|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

| Economics of Peak Energy | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 |

|

|

Switchboard | ||||

| Latest | |||||

| Past week | |||||

| Past month | |||||

|

|

The Oil Drum

Black_Dog on November 19, 2012

I think the EIA has been playing fast and loose with the petroleum statistics. As noted last week, the EIA Annual Review for 2010 states that the US produced a total of 9,443 mbbls/d, of which US crude production at 5,512 mbbls/day (which includes lease condensate), NGPL's at 2,001 mbbls/d and processing gain of 1,064 mbbls/d. The difference of 866 mbbls/d appears to be made up by biofuels.

Total product supplied is said to have been 19,148 mbbls/d, with imports minus exports totaling 9,434 mbbls/d of that. The amount of crude imported was 9,163 mbbls/d. From these data, the total crude supplied to the refineries was 14,675 mbbls/d, of which 62% is imported.

I've previously suggested that assigning all the processing gains to US production is factually incorrect, instead the processing gains resulting from refining imported crude should be added to the total for imports. For a rough guess, using the fraction of crude imported given above, 664 mbbls/d should be subtracted from the US production and added to the import side of the accounting. This revision reduces US production to 8,779 mbbls/d and increases imports to 10,098 mbbls/d, increasing the fraction imported from 49% to 53%.

Of course, the EIA misses the whole discussion about biofuels, especially ethanol, which require a large input of fossil fuels to produce the final product. The EIA ignores this fuel input, showing biofuels as an input to the front end of the refining process. With ethanol production now using about 40% of the US corn crop, it would be more accurate to consider this portion of the US agricultural system to have been added to the energy supply system and the energy used would thus become an internal consumption which would be subtracted from the petroleum energy available to the rest of society. Doing this calculation would increase the fraction of energy imported, which would give a more realistic picture of our situation...

E. Swanson

carnot on November 22, 2012

Sorry Guys but you have missed the point on refinery gains. It is a mirage. Remember the 1st law of thermodynamics.

Energy cannot be created or destroyed. US refiners continue to quote their refining capacities and products in barrels - a unit of volume which is meaningless unless a density unit is also quoted. What you should consider is the mass unit. In ALL refineries if you measure in units of mass it should add up to 100% plus the mass of hydrogen and other inputs added which increase the mass. ( methanol for an MTBE unit for instance).

When the crude is distiller in the crude unit it will produce a number of products with different densities and therefore different mass per barrel. Measure the products in barrels and you will have the following barrels per tonne.

Butane. 11

Naphtha 9

Gasoline 8.7

Jet 8

Diesel 7.5

Vacuum gas oil 6.8

Fuel oil 6.5In a cat cracker, with no hydrogen addition the mass of products is constant but because the volume of LESS dense light products exceed the total volume of HEAVY dense products , hey presto there is a refinery gain - in volume but not in mass.

Some refinery gain is due to the addition of hydrogen but typically this is 2-3% of the overall mass flow. Refiners love to sell in units of volume as they can benefit form the sleight of hand of selling a less dense and lower energy product to unsuspecting drivers. When energy density is compared in mass units there is NO significant difference between gasoline, jet or diesel. It is about 42-44 MJ per Kg but very different in volume units.

That is why diesels appear 30 % more fuel efficient on volumetric terms but in reality the differnce is much less.

December 7, 2012

This is the final installment of the tour of global crude + condensate + natural gas liquids (C+C+NGL) production data as published by the International Energy Agency (IEA) and deals with the rest of the world. OPEC and OECD production was described in earlier posts.

After many decades of growth, Chinese oil production appears to have stalled in 2012 at just over 4 million bpd. It remains to be seen if this is a temporary glitch or whether this heralds peak and decline in Chinese oil production.

Russia + Former Soviet Union (FSU) production has been on a plateau for 3 years at just below 14 million bpd. Russian production continues to grow slowly offset by declines in other FSU states.

Oil production in Oman peaked at 960,000 bpd in 2001 and declined steadily to around 700,000 bpd in 2008. An aggressive program of enhanced oil recovery (EOR) has turned things around and production has risen by over 200,000 bpd in the last 4 years and Omani production is challenging the 2001 highs. There are profound lessons to be learned here about the potential impact of EOR on heavy oil fields and future global production.

Columbia has also seen a reversal of fortune with new field developments reversing declines and new production highs just under 1 million bpd have been set in recent months.

Figure 1 Oil production has been largely flat in South and East Asia over the decade, rising slowly from 2002 to 2011 and since then in gentle decline. Production in China and India has been rising offset by declining production in Indonesia and Malaysia. All data published in this interim report are taken from the monthly IEA Oil Market Reports.

From May 2007 to August 2010, Rembrandt Koppelaar published an e-report called Oil Watch Monthly that summarised global and national oil production and consumption data from the International Energy Agency (IEA) of the OECD and Energy Information Agency (EIA) of the USA. This is the fourth in a series of new Oil Watch reports, co-authored with Rembrandt and details crude oil production data for the Rest of The World as reported by the International Energy Agency. Earlier editions:

Oil Watch - World Total Liquids Production

Oil Watch - OPEC Crude Oil Production (IEA)

Oil Watch - OECD Oil Production (IEA)

US domestic oil production has jumped by 18 per cent in the past year as the shale boom has expanded, and in the first eight months of this year oil imports were 800,000 barrels a day fewer than a year earlier. America's oil exports rose over the same time by 300,000 barrels a day, so net imports have fallen in just one year by 1.1 million barrels a day, or about 6 per cent of total consumption. If that pace if sustained the International Energy Agency's prediction of self sufficiency for the US by 2030 will prove to be conservative.Oil production from shale in the US is rising much more strongly than expected because the boom itself is working to shift production into liquids. The shale contains a mix of gas and liquids including oil, and enough gas has been discovered to produce a structural downshift in the price of US domestic gas, which by law cannot be exported.

Companies that have bought into the shale boom, including BHP Billiton, have reacted by pulling drilling rigs out of fields that are gas-rich and relocating them in ones that are rich in liquids that take a price that is roughly four times higher, pushing US shale oil and liquids production up. It is now running at about a million barrels a day, and is predicted to reach about 3.5 million barrels a day by 2016 (OPEC collectively exports more than 30 million barrels a day at over $100.)

Jesse's Café Américain

24 October 2012

"All war is based on deception. Of all those close to the commander, none is more intimate than the secret agent; of all rewards none more liberal than those given to secret agents; of all matters none is more confidential than those relating to secret operations."

Sun Tzu

"Let Hercules himself do what he may,

The cat will mew, and dog will have his day."William Shakespeare, Hamlet

There is a currency war underway.

The international trade clearing mechanisms are tottering. Countries are using their economic power, their banks and currencies, as a part of overall foreign as well as domestic policy.

This is a huge source of the tensions and problems which are are seeing both economically and militarily in the world today.

The current trade system based on the US dollar reserve currency is not sustainable. It has had a good long run, but like the euro it has reached the end of its rope. The US cannot continue to print enough money and increase its debt balance through trade any further. See Triffin Dilemma. Yes I am familiar with Eichengreen's counter argument.

And I am also aware of the already written and vetted proposals for a 'single world currency' with independent local governments, an arrangement which is even more fallacious and ill founded than the euro. Yes I know that there could be a series of agreements that could kick this down the road five or ten years. But something has got to give. The charade is getting a bit thin but the deception must go on.

I still think the only tenable solution, if one still wishes to cling to the notion of 'free trade' internationally, is an SDR based on a wider basket of currencies with a gold and silver component. And I am of the opinion as you know that much of these international theatrics and sword hammering is just the 'negotiations' phase with regard to the composition of the new SDR, and the ownership of its maintenance.

There are some who would treat the dollar as an arm of the military strategy, but that becomes a bit dramatic, in the Dr. Strangelove sense, but is nevertheless a good source of Defense Department consulting fees for those who promote the idea.

And I would hope that it goes without saying that the currency war is intimately tied in with the oil/energy situation, via the petrodollar. If you are going to send your country into multiple preemptive wars, one might take the time to understand the reasons why they are doing it. It is about the oil, and the positioning for it.

The problem is that there is no mechanism in place to bring the disputing parties together for an expedient resolution, given their conflicting interests. And those interests run deep, particularly for the Anglo-American banking cartel in NY and London. The dollar is the basis of their power.

And so we are locked in a 'currency war,' a resolution of differences in interest by other, less destructive, means than war itself. After all, nine-tenths of diplomacy is economic, if money is power.

If this notion is alien to you, then one can sympathize, because it is like watching an opera in a foreign tongue without a libretto to help you to understand the action on the stage. To have such knowledge of the basic plotline might not only help your understanding, it could be good for your investment portfolio. For in this currency war, your accounts and your savings are cannon fodder.

If you wish to read one pivotal post on the subject read the first part of this: Currency Wars

If you click on the label 'currency wars' at the bottom of this post, it will bring up all the other posts here that touch on that subject, some admittedly only tangentially.

I think the currency war will intensify quite a bit before it resolves. I have been tracking this since 1999. It is the reason I first became interested in gold. I went looking for something like it, and only gold really fit, and to a lesser extent silver.

Gold and silver are intimately involved in the unfolding currency war, because they take no sides, and have no counterparty risk. No one can print them. And this is why I think GATA is right, not because of the evidence they have, which is more substantial than one might suspect given obsessive secrecy and the disinformation campaigns, but because it is exactly what one would do if there was to be a currency war, and such things as gold and silver existed. It is basic strategy of war: seek to control the high ground. And along with oil, gold and silver are strategic high ground in a currency war. And the first victim in a war is the truth.

If one does not understand these things, and the scope of what is happening with the dollar and the euro, then the significance of the important things that are happening will be missed and dismissed. People will connect the dots that they see and draw their pictures accordingly and they will be wrong. And what is particularly Machiavellian is that some of that is being done by intent.

And even with all sorts of technical trading knowledge, one will be in the dark, literally be fighting 'the last war,' in their understanding of what is happening in the world as it is today.

August 2012

"To put it crudely, the US wants to inflate the rest of the world, while the latter is trying to deflate the US. The US must win, since it has infinite ammunition: there is no limit to the dollars the Federal Reserve can create.

What needs to be discussed is the terms of the world's surrender: the needed changes in nominal exchange rates and domestic policies around the world."

Martin Wolf, Financial Times, 12 Oct 2010

"...the Treasury secretary, who has primary authority on economic and financial issues in the cabinet, should be at every meeting to advise on how economic and security issues intersect, and to ensure that the United States is using its economic and financial strength in the most effective way."

Robert Kimmitt, NY Times, 23 July 2012

Looks like the US is getting ready to flex its financial muscle. I don't think the Anglo-American banking cartel will relinquish the dollar reserve currency supremacy easily. This is currency war.

I somehow missed this editorial when it first came out. But over the weekend and today I heard echoes of the same sentiment from various places in what looks like a loosely organized public relations campaign.

The National Security Council, formed in 1947 and comprised of the President, Vice-President, Secretary of State, Secretary of Defense, Director of the CIA, and the Joint Chiefs of Staff.

The National Security Council has an unmistakable military flavor.

The move to add the Treasury Secretary as a permanent member is just another sign of the currency wars heating up. At least from the US perspective, there is an unmistakable convergence between military and economic action.

As I have noted before, the language used often suggests that the US considers its TBTF's to be a modern form of financial battleship, able to move key markets at will to support official policy. And the credit rating agencies are like agile destroyers.

I think this will become very interesting.

NY Times

Give Treasury Its Proper Role on the National Security Council

By Robert M. Kimmitt

July 23, 2012THE National Security Act of 1947, which created the National Security Council, the Defense Department, the Joint Chiefs of Staff and the Central Intelligence Agency, turns 65 on Thursday. But it's not ready for retirement; it needs, instead, to be rejuvenated by making the Treasury secretary a statutory member of the National Security Council, rather than an invited attendee.

The act and the organizations it created performed well during the cold war, the post-cold-war decade and the period after 9/11. But they need to be updated to recognize the close connection between security and economic issues as we look forward from the global financial crisis of the last few years. The concept of national security has broadened considerably since the N.S.C.'s early decades, elevating economic and financial issues to crucial elements to our nation's security, alongside the traditional diplomatic and military issues. Diplomatic and military issues are still important, of course. Iran, Syria and North Korea make that clear. But the growth areas in national security policy are economic and financial.

During the cold war, the German chancellor, Helmut Kohl, knew with precision the throw-weights of American nuclear weapons based in Germany; today, Chancellor Angela Merkel has to know with equal precision the spreads on Spanish and Italian sovereign debt.

It may seem odd that the Treasury secretary would have been left off the list of statutory members of the National Security Council by the generation of American leaders who helped lay the groundwork for Western Europe's postwar revival with the Bretton Woods conference and the Marshall Plan. But at the time, military, diplomatic and economic policies were seen as largely separate tracks. And as the cold war deepened, the military challenge from the Soviet Union assumed overwhelming importance.

This is where the National Security Act has not kept pace. The statutory members of the National Security Council are still the president, vice president, secretary of state and secretary of defense, with the chairman of the Joint Chiefs of Staff and the director of national intelligence as statutory advisers. This is a good, but incomplete, team. Even though the Obama White House says that Treasury Secretary Timothy F. Geithner is a regular attendee, along with the statutory members, it is now time to add the secretary of the Treasury to the list of statutory members. That would ensure that the economic and financial dimensions of national security challenges are given equal weight in council deliberations, now and into the future...

There are, of course, other officials integral to international economic and financial success, like the secretary of commerce and the United States trade representative. They should still be invited to N.S.C. meetings. But the Treasury secretary, who has primary authority on economic and financial issues in the cabinet, should be at every meeting to advise on how economic and security issues intersect, and to ensure that the United States is using its economic and financial strength in the most effective way.

Read the entire editorial here.

October 24, 2012 | Jesse's Café Américain

The FOMC announcement was nothing new as expected.

If the Fed acts again I think it will be as a result of some crisis or event, and will be done with a better rationale. Bernanke is primarily supporting the big banks with the Fed's activities, and not much of his balance sheet expansion is flowing through to the real economy for a number of reasons, and I think by intent.

This is how the Fed is avoiding the problem of a general monetary inflation. The inflation the US is seeing is largely secular and structural.

Governments and economists around the world have not figured out that what the world economy is suffering from, to varying degrees, is "high-priced fuel syndrome".

High-priced fuel syndrome has a number of symptoms:

- Slow economic growth, or contraction

- People in discretionary industries laid off from work

- High unemployment rates

- Debt defaults (or huge government intervention to prevent debt defaults)

- Governments in increasingly poor financial condition

- Declining home and business property values

- Rising food prices

- Lower tolerance for immigrants

- Huge difficulty in funding retirement programs, programs for disabled, and regular pension plans

- Rising international tensions related to energy supply

Seeking Alpha

The following interview was conducted by James Stafford and originally published on Oilprice.com. It is reproduced here with permission.

Oilprice.com: Access to cheap energy is vital to economic growth. What do you see happening with the economy over the coming years as the time of cheap oil comes to an end?

Ed Dolan: In my view it is a myth that cheap energy--"affordable energy" as many people like to say--is vital to growth. The idea that there is a lockstep relationship between growth of GDP and use of energy is widespread, but the data simply does not bear it out. Instead, what they show is that the world's best-performing economies have become dramatically more energy efficient over time.

The World Bank uses constant-dollar GDP per kg of oil equivalent as an energy efficiency metric. From 1980 to 2010, the high-income countries in the OECD have increased their average energy efficiency by 55 percent. The United States has done a little better than that, increasing its energy efficiency by 81 percent over that period. That's pretty remarkable, considering that we haven't really had a policy environment that is supportive of efficiency.

Think what we could do if we did.

Even after the efficiency gains in efficiency we have made, we still have a long way to go. The U.S. economy is still 15 percent less energy efficient than the average for high-income OECD countries, giving it plenty of room to improve. Switzerland is almost twice as energy-efficient as the U.S., and the UK is 68 percent more efficient.

Some people say that the only reason the United States has been able to grow while using less energy is the deindustrialization of its economy, outsourcing heavy industry to China. However, compare the U.S. with Germany. Germany is an export powerhouse and Europe's best-performing economy, yet its energy efficiency has increased at almost the same rate over the last 30 years as the United States, an 80 percent gain in efficiency compared to 81 percent. Furthermore, despite being proportionately more industrialized than the U.S. and a major exporter, Germany squeezes out 41 percent more GDP from each kg of oil equivalent.

In short, we don't have to hypothesize about the possibility of someday breaking the lockstep relationship of growth and energy use-we and most of the rest of the advanced world are already doing it.

Oilprice.com: What effect can you see America's Oil & Gas boom having on foreign policy?

Ed Dolan: On the whole, I see it as beneficial. Energy dependence has led us to buy a lot of oil from countries that are unstable and/or unfriendly to us. Anything we can do to reduce that dependence gives our foreign policy more room to maneuver. The beneficial effects reach beyond our actual imports and exports. The U.S. gas revolution is having repercussions all the way to Russia, where Gazprom is seeing its market power undermined, and Russia, as a result, is losing some of the geopolitical leverage its pipeline network has given it.

Oilprice.com: From Siberia and Poland to China and Qatar - the shale revolution has politicians salivating at the thought of a cheap and abundant source of energy. But can the results seen in the U.S. be easily replicated in other parts of the world?

Ed Dolan: I think you're going to have to ask someone with more engineering background for the technical details, but from what I read, the answer is that it won't always be easy. It is my understanding that some countries where shale seemed just recently to have great promise have already encountered disappointments in practical exploratory work. Poland I think is an example. Furthermore, the environmentalist opposition to fracking seems even stronger in many European countries than in the United States.

Still, I am hoping that the shale revolution will pan out in at least some countries. Think how much difference it would make, say, to Ukraine's foreign policy if they were able to break their dependence on Russian gas.

Oilprice.com: Gail Tverberg has written a recent article suggesting the world is suffering from high-priced fuel syndrome, which has the following symptoms:

- Slow economic growth, or contraction

- People in discretionary industries laid off from work

- High unemployment rates

- Debt defaults (or huge government intervention to prevent debt defaults)

- Governments in increasingly poor financial condition

- Declining home and business property values

- Rising food prices

- Lower tolerance for immigrants

- Huge difficulty in funding retirement programs, programs for disabled, and regular pension plans

- Rising international tensions related to energy supply

Do you think this is too convenient and an oversimplification of the problems facing world economies at the moment? What would you blame for the plethora of economic woes being experienced at the moment?

Ed Dolan: I don't buy the argument at all. Yes, when countries are hit by unexpected upward shocks in fuel prices, we do see short-run results like slower growth and layoffs, but those are short-term problems. When the proper structural adjustments are made, countries with high fuel prices manage to achieve strong growth and full employment.

Where are fuel prices lowest? If you look up the data and rank countries by retail fuel prices, you find the low-price end of the rankings crowded with countries like Egypt, Cambodia, Iran, Pakistan-not exactly economies we would like to emulate.

We've got big economic problems, but a lot of them don't have much to do with energy. What about a healthcare system that delivers mediocre results at the world's highest cost? Health care isn't all that much energy driven.

What about our steady move down the international rankings in education-are you going to blame that on the high cost of heating classrooms? Hardly.

Oilprice.com: Oil prices have been near to the $100 a barrel mark for some time now, and don't look likely to drop back to previous low levels. What effect could this increased price have on oil importing economies compared to oil exporting economies?

Ed Dolan: Clearly, any oil price increase has the short-term effect of transferring wealth from using countries to producing countries. However, the long-run effects are what matter.

In the long run, high prices just accelerate the trend for using countries to become more efficient and less dependent. Meanwhile, the producing countries often don't manage their oil riches well. They fall victim to the "curse of riches." The curse takes the form partly of a loss of competitiveness in their non-energy sectors (the so-called "Dutch disease"). Partly it takes the form of corruption of their political systems. Russia is a poster child for both aspects of the curse of riches.

Oilprice.com: Renewable energy is more expensive than fossil fuels, so how can people be persuaded to choose the less economical option of renewables over the likes of coal and natural gas?

Ed Dolan: There is only one right way to promote renewables, and that is to introduce full-cost pricing of all forms of energy. Full-cost pricing is a two-part program.

First, it means pricing that covers the full production costs for every form of fuel. No subsidies for anyone-not for oil, not for ethanol, not for wind or solar.

The second half of full-cost pricing is to include all of the nonmarket costs, what economists call the "external costs" or "externalities." The most publicized of these are pollution costs, whether those take the form of local smog, oil spills, climate change, or bird kills. Some people, I am one of them, would like to count in something for the national security costs of dependence on unfriendly and unstable foreign sources of energy supply.

Full-cost pricing accomplishes two things. First, it levels the playing field so that each form of energy competes on its economic merits, not whether corn-growing states have early primaries or oil companies have big SuperPacs. Second, by raising prices to consumers to a realistic level, it accelerates the trend toward energy efficiency that is already underway.

Subsidies for renewables are just plain wrong, even if you look at them from a hard-core environmentalist point of view. With a subsidy, on the one hand, you say, "produce more green energy" and other the other hand, you turn around and tell the consumer, "waste more green energy." We don't want to waste energy from wind or solar any more than we want to waste oil and gas. We shouldn't forget that even the greenest renewables can have significant environmental impacts.

The whole "affordable energy" idea is based on the myth that if we don't include those external costs in the price-the pollution costs, the national security costs-they just go away. They don't. Keeping prices artificially low just transfers those costs to someone else, someone unlucky enough to live downwind, someone who owns beachfront property that gets eroded away as the sea level rises, someone who has to go off to fight a war to keep the shipping routes open. There are two things wrong that. First, it's immoral. If we believe in the market economy, the rule of law, and all that, we have to respect people's property rights and their human rights. Second, it's inefficient. It doesn't strengthen our economy, it weakens it. If there's one thing we can't afford, it's "affordable energy."

Oilprice.com: Obama has made clear his desires to cut the $4 billion a year tax breaks given to oil companies. What affect do you believe this would this have on the U.S. economy and the U.S. oil industry?

Ed Dolan: If it is done as part of a comprehensive move toward full-cost pricing, it could only strengthen the U.S. economy. The oil industry would whine, but if we cut subsidies and tax breaks for competing energy sources at the same time, oil will remain a competitive part of the energy mix for many years to come.

Oilprice.com: The oil industry has enjoyed decades of subsidies and grants, so do you think it is unreasonable to already start cutting the subsidies to renewable energies and expect them to survive on their own?

Ed Dolan: As I explained above, the answer is yes, provided it is done as part of a package that reforms our energy policy as a whole in the direction of full-cost pricing.

Oilprice.com: Economic growth is generally dependent on the access to energy. As the supply of energy grows, so too does the economy (more or less). Global oil supplies are pretty much stagnant, so do you predict that only nations that successfully convert to a renewable energy mix with an abundant supply of cheap energy will be able to experience continued economic growth at a similar level experienced by the developed countries of recent years?

Ed Dolan: Again, I just don't buy the doctrine that growth is dependent on ever-increasing energy use. For sure, those countries that pursue sound policies, like full-cost pricing to rationalize their energy mix and promote efficiency, are the ones that are going to keep growing.

Oilprice.com: As the arctic ice melts at a rapid pace the world's superpowers are jockeying for position to exploit the region's vast oil & gas & mineral deposits. Environmental groups are rightly concerned, but is this a resource that we cannot afford to ignore?

Ed Dolan: Arctic oil, like any other source of energy, should pay full freight for any environmental impacts it has. If it can bear those costs and still be competitive, I think it should be in the mix. I am worried about Russia, though. It has a dangerous combination of an environment-be-damned attitude and low technical competence that could lead to headline-grabbing disaster worse than the Gulf blowout or Exxon Valdez.

Oilprice.com: What effect do you see the shale revolution having on investments in renewable energy?

Ed Dolan: If I were trying to make money by generating electricity with wind or solar, I'd be worried about gas. I don't have all the relevant numbers at my disposal, but my gut feeling is that even if you price in full environmental costs for wind, solar, and gas-including environmental costs associated with fracking-gas is still going to be pretty competitive.

Oilprice.com: What are your views on Ben Bernanke's QE3?

Ed Dolan: I've written repeatedly about QE over at Economonitor, so I am on record as saying we should try it. The trouble is, QE is not a magic bullet. Properly executed and properly communicated, it can help support the recovery, but it can't do it alone.

That is one point where I agree 110 percent with Ben Bernanke. Here is what he said in a speech at the Fed's Jackson Hole conference at the end of the summer:

It is critical that fiscal policymakers put in place a credible plan that sets the federal budget on a sustainable trajectory in the medium and longer runs. . . Monetary policy cannot achieve by itself what a broader and more balanced set of economic policies might achieve.

Oilprice.com: How do you see the EU solving its debt crisis?

Ed Dolan: I'm afraid I'm a euro pessimist. The U.S. debt situation is hard enough to resolve, but Europe's is worse. At the same time, whatever you say about gridlock in Washington, our political decision making is a model of streamlined efficiency compared with the EU.

Oilprice.com: Do you think the EU was doomed to fail from the start with the format that it has? Could more success be seen in a split EU, with the northern/richer nations using one currency, and the southern/poorer nations using a different currency?

Ed Dolan: Doomed, I don't know, but flawed, certainly. Just recently, I was looking back at what economists were writing about the prospects for the euro back in the early 1990s, when it was still just a project. They were telling us, for one thing, that Europe is too diverse to be ideal for a currency union-and that was when there were only 15 EU countries. Second, they said that you can't run a monetary union without a central government, a fiscal union, and a banking union. You still don't have any of those.

I am not sold on the idea of a northern euro and a southern euro. If the currency union doesn't work, it doesn't work. Break it up. Sure, some countries will find it works for their special circumstances to tie their currencies to a large, stable neighbor. I could see the Danes or the Latvians keeping a link to the German currency, for example, and I'm sure the Vatican will continue to use whatever currency Italy uses. But a formal, north-south divide doesn't make much sense to me.

Oilprice.com: In terms of tackling the current economic situation in the U.S., of the two main presidential candidates, who do you suggest is the best man, and why?

Ed Dolan: I do not think we can tackle the current economic situation without a thorough-going fiscal policy reform that includes three key elements: Spending cuts, revenue increases, and a rewrite of the whole tax system to eliminate loopholes and cut marginal rates. Furthermore, the package can't be heavily front-loaded like George Osborne's austerity program in the UK, which has sent their economy back into recession. Ours should be back-loaded, with an element of stimulus now and an ironclad commitment to move the budget toward surplus as the economy improves. It's a lot to ask for.

We are not going to get good budget policy out of the GOP unless members of that party make a clean break with mantra that they will not accept a dime of new revenue, not even if it comes from eliminating the most loathsome tax loopholes. Personally, I am never going to vote for a candidate for President, the Senate, the House, or any office who has signed that nonsensical Grover Norquist tax pledge.

At the same time, I have been very disappointed at the lukewarm support Obama has given to the kind of program I would like to see. During the first debate, Romney said that when Obama didn't "grab" Simpson-Bowles-that was his word, and a good one-it was a failure of leadership. That was one point where I agreed with Mitt.

Then, you also have to take into account the vote for Congress. I'm afraid there is going to be continued gridlock as long as the GOP controls the House. In the Senate, there are at least a few people in both parties who are willing to meet behind the scenes and talk compromise, but not in the House, not right now, anyway. Maybe what we need in the White House is someone who is a real politician, a negotiator and dealmaker in the mold of a Clinton or an LBJ. Instead, we have the choice between a manager and a law professor. I'm not optimistic that either of them will be able to do what needs to be done.

June 03, 2011 | Information Clearing House

Finance is a form of warfare. Like military conquest, its aim is to gain control of land, public infrastructure, and to impose tribute. This involves dictating laws to its subjects, and concentrating social as well as economic planning in centralized hands. This is what now is being done by financial means, without the cost to the aggressor of fielding an army. But the economies under attacked may be devastated as deeply by financial stringency as by military attack when it comes to demographic shrinkage, shortened life spans, emigration and capital flight.

This attack is being mounted not by nation states as such, but by a cosmopolitan financial class. Finance always has been cosmopolitan more than nationalistic – and always has sought to impose its priorities and lawmaking power over those of parliamentary democracies.

Like any monopoly or vested interest, the financial strategy seeks to block government power to regulate or tax it. From the financial vantage point, the ideal function of government is to enhance and protect finance capital and "the miracle of compound interest" that keeps fortunes multiplying exponentially, faster than the economy can grow, until they eat into the economic substance and do to the economy what predatory creditors and rentiers did to the Roman Empire.

mmckinl

Another brilliant essay by Michael Hudson …

Having no recourse in the third world at neoliberalism the banksters have turned on their own territories. The failure of the Doha round of trade talks spells the end of the bankster financial Ponzi Scheme. Third world countries now know well this game of neoliberal conquest.

The "elephant in the room" is peak oil and peak food production. Without these and other resources growing the end game is clear … private bank fractional reserve banking will inevitably implode. The banksters are well aware of their fate and will steal, loot and pillage as fast as they can ..

Unfortunately the only path ahead for the banksters is war. This is the only remedy to reshuffle the world economy and financial system to make them viable once more, until of course their Ponzi Scheme inevitable implodes again. The stakes couldn't be higher …

The end of economic growth as we know it has eluded Hudson, at least from what I've read of his work. The Hirsch Report circa 2005 spells out in detail the problems associated with peak oil. It was vehemently ignored … and removed for a time from the USG website. Just recently Jeremy Grantham produced a report on peak resources …

The Hirsch Report

http://www.netl.doe.gov/publications/others/pdf/o...Time to wake up: "Days of abundant resources and falling prices are over forever" by Jeremy Grantham

http://www.energybulletin.net/stories/2011-04-29/...The "end game" is here my friends … an "end game" unlike any other in history …

Emanon :

Let me state it very simply : "the borrower [debtor] is SERVANT to the lender". The whole point of creating debtors is to gain control of and rule over them. Prof. Hudson's article illustrates this admirably.

kate

The World Central Bank: The Bank for International Settlements

"...The BIS is the most obscure arm of the Bretton-Woods International Financial architecture but its role is central. John Maynard Keynes wanted it closed down as it was used to launder money for the Nazis in World War II. Run by an inner elite representing the world's major central banks it controls most of the transferable money in the world. It uses that money to draw national governments into debt for the IMF..." http://www.bilderberg.org/bis.htm

Reader

Small wonder today... The usurers' dictatorship started conquering the world decades ago. The entire EU was founded upon their "market" crap once promoted by sick brains like Milton Friedman.

sijepuis

Excellent summary by Hudson. Although I'm becoming increasingly weary of the "we are here" [ie, the antechamber of hell] approach to problems, which leaves out suggestions for concrete action.

If Michael Hudson, William Black, Nomi Prins and Mike Whitney are physicians, they're doing little more than monitoring the patient's failing vital signs: blood pressure, blood count, heart rate, etc, when the vampire that's proceeding to drain their patient dry is right there in front of them.

While clearly pedagogy is very important, in order that as many people as possible grasp what is happening, and why, if there are no accompanying suggestions for practical action, from the likes of Hudson, et co, a sense of helplessness will grow at the rate of the compound interest/ financialization that's killing us.

There are bloggers galore who are actively advocating hunkering down, buying stores of 'survival' goods: preserved food, medicines, toilet paper, tobacco, and the like, which may be a good idea in any case, but this is little more than a stop-gap measure, an admission of defeat. - And while mass strikes and demonstrations may be cathartic, they take a deep bite out of the real economy and ironically become an invitation to the IMF and increased austerity measures! [cf Egypt and Greece].

David Malone, author of the Golem XIV blog who, although not trained as an economist, has been doing a superb job of revealing the sources of European debt, laying bare the treachery of EC/ECB policies and proposing possible solutions.

See this, for example: Ireland was Germany's off-shore tart, wherein Deutsche Bank established subsidiaries in Ireland, in order to benefit from lax financial regulation, which eventually failed. DB has slipped away, leaving the Irish taxpayer with the bill.

In the following, Malone explores the idea of cross cancellation of European debt:How to destroy the web of Debt.

Excerpt: "Among the 'debtor' nations a Debt Jubilee means Ireland reduces its debt load to from 130% of GDP to under 20%! That would virtually wipe out the crippling cuts being forced upon the Irish. While even among the 'Creditor' nations France benefits by nearly eliminating its debt. So the French people too would benefit. Which does beg the question - who is benefiting by enforcing all the debts? I'll give you one guess".

Mutually agreed cancellation of what amounts to incestuous debt, in a first step towards the elimination of the 'vampire'.

September 26, 2012Jim Hamilton on what determines prices in oil markets:

...The Wall Street Journal carried this account last week:

Oil prices dropped more than $3 in less than a minute late in the trading day on Monday, just as trading volume spiked. The move also dragged down prices of gold, copper and even the euro.

"Traders were looking like deer in the headlights," said Peter Donovan, a floor trader... "I called four different desks, and they all said, 'we don't know.' " ...

The move sparked talk of an erroneous trade-called a "fat-finger" error in industry parlance-or a computer algorithm gone awry.

Fat finger or no, there was an even bigger drop on Wednesday...

Those who doubt that oil prices are determined solely by fundamentals would naturally ask, what aspect of the supply or demand for oil could have possibly changed in the course of less than a minute last Monday? The obvious and correct answer is, there was no change in either the supply or the demand for physical oil over the course of that minute. The minute-by-minute price of a NYMEX contract is determined by how many people are wanting to buy that financial contract and at what price, not by how much gasoline motorists burned in their cars that minute. But since changes in the price of crude oil are the key determinant of the price consumers pay for gasoline, doesn't that establish pretty clearly that the whims or fat fingers of financial traders are ultimately determining the price we all pay at the pump?In one sense, the answer to that question is yes-- last week's decline in the price of crude oil will soon show up as a lower price Americans pay for gasoline. But here's the problem you run into if you try to carry that theory too far. There are at the end of this chain real people who burn real gasoline when they drive real cars. And how much gasoline they burn depends in part on the price they pay-- with a higher price, some people use a little bit less. Not a lot less-- the price of gasoline could change quite a lot and it would take some time before you could be sure you see a response in the data. That small (and often sluggish) response is why the price of oil can and does move quite a bit on a minute-by-minute basis, seemingly driven by forces having nothing to do with the final users of the product.But if the price of oil that emerges from that process turns out to be one at which the quantity of the physical product that is consumed is a different amount from the physical quantity produced, something has to give. Indeed, the bigger price drops we saw on Wednesday followed news that U.S. inventories of crude were significantly higher than expected ...reason:

"Indeed, the bigger price drops we saw on Wednesday followed news that U.S. inventories of crude were significantly higher than expected ..."

So doesn't it stink of insider trading?

Paine:

Hamilton is an energy industry pimp

Paul krugman is the real cautionHe wants to believe in way higher crude prices because he's green

Lots of nice friends of the planet types see the crude price gouging as a renigade pigou tax

Evil gains for the greater good

anne said in reply to Paine...

Darryl FKA Ron said...Lots of nice friends of the planet types see the crude price gouging as a renegade Pigou tax *

Evil gains for the greater good

* http://en.wikipedia.org/wiki/Pigovian_tax

A Pigouvian tax is a tax applied to a market activity that generates negative external outcomes.

[An important criticism.]

You could write a book on all the commodities futures trading scams that manipulate market prices. Oh wait! Somebody did.http://www.businessweek.com/magazine/content/11_09/b4217086779050.htm

The Asylum:

The Renegades Who Hijacked

the World's Oil Market

By Leah McGrath Goodman

Morrow, 398pp, $27.99Anyone who accuses New York Mercantile Exchange (CME) traders of being greedy and lawless anarchists who blow up markets obviously was not working the floor in 1978. In that year a sign at the entrance decreed: Please check your guns at the desk. "A gunshot never went off on the floor," claims John Tafaro, a trader at the time. "That's where we drew the line." He says traders were pretty dutiful about checking their guns, too.

The rest of the rules, though, they ignored, skirted, or subverted, sometimes with brazen crudity, sometimes through deft manipulation of the law-at least according to Leah McGrath Goodman's The Asylum: The Renegades Who Hijacked the World's Oil Market. "Any customer who traded there was molested, if not raped," says one ex-regulator with the U.S. Commodity Futures Trading Commission, speaking metaphorically, one hopes. "As far as we could see, the NYMEX traders did nothing but run scams."

They weren't always oil traders. They only stumbled upon oil futures after screwing up Maine potato futures. A whole industry had been built around predicting the Maine potato harvest, and - more importantly - trying to manipulate it. However, the market was closed by regulators in 1976, after defaults on deliveries of more than 50 million pounds of potatoes.

Casting about for something else to trade, then-Chairman Michel Marks tried to boost futures in boneless beef and plywood. After that didn't work, in 1978, he introduced heating oil futures. The market proved a gusher that led to 30 years of good times. Booming with the oil scares of the late '70s and early '80s, heating oil futures begat natural gas futures and became a huge market revolving around the price of West Texas Intermediate Crude, now the benchmark for a barrel of oil.

The years trading potatoes help explain why the NYMEX was able to trade oil for so long without worrying about meaningful oversight. Formed to offer hedges for farmers, the futures exchanges are under the purview of the same people who produce the omnibus farm bills: the House Agriculture Committee, which also runs the regulator in the business, the CFTC. In Goodman's account, the CFTC issued more exemptions than rules and, in any case, only enforced the latter gingerly.

The first big exemption, allowing large trades for a financial participant, went to Goldman Sachs (GS) in 1991. Others soon piled in.

... ... ...

Darryl FKA Ron:

Of course market fundamentals matter and traders can lose as well as win if they place their bets in the wrong direction. The question is whether spot markets can be successfully manipulated or not and they can. There can also be unsuccessful attempts, similar to speculators trying to corner the gold market (e.g., Black Friday 1869).

spencer:

Fundamentals determine the underlying trend of oil and commodity prices, but at the margin traders and speculators drive the short term price moves.

Market assumed that QE 3 would drive the dollar down and commodities and oil higher so they bid the price of oil up.

But they soon decided that with Europe in recession, Asian growth slowing and US petroleum imports contracting the demand fundamentals were a little different now than under the earlier QE. So you got a market reversal driven by traders and speculators.

The fundamentals probably say oil should be in a $80 to $100 trading range with cost too high for oil to go below $80 and demand too weak for it to go above $100.

The marginal cost of new oil is in $80 to $100 range. Moreover, the economic structure of the oil industry is changing. Historically, oil was a very unusual market where virtually all the costs were fixed or sunk costs. But with the tar sands and fracking now the marginal source of oil this structure is changing and variable costs are starting to become important.

Under the traditional fixed cost model short run price swing did not really impact supply. But now with the industry experiencing high variable cost short run price swing are having an impact on supply.

First last year and again this year when the price fell below $80 we started to see some marginal source of oil withdrawing from the market.

anne:

President Obama has for months been doing all that can be done short of waging war to limit the flow of oil from Iran which is among the prime producers, nonetheless the pretense is that limiting the supply of oil internationally, when the President decides on such a policy, has no relevance to price.

anne:

What strikes me as increasingly interesting, is how much about American foreign policy that affects us in differing ways, such as the price of oil, is simply turned away from by analysts possibly because discussion of our foreign policy from differing perspectives can seem too risky.

sherparick:

from the blog http://www.lawyersgunsmoneyblog.com/

"It's probably not uncommon for City traders to wonder how they burnt so much cash during a drunken night on the town.

But Steve Perkins was left with a bigger black hole in his memory than most when his employer rang one morning to ask what he'd done with $520m of the oil trading firm's money.

It was 7.45am on June 30 last year when the senior, longstanding broker for PVM Oil Futures was contacted by an admin clerk querying why he'd bought 7m barrels of crude in the middle of the night.

The 34-year old broker at first claimed he had spent the night trading alongside a client. But the story began to fall apart when he refused to put the customer in touch with his desk for official approval of the trades.

By 10am it emerged that Mr Perkins had single-handedly moved the global price of oil to an eight-month high during a "drunken blackout". Prices leapt by more than $1.50 a barrel in under half an hour at around 2am – the kind of sharp swing caused by events of geo-political significance. Ten times the usual volume of futures contracts changed hands in just one hour.

….

The investigation also shows that he was able to trade huge volumes with very little cash up front and no position limit, exposing how it easy it was for a single British broker on a bender to cause chaos in the oil market."

I guess you are right in the long term, but the short term, not so much.

Mcwop:

A market controlled and manipulated by a cartel? No it does not always operate on fundamentals. However, increased demand does bolster the cartel's ability to raise prices. And investment/speculative demand also has an effect.

The price is falling now because we are heading to a global slowdown. Speculators/investors will be running away from oil is my guess.

B said...

All markets fluctuate - forever - until the market itself fails. There is no equilibrium. This is proven. That fact is what George Soros used to make his money, by applying his non-mathematical insight of reflexivity based on Karl Popper.

Mathematically, reflexivity is chaos theory. It is an iterated, unknown function showing stability within limits.

What is astonishing is that anyone in the 21st century still believes in equilibrium market theory. There is no such thing. It cannot exist.

Michael Pettengill:

"But since changes in the price of crude oil are the key determinant of the price consumers pay for gasoline, doesn't that establish pretty clearly that the whims or fat fingers of financial traders are ultimately determining the price we all pay at the pump?"

But very little of the oil refined trades as contracts on the commodity exchanges. What consumers are willing to pay for gasoline determines the price of gasoline, unless Saudi Arabia is engaged in a market share war against competitors breaking the OPEC price setting.

Obama policy to Iran serves the Saudi intention to keep prices at $100 well, offsetting the higher CAFE standards. When global economic growth strengthens, the Saudis might want resolution of Iran and other regional conflicts to keep long term prices from rising much beyond $100. $150 for 5 years would drive so serious changes in the energy mix, plus spur uneconomic oil production, threatening a rerun of 1985-1998.

Main Street Muse:

Is the headline a joke? When was the last time "fundamentals" determined the price of oil?

The "market" seems highly distorted by the hysteria of traders.

efh:

Who are funded by cheap money from Central Banks.

John Cummings said in reply to efh...

Except no cheap money is coming from central banks. All from BRIC man. Now that is drying up.

September 23, 2012

Fat fingers and the price of oil

Can the wild swings in the price of oil over the last few weeks have anything to do with supply and demand?The Wall Street Journal carried this account last week:

Oil prices dropped more than $3 in less than a minute late in the trading day on Monday, just as trading volume spiked. The move also dragged down prices of gold, copper and even the euro.

"Traders were looking like deer in the headlights," said Peter Donovan, a floor trader at Vantage Trading on the New York Mercantile Exchange. "I called four different desks, and they all said, 'we don't know.' "

The move came at about 1:54 p.m. EDT. West Texas Intermediate crude for October delivery plummeted to $94.83 a barrel on the Nymex, from more than $98. Some 12,500 contracts changed hands in a minute, compared with less than 500 a minute previously.

The move sparked talk of an erroneous trade-called a "fat-finger" error in industry parlance-or a computer algorithm gone awry.

Fat finger or no, there was an even bigger drop on Wednesday, leaving the price of West Texas Intermediate well below where it had been prior to Fed Chair Ben Bernanke's Jackson Hole speech on August 31 and the Fed's announcement of QE3 on September 13.

Those who doubt that oil prices are determined solely by fundamentals would naturally ask, what aspect of the supply or demand for oil could have possibly changed in the course of less than a minute last Monday? The obvious and correct answer is, there was no change in either the supply or the demand for physical oil over the course of that minute. The minute-by-minute price of a NYMEX contract is determined by how many people are wanting to buy that financial contract and at what price, not by how much gasoline motorists burned in their cars that minute. But since changes in the price of crude oil are the key determinant of the price consumers pay for gasoline, doesn't that establish pretty clearly that the whims or fat fingers of financial traders are ultimately determining the price we all pay at the pump?

In one sense, the answer to that question is yes-- last week's decline in the price of crude oil will soon show up as a lower price Americans pay for gasoline. But here's the problem you run into if you try to carry that theory too far. There are at the end of this chain real people who burn real gasoline when they drive real cars. And how much gasoline they burn depends in part on the price they pay-- with a higher price, some people use a little bit less. Not a lot less-- the price of gasoline could change quite a lot and it would take some time before you could be sure you see a response in the data. That small (and often sluggish) response is why the price of oil can and does move quite a bit on a minute-by-minute basis, seemingly driven by forces having nothing to do with the final users of the product.

But if the price of oil that emerges from that process turns out to be one at which the quantity of the physical product that is consumed is a different amount from the physical quantity produced, something has to give. Indeed, the bigger price drops we saw on Wednesday followed news that U.S. inventories of crude were significantly higher than expected:

Oil dropped to a one-month low after U.S. crude inventories surged the most since March as production and imports rebounded from Hurricane Isaac.

Futures decreased as much as 3.3 percent after the Energy Department said supplies rose 8.53 million barrels last week, more than eight times what was projected in a Bloomberg survey. Imports arrived at the highest rate since January and output rose. Crude fell before the report on speculation Saudi Arabia is moving to reduce prices.

There are several channels by which QE3 may end up influencing the quantity of oil physically produced and consumed. A lower value for the U.S. dollar would mean a greater quantity demanded worldwide at a given dollar price of oil. A higher level of economic activity (the ultimate goal of QE3) would also boost demand for the physical product. And lower real interest rates may make it profitable to store more oil physically, leaving less available for the ultimate users of the product. So I would have expected QE3 overall to be one factor that could contribute to a higher dollar price for oil.

But any investors who have been assuming that QE3 will boost the price of oil for no reason other than the fact that other traders expect it to raise the price of oil may find themselves tripping painfully over the fat finger of reality.

Jul 17, 2012 | www.energypulse.net

Saudi Arabia is once again the biggest producer of oil in the world, surpassing Russia to regain its title. Saudi Arabia happens to be one of the most repressive and undemocratic regimes in the world. The Economist magazine ranked Saudi Arabia 161st out of 167 countries in their most recent Democracy Index.

The Saudis also have massive economic and demographic problems to deal with, including a pending peak and rapid decline in oil exports. You heard right: Saudi Arabia, the world's largest producer of oil, is facing a peak in its oil exports and a rapid decline thereafter.

There are solutions, however, to these very large problems, which I'll discuss further below.

Saudi Arabia's national oil company, Saudi Aramco, pumped about 11.5 million barrels per day for the last year, up from about 9.5 in early 2009. The Saudis are pumping more oil now than they have in decades, along with the rest of OPEC, which is at a 23-year high for combined oil production.

Russia held the top spot for oil production for a couple of years but Saudi Arabia came roaring back since 2010. The U.S. is a distant third place with about 6 million barrels per day.

Net oil exports, are, however, a very different picture. The U.S. is famously the world's biggest importer of oil. While our production of oil has taken an unusual upward tick in the last couple of years, spurred by record high prices, and our consumption of oil has declined even further due to increased energy efficiency, conservation and a still-struggling economy, we still import about half of the oil we consume: a massive 9 million barrels of oil per day.

Saudi Arabia exports about 8 million barrels per day (mbpd from now on), with Russia not too far behind at about 7 mbpd.

So far, this is all fairly familiar data. However, what is not well-known is the degree to which Saudi Arabia's massive oil exports are threatened by its demographics and a probable decline in its aging supergiant oil fields.

A new report from the UK's Chatham House examines this problem in detail. They conclude that Saudi Arabia's oil exports will peak around 2020 and, under current policies, decline to zero by 2038. You read that right: decline to zero. This decline will occur due to the dramatic growth in consumption by Saudi Arabia's rapidly growing population and increases in per capita energy consumption. Saudi domestic consumption of oil is growing at about 7% per year, which leads to a doubling of consumption in just ten years.

Now, 2038 is a long time away, in normal circumstances. But oil politics operates in decadal timespans, not normal timespans. 2038 is, in oil terms, not that far away, so if Chatham House's projections are accurate, we've got a major problem on our hands.

What will the world do if fully 10% of global oil production, and 20% of global net oil exports, is consumed by the Saudis rather than exported?

Saudi Arabia's governmental revenue will come under extreme pressure if net oil exports decline. The Saudis rely on oil revenue for fully 80% of their budget. Many things will have to give if oil exports do dry up. Net oil exports declined fairly dramatically from 2005 to 2010, as Figure 1 shows, but have risen back in the last couple of years. Chatham projects net exports will rise to about 9 mbpd by 2020, and then start a precipitous decline as the Saudis' demographic time bomb explodes.

Saudi Arabia's problem is not, of course, unique to Saudi Arabia. It is a global problem that afflicts many countries. Jeffrey Brown and Samuel Foucher have developed an "Export Land Model" to predict how the global net oil export situation will unfold in coming years. They found that the top five exporters of oil (Saudi Arabia, Russia, Iran, United Arab Emirates and Norway) decline from about 24 mbpd in 2008 to about 7.5 in 2020 and go to almost zero by 2030. Global net oil exports are about 40 mbpd, so these producers comprise more than half of the global export market.

Trend lines in Figure 1 were fitted to time periods based on oil supply growth patterns (described later in this post), because limited oil supply seems to be one critical factor in real GDP growth. It is important to note that over time, each fitted trend line shows less growth. For example, the earliest fitted period shows average growth of 4.7% per year, and the most recent fitted period shows 1.3% average growth.

In this post we will examine evidence regarding declining economic growth and discuss additional reasons why such a long-term decline in real GDP might be expected.

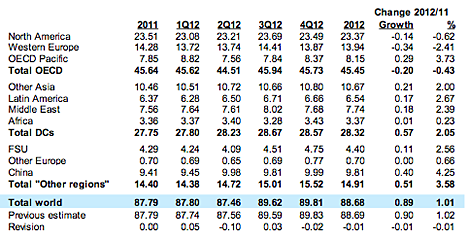

Overall, OPEC sees demand staying below 90 mbd over the remainder of this year, with total growth in demand lying at 1.01 mbd.

Nevertheless, after putting all this together, I re-iterate my conclusion from last time in that I doubt KSA will increase production much above 10 mbd (in June it was producing 9.888 or 10.103 mbd depending on source, and with the rising internal demands (domestic use in the Middle East is now projected to average 7.7 mbd in 2012) world markets will get tighter in the shorter, rather than the longer term.

Darwinian

FrugalDave, thanks for a fantastic article. You make the same point I have been trying to make for years now. And that is that Saudi has been able to offset declines in their old fields by bringing on new fields and with horizontal wells and in some cases MRC wells.

But these new additions are required to offset the decline in existing fields, which have been somewhat protected from the severity of declining well production by the switch from vertical to maximum reservoir contact (MRC) wells.

But when the water hits those horizontal wells the decline is likely to be swift and sudden. However with Manifa coming on line we may not see the decline hit with any impact until late in this decade. But we are all waiting with abated breath.

Ron P.

ROCKMANNote that they defined the reserve as the total amount of extractable oil, not the amount left to recover; they have done that in later computations also, and the latest annual report uses 259.7 billion barrels as that discovered reserveThis explains why Middle East reserves always go up, even after several 100 billion barrels have been extracted. The problem with this type of reserve definition is that the rest of the world defines reserves as the amount of oil that hasn't yet been extracted. Yet the IEA, EIA, BP, and even OPEC themselves do not take this discrepancy into consideration when reporting world reserves. All these organizations should deduct the amount Middle East oil already produced from their reserve estimates. But are they going to do this? If not, why not?jj – "Is it possible that the MRC wells are increasing the percentage of OOIP that is recovered?" Not only possible but likely. But impossible to estimate without much more detailed data than the KSA releases. In additional to probably having a longer commercial life than a vertical they'll have a better "sweep": the effective drainage radius. But there's the potential to be too optimistic of the gain based upon the higher flow rate. As pointed out the new hz wells won't show a significant increase in water production (indicating not much life left) until very late in the game. Though a different reservoir dynamic this is the same phenomenon we've see in Mexico's Cantrell FieldjjhmanExtend field life for years? Since we don't have the data to make that call I can only offer a WAG: no. Not only not add years but perhaps reduce life. These wells might recover some additional URR but they will produce what is recoverable much faster. IOW recover more oil but do it faster than the vert wells alone would have done.

Thanks, Rock, for the usually cogent reply but isn't " These wells might recover some additional URR but they will produce what is recoverable much faster." a choice? They can, and do, choose how fast they produce each resevoir.DarwinianI'm always impressed by the sophistication of the Saudi resource management and use of technology. Within the constraints of ELM (per Westexas)Saudi Arabia seems to be managing their output quite sensibly. It seems possible that they might keep their production rates down rather than use these capabilities to produce at the maximum possible rate.

As a congenital doomer I am constantly suprised at the resilience of BAU. After reading "Twilight in the Dessert" I expected KSA to have been in serious trouble by now, but they aren't and I now suspect they are much smarter than Matt Simmons gave them credit for.

ROCKMANisn't " These wells might recover some additional URR but they will produce what is recoverable much faster." a choice?JJ, the very purpose of these new horizontal wells is to produce the oil much faster, to stem the decline rate. Had they not needed this oil much faster than they were getting it, they would not have spent the billions required to get it out faster. Saudi Arabia's Strategic Energy InitiativeWithout "maintain potential" drilling to make up for production, Saudi oil fields would have a natural decline rate of a hypothetical 8%. As Saudi Aramco has an extensive drilling program with a budget running in the billions of dollars, this decline is mitigated to a number close to 2%.As Dave (Heading Out) points out above Saudi has been able to offset the decline of older fields by bringing on new production from Haradh, Shaybah and Khrais. They still have Manifa yet to come on line.No one has suggested that the Saudis were dumb, they know exactly what they are doing. They have kept their peak production, over the years, at between 9 and 10 mb/d with gaps in between where they cut production back substantially. Right now they are, in my opinion, producing flat out. Manifa will likely keep them able to produce at this level for a few more years before they start to decline. But the rest of OPEC may start to decline well before that.

Ron P.

Tony - Very true especially for carbonate (limestone) reservoirs. I don't know the details of this reservoir but in general semi-isolated pockets of oil can easily be distributed throughout the field. But there's the $64,000 question: better URR but at a faster rate so which wins the footrace? Perhaps the closer spacing recovers 10% more oil but at a 15% greater rate so the field depletes sooner as a result. Or maybe reverse those numbers.I've always heard the KSA had some of the best Swiss engineers with some of the most powerful computers managing their fields.

But decisions about withdrawl rates are controlled by different factors. And such decisions are not always made to the benefit of URR. I'm about to work on a project where the previous operator produced 5 oil wells at too fast a rate for the sake of cash flow. He destroyed all 5 completions prematurely and lost all cash flow so he can't afford to fix the problem.

If for no other reason than ELM I suspect the KSA may sacrifice URR for cash flow in the future. Perhaps even more so if prices stay lower long enough.

See also

From NOAA:

The United States reported its warmest spring since records began in 1895,...

... with 31 states in the eastern two-thirds of the country observing record warmth. The national temperature was 2.9°C (5.2°F) above its long-term average, surpassing the previous record by 1.1°C (2.0°F).

The globally-averaged temperature across land and oceans for the first five months of 2012 was the 11th warmest January–May o >

rj sigmundquoting my hyperlinked mailing from this morning:

the early summer heat wave with its accompanying record high temperatures that we mentioned last week lifted in the east this past week, but it continues in the plains states & eastern rockies; as we expected, the first six months of this year are now in the record books as the hottest ever for the continental US; in addition, the 12 months ending June 30th also ranks as the hottest 12 month stretch in history, as June temperatures came in at an average 71.2°F for the contiguous 48 states, which was 2.0°F above the 100 year average...the more significant weather story, however, continues to be the worsening drought over the south and the important agricultural states, which has become severe enough for the US Dept of Agriculture to declare to declare a federal disaster area in more than 1,000 counties over 26 states, the largest agricultural disaster ever declared due to drought; the drought declaration covers almost every state in the southern half of the US, from s.carolina to california, with parts of Colorado, Wyoming. Illinois, Indiana, Kansas and Nebraska also included... according to the weather service's drought monitor, 61% of the US was listed as being in drought this week, up from the 56% of last week's report....corn crops in particular have been hard hit; the USDA cut its corn crop forecast by 12%, from 166 bu/acre to 146 bu/acre this week, as corn growing regions in illinois and indiana in particular are experiencing drought conditions of "severe" and "extreme" intensity, as you can see in dark orange and red on the adjacent map, a larger 12 week animation of which will be embedded below...with higher corn prices making refineries unprofitable, ethanol output fell to its lowest in 2 years...the USDA also cut its yield forecast for the soybean crop nearly 8%, to 40.5 bushels per acre from 43.9 bushels per acre...this will likely translate into higher prices for variety of foods from cereals to soft drinks and cooking oil, as well as for meat, dairy & poultry products, as producers pass their costs on...

i'll be posting that later, with links and other reports, on my MW666 blog...

The history of oil production from Saudi Arabia has largely come from individual wells that produced in the thousands of barrels a day. In order to sustain that production over decades, it has been necessary to ensure that

- The pressure differential between the well and the rock are sustained;

- That the rock has an adequate permeability to ensure that flow continues at a steady state;

- That the oil itself is of relatively low viscocity and is thus able to easily flow through the rock; and

- That there is a sufficient thickness and extent in the reservoir to allow such sustained production.

All of those factors came together in the giant fields that provided high levels of production over many decades, most particularly in the northern segments of Ghawar.

Yet those conditions are less commonly congruent in the fields that Aramco must now exploit to address the coming falls in production from the historic sources. These best of the rest (as the late Matt Simmons called them) must now increasingly carry the burden of sustaining Saudi production fail, individually, on differing grounds from meeting those earlier parameters.

Collectively and in the face of Ghawars decline, they will only be able to sustain production to their original targets and will not provide replacement production as the oldest and larger begin to fade. I would remind you of the curve that Euan put up back in 2007.

Energy Bulletin

Countries in the Persian Gulf would like us to believe that there are great prospects for higher production from the area. Looking back at historical production and past changes in stated reserves, we should be a little cautious about believing what we are told. We should keep in mind that there are possibilities for disruption in oil supplies from that area as well possibilities for increases. The stories we are being told about higher productive capacity may be just that – stories.

The North Sea will no doubt continue to decline in its oil production. The US with its long-term decline also faces challenges. Unless a high level of deepwater production is maintained, it is likely that US oil production will again begin to decline.

The FSU and the Rest of the World have at least the possibility of increased production, but these increases are likely to be relatively small, based on past patterns.

In total, world oil production is unlikely to rise by much, and may fall in ways that are hard to predict in advance.

2012-06-24

The roller-coaster ride for gasoline prices continue ... remember when some forecasters were predicting $5 per gallon? Now we are seeing prediction of $3 per gallon.From the Atlantic Journal Constitution: Expect gas prices to fall below $3

Is it possible the average price at the pump could be below $3 a gallon by the time leaves begin to change?There are always threats to the oil supply - Iran, a storm in the GOM, a strike in Norway, but right now it looks like prices will continue to decline with adequate supply and week demand growth.Absolutely, according to experts who follow fuel price trends, and some areas of Georgia have already broken the barrier. At one station in Macon on Friday, unleaded regular was selling for $2.90, and in Duluth and Suwanee prices were as low as $3.04 and $3.05, respectively.

Barring any unforeseen calamity that might disrupt production or distribution ... the price trend should continue, even with the arrival of summer and more vehicles on the road for vacations.

"[T]he market is suggesting gas below $3 by Halloween, and certainly by Thanksgiving," Tom Kloza of the Oil Price Information Service ...

Oil prices are still moving down. Brent is down to $90.98 per barrel, down another 10% over the last two weeks, and WTI is down to $79.76. The lower oil prices will not only lead to lower gasoline prices, but also a lower trade deficit and lower headline inflation (CPI).

The following graph shows the decline in gasoline prices. Gasoline prices are down significantly from the peak in early April. Gasoline prices in the west had been impacted by refinery issues, but prices are now falling there too.

Note: If you click on "show crude oil prices", the graph displays oil prices for WTI, not Brent; gasoline prices in most of the U.S. are impacted more by Brent prices.

1 currency now -yogi:

Yet there is severe inflation in the tolls on interstate highways, bridges and tunnels (Holland Tunnel-- $12), parking meters, registration fees, speeding fines, etc. Cars may stink, but this inflation is a regressive tax.

.Jonathan

CR wrote:

There are always threats to the oil supply - Iran, a storm in the GOM, a strike in Norway, but right now it looks like prices will continue to decline with adequate supply and week demand growth.

Are you including the demands for exported gasoline? Because retail gasoline in the US looks to be going the other way.

Mr Slippery:

The lower oil prices will not only lead to lower gasoline prices, but also a lower trade deficit and lower headline inflation (CPI).

A lower trade deficit would be nice, since we are monetizing about $50 billion a month of imports. If we could get that down to $30 billion a month, say $1 billion a day on monetized imports, we would be back on a sustainable balance of trade path!

vtcodger: