

- 2012 Year In Review - Free Markets, Rule of Law, And Other Urban Legends

- Van Hoisington: "Has The Recession Really Ended?"

- Weekly Bull/Bear Recap

- David Stockman: "The Capital Markets Are Simply A Branch Casino Of The Central Bank"

- The Sell-Side Take On The Tepid GDP Growth

07/22/2013 | Zero Hedge

"It's hard to make the case that [US stocks are up 17% on a 2.5% earnings rise]based on fundamentals alone - it's money in motion," is how BofA's CIO Hans Olsen describes the unreality occurring in US asset markets currently. He noted in last week's interview with CNBC that Bernanke's experimentation has created asset-inflation "that would make the stock market bubble of 2000 look like a day at the beach. It's really quite remarkable." Critically, as many have noted, he notes "let the market start to price things based on fundamentals again rather than money printing. The sooner we get back to a market pricing, the more sustainable it becomes."

What is ironic is that Olsen is overweight stocks in spite of all this - but like everyone else in the status quo - is hoping Bernanke keeps the house of cards from collapsing. Olsen appears to be among the very few career bankers willing to tell the truth - the fear being, of course (as we showed here) that it would mean their "skills" are completely meaningless.

Zero Hedge

"Today's markets have a vulnerability that has not existed through most of history. Today's valuations only make sense in light of low expected cash rates. Remove that expectation, and pretty much every asset across the board is vulnerable to a fall in price, as the rising real discount rate plays no favorites. There is no asset class you can hold that would be expected to do well if the real discount rate rises from here.

Under normal circumstances, a rising real discount rate would probably come on the back of rising inflation or stronger than expected growth, which are diversifiable risks in a portfolio. But May's shock to the real discount rate came not because inflation was unexpectedly high or because growth will be so strong as to lift earnings expectations for equities and other owners of real assets, but because the Fed signaled that there was likely to be an end to financial repression in the next few years. And because financial repression has pushed up the prices of assets across the board and around the world, there is unlikely to be a safe harbor from the fallout, other than cash itself." - GMO

Bloomberg

Pacific Investment Management Co.'s Bill Gross said he expects the Federal Reserve won't tighten monetary policy until 2016 at the earliest.

"So bonds come out of their coffin & it's not even Halloween," Gross, who manages Pimco's $268 billion Total Return Fund, said in the posting on Twitter. "Bernanke says follow policy rate & we agree."

... ... ...

The Fed chairman was "relatively dovish" in his outlook on the U.S. economy and monetary policy, according to Mohamed El-Erian, Pimco's chief executive officer. Markets "took the tapering too far" and 10-year Treasury yields may drop to 2.2 percent this year, El-Erian, who is also co-chief investment officer with Pimco founder Gross, said in a July 17 interview.

... ... ...

Gross also added to holdings of mortgage securities in June, the fund's second-largest holdings. The proportion rose to 36 percent last month, from 34 percent in May.

Calculated Risk

robj wrote:

MBS market is very solid

$40 billion/month, rain or shine. Price irrelevant. Solid ponzi.

friar john

High-profile bond fund manager Jeffrey Gundlach has scooped up agency mortgage-backed securities in recent days as many other investors rushed for the exits.

Gundlach, the founder of investment firm DoubleLine Capital and co-manager of the $39.4 billion DoubleLine Total Return Bond Fund, told The Wall Street Journal Tuesday that the recent big selloff, which sent bond yields much higher, represents a buying opportunity.

"We have been buying modestly in recent days and will probably increase exposure when the market settles down," said Gundlach. "A few months ago if you bought MBS, you got a yield of 1%. Now you can buy agency MBS of 4%."

I wouldn't call the MBS market solid from the above article. Sounds like he is hunting for yield.

1 currency now -yogi wrote:

$40 billion/month, rain or shine. Price irrelevant. Solid ponzi.

QE tide goes in; QE tide could go out.

friar john wrote:

Gundlach. "A few months ago if you bought MBS, you got a yield of 1%. Now you can buy agency MBS of 4%."

I wouldn't call the MBS market solid from the above article. Sounds like he is hunting for yield.

Grundlach has done alright for himself and his investors, but past returns may not be predictive. Everyone is hunting for yield, obviously.

He's not the most attractive personality, but he and Bill the Grocer are probably two of the best.

"Solid" was not the best wordchoice, as you suggest. Precisely because of the sell-off Grundlach finds the pricing more attractive, just like the S&P was a bargain 4 years ago. But MBS are not that compelling a value, to be sure, value is relative. Buying after a haircut is always a better value.

Econbrowser

Macroeconomic Advisers estimates second quarter growth at around 0.6% SAAR. [0] Is it because of the sequester and the ending of the payroll tax rate reduction? In part, Jeff Frankel thinks so; see also [1]. Macroeconomic Advisers had predicted something over a 1% reduction in growth rate (SAAR) relative to baseline in the second quarter [2]

Ricardo

Brian,

Menzie is correct. Sequester is not a Republican idea but was an Obama administration plan. The Republicans, as the stupid party, simply signed on.

anonymous

If you're looking for someone to blame for the sequester then blame all of Washington. It does not fall solely on Obama, nor Republicans or Democrats. The blame falls on all of them. Talking about how the sequester is a bad idea is not a partisan debate because it's passage was not partisan either. To be more specific it passed with half of the house Democratics support and about three quarters of Republican house support. In the Senate 45 Democrats supported the measure and 2/3rds of Republicans supported the measure. Boehner said of the sequester that he got 98% of what he wanted, and Obama signed it into law. It's not reasonable to blame this on either party alone.

June 30, 2013 | Econbrowser

Steven Kopits

So let's assume then that China falls into outright recession, the sort of debt crisis we used to associated with emerging (rather than mature) economies. That's my current working assumption. In response, let's suppose the Chinese, to support their financial system, sell, say, $1 trillion of US govt bonds to cover domestic banking losses.

Were this to happen, it would seem that the price of Treasuries would fall, and the interest rate would rise.

Steve

Is that right? How might it play out?

There are a few oddities with the recent move in 10 year rates:

1. It has been associated with declining inflation expectations, not rising ones. 2. The negative impact on emerging market equities and bonds has been outsized relative to most people's expectations. 3. Currency value changes have been strangely small (excepting the yen).

I like the China theory, as it explains these oddities better than the standard explanation that investors suddenly reinterpreted the timing of the Fed's future actions.

Yahoo

Investors listen up: The Fed has NOT decided to reduce its asset purchases later this year, as many were expecting.

In prepared remarks to Congress Wednesday, Fed Chairman Ben Bernanke said the central bank's "asset purchases are by no means on a preset course," dispelling expectations many have held since late May when Bernanke, in another appearance before Congress, said the Fed could decide in the "next few meetings" to taper its bond buys.

Related: Ignore Feldstein, The Fed Should Taper in 2014: Dean Baker

At the same time Bernanke employed the stereotypical balanced approach of economists that's often made fun of:

"On the one hand, if economic conditions were to improve faster than expected, and inflation appeared to be rising decisively back toward our objective, the pace of asset purchases could be reduced somewhat more quickly," said Bernanke. "On the other hand, if the outlook for employment were to become relatively less favorable, if inflation did not appear to be moving back toward 2 percent, or if financial conditions... were judged to be insufficiently accommodative... the current pace of purchases could be maintained longer."

And the winner is: the same pace of asset purchases, says Yelena Shulyatyeva, U.S. economist at BNP Paribas. Bernanke's latest message "is really dovish," she tells The Daily Ticker.

Related: Fed Statement Could Lead to "Amateur Hour" in the Markets

"The Fed is watching the data very closely," Shulyatyeva says, and the data is shaping up to show "slower growth in the second quarter--much slower than the FOMC anticipated."

Indeed, June housing starts fell almost 10 percent to a 10-month low and June retail sales rose 0.4%--half the increase economists had expected--although other economic data suggest the recovery is continuing.

Related: Weak Retail Sales Means Fed Tapering Later vs. Sooner

Shulyatyeva herself says second quarter GDP will likely grow by less than 1%, which means second half growth would have to soar to 3% in order to reach the Fed's annual forecast. And that, says Shulyatyeva is "not possible." She expects the Fed will lower its growth forecast rather than taper its bond purchases anytime soon. Watch the video above to see her demystify how the Fed analyzes the economy and sets strategy.

Firemane wrote on Thu, 7/18/2013 - 6:44 am (in reply to...) Mook wrote:

Four words: Not in labor force.

Except the number of people COVERED by unemployment is steadily marching upward.