Tax policy and tax avoidance under neoliberal regime

Neoliberal government which adopted neoliberal ideology with its belief of self-regulation market and

in which no outside oversight is possible, due to the ability of the kleptocrat(s) to personally

control both the supply of public funds and the means of determining their disbursal.

Kleptocratic elite typically treat their country's

treasury as though it were their

own personal bank account, spending the funds on

luxury goods as they see fit.

Many members of kleptocratic elite (especially financial elite) also secretly transfer public funds

into secret personal numbered

bank accounts in foreign countries in order to provide them with continued luxury if/when their

criminal behavior was exposed and they are forced to leave the country.

Kleptocracy is the political regime to which countries in which the governing ideology is neoliberalism

gravitate. Such incomes constitute a form of

economic rent and are therefore

easier to siphon off without causing the income itself to decrease (for example, due to

capital flight as investors

pull out to escape the high taxes levied by the kleptocrats).

Tax avoidance is just one manifestation of neoliberal kleprocracy

Unfortunately,

seniors often miss tax-saving opportunities that are available to them. Don't let that happen

to you!

For new retirees, it's more important than ever to take full advantage of every tax break

available. That's especially true if you're on a fixed income. After all, you have to stretch

out your retirement savings to cover the rest of your life. But holding on to your money during

retirement is easier said than done. That's why retirees really need to pay close attention to

their tax situation.

Unfortunately, though, seniors often miss valuable tax-saving opportunities . In many cases,

it's simply because they just don't know about them. Don't let that happen to you -- check out

these often-overlooked tax breaks for retirees . You could save a bundle!

When you turn 65, the IRS offers you a gift in the form of a larger standard

deduction . For example, a single 64-year-old taxpayer can claim a standard deduction of

$12,550 on his or her 2021 tax return (it was $12,400 for 2020 returns). But a single

65-year-old taxpayer will get a $14,250 standard deduction in 2021 ($14,050 in 2020).

The extra $1,700 will make it more likely that you'll take the standard deduction rather

than itemize. And, if you do claim the standard deduction, the additional amount will save you

over $400 if you're in the 24%

income tax bracket .

Couples in which one or both spouses are age 65 or older also get bigger standard deductions

than younger taxpayers. If only one spouse is 65 or older, the extra amount for 2021 is $1,350

– $2,700 if both spouses are 65 or older. Be sure to take advantage of your age!

For new retirees, it's more important than ever to take full advantage of every tax break

available. That's especially true if you're on a fixed income. After all, you have to stretch

out your retirement savings to cover the rest of your life. But holding on to your money during

retirement is easier said than done. That's why retirees really need to pay close attention to

their tax situation.

Unfortunately, though, seniors often miss valuable tax-saving opportunities . In many cases,

it's simply because they just don't know about them. Don't let that happen to you -- check out

these often-overlooked tax breaks for retirees . You could save a bundle!

When you turn 65, the IRS offers you a gift in the form of a larger standard

deduction . For example, a single 64-year-old taxpayer can claim a standard deduction of

$12,550 on his or her 2021 tax return (it was $12,400 for 2020 returns). But a single

65-year-old taxpayer will get a $14,250 standard deduction in 2021 ($14,050 in 2020).

The extra $1,700 will make it more likely that you'll take the standard deduction rather

than itemize. And, if you do claim the standard deduction, the additional amount will save you

over $400 if you're in the 24%

income tax bracket .

Couples in which one or both spouses are age 65 or older also get bigger standard deductions

than younger taxpayers. If only one spouse is 65 or older, the extra amount for 2021 is $1,350

– $2,700 if both spouses are 65 or older. Be sure to take advantage of your age!

The rules are clear: To qualify for tax-free profit from the sale of a home, the home must

be your principal residence and you must have owned and lived in it for at least two of the

five years leading up to the sale. But there is a way to capture tax-free profit from the sale

of a former vacation home.

Let's say you sell the family homestead and cash in on the break that makes up to $250,000

in profit tax-free ($500,000 if you're married and file jointly). You then move into a vacation

home you've owned for 25 years. As long as you make that house your principal residence for at

least two years, part of the profit on the sale will be tax-free.

Basically, the $250,000/$500,00 exclusion doesn't apply to any profit that is allocable to

the time after 2008 that a home is not used as your principal residence. For example, assume

you bought a vacation home in 2001, convert it to your principal residence in 2015 and sell it

in 2021. The post-2008 vacation-home use is seven of the 20 years you owned the property. So,

35% (7 ÷ 20) of the profit would be taxable at capital gains rates; the other 65% would

qualify for the $250,000/$500,000 exclusion.

The U.S. has won international backing for a

global minimum rate of tax as part of a wider overhaul of the rules for

taxing international companies , a major step toward securing a final agreement on a key

element of the Biden administration's domestic plans for revenue raising and spending.

Officials from 130 countries that met virtually agreed Thursday to the broad outlines of

what would be the most sweeping change in international taxation in a century. Among them were

all of the Group of 20 major economies, including China and India, which previously had

reservations about the proposed overhaul.

Those governments now will seek to pass laws ensuring that companies headquartered in their

countries pay

a minimum tax rate of at least 15% in each of the nations in which they operate, reducing

opportunities for

tax avoidance .

David Milliken and Kate Holton Sat, June 5, 2021, 4:01 AM

...Hundreds of billions of dollars could flow into the coffers of governments left

cash-strapped by the COVID-19 pandemic after the Group of Seven (G7) advanced economies agreed

to back a minimum global corporate tax rate of at least 15%.

Facebook said it expected it would have to pay more tax, in more countries, as a result of

the deal, which comes after eight years of talks that gained fresh impetus in recent months

after proposals from U.S. President Joe Biden's new administration.

"G7 finance ministers have reached a historic agreement to reform the global tax system to

make it fit for the global digital age," British finance minister Rishi Sunak said after

chairing a two-day meeting in London.

The meeting, hosted at an ornate 19th-century mansion near Buckingham Palace in central

London, was the first time finance ministers have met face-to-face since the start of the

pandemic.

U.S. Treasury Secretary Janet Yellen said the "significant, unprecedented commitment" would

end what she called a race to the bottom on global taxation. German finance minister Olaf Scholz said the deal was "bad news for tax havens around the

world". Yellen also saw the G7 meeting as marking a return to multilateralism under Biden and a

contrast to the approach of U.S. President Donald Trump, who alienated many U.S. allies. "What I've seen during my time at this G7 is deep collaboration and a desire to coordinate

and address a much broader range of global problems," she said.

Ministers also agreed to move towards making companies declare their environmental impact in

a more standard way so investors can decided more easily whether to fund them, a key goal for

Britain.

... ... ...

Key details remain to be negotiated over the coming months. Saturday's agreement says only

"the largest and most profitable multinational enterprises" would be affected.

... ... ...

The G7 includes the United States, Japan, Germany, Britain, France, Italy and

Canada.

Last Wednesday, Federal Reserve Chair Jerome Powell showed how simple questions do not

always get simple answers. When speaking to the media after the latest Federal Open Market

Committee ( FOMC ) meeting,

some difficult questions were asked. So much so, Powell had to repeat one question to himself,

asking:

When will the economy be able to stand on its own feet?

He immediately followed with:

I'm not sure what the exact nature of that question is.

FOX News correspondent Edward Lawrence elaborated, asking when the Fed would lower the

number of treasuries it buys, and when the economy would function "without having that support

from the monetary side."

Powell found ways to avoid answering the idea of a nation which stands without central bank

supports, but he did refer to various "tests" the Fed will do in order to make decisions like

shrinking the balance sheet, explaining:

we've articulated our test for that, as you know, and that is just we'll continue asset

purchases at this pace until we see substantial further progress.

He went on to say that prior to making any decisions, such as buying fewer treasuries, they

will give the public a lot of notice beforehand.

There was also a question related to the Fed's influence in the housing market:

the housing market is strong, prices are up. And yet, the Fed is buying $40 billion per

month in mortgage related assets. Why is that, and are those purchases playing a role at all

in pushing up prices?

Despite amassing nearly $2.2 trillion of mortgage-backed securities

(MBS), Powell defended the central bank on the grounds that:

I mean, we started buying MBS because the mortgage-backed security market was really

experiencing severe dysfunction, and we've sort of articulated, you know, what our exit path

is from that. It's not meant to provide direct assistance to the housing market.

To be clear, the "severe dysfunction" occurred over a decade ago, when the Fed entered the

MBS market. As for the public knowing the exit path or not providing assistance to the housing

market, both ideas are highly debatable, to say the least.

But even more puzzling is when Powell says that during the current COVID crisis:

We bought MBS, too. Again, not intention to send help to the housing market, which was

really not a problem this time at all.

Strange, the Fed would commit to buying $40 billion a month of MBS when, according to the

Chair, there were no problems in the market. He concludes that purchases will go to zero over

time, but the "time is not yet."

The final question asked was in regards to market intervention:

if you get out of the markets, there aren't enough buyers for all of the Treasury debt?

And so, rates would have to go way up. Bottom line question is what do we get for $120

billion a month that we couldn't get for less?

Powell never explained what exactly "we get for $120 billion" a month, but assured us the

Fed was looking to reach its goals, and this was part of its plan. However, he did comment on

purchases, saying:

But if we bought less, you know, no. I mean, I think the effect is proportional to the

amount we buy And we articulated the, you know, the test for withdrawing that accommodation.

And we think, you know. So, we're waiting to see those tests to be fulfilled, both for asset

purchases and for lift off of rates. And, you know, when the tests are fulfilled, we'll go

ahead as, you know, we've done this before.

Between various tests to determine policy, vague responses, and a general avoidance of

answering questions directly, not much was offered other than providing perpetual liquidity

injections under accommodative monetary conditions. It was refreshing to see the mainstream

media ask more questions about the plan ahead; we can only hope the mainstream economic

community will do the same.

Janet Yellen caused market ructions when she noted in public that: "It may be that interest

rates will have to rise somewhat to make sure that our economy doesn't overheat, even though

the additional spending is relatively small relative to the size of the economy."

Firstly, because rates aren't the Treasury Secretary's job to comment on - EVER. Yes, there

is the same need for endless hockey-stick-projection optimism on growth, the same silken spiel,

and the same one-size-fits-all Panglossian policy prescriptions (of various vintages: Slash

taxes! Raise taxes!) in both roles: but there is a separation of powers between the two.

Secondly, because that very same Panglossian policy from the Fed has got global markets to

the point where the mere idea of small increase in US rates is going to bring a whole lot of

precariously-levered objects tumbling down. It's a good job that interest rates never, ever,

ever have to go up again then, isn't?

Naturally, Yellen immediately had to walk back these comments when qualifying that rate

increases " are not something that I am predicting or recommending ." So just what was the

correct verb then? Speculating? Hypothesizing? Imagining? Dreaming? Deluding?

For now, markets can happily seize on all of the usual Fed-driven speculative hypotheticals

to imagine, dream, and delude themselves to greater wealth as usual . US couples everywhere can

keep fantasizing that they too can one day get a billionaire divorce. Yet it's not as if Yellen

doesn't have just *a little* bit of experience in this rate field thing. It's not as if she

might not end up thinking a certain way on autopilot in the new job, and saying the quiet part

out loud – is it?

Of course, the question of who is driving applies to the Fed itself . Yellen added: "If

anyone appreciates the independence of the Federal Reserve I think that person is me." Yet

unlike the BOE, for example, the Fed allows US banks a major role (if not "ownership") in its

12 regional Reserve Banks, alongside balancing presidential appointees. So it a fusion body,

and even if it is independent of the Treasury, that is hardly true of all influence: the reason

for having 12 regional Reserve Banks was originally to water down that of Wall Street. Yet how

is that working out, and where are the union/labour representatives, for example? That's a

structural issue the US press doesn't talk about much even as much of it obsesses about power

structures everywhere else; but, sadly, anti-Semitic conspiracy theorists more than compensate,

because that's their defined role.

Meanwhile, we all know the Powell Fed is still firmly in pedal-to-the-metal mode . Yellen

just agreed to stay in the back seat in that regard, even if her proposed fiscal policy is the

equivalent of winding down the window and sticking her head out of it, like a dog having a good

time, which should see any caring central bank driver reduce speed accordingly.

The question remains, however, as to exactly what is driving the massive surge in commodity

prices we are still seeing all round us? Headlines yesterday were that corn hit USD7 a bushel,

the highest since 2013. Today Bloomberg reports "Raw materials surging across tighter markets

and recovery; Consumer prices rising as manufacturers pass on higher costs." Once upon a time,

central banks used to do something when headlines like this were seen. So why no need to brake?

Because this is all transitory, as Powell and Yellen, at the second attempt, just

underlined.

But how so? Is it Covid-19 related? We already hear that semiconductor supply will be

pinched for years. Or perhaps it is all just happening "because markets", as seems to be the

general consensus? Or, just maybe, the Fed, and other major central banks, are also playing a

role via their pedal-to-the-metal liquidity? Another key driver is Wall Street realising

commodities are an inflation hedge too – even as that creates the inflation they are

trying to avoid. (Don't worry: they still get to eat. Others might not though.) Another is

China's voracious commodity appetite. (Don't worry: they still get to eat. Others might not

though.) One thing we can be sure of. Prices seem to be moving significantly higher, and not

just due to the expected base effects.

Ironically, the only way in which Powell --and Yellen-- can be sanguine about this is in the

knowledge that even if prices go up, US wages almost certainly won't. Yes, at the moment we are

anecdotally seeing US labour shortages as millions of previously low-paid workers prefer to

live off of their last stimulus cheque rather than report for the daily drudgery. But have you

heard any anecdotes of wages going up as a result – or rather of businesses closing down,

or automating? As has been repeated here many times, are the structures *really* being put in

place to support sustained higher wages? If not, it's just higher prices - and so lower real

wages.

I am not sure that the 12 regional Reserve Banks and those in DC are aware of what that will

feel like to Joe Public. More so if their logical response is to keep monetary stimulus high,

and so pushing real wages even lower. If mishandled, this could easily drive us off a cliff. As

such, who is really in the driver's seat?

3 play_arrow

Cloud9.5 3 hours ago (Edited)

Who is running the show? The front is the CIA. Who is behind it? A collection of

oligarchs.

Brill 3 hours ago

No mention of Rothschild?

No mention of Rockefeller?

Joe Bribem 2 hours ago

The biggest cockroaches are never mentioned.

Lordflin 3 hours ago remove link

Geopolitics are in the driver's seat...

The economy is along for the ride...

radical-extremist 2 hours ago

If Antifa had any brains (which they don't), they'd be marching and rioting against the

CIA and the Fed - not the Proud Boys, ICE and local police stations. They're fighting to tear

down the SYSTEM, and they don't even know what or where the SYSTEM really is.

PAsucks 2 hours ago

"I am not sure that the 12 regional Reserve Banks and those in DC are aware of what that

will feel like to Joe Public." It's called a lack of empathy, an important trait of

sociopaths. Federal Reserve is an arm of .gov - a criminal organization.

Apollo Capricornus Maximus 2 hours ago

The unelected Council of Foreign Relations kleptocratic oligarchy is in charge of the

kinetic and psychological manipulation of Western finances and zeitgeist. The Federal

Reserve, CIA, National Security state, MSM, Congress all report and obey this criminal cabal

of whom every member should be hung by the American people.

Last Wednesday, Federal Reserve Chair Jerome Powell showed how simple questions do not

always get simple answers. When speaking to the media after the latest Federal Open Market

Committee ( FOMC ) meeting,

some difficult questions were asked. So much so, Powell had to repeat one question to himself,

asking:

When will the economy be able to stand on its own feet?

He immediately followed with:

I'm not sure what the exact nature of that question is.

FOX News correspondent Edward Lawrence elaborated, asking when the Fed would lower the

number of treasuries it buys, and when the economy would function "without having that support

from the monetary side."

Powell found ways to avoid answering the idea of a nation which stands without central bank

supports, but he did refer to various "tests" the Fed will do in order to make decisions like

shrinking the balance sheet, explaining:

we've articulated our test for that, as you know, and that is just we'll continue asset

purchases at this pace until we see substantial further progress.

He went on to say that prior to making any decisions, such as buying fewer treasuries, they

will give the public a lot of notice beforehand.

There was also a question related to the Fed's influence in the housing market:

the housing market is strong, prices are up. And yet, the Fed is buying $40 billion per

month in mortgage related assets. Why is that, and are those purchases playing a role at all

in pushing up prices?

Despite amassing nearly $2.2 trillion of mortgage-backed securities

(MBS), Powell defended the central bank on the grounds that:

I mean, we started buying MBS because the mortgage-backed security market was really

experiencing severe dysfunction, and we've sort of articulated, you know, what our exit path

is from that. It's not meant to provide direct assistance to the housing market.

To be clear, the "severe dysfunction" occurred over a decade ago, when the Fed entered the

MBS market. As for the public knowing the exit path or not providing assistance to the housing

market, both ideas are highly debatable, to say the least.

But even more puzzling is when Powell says that during the current COVID crisis:

We bought MBS, too. Again, not intention to send help to the housing market, which was

really not a problem this time at all.

Strange, the Fed would commit to buying $40 billion a month of MBS when, according to the

Chair, there were no problems in the market. He concludes that purchases will go to zero over

time, but the "time is not yet."

The final question asked was in regards to market intervention:

if you get out of the markets, there aren't enough buyers for all of the Treasury debt?

And so, rates would have to go way up. Bottom line question is what do we get for $120

billion a month that we couldn't get for less?

Powell never explained what exactly "we get for $120 billion" a month, but assured us the

Fed was looking to reach its goals, and this was part of its plan. However, he did comment on

purchases, saying:

But if we bought less, you know, no. I mean, I think the effect is proportional to the

amount we buy And we articulated the, you know, the test for withdrawing that accommodation.

And we think, you know. So, we're waiting to see those tests to be fulfilled, both for asset

purchases and for lift off of rates. And, you know, when the tests are fulfilled, we'll go

ahead as, you know, we've done this before.

Between various tests to determine policy, vague responses, and a general avoidance of

answering questions directly, not much was offered other than providing perpetual liquidity

injections under accommodative monetary conditions. It was refreshing to see the mainstream

media ask more questions about the plan ahead; we can only hope the mainstream economic

community will do the same.

ReadyForHillary 1 hour ago

When will the economy be able to stand on its own feet?

He immediately followed with:

I'm not sure what the exact nature of that question is.

HA HA HA HA!

HA HA HA HA HA HA HA HA!

CovidBannedTard 1 hour ago

C'mon man!!!

Lordflin 1 hour ago

The entire point to the Fed is to fail to answer tough questions...

no cents at all 1 hour ago

Or doublespeak. The fed probably has a talented linguistics department at their employ

Paul Bunyan 1 hour ago (Edited)

What they have always said is moronic. Yet the world is full of morons, so the people

can't see through the lies.

Miniminer1 1 hour ago

Not a confidence builder

SDShack 1 hour ago (Edited)

Good god, how many 'you know' responses did Powell have? Sounds like some brain dead

zoomer...'it's like, you know, complicated, and like, you know, we are working on it.' A

complete 'Emperor has no clothes' moment. And these are supposed to be the smartest people on

the planet. Clueless or just evil liars. Or both.

mtl4 53 minutes ago

I'll take both for $1000 Alex

Ajax_USB_Port_Repair_Service_ 1 hour ago

The Fed intervenes everyday, all day, because they have to. There is no market without the

Fed.

CovidBannedTard 1 hour ago

You know!!!....The Thing!!!

C'mon Man!!

Paul Bunyan 1 hour ago (Edited)

The game is almost over. The dollar has 1-2 years left before a complete monetary reset.

Make sure you get out soon. You won't want to make last minute decisions.

JOHNLGALT. 1 hour ago

My last minute decision is:

1). Do I buy Ounces?

2). Do I buy Kilograms?

🦍🦍🚀🚀🚀😂🤣😎.

Emmet Fitz-Hume 1 hour ago

Powell, Greenspan, et al are just word-salad machines

Why should seniors and retirees be sacrificed with ZIRP in order to advance the interests

of the US Treasury and Corporate borrowers?

I would call it elder abuse. He should be required to address this question. Let's have

the Press do their job

Ben A Drill 41 minutes ago

Why should anyone gamble with their hard earned money to keep up with inflation?

AhabQuixote 50 minutes ago

This is a ponzi scheme in plain sight. It is as if Bernie Madoff told his clients that his

firm is a scam but a scam is the only way the system can function. It will all be fixed at

some point in the future when pigs fly.

nuerocaster 29 minutes ago

You may think that the Mises Institute and Rabo Bank are idiots. But think how hard it is

to present all this as managerial error and make stupendous wealth transference and money

laundering sound like oopsie.

archipusz 1 hour ago

Why even ask.

They are going to print. Congress wants them to print. All the elite benefit from the

printing.

It is not going to stop.

JOHNLGALT. 1 hour ago

WE will stop them!!

We are a community that loves Silver, Period. 72.4k. Silverbacks. 2.2k. Online now Created

29 Jan 2021.

Go SILVERBACKS 🦍🦍🦍🦍.

This is a movement to bring the

🐍🐍🐍BANK$TER$🐍🐍🐍DOWN.

Biden the moron dictator doesn't like to answer questions either

ChromeRobot 47 minutes ago

Basically, if you haven't figured it after 108 years, these clowns don't have the

slightest clue what they're doing or worse....do.

Revolution_starts_now 1 hour ago

Do you prefer GITMO or SuperMax?

Ajax_USB_Port_Repair_Service_ 17 minutes ago

I'll take GITMO. Nonsmoking, non-vaccinated, section please.

CrabbyR 1 hour ago (Edited)

Politicians and banker's first language is bafflegab

Misesmissesme 1 hour ago (Edited)

Answers? We ain't got no answers! We don't need no answers! I don't have to give you any

steenking answers!

Backhandslicer 23 minutes ago

Life support? They have created a monster and the monster is ravaging the country side

Backhandslicer 25 minutes ago

Powell is thinking I'm a currency printing machine and all the chicks dig me I shouldn't

have to answer any questions

Backhandslicer 35 minutes ago

Powell sounds like the absent minded janitor

Backhandslicer 36 minutes ago (Edited)

Eliminate the central bank and use only metals as money with paper currency withdrawable

for any of the metals at any bank or credit union

CosmoJoe 35 minutes ago

Seriously? I haven't carried cash in years. I don't want to. I don't want to carry a bunch

of gold and silver around in a little money sack. It isn't the f&cking middle ages.

zorrosgato 31 minutes ago

A paper currency backed by gold would work fine enough.

MASTER OF UNIVERSE 18 minutes ago

Would cement bricks painted gold work well enough if we never allowed anybody to test gold

samples to verify authenticity?

That's what Fort Knox is, right?

MOU

Backhandslicer 26 minutes ago

Does a 100 dollar bill in your pocket give you a rash?

CosmoJoe 19 minutes ago

I wouldn't know, I don't carry $100 in my pocket.

permanent victim 55 minutes ago

The fed will be all powerful till the world abandons the dollar. Until then they will

print shamelessly

Ben A Drill 48 minutes ago

Understand the free masons and you will see how much evil is in the world.

Realism 1 hour ago

The list of paid liars keeps growing

VWAndy 1 hour ago

Why shouldnt they be hung from lamp posts is a valid question too.

Rainman 1 hour ago

By now we all know the bankster-owned Fed and the US Treasury are one and the same

entity.

Old Hickory twitches in his grave...

dlfield 1 hour ago

A: Why never, because then I would be out of a job.

sarret PREMIUM 1 hour ago

Here's a difficult question Powell. Do you identify more with a disabled penguin or a gay

orangutan? Get it wrong and you will be cancelled ya numpty.

JohnnyCrypto 19 seconds ago

Yeah, MadeofTheta was right!

It's over!

ClamJammer 2 minutes ago

Learned everything he knew about not answering questions from Pompeo........we lie, we

steal, we cheat.........

permanent victim 10 minutes ago

As long as the markets are up I am doing what I am getting paid to do

cowdiddly 14 minutes ago

Ummm....errrr... Questions? We don't need no stinking questions.

IDESofMARCH 16 minutes ago remove link

FED policy picks and chooses which busines fails and which makes all the money.

FED kills Ma and Pa Bus DEAD, Wall Mart, HD, Chain Restaurants and Dollar Stores all

having a good time raising prices.

Most tax havens are either American possessions or British possessions. Then there are the

tax havens that are firmly under American geopolitical control (Switzerland, Monaco,

Luxembourg, Ireland). Then there is the State of Delaware (of which the present POTUS is from).

There are no tax havens under the control of an enemy of the West.

The USA should stop with that charade. If it wanted to curb on tax evasion, it would've

already done so decades ago.

Capitalism is value that self-valorises. The rich must get richer and the poor must get

poorer over the long term. That's how a healthy capitalist system operates. To try to claim USD

1.4 trillion from their bourgeoisie is not how the American Empire should work. This is a

desperate attempt of the American Federal State to survive.

"... Instead of reining in the "globalist elites" he so vociferously ran against or those corporations "who have no loyalty to America," his one legislative achievement has been to award them a massive tax cut. Through it, he has maintained their favorite mix of low revenue intake and high deficits which gives Republicans a pretext to "starve the beast" and induce fiscal anorexia. ..."

"... Trump ran as a populist firebrand -- a fusion of Huey Long and Ross Perot -- and while he never abandoned that style, he has governed for the most part as a milquetoast free market Republican in perfect tandem with Paul Ryan and Mitch McConnell, one whose solution to everything is more tax cuts and deregulation: a kind of turbo-charged "high-energy Jeb." ..."

"... With the outbreak of COVID-19, many on the reformist right are hoping for the emergence of the President Trump they thought they were promised, a leader just as ready to break out of the donor-enforced "small government" straitjacket while in power as he was during the campaign. ..."

"... The heightened rhetoric against China will continue -- the one thing Trump is good at -- but it is unlikely to be matched with the required policy ..."

"... If neoliberalism excused inequality at home by extolling the equalization of incomes across the globe (millions of Chinese raised from poverty, while millions of American workers fall back into it!), the new position must shift emphasis back to ensuring a more equitable domestic distribution of wealth and opportunity across all classes and communities in this country. ..."

"... It is worth pondering what might have happened if the administration had gone the other way and followed the last piece of policy advice given by Steve Bannon before his ouster in August 2017. Bannon suggested raising the top marginal income tax rate to 44 percent while "arguing that it would actually hit left-wing millionaires in Silicon Valley, on Wall Street, and in Hollywood." ..."

"... It might well have put Trump on the path to becoming what Daniel Patrick Moynihan once proposed as a model for Richard Nixon when he gifted the 37th president a biography of Disraeli, namely a Tory Republican who could outsmart the left by crafting broad popular coalitions based on a blending of patriotic cultural conservatism with class-conscious economic and social policy. ..."

"... Then and even more so now, the idea resonates: a Reuters/Ipsos poll from January found that 64 percent of Americans support a wealth tax, a majority of Republicans included. Poll after poll has reaffirmed this. It seems as if there is right-wing populist support for taxing the rich more. ..."

"... There is one more thing to be said about the significance of taxing the rich. Up until very recently, there has been a prevailing tendency among the reformist right (with some important exceptions) to couch criticism of the elites primarily or even exclusively in cultural terms. There seems to have been a polite hesitation at taking the cultural critique to its logical economic conclusions. It is easy to excoriate the excesses of elite identity politics, the "woke" part of woke capitalism; it's something all conservatives -- and indeed growing numbers of liberals and socialists -- agree on. Fish in a barrel. ..."

"... But to challenge the capitalism part, i.e. free market orthodoxy, not in a secondary or tertiary way, but head on and in specific policy terms as Lofgren and a few others have done, would involve confronting difficult truths, namely that the biggest beneficiaries of tax cuts and Reaganite economic policy in general, which most conservatives enthusiastically promoted for four decades, are the selfsame decadent coastal elites they claim to oppose. It is they who more than anyone else thrive on financialized globalization, arbitrage and offshoring. ..."

"... In other words, it amounts to an honest recognition of the complicity of conservatism in the mess we're in, which is perhaps a psychological bridge too far for too many on the right, reformist or not. (Trigger Warning!) This separation of culture and economics has led to the farce of a self-styled nationalist president lining the pockets of his nominal enemies, the globalist ruling class. ..."

"... A conservative call to tax the rich would signal that the right is ready to end this charade and chart a course toward a more patriotic, public-spirited and yes, proudly hyphenated capitalism. ..."

"... Michael Cuenco is a writer on politics and policy. He has also written for American Affairs. ..."

They also left worker wages stagnant and increased the deficit. Where is our more nationalist economic policy?

Much has been written about the disappointment of certain segments of the right in the apparent capitulation of Donald Trump to

the agenda of the conservative establishment.

Instead of reining in the "globalist elites" he so vociferously ran against or those corporations "who have no loyalty to America,"

his one legislative achievement has been to award them a massive tax cut. Through it, he has maintained their favorite mix of low

revenue intake and high deficits which gives Republicans a pretext to "starve the beast" and induce fiscal anorexia.

The president has granted them as well their ideal labor market through an ingenious formula: double down on mostly symbolic raids

(as opposed to systemic solutions like Mandatory E-Verify) and ramp up the rhetoric about "shithole countries" to distract the media,

but keep the supply of cheap, exploitable low-skill labor (legal and illegal) intact for the business lobby.

Trump ran as a populist firebrand -- a fusion of Huey Long and Ross Perot -- and while he never abandoned that style, he has governed

for the most part as a milquetoast free market Republican in perfect tandem with Paul Ryan and Mitch McConnell, one whose solution

to everything is more tax cuts and deregulation: a kind of turbo-charged "high-energy Jeb."

With the outbreak of COVID-19, many on the reformist right are hoping for the emergence of the President Trump they thought they

were promised, a leader just as ready to break out of the donor-enforced "small government" straitjacket while in power as he was

during the campaign.

Despite signs of progress, what's more likely is a return to business as usual. Already the GOP's impulse for austerity and parsimony

is proving to be stronger than any willingness to think and act outside the box.

The heightened rhetoric against China will continue -- the one thing Trump is good at -- but it is unlikely to be matched with

the required policy, such as a long-term plan to reshore U.S. industry (that doesn't just rely on blindly giving corporations the

benefit of the doubt). At this point, we already know where the president's priorities lie when given a choice between the advancement

of America's workers or continued labor arbitrage and carte blanche corporate handouts.

Lest they be engulfed by it like everyone else, the reformist right should ask: is there any way to stand athwart the supply-side

swamp yelling Stop?

Many of these conservatives lament the Trump tax cut not just because it was a disaster that failed to spark reinvestment, left

wages stagnant, needlessly blew up the deficit and served as a slush fund for stock buybacks, but more fundamentally because it betrayed

the overwhelming intellectual inertia and lack of imagination that characterizes conservative policymaking.

More than in any other issue then, a distinct position on taxes would make the new conservatism truly worth distinguishing from

the old: tax cuts were after all the defining policy dogma of the neoliberal Reagan era.

If neoliberalism excused inequality at home by extolling the equalization of incomes across the globe (millions of Chinese raised

from poverty, while millions of American workers fall back into it!), the new position must shift emphasis back to ensuring a more

equitable domestic distribution of wealth and opportunity across all classes and communities in this country.

A reformulation of fiscal policy along populist economic nationalist lines can help with that.

It is worth pondering what might have happened if the administration had gone the other way and followed the last piece of policy

advice given by Steve Bannon before his ouster in August 2017. Bannon suggested raising the top marginal income tax rate to 44 percent

while "arguing that it would actually hit left-wing millionaires in Silicon Valley, on Wall Street, and in Hollywood."

Such a move would have been nothing short of revolutionary: it would have been a faithful and full-blown expression of the populist

economic nationalism Trump ran on; it would have presented a genuine material threat to the elite ruling class of both parties, and

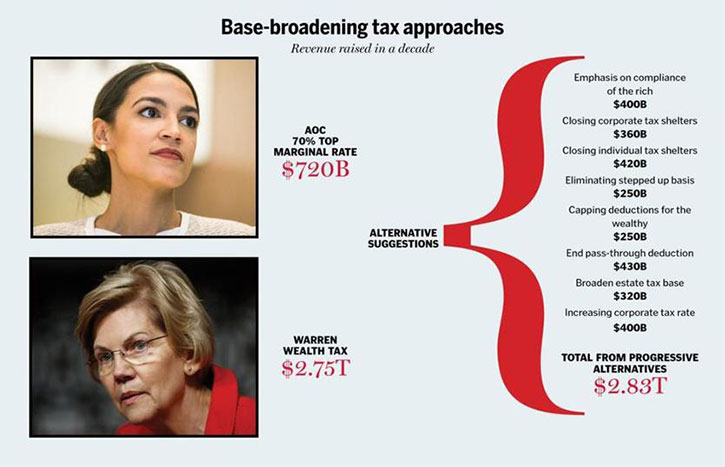

likely would have pre-empted the shock value of Alexandria Ocasio-Cortez proposing a 70 percent top marginal rate.

It might well have put Trump on the path to becoming what Daniel Patrick Moynihan once proposed as a model for Richard Nixon when

he gifted the 37th president a biography of Disraeli, namely a Tory Republican who could outsmart the left by crafting broad popular

coalitions based on a blending of patriotic cultural conservatism with class-conscious economic and social policy.

Not that Trump would have needed to go back to Nixon or Disraeli for instruction on the matter. In 1999, long before Elizabeth

Warren came along on the national scene, a presidential candidate eyeing the Reform Party nomination contemplated the imposition

of a 14.25 percent wealth tax on America's richest citizens in order to pay off the national debt: his name was Donald Trump.

What ever happened to that guy? The Trump of 1999 was onto something. Maybe this could be a way to deal with our post-pandemic

deficits.

Then and even more so now, the idea resonates: a Reuters/Ipsos poll from January found that 64 percent of Americans support a

wealth tax, a majority of Republicans included. Poll after poll has reaffirmed this. It seems as if there is right-wing populist

support for taxing the rich more.

To the common refrain, "the rich are just going to find ways to shelter their income or relocate it offshore," I have written

elsewhere about the concrete policy measures countries can and have taken to clip the wings of mobile global capital and prevent

such an outcome.

I have written as well about how taxing the rich and tightening the screws on tax enforcement have implications that go beyond

the merely redistributive approach to fiscal policy conventionally favored by the left; about how it can be a form of leverage against

an unaccountable investor class used to shopping at home and abroad for the most opaque assets in which to hoard vast amounts of

essentially idle capital.

A deft administration would use aggressive fiscal policy as an inducement for this irresponsible class to make things right by

reinvesting in such priorities as the wages and well-being of workers, the vitality of communities, the strength of strategic industries

and the productivity of the real economy – or else Uncle Sam will tax their wealth and do it for them.

It would also be an assertion of national sovereignty against globalization's command for countries to stay "competitive" by immiserating

their citizens with ever-lower taxes on capital holders and ever more loose and "flexible" labor markets in a never-ending race to

the bottom.

Mike Lofgren has penned a marvelous essay in these pages about the virtual secession of the rich from the American nation, "with

their prehensile greed, their asocial cultural values, and their absence of civic responsibility."

What better way to remind them that they are still citizens of a country and members of a society -- and not just floating streams

of deracinated capital -- than by making them perform that most basic of civic duties, paying one's fair share and contributing to

the commonweal? America need not revert to the 70-90 percent top marginal rates of the bolshevik administrations of Truman, Eisenhower

or Kennedy, but proposals for modest moves in that direction would be welcome.

There is one more thing to be said about the significance of taxing the rich. Up until very recently, there has been a prevailing

tendency among the reformist right (with some important exceptions) to couch criticism of the elites primarily or even exclusively

in cultural terms. There seems to have been a polite hesitation at taking the cultural critique to its logical economic conclusions.

It is easy to excoriate the excesses of elite identity politics, the "woke" part of woke capitalism; it's something all conservatives

-- and indeed growing numbers of liberals and socialists -- agree on. Fish in a barrel.

But to challenge the capitalism part, i.e. free market orthodoxy, not in a secondary or tertiary way, but head on and in specific

policy terms as Lofgren and a few others have done, would involve confronting difficult truths, namely that the biggest beneficiaries

of tax cuts and Reaganite economic policy in general, which most conservatives enthusiastically promoted for four decades, are the

selfsame decadent coastal elites they claim to oppose. It is they who more than anyone else thrive on financialized globalization,

arbitrage and offshoring.

In other words, it amounts to an honest recognition of the complicity of conservatism in the mess we're in, which is perhaps

a psychological bridge too far for too many on the right, reformist or not. (Trigger Warning!) This separation of culture and economics

has led to the farce of a self-styled nationalist president lining the pockets of his nominal enemies, the globalist ruling class.

Already, the White House is proposing yet another gigantic corporate tax cut. Using the exact same discredited logic as the last

one, senior economic advisor Larry Kudlow wants Americans to trust him when he says that halving the already lowered 2017 rate to

10.5 percent will encourage these eminently reasonable multinationals to reinvest. There he goes again.

A conservative call to tax the rich would signal that the right is ready to end this charade and chart a course toward a more

patriotic, public-spirited and yes, proudly hyphenated capitalism.

Michael Cuenco is a writer on politics and policy. He has also written for American Affairs.

"America need not revert to the 70-90 percent top marginal rates of the bolshevik administrations of Truman, Eisenhower or Kennedy,

but proposals for modest moves in that direction would be welcome."

Those tax rates were offset by direct investment in the US economy. So if I invested in the stock market, I'd get a 90% tax

rate because that doesn't produce actual wealth. On the other hand, if I invested in building factories that created thousands

of jobs for American citizens, my tax rate may fall to 0%. And those policies created a fantastic economy that we oldsters remember

as the golden age. That wasn't bolshevism, it was competitive capitalism. What we have today is libertarianism. And as long as

conservatives are going to let the libertarian boogey-man's nose under the tent, we are going to have this ugly, bifurcated economy.

Your choice. Man up.

You ever tell hear of sarcasm, bud? I think that's what the author was going for. Don't think he was trying to say that Ike and

Truman were Bolsheviks but was rather making fun of libertarians who hyperbolically associate high tax rates with socialism and

Soviet Communism...

We absolutely do not have libertarianism operating in this country today. There is simply no evidence that there is any

sort of libertarian economic or political system in place. Oh sure, you'll whine "but globalism without actually defining

what globalism is, or what is wrong about precisely, but just that it's somehow wrong and that libertarians are to blame for it.

There's a good word for such an argument: bullshit.

We have an economy that is extraordinarily dominated by the state via mandates, regulations, and monetary interference that is

most decidedly not libertarian in any way whatsoever. The current system though does create and perpetuate a system of

rent-seeking cronies who conform rather nicely to the descriptions of said actors by Buchanan and Tullock. The problems of the

modern economy are the result of state interference, not its absence, and Cuenco's sorry policy prescriptions do nothing to minimize

the state but instead just create a different set of rent-seeking cronies for which the wealth and incomes of the nation are to

be expropriated.

If you can point to how the current situation is in any way "libertarian" without creating your own perfect little lazy straw

man definition then by all means do so. Until then your retort is without

substance (you see a no true Scotsman reply doesn't work if the facts are in the favor of the person supposedly making such an

argument. Here you fail to establish why what I said is such a case; saying it doesn't make it so). When Kent makes some throwaway

comment that we're somehow living in some sort of libertarian era he's full of it, you know it, and all you can do is provide

some weak "no true Scotsman" defense? Come on and man up, stop appealing to artificial complaints of fallacious argumentation,

and give me an actual solid argument with evidence beyond "this is so libertarian" that we're living in some libertarian golden

age that's driving the oppression of the masses.

Busted unions, contracting out and privatization, deregulation of vast swaths of the economy since the late 1970's (Jimmy Carter

has gotten kudos from libertarian writers for his de-regulatory efforts), lowered tax rates, especially on financial speculation

and concentrated wealth, a blind eye or shrugged shoulder to anti-trust law and corporate consolidation. Yeah, nothing to see

here, no partial victories for the libertarian wings of the ruling class or the GOP, at all. The Koch Brothers accomplished nothing,

absolutely nothing, since David was the Libertarian Party's nominee for Vice President in 1980; all that money gone to waste.

Sure.

So, now some sort of "partial victory" means we're living in some sort of libertarian era? And what exactly was so wonderful about

all the things you listed being perpetuated? So, union "busting" is terrible, but union corruption was a great part of our national

solidarity and should have been protected? Deregulation of vast swathes of the economy? You mean the elimination of government

controlled cartels in the form of trucking and airlines? You mean the sorts of things that have enabled the working class folks

you supposedly favor to travel to places that were previously out of reach for them and only accessible to the rich for their

vacations? Yes, that's truly terrible. Again, you're on the side of the little guy, right? Lowered taxes? Are you seriously going

to argue that the traditional conservative position has been for high tax rates? What are taxes placed upon? People and property.

What do conservatives want to protect? People and property. So... arguing for higher taxes or saying that low taxes are bad or

even especially, libertarian, is really going off the rails. That's just bad reasoning. And regarding financialization, those

weren't especially libertarian in their enacting, but rather flow directly out of the consequences of the modern Progressive implementation

of neo-Keynesian monetary and fiscal policy. Suffice it to say, I don't think you'll find too many arguments from libertarians

that the policies encouraging financialization were good or followed libertarian economic policy prescriptions. Moreover, they

led entirely to the repulsive "too big to fail" situation and if there's one thing that libertarians hold to is that there is

no such thing (or shouldn't be) as "too big to fail." The objection to anti-trust law is that it was regularly abused and actually

created government-protected firms that harmed consumers. If you think anti-trust laws are good things and should be supported

by conservatives then by all means encourage Joe Biden to have Elizabeth Warren as his vice-presidential running mate and go vote

Democrat this fall.

"The problems of the modern economy are the result of state interference, not its absence". That's because the "state interference"

is working as proxy for the interests of vulture capitalist.

What we have today is vulture capitalism as opposed to free enterprise capitalism.

Exactly. The existence of a vulture capitalist or crony capitalist economy, which we have in many sectors, is evidence that "libertarianism"

is nothing more than a convenient totem to invoke as a rationale for complaint against the outcomes of the existing crony capitalist

state of affairs. My contention is that Cuenco, et al are simply advocating for a replacement of the cronies and vultures.

A very similar article(but probably coming at it from a slightly different angle) wouldn't look out of place in a socialist publication.

The culture war really is a pointless waste of time that keeps working class people from working towards a common solution to

shared problems.

I used to think that conservatism was about protecting private property and not, like Cuenco, in coming up with ever more excuses

for expropriating it.

No, that's libertarianism (or more properly propertarianism). Conservatism is first and foremost about responsibility to God,

community, family and self. Property is only of value in its utility towards a means.

As I see it, here are examples of how "conservatives" have actually practiced their "responsibility to God, community, family

and self":

The genocide of Native Americans

The slavery and murder of blacks

Their opposition to child labor laws, to womens' suffrage, etc.

Their support of Jim Crow laws

Their opposition to ending slavery and opposition to desegregation

Opposition to Civil Liberties Laws

Willingness to block, or curtail, voting rights.

Hyping the "imminent threat" of an ever more powerful communist menace bearing

down on us from the late 40s to the "unanticipated" collapse of the

USSR in '91. All of which was little more than endless "threat inflation" used

by our defense industry-corporate kleptocrats to justify monstrous increases

in deficits that have been "invested" in our meddlesome, murderous militarism all around the world, with the torture and deaths

of millions from S. E. Asia, to Indonesia, to Latin America, to the Middle East, to Africa, etc.

Violations of privacy rights (conservative hero J. Edgar Hoover's illegal domestic surveillance and acts of domestic terrorism,

"justified" by

his loopy paranoia about commies on every corner and under every bed.)

Toppling of democracies to install totalitarian despots in Iran

("Ike" '53), Guatemala (Ike, again, '54), Chile (Nixon '73), Brazil (LBJ, '64) and many, many more countries.

Strong support of the Vietnam War, the wars in Laos and Cambodia, and the Iraq War, which, according to conservative W. Bush,

God had inspired.

The myriad "dirty wars" we've fought around the world, and not only in Latin America.

With a few, notable exceptions, conservatives have routinely been on the wrong side of these issues. For the most part, it

has been the left, particularly the "hard left," that has gotten it right.

So conservatism should be entirely about taking people's property "for the good of the country"? That the purpose of a country

is to loot the people? That the people exist for the government and not the government for the people? Seems Edmund Burke and

Russell Kirk would like to have a word with you Adm.

To quote Kirk as just one example of your fundamental error:

Seventh, conservatives are persuaded that freedom and property are closely linked . [Apparently, Adm. you dispute

Kirk's assertion and accuse him thereby of conflating libertarianism and conservatism. Yes, I know Kirk was a hater of the

idea of patriotism, but he was such a raging libertarian what else could he do?] Separate property from private possession,

and Leviathan becomes master of all. Upon the foundation of private property, great civilizations are built. The more widespread

is the possession of private property, the more stable and productive is a commonwealth. Economic levelling[this

is the outcome of Cuenco's policy prescriptions by the way] , conservatives maintain, is not economic progress. Getting

and spending are not the chief aims of human existence; but a sound economic basis for the person, the family, and the commonwealth

is much to be desired.

So, either "Mr. Conservative" Russell Kirk wasn't really a conservative but a man who horribly conflated libertarianism and

conservatism, or we can say that Kirk was a conservative and that he recognized the protection of private property as crucial

in minimizing the control and reach of the Leviathan state. If the latter holds, then maybe what we've established is that AdmBenson

isn't particularly conservative.

"The more widespread is the possession of private property, the more stable and productive is a commonwealth." This status quo

has produced precisely the opposite of this. Wealth, assets, capital has been captured by the elite. The pitchforks are coming.

See this CBO chart:

View Hide

Conservatives accept taxes as a part of citizenship. Since taxes can't be avoided, a conservative insists on democratic representation

and has a general desire to get maximum bang for their taxpayer buck.

Libertarians, on the other hand, see everything through the lens of an individual's property rights. Taxes and regulation are

infringements on those rights, so a libertarian is always at war with their own government. They're not interested in bang for

their taxpayer buck, they just want the government to go away. I can't fault people for believing this way, but I can point out

that it is severely faulty as the operating philosophy beyond anything but a small community.

As for me not being particularly conservative, ya got me. It really depends on time of day and the level of sunspot activity.

I should have put the /s on my reply, but your response did give me a good chuckle. Besides, for that finger pointing at you,

there were three more pointing back at me.

And somehow people continually fall for the Trickle Down economic theory. George HW Bush was correct when he called this VooDoo

economics. Fiscal irresponsibility at it's finest.

Nah people don't fall for it, republicans do. The rest of us know this stuff doesn't work. We didn't need an additional datapoint

to realize that. The Tax Cuts and Jobs act was the single most unpopular piece of legislation to ever pass since polling began.

It never had support outside of the Republican Party which is why it's never had majority support.

John Kenneth Galbraith called Trickle Down "economics", "Oats and Horse Economics". If you feed the horse a lot of oats, eventually

some be left on the road...

Mitch is fully owned by Trump as is every republican that holds office except Romney. Mitch can't go to the bathroom with out

asking Trumps permission.

Mitch is owned by corporations and he likes it that way. He basically says as much whenever campaign finance reform pops up and

he defends the status quo.

Yep. The guy who declared war on the Tea Party. The guy who changed his tune entirely about China when he married into the family

of a shipping magnate.

I'm eagerly awaiting a GOP plan for economic restructuring. I've been waiting for decade(s). Surely there is someone in the entire

body of think tanks, congressional staffers, and political class that can propose a genuine and comprehensive plan for how to

rebalance production, education, and technology for the better of ALL Americans. Surely...

I honestly wonder if Jack Kemp might have had a "Road to Damascus" conversion away from his pseudo-libertarian and supply side

economic convictions if he had lived through the decade after the Great Recession. Probably not, given his political and economic

activity up until his death.

Trump pushed the tax cut because it saves him at least $20 million each year in taxes, probably closer to $50 million. That's

the only reason he does anything, because he benefits personally.

Thank you very much for posting the link to the wonderful essay by Mike Lofgren. Written 8 years ago it feels even more actual

than then. I have bookmarked it for future reference.

Looking at the US it always comes to my mind the way Rome and then Byzantium fell: a total erosion of the tax-base the rich

refused to pay anything to the imperial coffers, and then some of the rich had land bigger than some modern countries... And then

the barbarians came...

Lofgren: "What I mean by secession is a withdrawal into enclaves, an internal immigration, whereby the rich disconnect themselves

from the civic life of the nation and from any concern about its well being except as a place to extract loot."

That was in 2012, but that was what struck me about my well-to-do classmates

when I transferred from Cal State Long Beach to Columbia University in 1977 . Suddenly I was among people who saw America,

American laws, and a shared sense of civic responsibility as quaint, bothersome, rather tangential to the project of promoting

oneself and/or one's special interest.

The only way that factories would come back is when Americans start buying made in America. We can't wait for ANY government to

bring those factories and jobs ( and technology) . Only people voting with their pocketbooks can do it.

Still waiting for the day the first American asks "What have WE done wrong?" Rather than just following in Trumps step

and playing the victim card every step of the way and wondering why nothing gets better.

Not

surprisingly for those of you who are members of the ABA Tax Section, there is a meeting of

that group next week in Florida when a thousand tax lawyers (give or take a few) will be

talking about everything from basis to wealth taxes; GILTI, BEAT, Dual BEIT, to EITC. Yours

truly will be on a panel of the Tax Policy and Simplification Committee, meeting Friday

morning, to discuss how the tax system should respond to the wealth gap. Joining me on the dais

will be Roger Royse (moderator and panelist), Rich Prisinzano from the Penn Wharton Budget

Model, and Dan Shaviro, Wayne Perry Professor of Taxation at NYU and a blogger at Start Making

Sense. We'll talk about the income and wealth gap data, including the different perspectives of

Saez & Zucman, serving as wealth tax advisers to Senator and Democratic presidential

candidate hopeful Elizabeth Warren; Penn Wharton Budget Model, applying a more standard budget

model to determine harms and benefits of the Warren Wealth Tax; and Cato INstitute. We'll also

discuss Sen. Ron Wyden's proposal for a mark-to-market system of capital gains taxation

(including a lookback charge of some kind for hard-to-value assets, Prof. (and former Cleary

partner) Edward Kleinbard's Dual Business Enterprise Income Tax proposal, and other means of

making the regular tax system more progressive such as rates, removing the capital gains

preference, and reinvigorating the estate tax that has been the object of a GOP murder squad

for the last 20-30 years at least.

Meanwhile, today in Florida there was a Tax Policy Lecture at the University of Florida on

Taxing Wealth, with Alan Viard, resident scholar at the American Enterprise Institute, David

Kamin, Professor at NYU School of Law, Janet Holtzblatt, Senior Fellow at the Tax Policy

Center, and William Gale, Arjay and Frances Fearing Miller Chair in Federal Economic Policy7 at

the Brookings Institution.

Last fall, the Tax Policy Center held a program on Taxing Wealth (w ebcast recording available at this

link ) with Mark Mazur, Ian Simmons, Janet Holtzblatt, Beth Kaufman, Greg Leiserson,

Victoria Perry, and Alan Viard. Sony Kassam from Bloomberg Tax served as moderator. The link

has a series of power point presentations from that meeting as well, for your edification.

Ian Simmons, for example, includes

the letter from billionaires dated June 24, 2019, asking that "[ t]he next dollar of new

tax revenue should come from the most financially fortunate, not from middle-income and

lower-income Americans ." Such a tax " enjoys the support of a majority of

Americans–Republicans, Independents, and Democrats ." It's not a new idea, since all

those millions of middle-income Americans who own their home " already pay a wealth tax each

year in the form of property taxes on their primary form of wealth–their home ." The

billionaires are asking " to pay a small wealth tax on the primary source of our wealth as

well "–such as Elizabeth Warren's proposal, which would tax " only 75,000 of the

wealthiest families in the country " (those with assets over $50 million) and would

generate an estimated $3 trillion over ten years to "f und smart investments in our future,

like clean energy innovation to mitigate climate change, universal child care, student loan

debt relief, infrastructure modernization, tax credits for low-income families, public health

solutions, and other vital needs ." All this is necessary because of the wealth gap: "

[t]he top 1/10 of 1% of households now have almost as much wealth as all Americans in the

bottom 90% ." The signatories support a wealth tax because:

it's a powerful tool for solving our climate crisis

it's an economic winner for America through increased public investments

it will make Americans healthier, addressing the difference in longevity (15 years)

between the richest and the poorest Americans

It's fair -- "[ t]axing extraordinary wealth should be a greater priority than taxing

hard work ."

It strengthens American freedom and democracy, since high levels of economic inequality

lead to political power and pluotocracy and higher levels of distrust in democratic

institutions

It is patriotic -- ' The richest 1/10 of the richest 1% should be proud to pay a bit

more of our fortune forward to America's future ."

Janet Holtzblatt discussed whether wealth should be taxed, with a set of powerful

powerpoint charts . As she notes, there are a number of reasons to think taxing the wealthy

is a good idea because it (slide 4) :

curbs the accumulation of power that comes with the accumulation of wealth–and, I

will add, this is power to get laws and regulations written in your favor, including tax

laws, as well as power that allows pollution, rent-seeking, on-demand schedules for workers

and other 'evils' that come with plutocracy

ensures that the wealth pay their fair share of taxes

finances new initiatives (child care, student debt relieve, climate change policies,

housing initiatives)

provides better data for research on wealth inequality

Those not supportive (or, as JH puts it, "less optimistic") suggest that (slides 5, 7)

even with a wealth tax, the rich remain the richest and the most powerful

incremental changes to current tax system would be more easily implemented

wealth taxes would have a negative impact on savings, investment, entrepreneurship

wealth taxes won't raise as much revenue as claimed

OECD countries with wealth taxes haven't been all that successful (in 1990 12 had them,

in 2018 only 3 still retained wealth taxes: Norway, Switzerland, and Spain)

There are lots of issues with wealth taxes: (slides 8-20)

on what assets

at what rate (tax burden will depend partly on rate of returns on investments

using what exemption threshold (liquidity constraints at lower thresholds; taxing middle

income instead of wealthy)

using what means to prevent tax avoidance (dependents' wealth with parents? include

assets in family-run foundations? restrictive limits for trusts? exit taxes?)

and tax evasion (enhance IRS enforcement, enhance penalties, enhance IRS access to third

party data–but the wealthy have resources to battle IRS claims)

assuming what actual amounts of tax revenues could be raised (" street fights over

revenue estimates among top public finance economists ") (Slide 15)

how much wealth is there? JH notes several 2016 estimates between 86.9 trillion and

101.2 trillion (slides 16-17) {Zucman says just under $115 trillion]

Fed Reserve Survey of Consumer Finance ( 3 year intervals; leaves out Forbes 400

and some pension wealth)

estate tax data (adjusted for mortality probabilities and population)

income tax data (capitalized using assumed rates of returns)

how is that wealth distributed between the top 0.1% and the rest? Bricker 2016 study

estimates range from about 15% to 22% (Slide 18)

how much wealth is hidden by "tax net misreporting rates"? IRS 2016 misreporting:

farms 71%; nonfarm proprietors 64%; CGs 27%; PS/SCorps/Estates/Trusts 16% (slide 19)

how much tax revenues? between 815 billion and 1.098 trillion between 2021-2030

(slide 22, Urban-Brookings TPC Microsimulation Model [ with lower thresholds and rates

than those proposed by Warren]

who pays? 40,000 tax units in the top 1% minus the top 0.1%; 127,000 tax units in the

top 0.1%,with those in the top 0.1% paying between 97% and 100% on the different options

considered

Greg Leiserson discussed the idea of mark-to-market taxation (an idea that Ron Wyden has

endorsed), in "

Taxing wealth by taxing investment income: An introduction to mark-to-market taxation "

(Sept 11, 2019). The key to MTM taxation is that a tax is assessed annually on investments,

whether or not they are sold or otherwise disposed of ('through a transaction that results in

"realization" for federal income tax purposes). The burden of such a tax falls predominantly on

the wealthy, since those are the primary owners of bonds, stocks, real estate empires, and

pass-through businesses that produce investment income, as well as the appreciation of those

assets that is taxed currently as a capital gain on disposition. Leiserson provides a chart

(below) showing the nominal investment income of US households and nonprofits including an

offset for inflation.

As he notes, much of this income is taxed at preferential capital gains rates, and much of

the income tax is deferred because capital gains and losses are generally taxed only when the

asset is sold. Deferral amounts to a reduction in taxes paid under time-value-of-money

principles. But yet another way in which owners of investment assets escape taxation is the

estate tax: appreciation in property in the estate (such as unrealized capital gains from stock

that has appreciated in value significantly over decades) is never taxed, since the heirs get a

step up in basis to market value, so that if the asset were then immediately sold, there would

be no gain remaining.

MTM taxation eliminates the deferral advantage. MTM taxation combined with elimination of

the preferential rate for capital gains would eliminate the preferential treatment of capital

gains that exists in current law. Leiserson notes the difficulties for a MTM system: which

assets are covered, rate of tax applied, and whether there are special rules for volatility.

Further, "[ i]f a comprehensive system of mark-to-market taxation is enacted, then there

would be no unrealized gains at death going forward, because gains will have been taxed on an

annual basis, including in the year the person dies " so long as the system applies over

some transition period to gains accrued prior to enactment. Otherwise, the system would have to

tax gains at death (repealing step-up in basis rule) or at any other disposition, including

gifts, to ensure fair and equal treatment. He suggests other measures–such as limiting

the home sales capital gain exclusion or requiring mandatory distributions of pension account

balances above a threshold, that would be reasonable in a MTM context.

One difficulty with MTM taxation is valuation of assets that are not regularly traded. Ron

Wyden's proposal suggests a lookback charge–an additional tax payment for assets not

subject to MTM taxation that is collected upon disposition to account for the deferral value

while still relying on realization as a trigger for taxation. Wyden and Leiserson suggest

different possible methods. One is to take the gain upon sale and allocate it ratably to each

year between purchase and sale, compute the tax on each year's income at the rate applicable in

that year, and then calculate interest on those unpaid taxes for the years til payment.

Unrealized gains would be deemed realized on death or gift and taxed accordingly.

Three key ideas here:

To protect lower and middle income taxpayers from the tax, there could be a lifetime gain

exemption threshold ($0.5 million, say) that has to be reached before the rules apply or an

asset value threshold ($2 million; $10 million, etc.). Under the latter, taxpayers would fall

into and out of the MTM regime as assets fluctuate. (The asset approach is suggested by

Wyden.)

The revenue raised is significant though it depends on the particular model. Leiserson

suggests MTM combined with elimination of the preferential rate on capital gains "could

easily raise $1 trillion over the next decade–and potentially much more ." He notes

that just eliminating the preferential CG rate gives a much lower estimate–that's

because of "t he ease of tax avoidance under current law such as the ready opportunity to

defer tax by not selling assets and potentially avoid tax entirely through step up in

basis–all while simply borrowing against these same assets to finance any spending

."

"The wealthiest 1 percent of families holds 31 percent of all wealth, and the wealthiest

10 percent holds 70 percent of all wealth." "The highest-income 1 percent of families

receives 75 percent of the benefit of the preferential rates for capital gains and dividends

under current law." The wealthiest 10% would bear the burden of MTM reforms.

Of course, while everybody is talking about taxes, some of that talk is the same old endless

market fundamentalist myth (Reaganomics) about how tax cuts are what make the economy grow and

will actually pay for themselves -- in spite of near 4 decades of evidence to the contrary,

where highest growth rates have generally been in times of higher tax rates, with some

consideration for stimulus impact of tax cuts after periods of recessions. See, e.g., NY Times

editorial, There's No Such Thing as a Free

Tax Cut (Jan 22, 2020).

The op-ed notes that Treasury Secretary Steven Mnuchin "r epeated the risible fantasy

that the Trump administration's 2017 tax cuts will bolster economic growth sufficiently for the

government to recoup the revenue it lost by lowering tax rates " [in the 2017 tax

legislation] even though 2 years in, the " budget deficit has topped $1 trillion ."

This is because, as most of us who haven't drunk the Laffer-curve tax cut kool-aid know and

the Times op-ed reiterates, " businesses responded to increased demand more than they did to

the lower tax rates ." Nonetheless, we should not be surprised that the Trump

Administration is talking about two "big ideas" for taxes if the man gets reelected: 1) cutting

Medicare and Social Security: see, e.g., Trump Opens Door to

Cuts to Medicare and Other Entitlement Programs , NY Times (Jan 22, 2020) and 2)

passing another tax cut bill: see

Steven Mnuchin Confirms Trump's New Tax Plan is Imminent , USNews (Jan 23, 2020). Those two

ideas go hand in hand.

T hough Trump doesn't dare state what he is really doing to his base, who he has deceived

with typical right-wing rhetoric into thinking that he is trying to rightsize the economy to

serve them when he instead engages in class warfare to stuff his own pockets, he is hip to hip

with Newt Gingrich's desire t o "starve the government" to create a huge deficit (we are up to

$1 trillion in our new "gilded age economy") that then provides cover for the wealthy to suck

in even more of the country's wealth by downsizing Medicare and Social Security, programs

essential for those who are not among the wealthy.

"At the end of the day, perhaps, the equity side of the U.S. external balance sheet should

be understood not by thinking of the U.S. as a giant and very successful private equity fund

that borrows to buy equity -- but rather as one giant corporate tax dodge for U.S. based

multinationals

If you think I am exaggerating, I would encourage you to take a look at the IRS data on the

location of U.S. corporate profits -- and the location of the taxes that American firms pay

abroad. U.S. firms are earning big profits in jurisdictions where they don't pay tax, and small

profits in jurisdictions where they do and in the process, reducing their U.S. tax bill as

well. That's real exorbitant privilege."

In China's history when the largest landowners, the wealthiest individuals connived or

bribed their way out of paying taxes and the burden shifted down the income scale, the result

sooner rather than later was an uprising that ended with a new dynasty.

Why is there always more money than is even asked for for the "defense budget", but social

security and medicare are budget problems?

This is a constant in Chinese history, even the French Revolution was set up by the

exclusive taxation of the poor and middle classes. Eviscerating one's sources of income while

weakening the overall economy including the general population does not make for a strong

state able to withstand an unanticipated emergency. Somehow people keep doing the same thing

over and over.