|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

Corruption of regulators

Deep conflicts of interest of enforcement officials, especially in SEC

Lack of transparency, problems with following GAAP standards

Fiat currency problem

| "The purpose of studying economics is not to acquire a set of ready-made answers to economic questions, but to learn how to avoid being deceived by economists." |

Government controlled by financial oligarchy is not government of people by people and for people. It's more like an occupying force. Extremes meet and such a situation has scary similarities to the Bolshevik's 75 years occupation of Russia. In a way the USSR was yet another form of banana republic, the country controlled by criminal military junta.

Some observers suggest that the USA is sliding toward a more traditional model of the banana republic is which the role of Communist Party which controlled and wasted most of the resources in the USSR is played by financial oligarchy. That bodes bad for 401K investors as military overreach abroad and stagnant economy with high unemployment at home created problem of solvency for the USA. Historically banana republic solution to unsustainable government debt has been currency depreciation or, even, hyperinflation. But the USA situation is complicated by the instruments that make solution of debt problem via hyperinflation (gold ETFs, TIPs, commodities ETFs in general). That makes more probable that an intermediate step will be used to buy more time for the politicians in power: raiding retirement accounts of citizens. So two main threats from government now are:

Had we done so, boomers facing retirement over the next few years would be even worse off than they are today. Now they're struggling with pension plans worth less than they counted on, and home values that are tanking. At least they can rely on a monthly Social Security check.

But had we privatized, they'd be totally reliant on the stock market. And look what's happened to the market: Compared to stock values ten years ago, the S&P 500 has risen a little over 1 percent a year, adjusted for inflation. Even Treasury bonds have done better. Go back nine years and there's been no gain at all. Go back eight years and the market has been off an average of 1.4 percent a year.

Yes, I know, it's been a rough time. First the tech bubble bursting, then 9/11, then Enron, then the housing bubble bursting, then the credit crunch. But that's my point. We can't necessarily rely on the stock market. ...

Sure, the stock market has done well over the past half century. But there have been decades like the 1970s and this one, so far, where it's been a disaster. That's why we have Social Security – so that if your timing is bad and you get caught in a downdraft, you still have something to fall back on in retirement.

It would be a definite exaggeration to state that the US is already a banana republic. Built the relationship between Wall Street and Washington is as close to banana republic model as one can get ('The Single Most Drastic Error in Policy in Modern History')

DAVID STOCKMAN: ...we have gotten into this syndrome, I think, over the last 20 years, where policy of the Treasury and of the Fed has been dictated by Wall Street, that, if Wall Street threatens to have a hissy fit, or the stock market is going to go down, the Fed has basically capitulated and is creating a very unstable and dangerous financial system in our economy.

After all the key characteristic of banana republic is the existence of comprador elite (Bolshevik elite which adhered to an ideological doctrine rather then the host country also fits the bill ):

The members of a national business class of senior corporate managers who derive their position and status from connection to foreign corporations. The term is used in critical theories of the sociology of development to imply that a foreign-allied national business class tends to encourage local economic development that benefits other nations rather than their own.

But the trend is very suspicious and financial oligarchy is supra-national by definition. A banana republic isn't characterized only by a rotten political system, ruled by a small, wealthy, and corrupt clique usually put in power or supported by foreign interests (in the 20th century, in the case of several Central and Latin American countries, Ukraine and some other former USSR countries by the US). Other key characteristics include huge wealth and income inequities, poor infrastructure, backwardness in many sectors of the economy, low capital spending, the reliance on foreign capital inflow, and a weakening currency (see Will the US Become a Banana Republic by Marc Faber).

Another important feature of a banana republic is that it the data about its economy are extremely unreliable, often fudged in the interests of the current administration. The other way to say this is: nobody believes government data. Manipulation of statistics is an important, immanent feature of the banana republics. Kevin P. Phillips aptly called this "Numbers racket":

Almost four decades have passed since the United States scrapped its last currency ties to precious metals. Our copper and nickel coinage still retains some metallic value, but not nearly enough for the purpose of currency tampering—the historic temptation of inflation-plagued or otherwise wayward governments, including, at times, our own. Instead, since the 1960s, Washington has been forced to gull its citizens and creditors by debasing official statistics: the vital instruments with which the vigor and muscle of the American economy are measured. The effect, over the past twenty-five years, has been to create a false sense of economic achievement and rectitude, allowing us to maintain artificially low interest rates, massive government borrowing, and a dangerous reliance on mortgage and financial debt even as real economic growth has been slower than claimed. If Washington’s harping on weapons of mass destruction was essential to buoy public support for the invasion of Iraq, the use of deceptive statistics has played its own vital role in convincing many Americans that the U.S. economy is stronger, fairer, more productive, more dominant, and richer with opportunity than it actually is.

The corruption has tainted the very measures that most shape public perception of the economy—the monthly Consumer Price Index (CPI), which serves as the chief bellwether of inflation; the quarterly Gross Domestic Product (GDP), which tracks the U.S. economy’s overall growth; and the monthly unemployment figure, which for the general public is perhaps the most vivid indicator of economic health or infirmity. Not only do governments, businesses, and individuals use these yardsticks in their decision-making but minor revisions in the data can mean major changes in household circumstances—inflation measurements help determine interest rates, federal interest payments on the national debt, and cost-of-living increases for wages, pensions, and Social Security benefits. And, of course, our statistics have political consequences too. An administration is helped when it can mouth banalities about price levels being “anchored” as food and energy costs begin to soar.

The truth, though it would not exactly set Americans free, would at least open a window to wider economic and political understanding. Readers should ask themselves how much angrier the electorate might be if the media, over the past five years, had been citing 8 percent unemployment (instead of 5 percent), 5 percent inflation (instead of 2 percent), and average annual growth in the 1 percent range (instead of the 3–4 percent range). We might ponder as well who profits from a low-growth U.S. economy hidden under statistical camouflage. Might it be Washington politicos and affluent elites, anxious to mislead voters, coddle the financial markets, and tamp down expensive cost-of-living increases for wages and pensions?

Let me stipulate: the deception arose gradually, at no stage stemming from any concerted or cynical scheme. There was no grand conspiracy, just accumulating opportunisms. As we will see, the political blame for the slow, piecemeal distortion is bipartisan—both Democratic and Republican administrations had a hand in the abetting of political dishonesty, reckless debt, and a casino-like financial sector. To see how, we must revisit forty years of economic and statistical dissembling.

A short history of “pollyanna creep”

This apt phrase originated with John Williams, a California-based economic analyst and statistician who “shadows,” as he puts it, the official Washington numbers. In a 2006 interview, Williams noted that although few Americans ever see the fine print, the government “always footnotes the changes and provides all the fine detail. Nonetheless, some of the changes are nothing short of remarkable, and the pattern over time is what I call Pollyanna Creep.” Williams is one of the small group of economists and analysts who have paid any attention to the phenomenon. A few have pointed out the understatement of the Consumer Price Index—the billionaire bond manager Bill Gross has described it as an “haute con job,” and Bloomberg columnist John Wasik has dismissed it as “a testament to the art of spin.”

In 2003, a University of Chicago economist named Austan Goolsbee (now a senior economic adviser to Barack Obama’s presidential campaign) published an op-ed in the New York Times pointing out how the government had minimized the depth of the 2001–2002 U.S. recession, having “cooked the books” to misstate and minimize the unemployment numbers. Unfortunately, the critics have tended to train their axes on a single abuse, missing the broad forest of statistical misinformation that has grown up over the past four decades.

The story starts after the inauguration of John F. Kennedy in 1961, when high jobless numbers marred the image of Camelot-on-the-Potomac and the new administration appointed a committee to weigh changes. The result, implemented a few years later, was that out-of-work Americans who had stopped looking for jobs — even if this was because none could be found — were labeled “discouraged workers” and excluded from the ranks of the unemployed, where many, if not most, of them had been previously classified. Lyndon Johnson, for his part, was widely rumored to have personally scrutinized and sometimes tweaked Gross National Product numbers before their release; and by the 1969 fiscal year, Johnson had orchestrated a “unified budget” that combined Social Security with the rest of the federal outlays. This innovation allowed the surplus receipts in the former to mask the emerging deficit in the latter.

Richard Nixon, besides continuing the unified budget, developed his own taste for statistical improvement. He proposed—albeit unsuccessfully—that the Labor Department, which prepared both seasonally adjusted and non-adjusted unemployment numbers, should just publish whichever number was lower. In a more consequential move, he asked his second Federal Reserve chairman, Arthur Burns, to develop what became an ultimately famous division between “core” inflation and headline inflation. If the Consumer Price Index was calculated by tracking a bundle of prices, so-called core inflation would simply exclude, because of “volatility,” categories that happened to be troublesome: at that time, food and energy. Core inflation could be spotlighted when the headline number was embarrassing, as it was in 1973 and 1974. (The economic commentator Barry Ritholtz has joked that core inflation is better called “inflation ex-inflation”—i.e., inflation after the inflation has been excluded.)

In 1983, under the Reagan Administration, inflation was further finagled when the Bureau of Labor Statistics decided that housing, too, was overstating the Consumer Price Index; the BLS substituted an entirely different “Owner Equivalent Rent” measurement, based on what a homeowner might get for renting his or her house. This methodology, controversial at the time but still in place today, simply sidestepped what was happening in the real world of homeowner costs. Because low inflation encourages low interest rates, which in turn make it much easier to borrow money, the BLS’s decision no doubt encouraged, during the late 1980s, the large and often speculative expansion in private debt—much of which involved real estate, and some of which went spectacularly bad between 1989 and 1992 in the savings-and-loan, real estate, and junk-bond scandals. Also, on the unemployment front, as Austan Goolsbee pointed out in his New York Times op-ed, the Reagan Administration further trimmed the number by reclassifying members of the military as “employed” instead of outside the labor force.

The distortional inclinations of the next president, George H.W. Bush, came into focus in 1990, when Michael Boskin, the chairman of his Council of Economic Advisers, proposed to reorient U.S. economic statistics principally to reduce the measured rate of inflation. His stated grand ambition was to move the calculus away from old industrial-era methodologies toward the emerging services economy and the expanding retail and financial sectors. Skeptics, however, countered that the underlying goal, driven by worry over federal budget deficits, was to reduce the inflation rate in order to reduce federal payments—from interest on the national debt to cost-of-living outlays for government employees, retirees, and Social Security recipients.

It was left to the Clinton Administration to implement these convoluted CPI measurements, which were reiterated in 1996 through a commission headed by Boskin and promoted by Federal Reserve Chairman Alan Greenspan. The Clintonites also extended the Pollyanna Creep of the nation’s employment figures. Although expunged from the ranks of the unemployed, discouraged workers had nevertheless been counted in the larger workforce. But in 1994, the Bureau of Labor Statistics redefined the workforce to include only that small percentage of the discouraged who had been seeking work for less than a year. The longer-term discouraged—some 4 million U.S. adults—fell out of the main monthly tally. Some now call them the “hidden unemployed.” For its last four years, the Clinton Administration also thinned the monthly household economic sampling by one sixth, from 60,000 to 50,000, and a disproportionate number of the dropped households were in the inner cities; the reduced sample (and a new adjustment formula) is believed to have reduced black unemployment estimates and eased worsening poverty figures.

Despite the present Bush Administration’s overall penchant for manipulating data (e.g., Iraq, climate change), it has yet to match its predecessor in economic revisions. In 2002, the administration did, however, for two months fail to publish the Mass Layoff Statistics report, because of its embarrassing nature after the 2001 recession had supposedly ended; it introduced, that same year, an “experimental” new CPI calculation (the C-CPI-U), which shaved another 0.3 percent off the official CPI; and since 2006 it has stopped publishing the M-3 money supply numbers, which captured rising inflationary impetus from bank credit activity. In 2005, Bush proposed, but Congress shunned, a new, narrower historical wage basis for calculating future retiree Social Security benefits.

By late last year, the Gallup Poll reported that public faith in the federal government had sunk below even post-Watergate levels. Whether statistical deceit played any direct role is unclear, but it does seem that citizens have got the right general idea. After forty years of manipulation, more than a few measurements of the U.S. economy have been distorted beyond recognition.

America’s “opacity” crisis

Last year, the word “opacity,” hitherto reserved for Scrabble games, became a mainstay of the financial press. A credit market panic had been triggered by something called collateralized debt obligations (CDOs), which in some cases were too complicated to be fathomed even by experts. The packagers and marketers of CDOs were forced to acknowledge that their hypertechnical securities were fraught with “opacity”—a convenient, ethically and legally judgment-free word for lack of honest labeling. And far from being rare, opacity is commonplace in contemporary finance. Intricacy has become a conduit for deception.

Exotic derivative instruments with alphabet-soup initials command notional values in the hundreds of trillions of dollars, but nobody knows what they are really worth. Some days, half of the trades on major stock exchanges come from so-called black boxes programmed with everything from binomial trees to algorithms; most federal securities regulators couldn’t explain them, much less monitor them.

Transparency is the hallmark of democracy, but we now find ourselves with economic statistics every bit as opaque—and as vulnerable to double- dealing—as a subprime CDO. Of the “big three” statistics, let us start with unemployment. Most of the people tired of looking for work, as mentioned above, are no longer counted in the workforce, though they do still show up in one of the auxiliary unemployment numbers. The BLS has six different regular jobless measurements—U-1, U-2, U-3 (the one routinely cited), U-4, U-5, and U-6. In January 2008, the U-4 to U-6 series produced unemployment numbers ranging from 5.2 percent to 9.0 percent, all above the “official” number. The series nearest to real-world conditions is, not surprisingly, the highest: U-6, which includes part-timers looking for full-time employment as well as other members of the “marginally attached,” a new catchall meaning those not looking for a job but who say they want one. Yet this does not even include the Americans who (as Austan Goolsbee puts it) have been “bought off the unemployment rolls” by government programs such as Social Security disability, whose recipients are classified as outside the labor force.

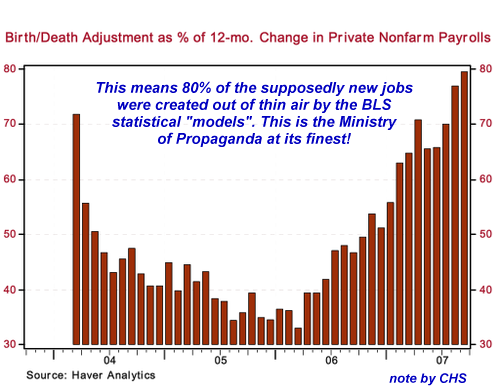

Second is the Gross Domestic Product, which in itself represents something of a fudge: federal economists used the Gross National Product until 1991, when rising U.S. international debt costs made the narrower GDP assessment more palatable. The GDP has been subject to many further fiddles, the most manipulatable of which are the adjustments made for the presumed starting up and ending of businesses (the “birth/death of businesses” equation) and the amounts that the Bureau of Economic Analysis “imputes” to nationwide personal income data (known as phantom income boosters, or imputations; for example, the imputed income from living in one’s own home, or the benefit one receives from a free checking account, or the value of employer-paid health- and life-insurance premiums). During 2007, believe it or not, imputed income accounted for some 15 percent of GDP. John Williams, the economic statistician, is briskly contemptuous of GDP numbers over the past quarter century. “Upward growth biases built into GDP modeling since the early 1980s have rendered this important series nearly worthless,” he wrote in 2004. “[T]he recessions of 1990/1991 and 2001 were much longer and deeper than currently reported [and] lesser downturns in 1986 and 1995 were missed completely.”

Nothing, however, can match the tortured evolution of the third key number, the somewhat misnamed Consumer Price Index. Government economists themselves admit that the revisions during the Clinton years worked to reduce the current inflation figures by more than a percentage point, but the overall distortion has been considerably more severe. Just the 1983 manipulation, which substituted “owner equivalent rent” for home-ownership costs, served to understate or reduce inflation during the recent housing boom by 3 to 4 percentage points. Moreover, since the 1990s, the CPI has been subjected to three other adjustments, all downward and all dubious: product substitution (if flank steak gets too expensive, people are assumed to shift to hamburger, but nobody is assumed to move up to filet mignon), geometric weighting (goods and services in which costs are rising most rapidly get a lower weighting for a presumed reduction in consumption), and, most bizarrely, hedonic adjustment, an unusual computation by which additional quality is attributed to a product or service.

The hedonic adjustment, in particular, is as hard to estimate as it is to take seriously. (That it was launched during the tenure of the Oval Office’s preeminent hedonist, William Jefferson Clinton, only adds to the absurdity.) No small part of the condemnation must lie in the timing. If quality improvements are to be counted, that count should have begun in the 1950s and 1960s, when such products and services as air-conditioning, air travel, and automatic transmissions—and these are just the A’s!—improved consumer satisfaction to a comparable or greater degree than have more recent innovations. That the change was made only in the late Nineties shrieks of politics and opportunism, not integrity of measurement. Most of the time, hedonic adjustment is used to reduce the effective cost of goods, which in turn reduces the stated rate of inflation. Reversing the theory, however, the declining quality of goods or services should adjust effective prices and thereby add to inflation, but that side of the equation generally goes missing. “All in all,” Williams points out, “if you were to peel back changes that were made in the CPI going back to the Carter years, you’d see that the CPI would now be 3.5 percent to 4 percent higher”—meaning that, because of lost CPI increases, Social Security checks would be 70 percent greater than they currently are.

Furthermore, when discussing price pressure, government officials invariably bring up “core” inflation, which excludes precisely the two categories—food and energy—now verging on another 1970s-style price surge. This year we have already seen major U.S. food and grocery companies, among them Kellogg and Kraft, report sharp declines in earnings caused by rising grain and dairy prices. Central banks from Europe to Japan worry that the biggest inflation jumps in ten to fifteen years could get in the way of reducing interest rates to cope with weakening economies. Even the U.S. Labor Department acknowledged that in January, the price of imported goods had increased 13.7 percent compared with a year earlier, the biggest surge since record-keeping began in 1982. From Maine to Australia, from Alaska to the Middle East, a hydra-headed inflation is on the loose, unleashed by the many years of rapid growth in the supply of money from the world’s central banks (not least the U.S. Federal Reserve), as well as by massive public and private debt creation.

The U.S. economy ex-distortion

The real numbers, to most economically minded Americans, would be a face full of cold water. Based on the criteria in place a quarter century ago, today’s U.S. unemployment rate is somewhere between 9 percent and 12 percent; the inflation rate is as high as 7 or even 10 percent; economic growth since the recession of 2001 has been mediocre, despite a huge surge in the wealth and incomes of the superrich, and we are falling back into recession. If what we have been sold in recent years has been delusional “Pollyanna Creep,” what we really need today is a picture of our economy ex-distortion. For what it would reveal is a nation in deep difficulty not just domestically but globally.

Undermeasurement of inflation, in particular, hangs over our heads like a guillotine. To acknowledge it would send interest rates climbing, and thereby would endanger the viability of the massive buildup of public and private debt (from less than $11 trillion in 1987 to $49 trillion last year) that props up the American economy. Moreover, the rising cost of pensions, benefits, borrowing, and interest payments—all indexed or related to inflation—could join with the cost of financial bailouts to overwhelm the federal budget. As inflation and interest rates have been kept artificially suppressed, the United States has been indentured to its volatile financial sector, with its predilection for leverage and risky buccaneering.

Arguably, the unraveling has already begun. As Robert Hardaway, a professor at the University of Denver, pointed out last September, the subprime lending crisis “can be directly traced back to the [1983] BLS decision to exclude the price of housing from the CPI. . . . With the illusion of low inflation inducing lenders to offer 6 percent loans, not only has speculation run rampant on the expectations of ever-rising home prices, but home buyers by the millions have been tricked into buying homes even though they only qualified for the teaser rates.” Were mainstream interest rates to jump into the 7 to 9 percent range—which could happen if inflation were to spur new concern—both Washington and Wall Street would be walking in quicksand. The make-believe economy of the past two decades, with its asset bubbles, massive borrowing, and rampant data distortion, would be in serious jeopardy. The U.S. dollar, off more than 40 percent against the euro since 2002, could slip down an even rockier slope.

The credit markets are fearful, and the financial markets are nervous. If gloom continues, our humbugged nation may truly regret losing sight of history, risk, and common sense.

A narrow focus on monetary policy reflected the realities of the current political structure of the US and was the most promoted by Greenspan's Fed. Some specialists think that it was Greenspan's Fed behavior of recklessly stimulation economy by preserving Fed rate artificially low for too long that caused the current financial crisis. During the period of "Greenspan rule" (and he was probably the second most powerful person in government, definitely he was the most powerful unelected official) we experienced three access bubbles (dot-com, subprime/securitization, and now commodities; the latter reflected the level of distrust accumulated during the previous two). And, naturally, Fed tried to discourage saving by driving rates into negative territory ;-).

Our government is also partially responsible for the misallocation of investment capital by perverse incentives which for the last ten-twenty years encouraged financial speculation and hypertrophy of financial industry simultaneously depressing growth in more important for nation and more sustainable areas. As for dollar, for a nation of net debtors, with much of our debt being held in foreign hands, it does not take a genius to see which way the winds will blow. They can reverse for a year or two in the heat of financial crisis but the general direction is probably irreversible. For significant periods real rates were negative, even in TIPS. And that stimulated excessive risk on all levels. If lenders like mutual funds are literally paying people to take loans (obviously they are not loaning their own money), then fiscal policy gives them a tax write off on top of it.

Quite often, our investment decisions are based on superficial, outdated, manipulated, or simply incomplete understandings of the facts. Understanding margin of error in statistical data is vital to coming up with intelligent investment decisions. Most informed observers have long been wary both of recent economic policy and of the economic data produced by the U.S. government. Palley describes the consequences of the government policy shift initiated by Reagan in the following way:

A second big American interest-rate cut in a fortnight, alongside an economic stimulus plan that united Republicans and Democrats, demonstrates that US policymakers are keen to head off a recession that looks like the likely consequence of rising mortgage defaults and falling home prices. But there is a deeper problem that has been overlooked: the US economy relies upon asset price inflation and rising indebtedness to fuel growth.Therein lies a profound contradiction. On one hand, policy must fuel asset bubbles to keep the economy growing. On the other hand, such bubbles inevitably create financial crises when they eventually implode.

This is a contradiction with global implications. Many countries have relied for growth on US consumer spending and investments in outsourcing to supply those consumers. If America’s bubble economy is now tapped out, global growth will slow sharply. It is not clear that other countries have the will or capacity to develop alternative engines of growth.

America’s economic contradictions are part of a new business cycle that has emerged since 1980. The business cycles of Presidents Ronald Reagan, George H.W. Bush, Bill Clinton, and George W. Bush share strong similarities and are different from pre-1980 cycles. The similarities are large trade deficits, manufacturing job loss, asset price inflation, rising debt-to-income ratios, and detachment of wages from productivity growth.

The new cycle rests on financial booms and cheap imports. Financial booms provide collateral that supports debt-financed spending. Borrowing is also supported by an easing of credit standards and new financial products that increase leverage and widen the range of assets that can be borrowed against. Cheap imports ameliorate the effects of wage stagnation.

This structure contrasts with the pre-1980 business cycle, which rested on wage growth tied to productivity growth and full employment. Wage growth, rather than borrowing and financial booms, fuelled demand growth. That encouraged investment spending, which in turn drove productivity gains and output growth.

The differences between the new and old cycle are starkly revealed in attitudes toward the trade deficit. Previously, trade deficits were viewed as a serious problem, being a leakage of demand that undermined employment and output. Since 1980, trade deficits have been dismissed as the outcome of free-market choices. Moreover, the Federal Reserve has viewed trade deficits as a helpful brake on inflation, while politicians now view them as a way to buy off consumers afflicted by wage stagnation.

The new business cycle also embeds a monetary policy that replaces concern with real wages with a focus on asset prices. Whereas pre-1980 monetary policy tacitly aimed at putting a floor under labor markets to preserve employment and wages, it now tacitly puts a floor under asset prices. This is not a matter of the Fed bailing out investors. Rather, the economy has become so vulnerable to declines in asset prices that the Fed is obliged to intervene to prevent them from inflicting broad damage.

All these features have been present in the current economic expansion. Wages have stagnated despite strong productivity growth, while the trade deficit has set new records. Manufacturing has lost 1.8 million jobs. Prior to 1980, manufacturing employment increased during every expansion and always exceeded the previous peak level. Between 1980 and 2000, manufacturing employment continued to grow in expansions, but each time it failed to recover the previous peak. This time, manufacturing employment has actually fallen during the expansion, something unprecedented in American history.

The essential role of asset inflation has been especially visible as a result of the housing bubble, which also highlights the role of monetary policy. Despite the massive tax cuts of 2001 and the increase in military and security spending, the US experienced a prolonged jobless recovery. That compelled the Fed to keep interest rates at historic lows for an extended period, and rates were raised only gradually because of fears about the recovery’s fragility.

Low interest rates eventually jump-started the expansion through a house price bubble that supported a debt-financed consumer-spending binge and triggered a construction boom. Meanwhile, prolonged low interest rates contributed to a “chase for yield” in the financial sector that resulted in disregard of credit risk.

In this way, the Fed contributed to creating the sub-prime crisis. However, in the Fed’s defense, low interest rates were needed to maintain the expansion. In effect, the new cycle locks the Fed into an unstable stance whereby it must prevent asset price declines to avert recession, yet must also promote asset bubbles to sustain expansions.

So, even if the Fed and US Treasury now manage to stave off recession, what will fuel future growth? With debt burdens elevated and housing prices significantly above levels warranted by their historical relation to income, the business cycle of the last two decades appears exhausted.

It is not enough to deal only with the crisis of the day. Policy must also chart a stable long-term course, which implies the need to reconsider the paradigm of the past 25 years. That means ending trade deficits that drain spending and jobs, and restoring the link between wages and productivity. That way, wage income, not debt and asset price inflation, can again provide the engine of demand growth.

Charles Hugh Smith is one of the most astute observers of this phenomena and we will rely mostly on his insights. His analysis is scattered in several post. The most recent is What Lies Ahead (Part II)

Please forgive this unpardonable pun, but what lies ahead is, well, "lies" ahead.

The sophistry and chicanery behind "official" statistics is truly a wonder to behold. The obfuscation and manipulation has reached such epic proportions that even a financial media that is utterly in thrall to the manufactured illusion of "prosperity" is now timidly questioning some of the more blatant lies. That once-mighty dinosaur, the mainstream media, has even raised itself from its blissful (or shall we say slothful?) torpor to wonder how food and energy can rise by double-digit leaps and bounds while official inflation hums along at a near-zero 2-3%.

Thus we may soon have shantytowns (see photo above) in which the residents will wonder what alternative universe their nation's media inhabits as it continues to spout the officially-massaged "data" that everything is really really fine.

Others with more expertise than myself have picked apart each statistical legerdemain in great detail, but let's just grant the obvious by noting that assuming jobs are being created because more people have been born than have died is a wee bit suspicious.

With this logic, why don't we also just assume that since people are living longer, they are also working longer? Since we can "model" this statistically, why bother actually surveying the populace?

Granted, this is a nation of 300 million people, and accuracy is always statistically ambiguous at the edges of any poll or survey. But why should people who have been unemployed longer than six months be dropped from the ledger? (Let's just call them "discouraged" and no longer count them. It might muss the glowing picture we're painting here to have to include the "discouraged" job seekers.)

Yes, there are reasons for all the adjustments and models, and no doubt those employed to prepare the stats can argue quite passionately for the inadequacies of a simple count. But the point is: who benefits from a rosier-than-reality snapshot? Who has a deep and abiding interest in maintaining the illusion that all is well in an economy staggering down a rocky slope to recession?

Somehow the statisticians never seem to address that question, or the agenda behind the models.

In the other post Charles Hugh Smith noted there is complex Web of deception with numerous players.

The short answer to the above questions is simple; everyone generating huge profits from the debt-based shell-game which is the global economy is desperate to hide the truth from everyone who isn't colluding on the ill-gotten gains.

Let's consider each player and their lies.

1. The Federal Government: the Fed, Treasury, agencies and elected officials. The government is a huge beneficiary of debt-fueled prosperity: tax revenues rise, giving politicians more free candy to spread around to grease the palms of their wealthy contributors and distract the voters with entitlements and other free-spending goodies.

The nightmare scenario for any politician is a shrinking budget. when some budget item has to be cut, then some donor or constituency will be screaming. Not only is this unpleasant, it might cost the politico the next election. much better to lie and keep the debt machine rolling onward and upward.

How does the government deceive us? Let's count the ways.

Employment/Unemployment: Job hunters vanish without a trace after six months, and ghost jobs are created in the hundreds of thousands by a bogus "birth/death" model.

Inflation: As even the mainstream media is now admitting, official inflation is grossly manipulated to appear half of the true rate (3% vs. 6%). This lowers payments to those costly entitlement retirees and maintains the illusion that interest rates can be kept low because inflation is so low.

GDP: The GDP number always comes in "hot" and is usually revised downward later, when nobody's looking.

Federal Deficit: The Federal deficit contains a huge deception: the Social Security surplus is spent to offset current spending, reducing the "official deficit" by hundreds of billions each and every year. In exchange for these trillions, the Government issues the Social Security fund an IOU. The IOU is now about $4 trillion.

If this fiscal legerdemain were outlawed, then the true Federal deficit would be double or triple the "official" deficit.

"A strong dollar is in the interests of the nation." Hahaha... is that why you've engineered a 33% decline in our buying power since 2002 (the dollar index dropped from 120 to 80 in that time and is currently 78.) I'd hate to see what would happen if a weak dollar were in our interests. All these accounting tricks serve one purpose: to deceive the citizenry and the world into believing the U.S. economy is stronger than it actually is.

2. The government has opened the floodgates of money and loosened banking regulations to help all those poor investment bankers. Regulators who should have provided oversight of the lending, mortgage and derivative markets have been idling away their time, doing anything but their job. Who's benefitted? Their pals churning all the origination fees, that's who.

3. The banks sold hundreds of billions in "safe investments" to institutions, domestic and foreign alike. Only now are the true risks and illiquidity of these SIVs, MBS, CDOs, etc. being revealed in the grim light of day.

4. Our trading partners who export vast quantities of goods to the U.S. (and who run stupendous trade deficits with the U.S.) have bought trillions in U.S. debt to keep us afloat. Since Americans don't save anything, somebody has to give them a credit card to fund all that spending.

So what's hidden? How utterly dependent the U.S. is on foreign buyers of Treasuries and debt to keep U.S. interest rates low. That's another little wink-wink, of course; when the Fed slashed the Fed Funds rate a half-a percentage point, headlines blared "Fed Cuts Interest Rate." Meanwhile, back at the Long-Term Interest Rate Ranch, 30-year mortgage rates actually went higher after the Fed's cut. Huh? Yes, that's right--because the market sets the long-term interest rates, not the Fed. Not that you'll ever read much about that, though.

So the "debt junkies" in the U.S. get their "fix" of abundant, low-interest debt from the "pushers" who need the junkie to keep buying exports and oil.

5. Exporters weaken their own currencies to keep goods affordable to the U.S. debt junkies. No matter how low the U.S. dollar sinks, the Japanese Yen and the Chinese Yuan stay at about the same exchange rate. Curious, isn't it? The Euro rises, the Canadian dollar rises, the Swiss Franc rise, but the Yen drops and the Yuan nudges up a couple percent.

The Pushers are happy to keep the cost of their "product" affordable to the hapless debt junkie. Manipulating Forex (foreign exchange) rates and sopping up another trillion in U.S. debt--hey, it's all in a day's work to keep the exporting profits rolling in.

6. The biggest supplier of debt junkies--a.k.a. debt serfs--is the real estate industry. Debt serfs couldn't believe their good fortune: not only were their houses rising in value at a fast clip (a rise fueled by subprime mortgages and "no document" loans), but banks and mortgage brokers were happy to loan them stupendous sums of practically free money on their rising equity to buy more furniture, flat-screen TVs, additions, carpeting, and heck, a second or third "investment property" ( i.e. speculative leveraging to buy more real estate.)

Whoo-hee, it doesn't get any better than HELOC (home equity line of credit) Heaven. And the lenders were happy to keep it all going onward and upward--the origination fees and re-finance fees were in the billions.

As for financial trickery--the real estate industry is a master. Sales figures for new and existing house look great--and then the number of escrows that actually closed is released quietly much later--a much lower number. Listing are "refreshed" so potential buyers won't see the original asking price or how many months the house has been on the market. Buyers were told they could refinance their option-ARM loans into a fixed rate virtually any time they chose to; not true, but so what? The buyer signed and the origination fee was pocketed. Yeah for our team!

7. The key was the astounding creation of new money via lending. OK, you're a bank. You need a paltry 1% cash reserve. So bank $1 million in deposits and you can write $100 million in new loans tomorrow, created right out of thin air.

But what a bother to be limited to a mere 100-fold leverage. So sell that first $100 million to a European bank as an SIV (structured investment vehicle) which puts it off-balance sheet--then write another $100 million in new loans. Rinse and Repeat. Is there any wonder that banks are terrified of the merry-go-round being shut down?

8. All that free cash from newly enriched homeowners spread everywhere: into more real state, SUVs, vacations, and even into the stock market. And since the market never goes down, it's also "safe" to margin your account and buy 50% more stock than you could have with only cash (which was borrowed off your house).

And to maintain the illusion of growing profits, corporations cook their books a la Enron. The game is still being played; liabilities are shunted off the balance sheet, profits are goosed with phony pro-forma numbers and trickery, analysts' estimates are magically exceeded every quarter by a penny, and insiders rake off hundreds of millions in stock option profits while the gullible debt serfs plow their 401K and IRA contributions into the market at the very top, having foolishly believed the insiders' accounting.

9. Investment banks have written hundreds of trillions of stock market derivatives--for nice plump fees, of course. What's the risk? Why, the market is safer now with all these derivatives floating around out there marked to model/myth/back-of-this-envelope.

10. And through it all, the mainstream media--endlessly worried about its own profitability-- soaked up hundreds of millions in advertising revenues from every business benefitting from the debt bubble. Realtors, furniture sales, home improvement stores, you name it--even as ad income from classified employment ads disappeared, these stalwarts of the debt/housing bubble economy were happy to spend millions on print and broadcast ads.

Which explains why the media has been asleep at the wheel until things are so obvious even they can't ignore them any longer. The media discovered the housing bubble a mere 18 months after it broke, and it is now discovering that inflation--I'm shocked, just shocked-- does not reflect reality.

What happens to media revenue and profits when the recession takes down their advertisers? And that's why the media and everyone else has kept all the web of deception under wraps as long as possible--because once the wheels finally fall off, so do their immense profits.

Correspondent Zeus Y. submitted a link and a comment which reveals how the financial deception has been disseminated as propaganda; even as the numbed citizenry are brainwashed into how "prosperous" they are, reality intrudes:

The Karl Roves think they can “create” reality by simply gulling people into believing that what is good for Wall Street is good for everyone, and then bemoan the liberal media for getting people to be “irrationally” pessimistic as they are having to make choices between bread and heat. Man, something here is screwed up and it isn’t the people who are suffering.PAYCHECKS BEING STRETCHED TO THE BREAKING POINT.What used to last four days might last half that long now. Pay the gas bill, but skip breakfast. Eat less for lunch so the kids can have a healthy dinner.Does that sound like "prosperity," "low inflation," a "growing economy," and "a strong dollar" to you? Frequent contributor Michael Goodfellow sent in this disturbing financial fact:Across the nation, Americans are increasingly unable to stretch their dollars to the next payday as they juggle higher rent, food and energy bills. It's starting to affect middle-income working families as well as the poor, and has reached the point of affecting day-to-day calculations of merchants like Wal-Mart Stores Inc., 7-Eleven Inc. and Family Dollar Stores Inc.

Pantries that distribute food to the needy are reporting severe shortages and reduced government funding at the very time that they are seeing a surge of new people seeking their help.

While economists debate whether the country is headed for a recession, some say the financial stress is already the worst since the last downturn at the start of this decade.

From Family Dollar to Wal-Mart, merchants have adjusted their product mix and pricing accordingly. Sales data show a marked and more prolonged drop in spending in the days before shoppers get their paychecks.

An article in yesterday's Financial Times said that, "Only $9.9 billion of home equity loan securitizations have come to market since July 1---A 95% DECLINE FROM THE $200.9 BILLION IN THE FIRST HALF OF THIS YEAR AND A ROUGHLY 92% DECREASE FROM THE SAME PERIOD LAST YEAR."Funny, isn't it, how little notice that stunning contraction received in our media.There is something you can do to stop the financial deception juggernaut. Astute readers Charley R. and Graham M. recommended the petition analyst Karl Denninger has started, Financial Petition. Karl's blog Market Ticker has been listed in my right sidebar for many moons, and Karl is one of my heroes for starting this campaign to end financial deception.

When someone deceives you, it is prudent to ask several questions. Among them:

One of the key questions about current 401K plans is what will happens with inflation and what will happen to the dollar. And the correct answer is that nobody knows. In a world of fiat currencies the reserve currency is the less vulnerable ("exorbitant privilege"). But there are some troubling signs: dollar might fall (or inflation can rise) faster then current 3-5% annual estimate (forget about CPI -- that's a phony number in its own way -- see below). Here is one apt description of the problem (The Deal Bush's budget numbers - Sep. 4, 2007) :

But I have a nasty little secret for you, folks. If you use realistic numbers rather than what I call WAAP - Washington Accepted Accounting Principles - the real federal deficit for the current fiscal year is more than 2-1/2 times the stated deficit.

Why am I inflicting this information on you? Because there's been so much joyous noise about the budget emanating from Washington, despite the subprime mess and market meltdowns (which don't bode particularly well for future tax collections), that my natural contrarianism makes me feel like bombing the buzz machine.

In addition, so many investors (and speculators) are fleeing to the supposed safe haven of Treasury securities lately that it's a good time to take a look at what's really going on with the federal budget.

Welcome to Bailout CityIf a publicly traded corporation tried keeping books the WAAP way rather than the GAAP (Generally Accepted Accounting Principles) way, its auditors would be on the phone to the SEC before you could say "Sarbanes-Oxley."

But this is the federal government, which operates its unique budget accounting system, regardless of which party's running the show. Making the deficit look smaller than it really is helps those in power, be it today's borrow-and-spend crew or yesteryear's tax-and-spenders.

Let me show you how this works, using numbers from the recent update issued by the nonpartisan Congressional Budget Office. (I'm giving you the simplified version to keep your eyes from glazing over. You can find the detailed version in "The numbers" on the right.)

We'll start with Social Security, which will take in about $78 billion more in payroll and income taxes than it shells out. The Treasury takes that cash, gives the trust fund IOUs for it, and spends it. That $78 billion isn't in the stated deficit.

Wait, there's more. The Treasury will fork over $108 billion of interest on the trust fund's $2.2 trillion of Treasurys - but will give the trust fund IOUs, not cash. They won't count in the deficit either. Add that $186 billion to the stated budget deficit, and it more than doubles, to $344 billion.

The stated deficit, you see, measures how much less cash Uncle Sam takes in than he spends. That's fine for gauging the deficit's impact on the economy, which is what budget experts generally do. But if you're trying to assess Uncle Sam's overall fiscal condition, as I am, you should count those IOUs in the deficit because they have to be paid someday.

Now, let's move on. We end up with a total deficit of more than $400 billion by undoing another piece of WAAP ledger-demain: the $97 billion increase in Treasury securities held by "other government accounts," such as federal employee pension funds.

Thanks to the magic of Washington math, that doesn't increase the deficit, even though it increases the government's overall debt. Don't you wish you could keep books this way at home?

I worry that the happy news may produce unhappy long-term results by making politicians even less inclined than usual to inflict pain on voters by raising taxes or trimming future benefits to keep entitlements from overwhelming the public fisc.

Budget office Director Peter Orszag warns that at their current growth rate, Medicare and Medicaid will devour 20 percent of our gross domestic product in 2050 - more than today's entire federal budget. Yech!

So even though the deficit's smaller than it was and financial markets (for now) love Treasury securities, don't take next month's budget numbers at face value. If you do, you're setting yourself up to be WAAPed.

From GDP to unemployment and, especially, CPI government statistics is lightly or seriously flawed. So flawed that this is visible to a non-professional observer. Some troubling figures are overstated. For example trade deficit with China is calculated simplistically and is grossly overstated. If for example iPod is exported to the USA it is assumed that $150 is added to the current deficit. But Chinese made part in iPod are minority: most are from Japan and Korea. It might well be only $50 of Chinese origin in the cost of the product.

As an another example, much of the spectacular rise in corporate profits in recent years (and drop of R/E ratio for S&P 500 and other indexes) might be attributable to falling investment (and therefore lower depreciation), severe cuts in labor costs (layoffs that politically correctly are called "rising productivity") as well as sharply reduced by Bush administration corporate taxes and extremely low interest rates. Despite this huge stimulus the quality of profits last several years were very low in "investment-speak" but few people dare to discuss it.

All-in-all most government statistics has problems and looks like firmly on the way achieving the reliability of the USSR government statistics. Nobody believes productivity numbers published so in this particular sense the level of the USSR statistics was already reached. Few seriously consider reliable such metrics as inflation (core inflation is by-and-large a "paper tiger" if you use Chinese's cliché), job growth and GDP growth but for different reasons. We will discuss the following topics:

The declining participation in work force also means that actual unemployment

rate is higher and might well be above 5%.

That does not means that other statistical measures are perfect. Recently the accuracy of productivity gains calculations was questioned by Business Week. The key issue here that you can not take them as face value and base your decision on them without understanding the level of accuracy, possible bias and shortcomings of each measure. Unfortunately this "homework" is not done.

There is a special term rarely use in connection with financial statistics but that is perfectly applicable. It is called Occult statistics. Here is how Skeptic dictionary defines the term:

Occult statistics are statistics used as the handmaiden of occult theorizing, in much the same way that philosophy was used by theology during medieval times, viz., to justify beliefs in supernatural beings and occult forces.

Parapsychologists, astrologers, theologians, and others who seek anomalies to guide them to transpersonal wisdom and insight into the true nature of the universe, are now able to use computers to do extremely complex statistical analyses of monumental masses of data. When they find a statistically significant correlation between or among variables, they are extremely impressed and consider the discovery to be proof of the occult or the supernatural. To the occult statistician there is no such thing as a spurious correlation.

For example, William Dembski's The Design Inference: Eliminating Chance through Small Probabilities is said to "provide a mathematical foundation for the types of statistical inferences parapsychologists use to identify paranormal phenomena. In particular, the book shows how to deal with statistical experiments whose p-values are extremely small (like those that regularly come up in parapsychology experiments). This work is clearly relevant to Carl Jung's idea of synchronicity. [It] promises to put synchronicity on a solid scientific footing" (Rabi Gupta, personal correspondence).

Likewise, The Princeton Engineering Anomalies Research program led by Robert Jahn, Dean of the School of Engineering and Applied Science, claims that in their experiments where human operators try to use their minds to influence a variety of mechanical, optical, acoustical, and fluid devices, they have gotten results that can't be due to chance and "can only be attributed to the influence of the human operators."

Legions of parapsychologists, led by such generals as Gary Schwartz and Dean Radin, have also appealed to statistical anomalies as proof of ESP. Statistician Jessica Utts of the University of California at Davis gave her imprimatur to U.S. government studies of ESP and remote viewing. Many occultists have claimed that certain dreams must be clairvoyant and cannot be explained by coincidence because they defy the laws of probability.

It was not long ago that astrologers were claiming that Gauquelin had found the Holy Grail with his statistics showing the so-called "Mars effect." More recently, millionaire playboy Gunter Sachs published Die Akte Astrologie, which uses data analyzed by professors of statistics at the University of Munich to prove astrology is true.

Obviously, this list could go on and on, and could include the Bible Code and various proofs of the existence of God on the grounds of improbability that chance could explain the nature of the universe or some complex aspect of it such as the genetic code.

Skeptics unimpressed by occult stats

Skeptics are unimpressed with arguments that assert improbabilities for what has already happened. Whatever has already happened is obviously not an impossible event. Accurately calculating the odds of either the genetic code or the universe occurring by "chance," i.e., by natural laws alone without the design of a divine being, is impossible. Analogies to a monkey typing up Hamlet by chance, or to a Mona Lisa being "created" by nature, are irrelevant and notably without impact on skeptics.

Skeptics are not very impressed by statistical anomalies generated by those in quest of occult forces. Sometimes parapsychological colleagues have discovered that statistics were generated by fraudulent means, e.g., the work of Walter J. Levy at Rhine's Institute of Parapsychology (Williams 191, 319). The history of ESP research is a paradigm of dishonesty and incompetence (Rawcliffe, Randi), though it should be mentioned that the two major incidents of fraud (Levy and that of S. G. Soal), though suspected by skeptics, were uncovered and reported on by true believers. Skeptics have noted many times while investigating the statistical claims of paranormal researchers that there are often significant problems with subjective validation, confirmation bias, optional starting and stopping, the clustering illusion, the regressive fallacy, etc.

Sometimes the variables being correlated are ambiguous or vaguely defined, if defined at all, so that practically anything can count in support of the occult hypothesis. What is a "great" athlete or a "rebel"? Sometimes the methods of finding patterns are deceptive and inappropriate, e.g., finding hidden messages in texts. As John Ruscio notes, "If you look in a fantastic number of places, and count anything that you stumble upon as supportive evidence, you are guaranteed to discover meaning where none exists" (45).

Skeptics have noted that many times something seems to be statistically improbable when, in fact, it is not improbable at all. Some spurious correlations are due to lack of clarity regarding the variables; others are due to incorrect calculation of the odds. Both errors are common occurrences regarding so-called clairvoyant dreams.

Finally, skeptics are unimpressed with artificially evoked statistical anomalies because such anomalies are expected to occur with some frequency given the vast number of trials that are made.

Correlating just a couple dozen variables with one another will produce a matrix containing nearly 300 correlation coefficients. By convention, results that occur at a level expected by chance just 5 percent of the time are called "statistically significant." We can therefore expect about fifteen spuriously significant correlations within every matrix of 300 (Ruscio, 45).

Each of those spurious correlations is a temptation to see causal connections where there are none and to engage in post hoc theorizing to explain non-existent mysterious forces.

See also Bible Code, clustering illusion, confirmation bias, ESP, Forer effect, law of really large numbers, Mars effect, numerology, optional starting and stopping, post hoc fallacy, regressive fallacy, remote viewing, and selective thinking.

Society

Groupthink : Two Party System as Polyarchy : Corruption of Regulators : Bureaucracies : Understanding Micromanagers and Control Freaks : Toxic Managers : Harvard Mafia : Diplomatic Communication : Surviving a Bad Performance Review : Insufficient Retirement Funds as Immanent Problem of Neoliberal Regime : PseudoScience : Who Rules America : Neoliberalism : The Iron Law of Oligarchy : Libertarian Philosophy

Quotes

War and Peace : Skeptical Finance : John Kenneth Galbraith :Talleyrand : Oscar Wilde : Otto Von Bismarck : Keynes : George Carlin : Skeptics : Propaganda : SE quotes : Language Design and Programming Quotes : Random IT-related quotes : Somerset Maugham : Marcus Aurelius : Kurt Vonnegut : Eric Hoffer : Winston Churchill : Napoleon Bonaparte : Ambrose Bierce : Bernard Shaw : Mark Twain Quotes

Bulletin:

Vol 25, No.12 (December, 2013) Rational Fools vs. Efficient Crooks The efficient markets hypothesis : Political Skeptic Bulletin, 2013 : Unemployment Bulletin, 2010 : Vol 23, No.10 (October, 2011) An observation about corporate security departments : Slightly Skeptical Euromaydan Chronicles, June 2014 : Greenspan legacy bulletin, 2008 : Vol 25, No.10 (October, 2013) Cryptolocker Trojan (Win32/Crilock.A) : Vol 25, No.08 (August, 2013) Cloud providers as intelligence collection hubs : Financial Humor Bulletin, 2010 : Inequality Bulletin, 2009 : Financial Humor Bulletin, 2008 : Copyleft Problems Bulletin, 2004 : Financial Humor Bulletin, 2011 : Energy Bulletin, 2010 : Malware Protection Bulletin, 2010 : Vol 26, No.1 (January, 2013) Object-Oriented Cult : Political Skeptic Bulletin, 2011 : Vol 23, No.11 (November, 2011) Softpanorama classification of sysadmin horror stories : Vol 25, No.05 (May, 2013) Corporate bullshit as a communication method : Vol 25, No.06 (June, 2013) A Note on the Relationship of Brooks Law and Conway Law

History:

Fifty glorious years (1950-2000): the triumph of the US computer engineering : Donald Knuth : TAoCP and its Influence of Computer Science : Richard Stallman : Linus Torvalds : Larry Wall : John K. Ousterhout : CTSS : Multix OS Unix History : Unix shell history : VI editor : History of pipes concept : Solaris : MS DOS : Programming Languages History : PL/1 : Simula 67 : C : History of GCC development : Scripting Languages : Perl history : OS History : Mail : DNS : SSH : CPU Instruction Sets : SPARC systems 1987-2006 : Norton Commander : Norton Utilities : Norton Ghost : Frontpage history : Malware Defense History : GNU Screen : OSS early history

Classic books:

The Peter Principle : Parkinson Law : 1984 : The Mythical Man-Month : How to Solve It by George Polya : The Art of Computer Programming : The Elements of Programming Style : The Unix Hater’s Handbook : The Jargon file : The True Believer : Programming Pearls : The Good Soldier Svejk : The Power Elite

Most popular humor pages:

Manifest of the Softpanorama IT Slacker Society : Ten Commandments of the IT Slackers Society : Computer Humor Collection : BSD Logo Story : The Cuckoo's Egg : IT Slang : C++ Humor : ARE YOU A BBS ADDICT? : The Perl Purity Test : Object oriented programmers of all nations : Financial Humor : Financial Humor Bulletin, 2008 : Financial Humor Bulletin, 2010 : The Most Comprehensive Collection of Editor-related Humor : Programming Language Humor : Goldman Sachs related humor : Greenspan humor : C Humor : Scripting Humor : Real Programmers Humor : Web Humor : GPL-related Humor : OFM Humor : Politically Incorrect Humor : IDS Humor : "Linux Sucks" Humor : Russian Musical Humor : Best Russian Programmer Humor : Microsoft plans to buy Catholic Church : Richard Stallman Related Humor : Admin Humor : Perl-related Humor : Linus Torvalds Related humor : PseudoScience Related Humor : Networking Humor : Shell Humor : Financial Humor Bulletin, 2011 : Financial Humor Bulletin, 2012 : Financial Humor Bulletin, 2013 : Java Humor : Software Engineering Humor : Sun Solaris Related Humor : Education Humor : IBM Humor : Assembler-related Humor : VIM Humor : Computer Viruses Humor : Bright tomorrow is rescheduled to a day after tomorrow : Classic Computer Humor

The Last but not Least Technology is dominated by two types of people: those who understand what they do not manage and those who manage what they do not understand ~Archibald Putt. Ph.D

Copyright © 1996-2021 by Softpanorama Society. www.softpanorama.org was initially created as a service to the (now defunct) UN Sustainable Development Networking Programme (SDNP) without any remuneration. This document is an industrial compilation designed and created exclusively for educational use and is distributed under the Softpanorama Content License. Original materials copyright belong to respective owners. Quotes are made for educational purposes only in compliance with the fair use doctrine.

FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to advance understanding of computer science, IT technology, economic, scientific, and social issues. We believe this constitutes a 'fair use' of any such copyrighted material as provided by section 107 of the US Copyright Law according to which such material can be distributed without profit exclusively for research and educational purposes.

This is a Spartan WHYFF (We Help You For Free) site written by people for whom English is not a native language. Grammar and spelling errors should be expected. The site contain some broken links as it develops like a living tree...

|

|

You can use PayPal to to buy a cup of coffee for authors of this site |

Disclaimer:

The statements, views and opinions presented on this web page are those of the author (or referenced source) and are not endorsed by, nor do they necessarily reflect, the opinions of the Softpanorama society. We do not warrant the correctness of the information provided or its fitness for any purpose. The site uses AdSense so you need to be aware of Google privacy policy. You you do not want to be tracked by Google please disable Javascript for this site. This site is perfectly usable without Javascript.

Last modified: March 29, 2020