|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

| News | Kleptocracy | Credit Default Swaps | Control Fraud and Principal-agent problem | Corporatist Corruption: Systemic Fraud under Clinton-Bush-Obama Regime | Glass-Steagall repeal |

| Etc |

Nice illustration of criminal tricks used by private equity (from comment by jomellon to [Mar 30, 2009]The revival of American populism Will there be blood The Economist)

March 29, 2009The Problem that The Economist wants to talk about? Public Outrage a.k.a. Populism.

The other less important problem that a magazine called The Economist might want to address, but which it doesn't want to talk about: the economy is bust, and why.

Typical scenario for the last 18 years:

- January - Private Equity Investor (PEI) has 20 million. He uses it a security to borrow 200 mio from Bank1 to buy a company Widgets. Widgets is a solid manufacturing business with assets of land, factories, patents, a brand, good will and no debts.

- March - Widgets borrows 300 million from Bank2 – no problems, its a solid business – but here comes the bit where it all goes criminal, but not illegal... Widgets pays out 300 million to PEI its owner as a dividend, who repays 200 to Bank1. PEI now has 100 million cash, and has done nothing for it. Widgets however has to pay 20 million in interest per year. PEI now has 100 million.

- July - Widgets also sells its assets: land, patents and so on and leases them back for 30 million a year. The sales bring 200 million which Widgets also pays out to PEI its owner. PEI now has 300 million.

- August - Widgets Pension Fund is 'restructured' bringing a liquid 150 million onto the balance sheet. Widgets has liabilities to its pensioners with little to back them. 150 million is paid out to PEI as a special dividend., PEI now has 450 million.

- December - PEI sells the business to a pension fund, for 100 million, less than he paid as it has a lot of debt, but it is a good business. PEI now has 550

- Recap: Widgets now has 300 million debt causing 20 million a year in interest, plus 30 million in leasing payments. It has pension liabilities and the pension fund is almost worthless. PEI had 20 million at the start of the year and now has 550 million. But the business is still viable, as Widgets can meet its payments.

- 5 years later - Sadly hard times come. Turnover drops, prices drop, costs are cut, people lose their jobs, including engineers, managers, the shop floor and the sales team who did real work for years, created real value, invented the patents, built the brand. It doesn't help. The company has no stores of fat - it goes bust. The banks loans are sour. People lose their jobs, the pensioners cannot be paid.

This happens 100 times so the banks are bust too, but get bailed out by the taxpayer (that's those guys who lost their jobs and pensions at Widgets)

PEI lives happily in The Bahamas with the 550 million which he 'earned' in a fabulous year of 'value creation' made possible by the power of free and light touch regulated markets.

Sadly, due to the complexity of all this the bright chaps at The Economist can not quite see why this is a slightly problematic way to run an economy... Honi suit qui mal y pense.

And if you are wondering whether firms like hedge funds and private equity funds -- significant parts of the "shadow" banking system -- add real value to the economy, you might enjoy this article by Harlan Platt about private equity, The Private Equity Myth. Download Platt. The Private Equity Myth.

The juggernaut of Kohlberg Kravis Roberts & Co. began rolling in 1976 when Jerome Kohlberg and cousins Henry Kravis and George Roberts left Bear, Stearns with about $120,000 to spend. The three invented and dominated the leveraged buyout as they sought investors and borrowed money to acquire Fortune 500 companies in dizzying succession.

Time after time, the KKR men presented a tempting offer. The CEO could cash out his company's existing shareholders by agreeing to sell the company to a new group that would be headed by KKR, but would include a lot of room for existing management. The new ownership group would take on a lot of debt, but aim to pay it off quickly. If this buyout worked out as planned, the KKR men hinted, the new owners could earn five times their money over the next five years. Presented with such a choice in the frenzied takeover climate of the 1980s, manages and corporate directors again and again said yes… To top management a leveraged buyout was the most palatable way to ride out the merger-and-acquisition craze."

They put up very little money of their own funds, but their partnerships made out like bandits. Consider the case of Owens-Illinois: KKR pup up only 4.7 percent of the purchase price. The company's chairman earned $10 million within a few years, the takeover advisors got $60 million, Owens-Illinois was left "gaunt and scaled back," and about five years later, KKR took it public at $11 a share, more than twice what the KKR partnership had paid for it.

Discussing the $26.4 billion buyout of RJR Nabisco Inc., ``Anders goes beyond what has been previously published,'' Bianco wrote, with his convincing assertion that RJR's post-deal crises pushed KKR close to ruin. Leveraged buyouts in general Anders terms ``one of the most profoundly undemocratic ventures the United States had ever seen.'' Their only lasting impact, he says, was to shift wealth from the mass of corporate employees to a managerial elite allied with Wall Street.

"For the first fourteen years of KKR's existence, the buyout firm's hallmark could be expressed in one word: debt… As KKR grew evermore powerful, Kravis and Roberts derived their economic clout from a single fact: They could borrow more money, faster, than anyone else," according to the chronicler of this high-flying firm. KKR acquired $60 billion worth of companies in wildly different industries in the 1980s: Safeway Stores, Duracell, Motel 6, Stop & Shop, Avis, Tropicana, and Playtex. They made piles of money by deducting interest expenditures from their taxes, cutting costs in their new companies and riding a long-running bull market.

This behind-the-scene accounts shows the ambition, pride, envy and fear that characterized the debt mania largely engineered by KKR, a mania that put millions out of work and made a very few very rich.

|

|

Switchboard | ||||

| Latest | |||||

| Past week | |||||

| Past month | |||||

Vedant Desai , April 25, 2017 at 3:17 amApr 26, 2017 | www.nakedcapitalism.com

Art Eclectic , April 25, 2017 at 11:49 amThat's a new angle for evaluating Amazon : it's not that retailers are closing because Amazon is expanding . Rather its seems that Amazon is expanding Because retailers are closing. Bezos probably should thank PE firms for their destructive activities.

Vatch , April 25, 2017 at 12:46 pmExactly. The crappified shopping experience and lack of inventory came first. A miserable brick and mortar experience drove shoppers into the welcoming arms of Amazon because they just wanted to buy stuff and retail made it hard.

sgt_doom , April 25, 2017 at 2:01 pmlack of inventory

A couple of days ago, reader Heron pointed this out:

Whether it's called "slim inventory" or "JIT", it's a problem for shoppers.

AnotherTosser , April 25, 2017 at 6:18 pmIndeed!

I'm sure an old junk bond Wall Street dood like Bezos is already pals with 'em!

Great article, and should be enlightening for those not in the know.

Whether Josh Kosman's outstanding book, The Buyout of America , or Eileen Appelbaum's marvelous work, the PE swineherds have been dismantling the American (and other countries') economy for quite a few years now , and the kings of debt, led by Peter G. Peterson who spends his free time decrying debt (?!?!?!?), are the villains of our age!

cnchal , April 25, 2017 at 10:06 pmThe retail market, by and large, is hosed, especially if they've decided to get into bed with PE. Amazon might be filling out the areas left bare by the collapse, but Amazon itself has a major problem in the form of counterfeit inventory which is going to blow up in its face.

If you look at the comments on HN, more than a few people mention how they got something that was sold (sometimes by Amazon) as legit, but turned out to be fake – this stems from Amazon's practice of commingling inventory when you participate in their "fulfilled by" program. Considering their expansion into grocery and other food-type items, a counterfeit scandal is one they can ill afford.

If retail's currently fried, and you can't trust what you buy on Amazon, what's left? The correction is going to take a while, and will be deeply felt, I fear.

fajensen , April 26, 2017 at 10:53 am> If retail's currently fried, and you can't trust what you buy on Amazon, what's left?

Manufacturers cooperating or colluding to develop their own sales platform and cutting out Amazon and Wal Mart and selling direct to the customer.

Colonel Smithers , April 25, 2017 at 5:26 amI do believe that alibaba.com and dealextreme.com has cornered that market opportunity already.

These days you can buy an insurance for your shipment so if your package is nailed by customs they will send another one until one finally makes it. I buy components that way, one can buy hundreds-off components at the 2-5k price levels offered by f.ex. digikey.com. Exotic stuff too.

The reason to still use Digikey & co are mainly for traceability, assured quality, genuineness and convenient re-ordering but for personal use it doesn't matter so much.

Colonel Smithers , April 25, 2017 at 5:33 amThank you, Yves.

You won't be surprised to hear about this scam operating in the UK. It has been the case for about thirty years and forms part of the "financial engineering" that has replaced metal bashing in Blighty.

It's not just retail, but football (aka soccer) that has fallen victim. Many clubs were similarly divided between the operating company / team and the ground. Some still are, e.g. Chelsea and Stamford Bridge.

Around the turn of the century, a former footballer (ex West Ham and Manchester City and one of the mobile chicanes negotiated by Diego Maradona for his second goal against England at the World Cup in 1986) who had made a small fortune at the Lloyd's insurance market, approached my employer, HSBC, for a loan, if not a partnership, to take over Aston Villa, which operates from a big site in Birmingham (Villa Park). His plan was to split the football club from the ground / stadium and get the club to pay the landlord rent, develop the ground for residential and retail purposes, and get the club to share a stadium with another Birmingham / Midlands region club, e.g. Birmingham City, Wolverhampton Wanderers (Wolves) or Port Vale.

HSBC wisely declined. It was still just about a boring trade bank then, but was embarking on a spree under John Bond.

Not long after, Barclays (a future employer at the time) became adviser to Leeds United. I don't know if Leeds split between club and ground (Elland Road), but the club began leasing, not buying players, and securitising the income stream. After some success, including an appearance in Europe's top competition, Leeds fell apart and is languishing in the lower divisions (minor leagues).

Philip Augar, a former banker (Schroeders, NatWest etc.) and author (Reckless Capitalism, Decline Of Gentlemanly Capitalism etc.), dedicated one of his books to Leeds United, his childhood club, "one of the early victims of this madness".

The footballer I mentioned above is still active in the City, not so much at Lloyd's (opposite one of my two offices), but with financial engineering in sport. He was widely quoted in the FT a few weeks ago.

With regard to retail, the scam played a part in the collapse of a retail chain, British Home Stores. The former chairman and main shareholder, "Sir" Philip Green, split the retail operations from the stores. He / his Monaco company owns many of the (former) sites, including what was BHS HQ in Marylebone (just down the road from Baker Street station and Mme Tussaud).

Colonel Smithers , April 25, 2017 at 5:40 amI forgot to add that said player was still hawking the same "financial solutions" (snake oil) in the FT. The paper did not mention how the solutions had worked out. The thing is, in many cases, the solutions seem / are designed to fail, after some roaring success, and (or so) the insiders can profit from the wreckage ("disaster capitalism") as they are often creditors (e.g. the knight of the realm above) and can salvage what they consider to be the valuable bits.

allan , April 25, 2017 at 6:58 amJust one more thing to add, sorry, is that many UK retailers are under similar pressure. One hears in the City that one or two household names are nearing collapse.

One well known US Main Street store merged with a well known and similar UK High Street store a couple or so years ago. They are run / owned from Switzerland, I think, by an Italian, whose PE firm, again based off shore, is one of the biggest shareholders in the group. The Italian billionaire ran the UK firm before the merger. They are rumoured to be one, if not the, next domino.

Jim A. , April 25, 2017 at 8:06 amYet another unintended (?) consequence of QE ∞. The ZIRP simultaneously made pension funds and endowments desperate for returns and enabled PE firms to raise large amounts of money at low rates.

But on the bright side, QE saved us over the last 8 years from the horror of meaningful fiscal stimulus and infrastructure investment. So we should thank Drs. Bernanke and Yellen and their enablers for letting the market work its magic and protecting us from the dead hand of state intervention .

Grumpy Engineer , April 25, 2017 at 9:58 amAnd the great recession meant that there were plenty of stressed business which PE funds could gain controlling interests in for relatively low cost.

HBE , April 25, 2017 at 8:14 amZIRP also made it easier to load all of these retailers up with excess debt. Management could borrow more money than necessary, pay themselves lavish bonuses with the excess, and claim that " interest rates are low; making payments will be easy ". They could even show you the math.

Of course, that math assumed that sales would steadily climb into the future. If sales fell even slightly, the payments became an oversized burden. And paying off the enormous loan principal was beyond all hope.

Companies with little debt can generally survive a reduction in sales. They can engage in cost-cutting exercises, maybe encourage some employees to retire earlier, etc. It's even easier if they own their own property and don't have to renegotiate a lease. But when you've got a lot of debt and servicing that debt requires that sales continue to rise quarter after quarter after quarter without fail, then things get a LOT more fragile. The effects of even a single bad quarter get greatly amplified. ["Leverage" can work both ways.] And steadily-declining sales are the kiss of death.

Oh, yes. Ultra-low interest rates "helped" retailers a lot. Helped set them up for failure, that is.

RUKidding , April 25, 2017 at 8:48 amMost retail jobs are already part time and now 2017-18 looks to be the death of retail altogether. Which sector is absorbing these legions of workers?

It's certainly not manufacturing and I'm fairly certain 60,000 new Uber drivers didn't hit the streets.

justanotherprogressive , April 25, 2017 at 9:39 amI dunno but seems like every time I turn around I discover someone else I know who's driving for Uber and/or Lyft. All age groups. All struggling to survive.

The demise of retail is especially chilling as it used to be a sort of fall-back job. Not no more.

Where's all the zillions of jawbs Trump is going to magically provide??

RUKidding , April 25, 2017 at 10:17 amI see that Trump today is claiming he's created 500,000 new jobs in his first 100 days, but he doesn't say what these jobs are or where these jobs are – obviously they aren't in my state

MyLessThanPrimeBeef , April 25, 2017 at 2:35 pmMaybe Trump's claiming responsibility for creating 500,000 new Uber and Lyft jawbs?

Guess a huge component of Boeing workers are about to become Uber drivers in Seattle in May. Woo hoo!

Thanks, Trump!

sgt_doom , April 25, 2017 at 2:04 pmTechnology is doing its best to hide the misery of the 99% temporarily.

"Take out a loan and get a car. Defer maintenance. Get cash flow now!"

"Get more cash flow renting out your bathroom and living room."

Ed , April 25, 2017 at 10:10 am" Which sector is absorbing these legions of workers?"

That's a good one (LFMAO)!

McWatt , April 25, 2017 at 10:36 amI know some firm bought Friendlys the ice cream/restaurant took the ice cream in a box business and split it off then left the restaurant part to die. It was American businesses best friend Sun Capital.

FedUpPleb , April 25, 2017 at 10:47 amInterestingly, it seems to me, that the off shoring of clothing manufacturing to China, and the subsequent fall in inventory cost to retailers and the incredible margins they operate on hasn't done anyone any good in the end.

sgt_doom , April 25, 2017 at 2:05 pmI have found retail shopping over the last ten years to be a poor now bordering on depressing experience. Poor selection, sparse stores, uncompetitive prices,staff either untrained or trained only to nag about loyalty cards, and the quality of items has nosedived across the board. Even the "luxury" items are cheap and poorly made. The only consistent exception to this trend is toy stores. I guess kids are tougher customers.

I hate shopping online. I hate the uncertainty. I hate the delay. I hate the decision fatigue. But what choice do I even have anymore? It costs me more petrol to go shopping than they charge for delivery.

Sutter Cane , April 25, 2017 at 12:28 pmThanks, FedUpPleb - I keep telling this to the stooges who keep prattling on about the low cost of items - which are far too expensive, last only several washings (delicate cycle only, of course) or several months and are of the poorest quality, completely different from my youth!

MyLessThanPrimeBeef , April 25, 2017 at 2:42 pmGiven the post and the comments, it actually sounds like the future for retailers that survive doesn't seem so bleak, IF (big if):

1. They manage to avoid private equity takeover

2. Don't take on debt

3. Make customer service a priority

4. Sell quality goods a step above the usual Chinese garbage found everywhere else (or at least that can't be shipped as easily)

4. Keep their stores updated and pleasant to visitWhat with all of the closures, there might be opportunities for the retailers that survive if they avoid the mistakes of their fallen competitors. But are there any examples of companies out there that are doing these things? Nordstrom? Costco? Anybody?

Ancient 1 , April 25, 2017 at 12:52 pmThere retailers are national chain retailers.

Before them, there were mom-and-pop retailers. They had bleak-future-moment a long, long time ago.

Perhaps they will come back one day, when people make enough money to value service again, instead of supporting 'trade' as a WSJ poll shows, because trade means affordable junk commensurate with stagnant or declining real wages.

anonymous , April 25, 2017 at 1:00 pmYou can blame the present situation that Neiman Marcus is dealing with on it managers, especially Ms. Katz, who were paid a lot of money in the sell out to PE. These people have destroyed an old Dallas brand with their greed and mismanagement. A brand that has a history of innovation and customer service driven by Stanley Marcus. A real loss for Dallas and for retail history,

Dave , April 25, 2017 at 10:15 pmI stopped buying clothes at brick and mortar stores starting around a decade ago because of crapification. If you need tall sizes for shirts, you used to be able to get these at most every department store, but over the last decade or two almost every department store around these parts was sold and restructured; after these changes the stores always have less inventory for higher prices. Now the only place you can find a wide selection of tall sizes is the internet.

Retail clothiers have essentially said we're not interested in selling things to tall men. And they're not interested in selling things to large men, or large women, or short people, or old people.

How badly should I feel about the disappearance of an industry that decided they had no interest in me whatsoever?

Susan the other , April 25, 2017 at 1:26 pmAsians, Hispanics and teenagers are a more important market to them than tall white and black men.

Synoia , April 25, 2017 at 1:49 pmJust curious. First they killed off family farms; then mom and pop stores; then they wiped out mainstreet; now they are busy demolishing brick and mortar malls. What comes next? It looks like PE might be killing itself.

Paul Greenwood , April 26, 2017 at 1:42 amIn destroying malls they are also distroying a class of investor who wanted the income based on that capital.

Many of the 10% are heavily invested in mall real estate,

Lambert Strether , April 26, 2017 at 2:02 amParasites destroy hosts

allan , April 25, 2017 at 2:20 pmNot all of them. Looks like ours might, though.

Yves Smith Post author , April 25, 2017 at 2:22 pmApril 25 – Guitar Center :

Guitar Center's latest jam: Future threatened by its huge debt burden [Marketwatch]Is the big leveraged buyout wave of 2005-2007 about to claim another victim?

Bonds issued by Guitar Center, the biggest retailer of musical instruments in the world, are languishing at record lows on growing concern that the company is going to be overwhelmed by its roughly $1 billion of outstanding bond debt, part of a debt burden that totals about $1.6 billion, once loans and other borrowings are included.

in 2007, the company was taken private by Mitt Romney's former private-equity firm Bain Capital in an LBO valued at $2.1 billion that left it saddled with $1.6 billion of high-yield debt. Coming just ahead of the 2008 financial crisis, the company struggled with its high interest payments for several years.

In 2014, its main creditor, private-equity firm Ares Management LLC, took a controlling stake in the company in a deal in which it converted some of its debt into equity, and left Bain as a partial owner with representation on the board.

As Mitt would say, why don't they get a loan from their parents?

Sutter Cane , April 25, 2017 at 3:44 pmWe had several posts on Guitar Center:

http://www.nakedcapitalism.com/2014/08/guitar-center-private-equitys-magical-growth-curve.html

http://www.nakedcapitalism.com/2015/02/end-guitar-center.html

MyLessThanPrimeBeef , April 25, 2017 at 2:37 pmI used to enjoy Garland's writing about Guitar Center. Too bad he embarrassed himself and became the epitome of the deluded Clintonite liberal with his "Time for some game theory" tweetstorm.

Pwelder , April 25, 2017 at 6:55 pmWho was the smarter private equity kid in the room – Bain or Ares?

Paul Greenwood , April 26, 2017 at 1:42 amAres had a deal down in West Texas with Clayton Williams Energy Inc. (You remember Clayton – he ran for Governor of Texas against Ann Richards) Unfortunately Clayton decided not to hedge his production for 2015-6, just before the Saudis pulled the plug on the oil price in November 2014.

All of a sudden CWEI, whose share price had been bouncing around above $100, was two jumps ahead of the sheriff with bankruptcy a real threat. The stock got down to 7.

Beginning last March Ares put in a bunch of equity and debt, and it turned out Clayton had squirreled away a ton of acres in the best part of the Permian Basin. With BK off the table the stock price recovered, Noble Energy bought them out for $130+ per share, and Ares made about six times their money in less than a year.

What's interesting for present purposes is there was no asset-stripping or any other shenanigans. Ares took a risk – which looked huge at the time – and made out like bandits. That's how it's supposed to work. And the funny thing is, Ares is owned by a bunch of Arabs out in the Middle East.

Great piece by Richter and Yves – and a lot of smart commentary from out here in the bleachers. Thanks to all.

jo6pac , April 25, 2017 at 5:17 pmThere are often clauses which allow Courts to revoke Limited Liability where Fraud is suspected. A few cases of Unlimited Liability would change business practices at Board level immensely

JustAnObserver , April 25, 2017 at 6:30 pmI buy about 50% my stuff on line and stores that have figured out to make themselves web friendly are best buy, home depot, osh, and then some manufacture like Haynes underwear have friendly sites. These 3 box stores site went from impossible to use to very friendly to use and shipping is normally free over small amount.

I had to buy a new blue tooth the other day and amazon wanted $170.00 I then went to the company site and it's very much improved bought recondition one for $39.00 free shipping. The new one there was $69.00 they have a third party sell through their site.

Laura weaver , April 25, 2017 at 8:21 pmVery interesting. Could Amazon suffer the fate that people go there to browse what's available but then buy online direct from the maker's site ? As you remarked many of the manufacturers' sites have vastly improved as well as their access to fast shipping channels.

This is already a known defense against the proliferation of counterfeit goods on generic online sites like Amazon that really don't give a f**k about the fakes problem as long as they get their cut of the price.

Mark , April 25, 2017 at 10:36 pmBig box retailers appear to be the " canary in the coal mine " !!

Paul Greenwood , April 26, 2017 at 1:40 amI am a sales rep who sells retailers, both big and small. My accounts are struggling to stay even. No one mentions Amazon as competition, but it is a huge factor.

My three reasons why retail is in decline:

1. Amazon

2. Anyone younger than 35 just doesn't buy or even want to accumulate stuff. They just want wifi and to play with their phones. I wanted everything when I was young and for the most part, still do.

3. The economy. 2% GDP isn't exactly blazing.

Good luck

private equity fund managers do have an incentive not to burn private equity limited partners,

So they flip it at an inflated value to another PE buyer to keep portfolio performances looking good and churn regularly until a secondary-fund picks it up to forward to a Liquidation Front Company. It is exactly what Philip Green did at BHS having stripped a £1 billion dividend courtesy of HBOS corruption.

This game was well exposed under Robert Campeau decades ago. It is amazing how the old shell games continue. Same story at Karstadt in Germany with Thomas Middlehof and the Arcandor disaster.

The Western economic model has been built around Liquidation for decades and the ramping up of liabilities within shell businesses so looters can extract equity and cash. It is so transparent that only criminals do not notice

August 24, 2012 | Jesse's Café Américain

When Gawker first published the Bain Capital tax return data I remember reading somewhere that one should not bother even looking at them because they are not relevant and won't tell you anything.

That struck me as odd at the time. How could someone just dismiss information like this as not even worth reading? Move on, don't look at them?

Well, apparently that is not the case. They seem to contain some nuggets of information suggesting that Romney was being particular aggressive (euphemism for engaging in extra-legal activity) in misstating not trivial income for the purpose of avoiding taxes.

One can only wonder what those undisclosed personal returns might contain.

I don't want to pick on Mitt in particular, although he is starting to look like a setup to make the other guy look good. And what he had done with his income from Bain is certainly open to interpretation as the author admits.

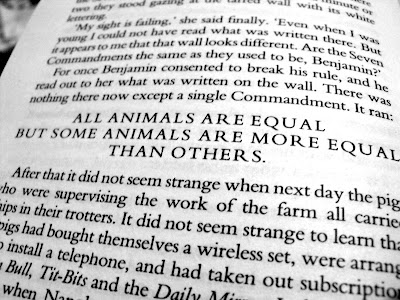

But rather, this speaks to the 'rule of law' issue and how there is a duality in the US, and some animals are more equal than others. And strangely enough, the barnyard hoots its approval.

"Private equity fund managers are compensated in two primary ways: management fees and carried interest. The management fee, traditionally two percent annually, is paid to the managers to cover overhead, salaries, and so forth. The carried interest, traditionally twenty percent, is a share of the profits from the underlying investments. My paper Two and Twenty described the typical arrangement.Management fees are taxed at ordinary income rates; carried interest is often taxed at capital gains rates (around 15 percent - Jesse). I focused in the article on why the carried interest portion is better viewed like bonus compensation and should be taxed at ordinary income rates.

Current law on carried interest is already a sweetheart tax deal for private equity, but why not make it better? Private equity folks are not the type to walk past a twenty-dollar bill lying on the sidewalk.

In the 2000s it became common for private equity fund managers to "convert" their management fees into carried interest. There are many variations on the theme, but here's how many deals worked: each year, before the annual management fee comes due, the fund manager waives the management fee in exchange for a priority allocation of future profits. There is minimal economic risk involved; as long as the fund, at some point, has a profitable quarter, the managers get paid. (If the managers don't foresee any future profits, they won't waive the fees, and they will take cash instead.)

In exchange for a minimal amount of economic risk, the tax benefit is enormous: the compensation is transformed from ordinary income (taxed at 35%) into capital gain (taxed at 15%). Because the management fees for a large private equity fund can be ten or twenty million per year, the tax dodge can literally save millions in taxes every year.

The problem is that it is not legal. Because the deals vary in their aggressiveness, there is some disagreement among practitioners about when it works and when it doesn't. But in my opinion, and the opinion of many tax practitioners, the practices that were common in the private equity industry in the 2000s became very, very questionable, and it's unlikely that they would have stood up in court.

Gawker today posted some Bain documents today showing that Bain, like many other PE firms, had engaged in this practice of converting management fees into capital gain. Unlike carried interest, which is unseemly but perfectly legal, Bain's management fee conversions are not legal. If challenged in court, Bain would lose. The Bain partners, in my opinion, misreported their income if they reported these converted fees as capital gain instead of ordinary income."

Victor Fleischer, Romney's Management Fee Conversions

Read the entire article here.

Jan 30, 2012 | http://www.newyorker.com/

At this point, the people who run America's private-equity funds must be ruing the day Mitt Romney decided to run for President. His fellow Republican candidates, of all people, have painted a vivid picture of private-equity firms-including Bain Capital, where he worked for fifteen years-as job-destroying vultures, who scavenge the meat from American companies and leave their carcasses by the side of the road. Not since the days of "Wall Street" and "Barbarians at the Gate" have the masters of leveraged buyouts looked quite so bad.Given the weak job market, it makes sense that the attacks have focussed on layoffs. But the real problem with leveraged-buyout firms isn't their impact on jobs, which studies suggest isn't that substantial one way or the other. A 2008 study of companies bought by private-equity firms found that their job growth was only about one per cent slower than at similar, public companies; there was more job destruction but also more job creation. And, while private-equity firms are not great employers in terms of wage growth, there's not much evidence that they're significantly worse than the rest of corporate America, which has been treating workers more stingily for about three decades.

The real reason that we should be concerned about private equity's expanding power lies in the way these firms have become increasingly adept at using financial gimmicks to line their pockets, deriving enormous wealth not from management or investing skills but, rather, from the way the U.S. tax system works. Indeed, for an industry that's often held up as an exemplar of free-market capitalism, private equity is surprisingly dependent on government subsidies for its profits. Financial engineering has always been central to leveraged buyouts. In a typical deal, a private-equity firm buys a company, using some of its own money and some borrowed money. It then tries to improve the performance of the acquired company, with an eye toward cashing out by selling it or taking it public. The key to this strategy is debt: the model encourages firms to borrow as much as possible, since, just as with a mortgage, the less money you put down, the bigger your potential return on investment. The rewards can be extraordinary: when Romney was at Bain, it supposedly earned eighty-eight per cent a year for its investors. But piles of debt also increase the risk that companies will go bust.

This approach has one obvious virtue: if a private-equity firm wants to make money, it has to improve the value of the companies it buys. Sometimes the improvement may be more cosmetic than real, but historically private-equity firms have in principle had a powerful incentive to make companies perform better. In the past decade, though, that calculus changed. Having already piled companies high with debt in order to buy them, many private-equity funds had their companies borrow even more, and then used that money to pay themselves huge "special dividends." This allowed them to recoup their initial investment while keeping the same ownership stake. Before 2000, big special dividends were not that common. But between 2003 and 2007 private-equity funds took more than seventy billion dollars out of their companies. These dividends created no economic value-they just redistributed money from the company to the private-equity investors.

As a result, private-equity firms are increasingly able to profit even if the companies they run go under-an outcome made much likelier by all the extra borrowing-and many companies have been getting picked clean. In 2004, for instance, Wasserstein & Company bought the thriving mail-order fruit retailer Harry and David. The following year, Wasserstein and other investors took out more than a hundred million in dividends, paid for with borrowed money-covering their original investment plus a twenty-three per cent profit-and charged Harry and David millions in "management fees." Last year, Harry and David defaulted on its debt and dumped its pension obligations. In other words, Wasserstein failed to improve the company's performance, failed to meet its obligations to creditors, screwed its workers, and still made a profit. That's not exactly how capitalism is supposed to work.

The people who ran Harry and David into the ground have a defense: economic conditions changed in unforeseeable ways. But that's precisely why loading firms with debt in order to reap short-term benefits is bad. It leaves companies unable to weather tough times, and allows private-equity firms to make money even if things go wrong.

As if this weren't galling enough, taxpayers are left on the hook. Interest payments on all that debt are tax-deductible; when pensions are dumped, a federal agency called the Pension Benefit Guaranty Corporation picks up the tab; and the money that the dealmakers earn is taxed at a much lower rate than normal income would be, thanks to the so-called "carried interest" loophole. The money that Mitt Romney made when he was at Bain Capital was compensation for his (apparently excellent) work, but, instead of being taxed as income, it was taxed as a capital gain. It's a very cozy arrangement.

If private-equity firms are as good at remaking companies as they claim, they don't need tax loopholes to make money. If we capped the deductibility of corporate debt, and closed the carried-interest loophole, it would not prevent private-equity firms from buying companies or improving corporate performance. But it would reduce the incentives for financial gimmickry and save taxpayers billions every year. Private-equity firms are excellent at gaming the rules. Time to change them.

During the entire decade of the 1980's, the policies of the Reagan Bush and Bush administrations encouraged one of the greatest paroxysms of speculation and usury that the world has ever seen. Starting especially in the summer of 1982, a malignant and cancerous mass of speculative paper spread through all the vital organs of the banking, credit, and financial system. Capital had long since ceased to be used for the creation of new productive plant and equipment, and new productive manufacturing jobs; investment in transportation, power systems, education, health services and other infrastructure declined well below thje break even level. Wall Street investors came more and more to resemble vampires who ranged over a ghouilish landscape in search of living prey whose blood they could suck to perpetuate their own lively form of death.Industrial employment was out, the service sector was in. The post-industrial society meant that the production of tangible, physical wealth, of hard commodities, within US borders was being terminated. The future would belong to parasitical legions of lawyers, financial services experts, accountants, and clerical support personnel, but the growth in the balance of payments deficit signalled that the game could not go on forever.

On the surface, wild speculation was the order of the day: there was the stock market boom, which underwent a crash in 1987, but then, thanks to James Brady's drugged futures and index options markets, kept rising until the Dow had passed 3,000, although by that time no one could remember why it was still called the industrial average. The stock market provided the right atmosphere for a much broader speculative boom, the one in commercial and residential real estate, which kept going until almost the end of the decade, but which then began to crash with a vengeance. When real estate began to implode, as in Texas at the middle of the 1980's or the northeast after 1988, savings banks and commercial banks by the scores became insolvent. Thus, by the third year of the Bush administration, a bankrupt savings and loan was being seized by federal regulators on almost every business day, and Congressman Dingell of Michigan had to announce that Citibank, still the largest bank in the USA, was indeed "technically" bankrupt. Depositors in Hong Kong started a run on the Citibank branch there; their US counterparts were slower to react, perhaps because deluded by the pathetic faith that the Federal Deposit Insurance Corporation could still cover their deposits.

Even more fundamental than speculation was the absolute primacy of debt. During the Reagan and Bush years, unprecedented federal deficits pushed the public debt of the United States into the ionosphere, with the total almost quadrupling over a little more than ten years to approach the fantastic total of $3.25 thousand billion. In 1989, it was estimated that total debt claims in the US economy had attained almost $25 thousand billion, and their total has increased exponentially ever since. The debt of state and local governments, corporate debt, consumer debt –all expanded into the wild blue yonder. In the meantime, the Great Lakes industrial region became the rust bowl, the Sun belt oil and computer booms collapsed, the great cities of the east were rotten to the core with slums, and farmers went bankrupt more rapidly than at any other time in the memory of man.

Living standards had been in a gradual but constant decline since the days of Nixon, and it began to dawn on more and more families who considered themselves members of the middle class that they could no longer afford their own home, nor hope to send their children to college, all because of the prohibitive costs. The Bureau of the Census made sure in 1990 not to count the number of those who had become homeless during the 1980's, since the real figure would be an acute political embarrassment to George Bush: were there 5 million, or 6, as many as the total population of Sweden, or of Belgium?

New jobs were created, but most of them were dead-ends for losers at or below the mimimum wage that presupposed illiteracy on the part of the applicant: hamburger sales and pizza home delivery were the growth areas, although a smart kid might still aspire to become a croupier. Behind it all lurked the pervasive narcotics trade, with hundreds of billions of dollars a year in heroin, crack, marijuana.

For the vast majority of the US population (to say nothing of the brutal immiseration in the developing countries) it was an epoch of austerity, sacrifice, and decline, of the entropy of a society in which most people have no purpose and feel themselves becoming redundant, both on the job market and ontologically.

But for a paper thin stratum of plutocrats and parasites, the 1980's were a time of unlimited opportunity. These were the practioners of the monstrous financial swindles that marked the decade, the protagonists of the hostile takeovers, mergers and acquisitions, leveraged buy-outs, greenmail and stock plays that occupied the admiration of Wall Street. These were corporate raiders like J. Hugh Liedkte, Blaine Kerr, T. Boone Pickens, and Frank Lorenzo, Wall Street financiers like Henry Kravis and Nicholas Brady.

... ... ...

Henry Kravis's epic achievements in speculation and usury perhaps had something to do with the fact that he was a close family friend of George Bush.

As we have seen, when Prescott Bush was arranging a job for young George Herbert Walker Bush in 1948, he contacted Ray Kravis of Tulsa, Oklahoma, whose business included helping Brown Brothers, Harriman to evaluate the oil reserves of companies. Ray Kravis had quickly offered George a job, but George declined it, preferring to go to work for Dresser Industries, a much larger company. That was how George had ended up in Odessa and Midland, in the Permian basin of Texas. Ray Kravis over the years had kept in close touch with Senator Prescott Bush and George Bush, and young Henry Kravis had been introduced to George and had hob-nobbed with him at various Republican Party and other fund-raising events. Henry Kravis by the early 1980's was a member of the Republican Party's elite Inner Circle.

Bush and Henry Kravis became even more closely associated during the time that Bush, ever mindful of campaign financing, was preparing his bid for the presidency. Among political contributors, Henry Kravis was a very high roller. In 1987-88, Kravis gave over $80,000 to various senators, congressmen, Republican Political Action Committees, and the Republican National Committee. During 1988, Kravis gave $100,000 to the GOP Team 100, which meant a "soft money" contribution to the Bush campaign. Kravis's partner George Roberts also anted up $100,000 for the Republican Team 100. In 1989, the first year in which it was owned by KKR, RJR Nabisco also gave $100,000 to Team 100. During that year, Kravis and Roberts gave $25,000 each to the GOP.

During the 1988 primary season, Kravis was the co-chair of a lavish Bush fundraiser at the Vista Hotel in lower Manhattan at which Henry's fellow Wall Street dealmakers and financier fatcats coughed up a total of $550,000 for Bush. Part of Kravis's symbolic recompense was to be honored with the prestigious title of co-chairman of Bush's Inaugural Dinner in January, 1989. One year later, in January 1990, Kravis was the National Chairman of Bush's Inaugural Anniversary Dinner. This was a glittering gala held at the Kennedy Center in Washington for a thousand members of the Republican Eagles, most of whom qualify by giving the GOP $15,000 or more. The entertainment was organized as an "oldies night," with Chubby Checker, Tony Bennett, and B.B. King. When George Bush addressed the Eagles, he was prodigal in his praise for Henry Kravis as one of "those who did the heavy lifting on this." [fn 5 ]

According to Jonathan Bush, George Bush's brother and the finance chiarman of the New York State Republican Party, Henry Kravis was "very helpful to President Bush in fundraisers." According to brother Jonathan, Kravis "admired the President. And also, significantly, on a personal level, his father, Ray, and [George Bush] were friends from way back. And that meant a lot to Henry. He wanted to be part of that."

Henry Kravis had married the former Janey Smith of Kirksville, Missouri, who now called herself Carolyne Roehm. Carolyne Roehm had been introduced into New York Nouvelle Society by Oscar de la Renta. She and Henry Kravis cultivated a frenetically sybaritic lifestyle in the company of a social circle that included Bush's patron Henry Kissinger, American Express Chairman Jim Robinson and his wife Linda, Donald and Ivana Trump, Anne Bass, corporate raider Saul Steinberg, cosmetics magnate Ronald Lauder, and Bush's finance operative Robert Mosbacher and his wife Georgette. It was very much a Bushman crowd. Kravis and his "trophy wife" lived in a Park Avenue apartment large enough to be a Hollywood sound stage, and also had a 270 acre estate in Weatherstone, Connecticut. The palatial house there, which is listed in the National Historic Register, has nine fireplaces. Henry and Carolyne added a $7 million, six-building, 42,000 square foot "farm complex" for their seven horses. This was Henry Kravis, chief stoker of the bonfire of the vanities, celebrated by Vice President Dan Quayle as the New York Republican Party Man of the Year.

It was to such an apostle of usury that George Bush turned for advice on public policy in economics and finance. According to Kravis, Bush "writes me handwritten notes all the time and he calls me and stuff, and we talk." The talk concerned what the US government should do in areas of immediate interest to Kravis: "We talked on corporate debt–this was going back a few years–and what that meant to the private sector," said Kravis.

Henry Kravis certainly knows all about debt. The 1980's witnessed the triumph of debt over equity, with a tenfold increase in total corporate debt during the decade, while production, productive capacity, and unemployment stagnated and declined. One of the principal ways in which this debt was loaded onto a shrinking productive base was through the technique of the hostile, junk-bond assisted leveraaged buyout, of which Henry Kravis and his firm were the leading practitioners.

The economist Franco Modigliani had written in the 1950's about the theoretical debt limits of corporations. Small scale leveraged buyouts were pioneered by Kohlberg during the late 1970's. In its final form, the technique looked something like this: Corporate raiders looked around for companies that would be worth more than their current stock price if they were broken up and sold off. Using money borrowed from a number of sources, the raider would make a tender offer (once again, a la Jimmy Gammell in the Liedkte United Gas buyout) or otherwise secure a majority of the shares. Often all outstanding shares in the company would be bought up, taking the company private, with ownership residing in a small group of financiers. The company would end up saddled with an immense amount of new debt, often in the form of high-yield, high-risk sunbordinated debt certificates called junk bonds. The risk on these was high since, if the company were to go bankrupt and be auctioned off, the holders of the junk bonds would be the last to get any compensation.

Often, the first move of the raider after seizing control of the company and forcing out its existing management would be to sell off the parts of the firm that produced the least cash-flow, since enhanced cash flow was imperative to start paying the new debt. Proceeds from these sales could also be used to pay down some of the initial debt, but this process inevitably meant jobs destroyed and production diminished.

These raiding operations were justified by a fascistoid-populist demagogy that accused the existing management of incompetence, indolence and greed. The LBO pirates professed to have the interests of the shareholders at heart, and made much of the fact that their operations increased the value of the stock and, in the case of tender offers, gave the stockholders a better price than they would have gotten otherwise. The litany of the corporate raider was built around his committment to "maximize shareholder value;" workers, bondholders, the public, and management were all expendable. Ivan Boesky and others further embroidered this with a direct apology for greed as a motor force of progress in human affairs.

An important enticement to transform stocks and equity into bonded and other debt was provided by the insanity of the US tax code, which taxed profits distributed to shareholders, but not the debt paid on junk bonds. The ascendancy of the leveraged buyout therefore proceeded pari passu with the demolition of the US corporate tax base, contributing in no small way to the growth of federal deficits. Plutocrats are always adept in finding loopholes to avoid paying their taxes. Ultimately, the big profits were expected when the companies acquired, after having been downsized to "lean and mean" dimensions, had their stock sold back to the public. KKR reserved itself 20% of the profits on these final transactions. In the meantime Kravis and his associates collected investment banking fees, retainer fees, directors' fees, management fees, monitoring fees, and a plethora of other charges for their services.

The leverage was accomplished by the smaller amount of equity left outstanding in comparison with the vastly increased debt. This meant that if, after deducting the debt service, profits went up, the return to the investors could become very high. Naturally, if losses began to appear, reverse leverage would come into play, producing astronomical amounts of red ink. Most fundamental was that companies were being loaded with debt during the years of what the Reagan-Bush regime insisted on calling a boom. It was evident to any sober observer that in case of a recession or a new depression, many of the companies that had succumbed to leveraged buyouts and related forces of usury would very rapidly become insolvent. The Reagan-Bush regime was forced to argue that supply-side economics and Bush's deregulation had abrogated the business cycle, and that there never would be any more recessions. This is why the "recession" (in reality the exacerbation of the pre-existing depression) that George Bush was forced to acknowledge during late 1990 was so ominous in its implications. The leveraged buyouts of the 1980's were now doomed to collapse. The handwriting on the wall was clear by September-October of 1989, the first year of George Bush's presidency, when the $250 billion market for junk bonds collapsed just in advance of the mini-crash of the New York Stock Exchange.

All in all, during the years between 1982 and 1988, more than 10,000 merger and acquisition deals were completed within the borders of the USA, for a total capitlization of $1 trillion. There were in addition 3500 international mergers and acquisitions for another $500 billion. [fn 6 ] The enforcement of antitrust laws atrophied into nothing: as one observer said of the late 1980's, "such concentrations had not been allowed since the early days of antitrust at the beginning of the century."

George Bush's friend Henry Kravis raised money for his leveraged buyouts from a number of sources. Money came first of all from insurance companies such as the Metropolitan Life Insurance Company of New York, which cultivated a close relation with KKR over a number of years. Met was joined by Prudential, Aetna, and Northwest Mutual. Then there were banks like Manufacturers Hanover Trust and Bankers Trust. All these institutions were attracted by astronomical rates of return on KKR investments, estimated at 32.2% in 1980, 41.8% in 1982, 28% in 1984, and 29.6% in 1986. By 1987, KKR prospectus boasted that they had carried out the first large LBO of a publicly held company, the first billion-dollar LBO, the first large LBO of a public company via tender offer, and the largest LBO in history, Beatrice Foods.

Then came the state pension funds, who were also anxious to share in these very large returns. The first to begin investing with KKR was Oregon, which shovelled money to KKR like there was no tomorrow. Other states that joined in were Washington, Utah, Minnesota, Michigan, New York, Wisconsin, Illinois, Iowa, Massachusetts, and Montana. The decisions to committ funds were typically made by state boards. An example is Minnesota: here the State Board of Investment is made up of the Governor, the state Treasurer, the state auditor, the Secretary of State, and the Attorney General, currently Skip Humphrey. Some of these funds are so heavily committed to KKR that if any of the highly-leveraged deals should go sour in the current "recession," pensions for many retired state workers in those states would soon cease to exist. In that eventuality, which for many working people has already occurred, the victims should remember George Bush, the political godfather of Henry Kravis and KKR.

KKR had one other very important source of capital for its deals: this was the now-defunct Wall Strreet investment firm of Drexel, Burnham, Lambert, and its California-based junk bond king, Michael Milken. Drexel and Milken were the most important single customers KKR had. (Drexel had its own Harriman link: it had merged with Harriman Ripley & Co. of New York in 1966.) During the period of close working alliance between KKR and Drexel, Milken's junk-bond operation raised an estimated $20 billion of funds for KKR. Junk bonds were high-risk, high-yield, junior debt securities that Milken floated. He started off with junk bonds issued by fly-by-night insurance companies owned by financiers seeking to emerge from the penumbra of Meyer Lansky. These included Carl Lindner and his Great American; Saul Steinberg and his Reliance Insurance Co., Meshulam Riklis and his Rapid American group; Laurence Tisch and CNA; Nelson Peltz; Victor Posner; Carl Icahn; Thomas Spiegel and his Columbia Savings and Loan; and Fred Carr, a financial gunslinger of the 1960's and his First Executive Corp. insurance firm. Later, the circle of Milken's customers would expand to include commercial banks, savings and loans, mutual funds, upscale insurance companies and others who could not resist the high yields. These robbery barons of modern usury were dubbed "Milken's monsters" by one of their number, Meshulam Riklis.

All of these personages pranced at Milken's annual meetings in Beverley Hills, which were followed by evenings of sumptuous entertainment. These became known as "the predators' ball," and attracted such people as T. Boone Pickens, Icahn, Irwin Jacobs, Sir James Goldsmith, Oscar Wyatt, Saul Steinberg, Boesky, Lindner, the Canadian Belzberg family, Ron Perelman, and other such figures.

First Executive Corp. was the first great bankruptcy among the insurance companies in early 1991, giving the depression of the 1990's a dimension that the economic-financial conflagration of the 1930's did not possess. First Executive Life succumbed to losses on its junk bond portfolio, and it will be the first of many insurance companies to find bankrutpcy via this route. Shortly thereafter, Mutual Benefit Life Insurance Company of New Jersey was seized by state regulators. Mutual Benefit was also the victim of combined real estate and junk bond losses, and more retirement plans were threatened with annihlitation. Those whose pensions are lost must recall the junk bond united front that reached from Milken to Kravis to Bush.

Spiegel's Columbia S&L is a classic case of a thrift institution that went wild in its acquisition of Milken's high-yield junk. At one time this instutution had about $10 billion of junk in its portfolio. Columbia S&L was seized by federal regulators during the early months of 1990. Although many savings and loan bankruptcies have been caused by real estate speculation, many must also be attributed to a failed quest for a junk bonanza.

Milken's silent partner was Ivan Boesky, the arbitrageur who went beyond program trading to become a silent partner in advancing Milken's stockjobbing: sometimes Milkenm would have Boesky begin to acquire the stock of a certain company so as to signal to the market that it was in play, setting off a stampede of buyers when this suited Milken's strategy.

The Beatrice LBO illustrates how necessary Milken's role was to the overall strategy of Bush backer Kravis. Beatrice was the biggest LBO up to the time it was completed in January-February 1986, with a price tag of $8.2 billion. As part of this deal, Kravis gave Milken warrants for five million shares of stock in the new Beatrice corporation. These warrants could be used in the future to buy Beatrice shares at a small fraction of the market price. One result of this would be a dilution of the equity of the other investors. Milken kept the warrants for his own account, rather than offer them to his junk bond buyers in order to get a better price for the Beatrice junk bonds. Later in the same year, KKR bought out Safeway grocery stores for $4.1 billion, of which a large part came from Milken.

After 1986, Kravis and Roberts were gripped by financial megalomania. Between 1987 and 1989, they acquired 8 additional companies with an aggregate price tag of $43.9 billion. These new victims included Owens-Illinois glass, Duracell, Stop and Shop food markets, and, in the landmark transaction of the 1980's, RJR Nabisco. RJR Nabisco was the product of a number of earlier mergers: National Bisucuit Company had merged with Standard Brands to form Nabisco Brands, and this in turn merged with R.J. Reynolds Tobacco to create RJR Nabisco. It is important to recall that R.J. Reynolds was the concern traditionally controlled by the family of Bush's personal White House lawyer, C. Boyden "Boy" Gray.

The battle for control of RJR Nabisco was lost by RJR Nabisco chairman Ross Johnson, Peter Cohen of Sherason Lehman Hutton and the notorious John Gutfruend of Salomon Brothers. KKR opposed this group, and a third offer for RJR came from First Boston. The Johnson offer and the KKR were about the same, but a cover story in the Luce-Skull and Bones Time Magazine in early December, 1988 targetted Johnson as the greedy party. The attraction of RJR Nabisco, one of the twenty largest US corporations, was an immense cash flow supplied especially by its cigarette sales, where profit margins were enormous. The crucial phases of the fight corresponded with the presidential election of 1988: Bush won the White House, so it was no surprise that Kravis won RJR with a bid of about $109 per share compared to a stock price of about $55 per share before the company was put into play, giving the prebuyout shareholders a capital gain of more than $13.3 billion. How much of that went to Boy Gray of the Bush White House?

The RJR Nabisco swindle generated senior bank debt of about $15 billion. The came $5 billion of subordinate debt, with the largest offering of junk bonds ever made. Then came an echelon of even more junior debt with payment in securities and junk bonds that payed interest not in cash, but in other junk bonds. But even with all the wizardry of KKR, there could have been no deal without Milken and his junk bonds. The banks could not muster the cash required to complete the financing; KKR required bridge loans. Merrill Lynch and Drexel were in the running to provide an extra $5 billion of bridge financing. Drexel got Milken's monsters and many others to buy short-term junk notes with an interest rate that would increase the longer the owner refrained from cashing in the note. Drexel's "increasing rate notes" easily brought in the entire $5 billion required.

In November of 1986, Ivan Boesky pleaded guilty to one felony count of manipulating securities, and his testimony led to the indictment of Milken in March, 1989, some months after the RJR Nabisco deal had been sewn up. In order to protect more important financial players, Milken was allowed to plead guilty in April 1990 a five counts of insider trading, for which he agreed to pay a fine of $600 million. On February 13, 1990, Drexel Burnham Lambert had declared itself bankrupt and gone into liquidation, much to the distress of junk bond holders everywhere who saw the firm as a junk bond buyer of last resort.

By this time, many of the great LBOs had begun to collapse. Robert Campeau's retail sales empire of Allied and Federated stores blew up in the fall of 1989, bring down almosty $10 billion of LBO debt. Revco, Freuhauf, Southland (Seven-Eleven stores), Resorts International, and many other LBOs went into chapter eleven proceedings. As for KKR's deals, they also began to implode: SCI-TV, a spin-off of Storer Broadcasting, announced that it could not service its $1.3 billion of debt, and forced the holders of $500 million in junk bonds to settle for new stocks and bonds worth between 20 and 70 cents on the dollar. Hillsborogh Holdings, a subsidiary of Jim Walker, went bankrupt, and Seamans Furniture put through a forced restructuring of its debt.

It was clear at the time of the RJR Nabisco LBO that the totality of the company's large cash flow would be necessary to maintain payments of $25 billion of debt. That will take a lot of animal crackers and Winstons. If RJR Nabisco had been a foreign country, it would have ranked among the top 15 debtor nations, coming in between Peru and the Phillipines. Within a short time after the LBO, RJR Nabisco proved unable to maintain payments. KKR was forced to inject several billion dollars of new equity, take out new bank loans, and dunning its clients for an extra $1.7 billion. RJR Nabisco by the early autumn of 1991 was a time bomb ticking away near the center of a ruined US economy. If citizens are bright enough to follow the line that leads back from Milken to Kravis to Bush, RJR and similar horror stories could politically demolish George Bush.

In September 1987, Senator William Proxmire submitted a bill which aimed at restricting takeovers. Two weeks later, Rep. Rostenkowski of Illinois offered a bill to limit the tax deductability of the interest on takeover debt. The LBO gang in Wall Street was horrified, even though it was clear that the Reagan-Bush team would oppose such legislation using every trick in the book. Later, LBO ideologues blamed the Congress for causing the crash of October, 1987.

Kravis has always been adamant in opposing any restrictions on the kind of insanity we have briefly reviewed. "I'm very much of a free-market person," says Kravis. I don't want interference. My life…you've listened to my life story, I don't want interference! The best thing to happen to people and this country is a free market system, and I'm very concerned, if we don't keep the right people in office, that we're not going to have this free-market environment. And we should have it!" [fn 7]

This corresponds exactly to Bush's policy. During the 1988 campaign, Bush presented his views on hostile takeovers, using the forum provided by his old friend T. Boone Pickens' USA Advocate, a monthly newsletter published by the United Shareholders Association, which Pickens runs. In the October, 1988 issue of this publication, Bush made clear that he was not worried about leveraged buyouts. Rather, what concerned Bush was the need to prevent corporations from adopting defenses to deter such attempted hostile takeovers. Bush indicated he wanted to ban poison pill defenses, which often take the form of a new class of stock in a company that lets its holders buy stock in the successor company at rock-bottom prices after a buyout. Poison pills were invented by New York lawyer Marty Lipton, and did not deter raider Sir James Goldsmith from seizing control of Crown Zellerbach in the mid-1980's, although Goldsmith's costs were increased.

Bush also railed against "golden parachutes," which provide lucrative settlements for top executives who are ousted as the result of a takeover:

I am frankly a bit skeptical about claims that these so-called 'defensive' tactics are necessary to encourage long-term investment. Studies suggest that prices of stock reflect information that is publicly available. Sometimes it seems that managers use these tactics to save themselves from the competitive pressures of the market for corporate control, not to protect the interests of the shareholders.

Bush was clearly hostile to any federal restrictions on hostile takeovers. If anything, he was closer to those who demanded that the federal government stop the states from passing laws that interfere with LBO activity. For that notorious corporate raider and disciple of Chairman Mao Liedtke, T. Boone Pickens, the message was clear:

I know that Vice President Bush is a free enterpriser. I don't think there is any doubt if you look at what Vice President Bush has said and what Gov. Dukakis has said that Bush is pro-stockholder. I would say Dukakis is pro-management. *

The expectations of Pickens and his ilk were not disappointed by the Bush cabinet that took office in January, 1989. The new Secretary of the Treasury, Bush crony Nicholas Brady, was only a supporter of leveraged buyouts; he had been one of the leading practitioners of the mergers and acquisitions game during his days in Wall Street as a partner of the Harriman-allied investment firm of Dillon Read.

The family of Nicholas Brady has been allied for most of this century with the Bush-Walker clan. During his Wall Street career at Dillon, Read, Brady, like Bush, cultivated the self-image of the patrician banker, becoming a member of the New York Jockey Club and racing his own thorougbred horses at the New York tracks once presided over by George Herbert Walker and Prescott Bush. Brady, like Bush, is a member of the Bohemian Club of San Francisco and attended the Bohemian Grove every summer. Inside the Bohemian Grove oligarchic pantheon, Brady enjoys the special distinction of presiding over the prestigious Mandalay Camp (or cabin complex), the one habitually attended by Henry Kissinger, and sometimes frequented by Gerald Ford. When Senator Harrison Williams of New Jersey was driven out of office by the FBI's "Abscam" entrapment operation, Brady was appointed to fill out the remainder of the term to which Williams had been elected. Brady is also reportedly a victim of dyslexia.

At the Regency in Lower Manhattan, Brady rubbed elbows each morning at breakfast with Joe Flom and the rest of the the Skadden Arps crowd, Arthur F. Long of D.F. King and Co., Marty Lipton, Arthur Liman, Felix Rohatyn, Boesky's friend Marty Siegel, and Joe Perella of First Boston.

Brady's LBO experience goes back to the 1985 battle for control of Unocal, the former Union Oil Company. T. Boone Pickens and Mesa Petroleum attempted a hostile takeover of Unocal through a complex "two-tiered" tender offer by which those shareholders willing to help Pickens to a majority stake in Unocal would receive cash payment for their stocks, but those forced to sell to Pickens after he had gone over the top would be compelled to accept junk securities. In order to defend against this two-tier, front-loaded hostile tender offer, Unocal management called in Brady's Dillon Read together with Goldman Sachs.

Working with Goldman Sachs, Brady helped to devise a new form of anti-takoever defense for Unocal: it was in effect a self-inflicted leveraged buyout, a self-tender for a large portion of Unocal's stock which the company offered to buy back at a higher price than the one stipulated in the Pickens tender offer, although Unocal would refuse to accept any of the shares held by Pickens. Pickens tried to overturn this selective self-tender in the courts of Delaware, but he was defeated.

The self-tender sponsored by Brady's investment bankers was actually a usurious chicken game: Unocal's tender offer to buy 80 million shares at an astronomical $72 per share in comparison with the $54 offered by Pickens. This meant $5.8 billion in new high-interest junk-bond debt for Unocal, in another triumph of debt over equity. The premiss was that if Pickens insisted on going ahead, he might very well take over Unocal, but the new debt burden would mean that the company would soon go bankrupt and Pickens would lose all his money. In this case, the Unocal management advised by Nick Brady was more than willing to gamble with the existence of their entire company, and thus with the livelihoods of thousands of workers and their families, to ward off the advances of Pickens. In the end, this device would load Unocal with a crushing $3.6 billion of high-interest debt as a result of the plan advocated by Brady's firm.

Nick Brady got the job he presently occupies by heading up a study of the October, 1987 stock market crash, the results of which Brady announced on a cold Friday afternoon in January, 1988, just after the New York stock market had taken another 150 point dive.

The study of the October, 1988 "market break" was produced by a group of Wall Street and Treasury insiders billed as the "Presidential Task Force on Market Mechanisms." At the center of the report's attention was the relation between the New York Stock Exchange, American Stock Exchange, and NASDAC over-the-counter stock trading, on the one hand, and the future, options, and index trading carried on at the Chicago Board of Trade, Chicago Board Options Exchange, and Chicago Mercantile Exchange. The Brady group examined the impact of program trading, index arbitrage and portfolio insurance strategies on the behavior of the markets that led to the crash. The Brady report recommended the centralization of all market oversight in a single federal agency, the unification of clearing systems, consistent margins, and the installation of circuit breaker mechanisms. That, at least, was the public content of the report.

The real purpose of the Brady report was to create a series of drugged and manipulated markets using funds from the Federal Reserve and other sources. The Brady group realized that if the Chicago futures price of a stock or stock index could be artifically inflated, this would be of great assistance in propping up the value of the underlying stock in New York. The Brady group focussed on the Major Market Index of 20 stock futures traded on the Chicago Board of Trade, which roughly corresponded to the principal stocks of the Dow Jones Industrial Average. As long as the MMI was trading at a higher price than the DJIA, the program traders and index arbitrageurs would tend to sell the MMI and buy the underlying stock in New York in order to lock in their stockjobbing profits. The great advantage of this system was first of all that some tens of millions of dollars in Chicago could generate some hundreds of millions of dollars of demand in New York. In addition, the margin requirements for borrowing money for use to buy futures in Chicago were much less stringent than the requirements for margin buying of stocks in New York. Liquidity for this operation could be drawn from banks and other institutions loyal to the Bush-Baker-Brady power cartel, with full backup and assistance from the district banks of the Federal Reserve.

The Brady "drugged market" mechanisms, with the refinements they have acquired since 1988, are a key factor behind the Dow Jones Industrials' seeming defiance of the law of gravity in attainting a new all time high well above the 3000 mark during 1991.

Brady's exercise was nothing new: during the collapse of the Earl of Oxford's South Sea bubble in 1720, the South Sea Company attempted to support the astronomically inflated price of its shares by becoming a buyer of its own stock until its cash and credit reserves were exhausted. Such maneuvers can indeed delay the onset of the final collapse for some period of time, but they guarantee that when the panic, crash and bankruptcy finally become overwhelming, the aggregate damage to society will be far greater than if the crash had been allowed to occur according to its own spontaneous dynamic. For this reason, a large part of the fearful price that is being exacted from the American people as the depression unfolds in its full fury is a result of the Bush-Brady measures to postpone the inevitable reckoning beyond the 1988 election.

One important case study of the impact of Bush's Task Force on Regulatory Relief is the meat-packing industry. In February 1981, when Reagan gave Bush "line" authority for deregulation, he promulgated Executive Order 12291, which established the principle that federal regulations "be based upon adequate evidence that their potential benefits to society are greater than their potential costs to society." In practice, that meant that Bush threw health and safety standards out the window in order to ingratiate himself with entrepreneurs. In March 1981, Bush wrote to businessmen and invited them to enumerate the 10 areas they wanted to see deregulated, with specific recommendations on what they wanted done. By the end of the year Bush's office issued a self-congratulatory report boasting of a "significant reduction in the cost of federal regulation." In the meatpacking industry, this translated into production line speedup as jobs were eliminated, with a cavalier attitude towards safety precautions. At the same time the Occupational Safety and Health Administration sharply reduced inspections, often arriving only after disabling or lethal accidents had already occured. In 1980 there were 280 OSHA inspections in meat packing plants, but in 1988 there were only 176. This, in an industry in which the rate of personal injury is 173 persons per working day, three times the average of all remaining US factories. [fn 8]

Bush used his Regulatory Relief Task Force as a way to curry favor with various business groups whose support he wanted for his future plans to assume the presidency in his own right. According to one study made midway through the Reagan years, Bush converted his own office "into a convenient back door for corporate lobbyists" and "a hidden court of last resort for special interest groups that have lost their arguments in Congress, in the federal courts, or in the regulatory process." "Case by case, the vice president's office got involved in some mean and petty issues that directly affect people's health and lives, from the dumping of toxic pollutants to government warnings concerning potentially harmful drugs." [fn 9]

There were also reports of serious abuses by Bush, especially in the area of conflicts of interest. In one case, Bush intervened in March, 1981 in favor of Eli Lilly & Co., a company of which he had been a director in 1977-79. Bush had owned $145,000 of stock in Eli Lilly until January, 1981, after which it was placed in a blind trust, meaning that Bush allegedly had no way of knowing whether his trust still owned shares in the firm or not. The Treasury Department had wanted to make the terms of a tax break for US pharmaceutical firms operating in Puerto Rico more stringent, but Vice President Bush had contacted the Treasury to urge that "technical" changes be made in the planned restriction of the tax break. By April 14 Bush was feeling some heat, and he wrote a second letter to Treasury Secretary Don Regan asking that his first request be withdrawn because Bush was now "uncomfortable about the appearance of my active personal involvement in the details of a tax matter directly affecting a company with which I once had a close association." [fn 10] Bush's continuing interest in Eli Lilly is underlined by the fact that the Pulliam family of Indiana, the family clan of Bush's later running mate Dan Quayle, owned a very large portion of the Eli Lilly shares. Bush's choice of Quayle was but a re-affirmation of a pre-exisiting financial and political alliance with the Pulliam interests, which also include a newspaper chain.

The long-term results of the deregulation campaign that Bush used to burnish his image are suggested by the September, 1991 fire in a chicken-processing plant operated by Imperial Food Products in Hamlet, North Carolina, in which 25 persons died. One obvious cause of this tragedy was an almost total lack of adequate state and federal inspection, which might have identified the fire hazards that had built up over a period of years. This fire led during October, 1991 to the bankruptcy of the Imperial Food Products Company, which could not obtain financing to roll over its short-term and long-term debt obligations. 225 workers at the Hamlet plant lost their jobs, as did 200 workers at the company's other plant in Cumming, Georgia.