|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

| Jan | Feb | Mar | Apr | May | June | July | Aug | Sep | Oct | Nov | Dec |

|

|

|

|

It's really funny to read forecasts that are just one year old.

Note: Despite doom and gloom stock market went from 1260 to 1460 in one year. This new stock and bonds bubble was supported by Fed.

Some positive points

Some negative points:

The "recovery" is now the worst in US history, having just dipped below the heretofore lowest on record.

If there was any debate whether the Fed's policies have helped the economy or just the market (and specifically the Bernanke-targeted Russell 2000), the following two charts will end any and all debate. As the following chart from the St Louis Fed shows, as of the just completed quarter, US GDP "growth" since the "recovery" is now the worst in US history, having just dipped below the heretofore lowest on record. (It's Official: Worst. Recovery. EVER)

"...the formal debt/GDP is now 103.8% and growing fast."

01/30/2013Previously, when calculating debt/GDP metrics for the US, we naturally assumed some GDP growth in Q4. Following today's GDP data we now know what Q4 GDP is. We also know that, at least on a preliminary basis, it posted a decline on an annualized basis. This means that we now have an official print for US Debt/GDP as of December 31, 2012. The numerator, or debt: $16.432 trillion, or the debt ceiling, which as we know was breached on the same day, and which has yet to be formally raised. The denominator, or GDP: $15.829 trillion. This means that the formal debt/GDP is now 103.8% and growing fast.[Jan 30, 2013] US Ends 2012 With 103.8% Debt To GDP by Tyler Durden

Shrinkage: US Economy Declined By -0.1% In Q4

A stunner out of the BEA which just reported a Q4 GDP of -0.1% that was leaps and bounds below the 1.1% estimate, and a plunge from Q3's 3.1%. The factors: Private Inventories, Exports and Government Expenditures all of which contracted, by -1.27%, -0.81%, and -1.33%. The silver lining was in Personal Consumption Expenditures which added 1.52% to the negative print, most of it however driven by a surge in spending ahead of the fiscal cliff. Ironically, this was the biggest government-driven detraction from growth since Q1 2011, when GDP led to a -1.49% cut in the GDP, same in Q4 when government spending on defense fell the most since 1972. The solution is simple: print moar drones. Enter Mali. And since everything is now AMZN-ing, we can't wait for the spin that the GDP's margins were actually better than expected, leading to a 200 point surge in the DJIA.[Jan 30, 2013] Shrinkage: US Economy Declined By -0.1% In Q4

The removal of "event risk" is the bottom line which defines the markets currently and which is why there is such a large disparity between economic fundamentals and the markets' collective reaction.

Short and sweet; risk has subsided or at least that is the common perception. This does not mean that the collective thinking is correct or even that it will be the "collective thinking" for long.

The lack of a "fear factor" will push "relative valuations" in new directions which will impact the Dollar/Euro ratio causing even greater financial issues for Europe and higher Treasury yields will impact not just bonds with credit risk but equities as a matter of comparison.

Yields in Europe, which went down because of the Draghi promise coupled with our great slosh of capital and the "delay, defer and postpone" mindset of the Europeans may begin to rise again because of other factors which primarily would be their "relative valuations" against their American counterparts. The lack of "event risk" has two sides and two sets of consequences.

|

|

Switchboard | ||||

| Latest | |||||

| Past week | |||||

| Past month | |||||

February 7, 2013 | FRB Speech with Slideshow

At the "Restoring Household Financial Stability after the Great Recession: Why Household Balance Sheets Matter" research symposium sponsored by the Federal Reserve Bank of St. Louis, St. Louis, Missouri

Thank you very much. It's a pleasure to be here. The question I'd like to address today is this: What factors lead to overheating episodes in credit markets?1 In other words, why do we periodically observe credit booms, times during which lending standards appear to become lax and which tend to be followed by low returns on credit instruments relative to other asset classes?2 We have seen how such episodes can sometimes have adverse effects on the financial system and the broader economy, and the hope would be that a better understanding of the causes can be helpful both in identifying emerging problems on a timely basis and in thinking about appropriate policy responses.

Two Views of the Overheating Mechanism

I will start by sketching two views that might be invoked to explain variation in the pricing of credit risk over time: a "primitive preferences and beliefs" view and an "institutions, agency, and incentives" view. While the first view is a natural starting point, I will argue that it must be augmented with the second view if one wants to fully understand the dynamics of overheating episodes in credit markets.

According to the primitives view, changes in the pricing of credit over time reflect fluctuations in the preferences and beliefs of end investors such as households, where these beliefs may or may not be entirely rational. Perhaps credit is cheap when household risk tolerance is high--say, because of a recent run-up in wealth.3 Or maybe credit is cheap when households extrapolate current good times into the future and neglect low-probability risks.4

The primitives view is helpful for understanding some aspects of the behavior of the aggregate stock market, with the 1990s Internet bubble being one illustration. It seems clear that the sentiment of retail investors played a prominent role in inflating this bubble.5 More generally, research using survey evidence has shown that when individual investors are most optimistic about future stock market returns, the market tends to be overvalued, in the sense that statistical forecasts of equity returns are abnormally low.6 This finding is consistent with the importance of primitive investor beliefs.

By contrast, I am skeptical that one can say much about time variation in the pricing of credit--as opposed to equities--without focusing on the roles of institutions and incentives. The premise here is that since credit decisions are almost always delegated to agents inside banks, mutual funds, insurance companies, pension funds, hedge funds, and so forth, any effort to analyze the pricing of credit has to take into account not only household preferences and beliefs, but also the incentives facing the agents actually making the decisions. And these incentives are in turn shaped by the rules of the game, which include regulations, accounting standards, and a range of performance-measurement, governance, and compensation structures.

At an abstract level, one can think of the agents making credit decisions and the rulemakers who shape their incentives as involved in an ongoing evolutionary process, in which each adapts over time in response to changing conditions. At any point, the agents try to maximize their own compensation, given the rules of the game. Sometimes they discover vulnerabilities in these rules, which they then exploit in a way that is not optimal from the perspective of their own organizations or society. If the damage caused is significant enough, the rules themselves adapt, driven either by internal governance or by political and regulatory forces. Still, it is possible that at different times in this process, the rules do a better or worse job of managing the incentives of the agents.

To be more specific, a fundamental challenge in delegated investment management is that many quantitative rules are vulnerable to agents who act to boost measured returns by selling insurance against unlikely events--that is, by writing deep out-of-the-money puts. An example is that if you hire an agent to manage your equity portfolio, and compensate the agent based on performance relative to the S&P 500, the agent can beat the benchmark simply by holding the S&P 500 and stealthily writing puts against it, since this put-writing both raises the mean and lowers the measured variance of the portfolio.7 Of course, put-writing also introduces low-probability risks that may make you, as the end investor, worse off, but if your measurement system doesn't capture these risks adequately--which is often difficult to do unless one knows what to look for--then the put-writing strategy will create the appearance of outperformance.

Since credit risk by its nature involves an element of put-writing, it is always going to be challenging in an agency context, especially to the extent that the risks associated with the put-writing can be structured to partially evade the relevant measurement scheme. Think of the AAA-rated tranche of a subprime collateralized debt obligation (CDO), where the measurement scheme is the credit risk model used by the rating agency. To the extent that this model is behind the curve and does not fully recognize the additional structural leverage and correlational complexities embedded in a second-generation securitization like the CDO, as opposed to a first-generation one, it will be particularly vulnerable to the introduction of a second-generation product.8

These agency problems may be exacerbated by competitive pressures among intermediaries and by the associated phenomenon of relative performance evaluation. A leading example here comes from the money market fund sector, where even small increases in a money fund's yield relative to its competitors can attract large inflows of new assets under management.9 And if these yield differentials reflect not managerial skill but rather additional risk-taking, then competition among funds to attract assets will only make the underlying put-writing problem worse.

But it is not all that satisfying--either intellectually or from a policy perspective--to simply list all of the ways that the delegation of credit decisions to agents inside big, complicated institutions can lead things astray. It must be the case that, on average over long periods of time, these agency problems are contained tolerably well by the rules of the game--by some combination of private governance and public policy--or else our credit markets would not be as large and as well developed as they are. A more interesting set of questions has to do with time-series dynamics: Why is it that sometimes, things get out of balance, and the existing set of rules is less successful in containing risk-taking? In other words, what does the institutions view tell us about why credit markets sometimes overheat?

Let me suggest three factors that can contribute to overheating.

- The first is financial innovation. While financial innovation has provided important benefits to society, the institutions perspective warns of a dark side, which is that innovation can create new ways for agents to write puts that are not captured by existing rules. For this reason, policymakers should be on alert any time there is rapid growth in a new product that is not yet fully understood. Perhaps the best explanation for the existence of second-generation securitizations like subprime CDOs is that they evolved in response to flaws in prevailing models and incentive schemes.10 Going back further, a similar story can be told about the introduction of payment-in-kind (PIK) interest features in the high-yield bonds used in the leveraged buyouts (LBOs) of the late 1980s. I don't think it was a coincidence that among the buyers of such PIK bonds were savings and loan associations, at a time when many were willing to take risks to boost their accounting incomes.

- The second closely related factor on my list is changes in regulation. New regulation will tend to spur further innovation, as market participants attempt to minimize the private costs created by new rules. And it may also open up new loopholes, some of which may be exploited by variants on already existing instruments.

- The third factor that can lead to overheating is a change in the economic environment that alters the risk-taking incentives of agents making credit decisions. For example, a prolonged period of low interest rates, of the sort we are experiencing today, can create incentives for agents to take on greater duration or credit risks, or to employ additional financial leverage, in an effort to "reach for yield."11 An insurance company that has offered guaranteed minimum rates of return on some of its products might find its solvency threatened by a long stretch of low rates and feel compelled to take on added risk.12 A similar logic applies to a bank whose net interest margins are under pressure because low rates erode the profitability of its deposit-taking franchise.

Moreover, these three factors may interact with one another. For example, if low interest rates increase the demand by agents to engage in below-the-radar forms of risk-taking, this demand may prompt innovations that facilitate this sort of risk-taking.

Why the Distinction Matters

To summarize the argument thus far, I have drawn a distinction between two views of risk-taking in credit markets. According to the primitives view, changes over time in effective risk appetite reflect the underlying preferences and beliefs of end investors. According to the institutions view, such changes reflect the imperfectly aligned incentives of the agents in large financial institutions who do the investing on behalf of these end investors. But why should anybody care about this distinction?

One reason is that your view of the underlying mechanism shapes how you think about measurement. Consider this question: Is the high-yield bond market currently overheated, in the sense that it might be expected to offer disappointing returns to investors? What variables might one look at to shape such a forecast? In a primitives-driven world, it would be natural to focus on credit spreads, on the premise that more risk tolerance on the part of households would lead them to bid down credit spreads; these lower spreads would then be the leading indicator of low expected returns.

On the other hand, in an institutions-driven world, where agents are trying to exploit various incentive schemes, it is less obvious that increased risk appetite is as well summarized by reduced credit spreads. Rather, agents may prefer to accept their lowered returns via various subtler nonprice terms and subordination features that allow them to maintain a higher stated yield. Again, the use of PIK bonds in LBOs is instructive. A long time ago, Steve Kaplan and I did a study of the capital structure of 1980s-era LBOs.13 What was most noteworthy about the PIK bonds in those deals was not that they had low credit spreads. Rather, it was that they were subject to an extreme degree of implicit subordination. While these bonds were not due to get cash interest for several years, they stood behind bank loans with very fast principal repayment schedules, which in many cases required the newly leveraged firm to sell a large chunk of its assets just to honor these bank loans. Simply put, much of the action--and much of the explanatory power for the eventual sorry returns on the PIK bonds--was in the nonprice terms.

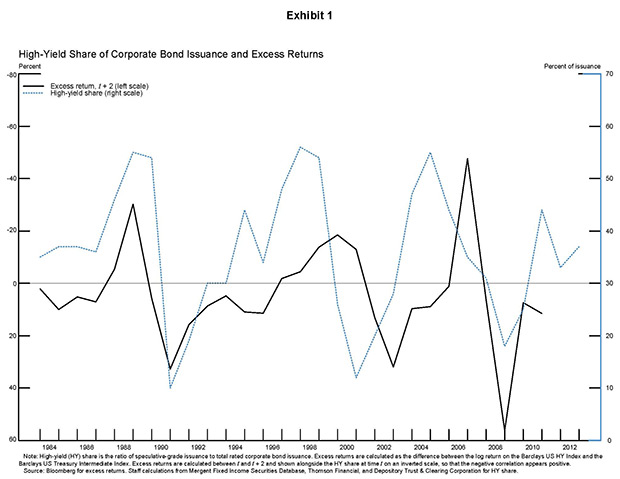

It is interesting to think about recent work by Robin Greenwood and Sam Hanson through this lens.14 They show that if one is interested in forecasting excess returns on corporate bonds (relative to Treasury securities) over the next few years, credit spreads are indeed helpful, but another powerful predictive variable is a nonprice measure: the high-yield share, defined as issuance by speculative-grade firms divided by total bond issuance. When the high-yield share is elevated, future returns on corporate credit tend to be low, holding fixed the credit spread. Exhibit 1 provides an illustration of their finding. One possible interpretation is that the high-yield share acts as a summary statistic for a variety of nonprice credit terms and structural features. That is, when agents' risk appetite goes up, they agree to fewer covenants, accept more-implicit subordination, and so forth, and high-yield issuance responds accordingly, hence its predictive power.

A second implication of the institutions view is what one might call the "tip of the iceberg" caveat. Quantifying risk-taking in credit markets is difficult in real time, precisely because risks are often taken in opaque ways that escape conventional measurement practices. So we should be humble about our ability to see the whole picture, and should interpret those clues that we do see accordingly. For example, I have mentioned the junk bond market several times, but not because this market is necessarily the most important venue for the sort of risk-taking that is likely to raise systemic concerns. Rather, because it offers a relatively long history on price and nonprice terms, it is arguably a useful barometer. Thus, overheating in the junk bond market might not be a major systemic concern in and of itself, but it might indicate that similar overheating forces were at play in other parts of credit markets, out of our range of vision.

Recent Developments in Credit Markets

With these remarks as a prelude, what I'd like to do next is take you on a brief tour of recent developments in a few selected areas of credit markets. This tour draws heavily on work conducted by the Federal Reserve staff as part of our ongoing quantitative surveillance efforts, under the auspices of our Office of Financial Stability Policy and Research.

The first stop on the tour is the market for leveraged finance, encompassing both the public junk bond market and the syndicated leveraged loan market. As can be seen in exhibit 2, issuance in both of these markets has been very robust of late, with junk bond issuance setting a new record in 2012. In terms of the variables that could be informative about the extent of market overheating, the picture is mixed. On the one hand, credit spreads, though they have tightened in recent months, remain moderate by historical standards. For example, as exhibit 3 shows, the spread on nonfinancial junk bonds, currently at about 400 basis points, is just above the median of the pre-financial-crisis distribution, which would seem to imply that pricing is not particularly aggressive.15

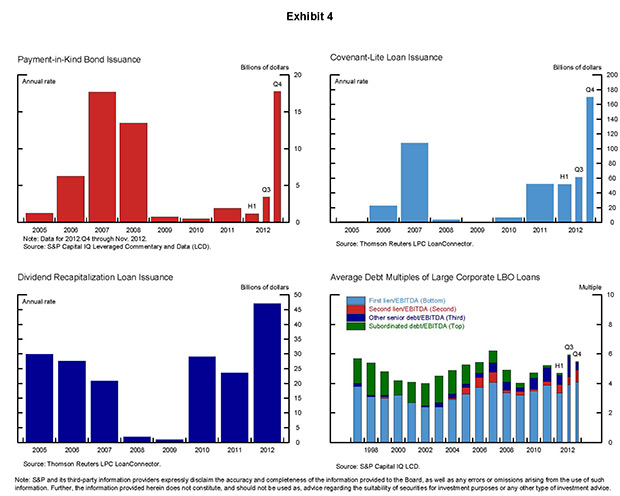

On the other hand, the high-yield share for 2012 was above its historical average, suggesting--based on the results of Greenwood and Hanson--a somewhat more pessimistic picture of prospective credit returns.16 This notion is supported by recent trends in the sorts of nonprice terms I discussed earlier (exhibit 4). The annualized rates of PIK bond issuance and of covenant-lite loan issuance in the fourth quarter of 2012 were comparable to highs from 2007. The past year also saw a new record in the use of loan proceeds for dividend recapitalizations, which represents a case in which bondholders move further to the back of the line while stockholders--often private equity firms--cash out.17 Finally, leverage in large LBOs rose noticeably, though less dramatically, in the third and fourth quarters of 2012.

Putting it all together, my reading of the evidence is that we are seeing a fairly significant pattern of reaching-for-yield behavior emerging in corporate credit. However, even if this conjecture is correct, and even if it does not bode well for the expected returns to junk bond and leveraged-loan investors, it need not follow that this risk-taking has ominous systemic implications. That is, even if at some point junk bond investors suffer losses, without spillovers to other parts of the system, these losses may be confined and therefore less of a policy concern.

In this regard, one lesson from the crisis is that it is not just bad credit decisions that create systemic problems, but bad credit decisions combined with excessive maturity transformation. A badly underwritten subprime loan is one thing, and a badly underwritten subprime loan that serves as the collateral for asset-backed commercial paper (ABCP) held by a money market fund is something else--and more dangerous. This observation suggests an idealized measurement construct. In principle, what we'd really like to know, for any given asset class--be it subprime mortgages, junk bonds, or leveraged loans--is this: What fraction of it is ultimately financed by short-term demandable claims held by investors who are likely to pull back quickly when things start to go bad? It is this short-term financing share that creates the potential for systemic spillovers in the form of deleveraging and marketwide fire sales of illiquid assets.

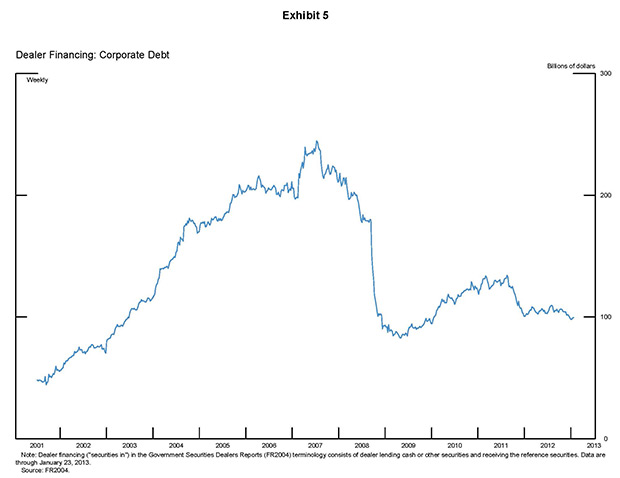

This short-term financing share is difficult to measure comprehensively, but exhibit 5 presents one graph that gives some comfort. The graph shows dealer financing of corporate debt securities, much of which is done via short-term repurchase agreements (repos). This financing rose rapidly in the years prior to the crisis, then fell sharply, and remains well below its pre-crisis levels today. So, on this score, there appears to be only modest short-term leverage behind corporate credit, which would seem to imply that even if the underlying securities were aggressively priced, the potential for systemic harm resulting from deleveraging and fire sales would be relatively limited.

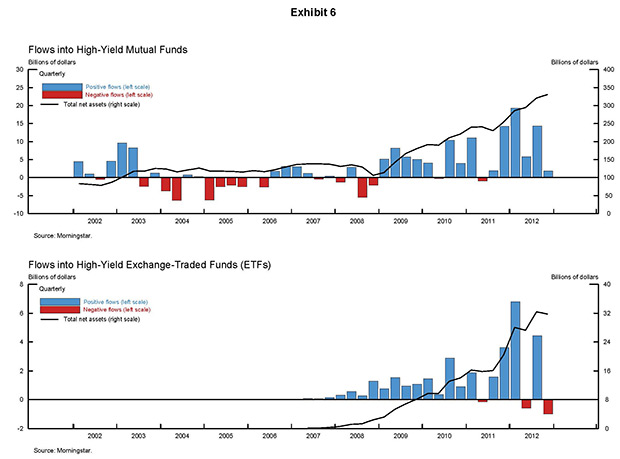

Nevertheless, I want to urge caution here and, again, stress how hard it is to capture everything we'd like. As I said, ideally we would total all of the ways in which a given asset class is financed with short-term claims. Repos constitute one example, but there are others. And, crucially, these short-term claims need not be debt claims. If relatively illiquid junk bonds or leveraged loans are held by open-end investment vehicles such as mutual funds or by exchange-traded funds (ETFs), and if investors in these vehicles seek to withdraw at the first sign of trouble, then this demandable equity will have the same fire-sale-generating properties as short-term debt.18 One is naturally inclined to look at data on short-term debt like repo, given its prominence in the recent crisis. But precisely because it is being more closely monitored, there is the risk that next time around, the short-term claims may take another form.

With this caveat in mind, it is worth noting the pattern of inflows into mutual funds and ETFs that hold high-yield bonds, shown in exhibit 6. Interestingly, the picture here is almost the reverse of that seen with dealer financing of corporate bonds. Assets under management in these vehicles were essentially flat in the years leading up to the crisis, but they have increased sharply in the past couple of years.19 This observation suggests, albeit only loosely, that there may be some substitutability between different forms of demandable finance. And it underscores the importance of not focusing too narrowly on any one category.

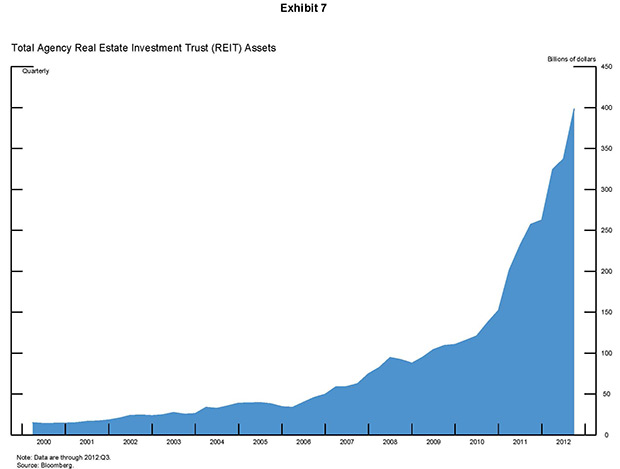

Continuing on with the theme of maturity transformation, the next brief stop on the tour is the agency mortgage real estate investment trust (REIT) sector. These agency REITs buy agency mortgage-backed securities (MBS), fund them largely in the short-term repo market in what is essentially a levered carry trade, and are required to pass through at least 90 percent of the net interest to their investors as dividends. As shown in exhibit 7, they have grown rapidly in the past few years, from $152 billion at year-end 2010 to $398 billion at the end of the third quarter of 2012.

One interesting aspect of this business model is that its economic viability is sensitive to conditions in both the MBS market and the repo market. If MBS yields decline, or the repo rate rises, the ability of mortgage REITs to generate current income based on the spread between the two is correspondingly reduced.

Another place where the desire to generate yield can show up is in commercial banks' securities holdings. In recent work, Sam Hanson and I documented that the duration of banks' non-trading-account securities holdings tends to increase significantly when the short rate declines.20 We hypothesized that this pattern was due to a particular form of agency behavior--namely, that given the conventions of generally accepted accounting principles, a bank can boost its reported income by replacing low-yielding short-duration securities with higher-yielding long-duration securities.

Something along these lines seems to be happening today: The maturity of securities in banks' available-for-sale portfolios is near the upper end of its historical range. This finding is noteworthy on two counts. First, the added interest rate exposure may itself be a meaningful source of risk for the banking sector and should be monitored carefully--especially since existing capital regulation does not explicitly address interest rate risk. And, second, in the spirit of tips of icebergs, the possibility that banks may be reaching for yield in this manner suggests that the same pressure to boost income could be affecting behavior in other, less readily observable parts of their businesses.

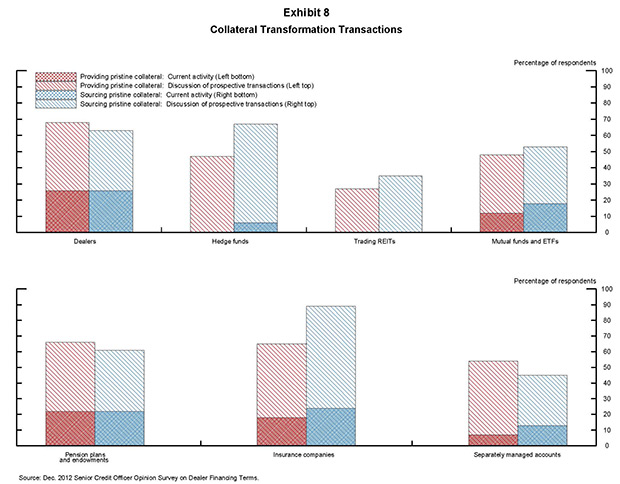

The final stop on the tour is something called collateral transformation. This activity has been around in some form for quite a while and does not currently appear to be of a scale that would raise serious concerns--though the available data on it are sketchy at this point. Nevertheless, it deserves to be highlighted because it is exactly the kind of activity where new regulation could create the potential for rapid growth and where we therefore need to be especially watchful.

Collateral transformation is best explained with an example. Imagine an insurance company that wants to engage in a derivatives transaction. To do so, it is required to post collateral with a clearinghouse, and, because the clearinghouse has high standards, the collateral must be "pristine"--that is, it has to be in the form of Treasury securities. However, the insurance company doesn't have any unencumbered Treasury securities available--all it has in unencumbered form are some junk bonds. Here is where the collateral swap comes in. The insurance company might approach a broker-dealer and engage in what is effectively a two-way repo transaction, whereby it gives the dealer its junk bonds as collateral, borrows the Treasury securities, and agrees to unwind the transaction at some point in the future. Now the insurance company can go ahead and pledge the borrowed Treasury securities as collateral for its derivatives trade.

Of course, the dealer may not have the spare Treasury securities on hand, and so, to obtain them, it may have to engage in the mirror-image transaction with a third party that does--say, a pension fund. Thus, the dealer would, in a second leg, use the junk bonds as collateral to borrow Treasury securities from the pension fund. And why would the pension fund see this transaction as beneficial? Tying back to the theme of reaching for yield, perhaps it is looking to goose its reported returns with the securities-lending income without changing the holdings it reports on its balance sheet.

There are two points worth noting about these transactions. First, they reproduce some of the same unwind risks that would exist had the clearinghouse lowered its own collateral standards in the first place. To see this point, observe that if the junk bonds fall in value, the insurance company will face a margin call on its collateral swap with the dealer. It will therefore have to scale back this swap, which in turn will force it to partially unwind its derivatives trade--just as would happen if it had posted the junk bonds directly to the clearinghouse. Second, the transaction creates additional counterparty exposures--the exposures between the insurance company and the dealer, and between the dealer and the pension fund.

As I said, we don't have evidence to suggest that the volume of such transactions is currently large. But with a variety of new regulatory and institutional initiatives on the horizon that will likely increase the demand for pristine collateral--from the Basel III Liquidity Coverage Ratio, to centralized clearing, to heightened margin requirements for noncleared swaps--there appears to be the potential for rapid growth in this area. Some evidence suggestive of this growth potential is shown in exhibit 8, which is based on responses by a range of dealer firms to the Federal Reserve's Senior Credit Officer Opinion Survey on Dealer Financing Terms.21 As can be seen, while only a modest fraction of those surveyed reported that they were currently engaged in collateral transformation transactions, a much larger share reported that they had been involved in discussions of prospective transactions with their clients.

Feb 28, 2013

Typically, these days when people compare the U.S. to Japan, it's a cautionary economic tale - a warning about persistent low growth and high government debt.

After Japan's asset bubble burst in the early 1990s, the country has suffered two "lost decades" of stagnant or no growth.

Some believe the U.S. is headed on a similar trajectory.

Related: 2013 Could be the Year Japan's Economy Turns Around: Cumberland's Witherell

But for Zachary Karabell, president of River Twice Research, that wouldn't be the worst thing for the U.S. He argues the economic trends we are used to hearing about regarding Japan are not the entire story. And that in many ways, the U.S. would be so lucky to be like Japan in ways some would use to describe "utopia."

Related: Japan's Monetary Policies Are Disastrous for U.S. Economy: Peter Schiff

In the accompanying interview, he makes the case that Japan's citizens enjoy great health, the third-highest life expectancy in the world, low violence, orderly democratic government, and efficient bureaucracy attending to issues such as public safety, infrastructure, education, housing and healthcare with a high level of competence and efficiency.

Related: Bank of Japan Reignites Currency War Debate

That said, those aren't the points that draw comparisons with the U.S. economy.

Karabell says his analysis is more about making the point that Japan wouldn't be the most dire scenario the U.S. economy could face.

"We don't know what outcome the United States is headed for, but if Japan is what we point to for the 'oh my god' moment, we're pointing to the wrong thing," he tells The Daily Ticker. "We could do a lot worse and I'm actually concerned we're heading on a track that will be considerably worse.

"So I would much rather focus America's attention on both the perils and possibilities of our current trajectory rather than holding up Japan as the thing we should avoid."

Lauren Lyster is the host of The Daily Ticker and Hot Stock Minute. You can follow her on Twitter at @LaurenLyster.

Crooks and Liars

While the Foxies were busy maligning the president, they didn't have time left to consider how the sequester might affect everyday people not earning television-pundit salaries and not with a partisan agenda: Teaching jobs and education funding are at risk; unemployment insurance benefits and aid for Hurricane Sandy victims are also subject to sequester.

The Bipartisan Policy Center reported the following:

(T)he immediate and across the board nature of the cuts, along with their magnitude concentrated in a seven-month period, will impair economic growth as the year progresses. At BPC, we estimated last year that the sequester would reduce 2013 gross domestic product (GDP) growth by half a percentage point, and would cost the economy approximately one million jobs over the next two years. More recent estimates released by the CBO and Macroeconomic Advisors have roughly confirmed these projections.

2/26/2013

cdresearch:

Housing Smoke And Mirrors | Global Economic Intersection

"The consensus opinion on the US Housing Market is that it is in recovery mode. Closer analysis of the data reveals that this recovery is artificial; and that the tools that made the recovery have built in a self-destruct mechanism.......

........ The slow death is easy to visualize. Loans with vintages from 2005-2007, when the bubble was inflating, were the first to have problems. Federal programmes have now got the delinquency rate of these 2005-2007 vintages falling. Loans taken out after 2008 are all accelerating into delinquency. This signals that borrowers since 2008 cannot afford to meet their current debt obligations. This could be because the economy is weak. It could also be because the size of the loans (i.e. the value of the underlying houses) is still too large.

Federal programmes have stopped the market from falling; and combined with easy money have actually made prices rise. People buying with mortgages however still can't really afford the current sales price. Only vultures with cash can afford the price, because they have no debt........

....... The current rising delinquency line, albeit less steep than in 2008 and 2009, still signals that the housing market is in stress and prices are still too high for buyers. Even with modifications and low interest rates, thanks to the Government and the Fed, the market remains unsustainable.

The Federal Programmes and the Federal Reserve have prevented true price discovery from occurring in the present; this price discovery however cannot be avoided. They hope that the discovery will be made in conditions of economic growth, so that the adjustment to realistic market prices for houses is higher rather than lower. The housing market is therefore the hostage of economic growth and not the signal of economic growth."

poicv2.0

Tommy Vu"Sometimes the problems are actually corrected, but sometimes (most of the times?) the problems continue but the economy adjusts to them, in the form of slower/negative growth, higher unemployment, bankruptcy, etc."

Historically turning a blind eye to corruption in the form that we are now doing as a society has not ended well. When so many large companies are deemed so important and interconnected that there is an explicit decision to not bring criminal charges, against the recommendation of those investigating the crimes, that is a HUGE warning sign that we are on a very dangerous road as a society.

If you can point me to a period in history where the above behavior turned out well for the country in question I'm all ears.

Recessions don't clear away high-level corruption. They clear away bad debt.

"In general terms, methodological shifts in government reporting have depressed reported inflation, moving the concept of the CPI away from being a measure of the cost of living needed to maintain a constant standard of living."

Simply put, if the same measures used in the past were applied today. Apples to apples if you will

poicv2.0 wrote:

Recessions don't clear away high-level corruption. They clear away bad debt.

if only that were the case. In the current example it appears that bad debt was cleared by revising accounting rules, printing wild amounts of new money (300%) and directing such money to those who speculated us into the crash on terms that one can only describe as a gift. It appears in this case the purpose of recession was to enhance corruption and transfer private bad debt into

poicv2.0:Not-So-Golden Years: Over 75, Crushed by Debt - Yahoo! Finance

"In general, the good news is that people ages 75 and older are much less likely to have debt, and generally carry far less debt, than other older Americans. But Craig Copeland, a senior research associate with EBRI and the report's author, said it was still troubling to see that the trend for that group was toward increasing, rather than decreasing, debt burdens."

"But in general, she said the really troubling finding she's seeing is that younger Americans appear to be taking on more debt than previous generations, and paying it off at slower rates.

That could mean that today's young people have even bigger problems than their parents and grandparents when they reach age 75 and older."

..But I see BennyBoy today says that continued ZIRP has few risks, in his opinion, like asset bubbles or inflation. Of course a lack of assets among the elderly or the young might not be considered a bubble...hmmmmmm...

...Could Bernanke be economic antimatter? An anti-bubble?

" It appears in this case the purpose of recession was to enhance corruption and transfer private bad debt into public bad debt(through a combination of the CB balance sheet and currency debasement). "bidders buy 41.7% of 5-year note auction .I don't believe the purpose of the recession was to enhance corruption. I do believe the post-crash policies led to enhancement of existing corruption.

Rob Dawg

Former Idealist wrote:When Bernanke took office Feb 3, 2006 gold was $530/oz.

At 2% compounded gold should be $609/oz. Robbie.

Understates inflation, costs $800 to mine an ounce.My point. And mining an ounce or extracting a barrel are pretty damn good measures of inflation when you think about it as both involve almost every sector of the general economy.

ResistanceIsFeudal:

Rob Dawg wrote:

And mining an ounce or extracting a barrel are pretty damn good measures of inflation when you think about it as both involve almost every sector of the general economy.

Especially since we're dealing in a completely liquid, 100% cash-only market in both instances.

arthur_dent:

Tommy Vu :poicv2.0 wrote:

I don't believe the purpose of the recession was to enhance corruption. I do believe the post-crash policies led to enhancement of existing corruption.

I see your point but I would not be so sure that post-crash policies were any different from pre-crash policies, so that the purpose of recession was merely a continuation of the enhancement process.

"While the CPI at one time was the measure desired by the public, government efforts turned the CPI away from measuring the price changes in a fixed-weight basket of goods and services to a quasi-substitution-based basket of goods, which destroyed the concept of the CPI as a measure of the cost of living of maintaining a constant standard of living.

The use of hedonic quality modeling in adjusting the prices of goods and services has destroyed the concept of the CPI as a measure of out-of-pocket expenses.

'

The Way the Politicians Wanted ItIn the early-1990s, political Washington moved to change the nature of the CPI. The contention was that the CPI overstated inflation (it did not allow substitution of less-expensive hamburger for more-expensive steak). Both sides of the aisle and the financial media touted the benefits of a "more-accurate" CPI, one that would allow the substitution of goods and services.

The plan was to reduce cost of living adjustments for government payments to Social Security recipients, etc. The cuts in reported inflation were an effort to reduce the federal deficit without anyone in Congress having to do the politically impossible: to vote against Social Security.

The changes afoot were publicized, albeit under the cover of academic theories. Few in the public paid any attention.

Carrying water for billionaires on fixed income...

poicv2.0 wrote on Tue, 2/26/2013 - 10:53 am

"I realize that Lehman Bros was not a bank, but wasn't that the event that caused a sea change in what to save and what to allow to fail ? "

That's the event that precipitated our decision to explicitly support any inter-connected financial institution as well as not bring criminal charges against officers or the banks themselves even when investigators recommend bring such charges.

shill

Obama: Sequestration 'dumb way of doing things' - MarketWatch

Looks like Obama went off Teleprompter...

Nothing is going to happen, they will ( just like they have since january 20th 2009 ) crank up the federal printing presses. Hence the dip in the precious. I only hope many took advantage of the sale.

arthur_dent:azuritebarfly wrote:

I believe the authority to close a bank is the responsibility of the FDIC

if the Fed props up a bank there is no reason for the FDIC to close it, although I have difficulty seeing that the FDIC has the wherewithal to close JPM. The banks are sitting on a vast amount of the freshly printed money parked as reserves and collecting profits from interest paid by the Fed. Since there is no new corresponding productive capacity to justify that new money the only way to fund the profits is by debasing the existing currency or transfer payments from the existing value base.

halbhh wrote:

In fact, not a single one of older generation want to stay in large house.

Married couple I know, almost 60, still working, plan to close on smaller home next week. Already cleared out most of extra stuff/clutter in current home, done some packing-- comment of one re: clearing out current home: "I'm so glad we've done this now, not had to do it when we were older". New home is in smaller town/city. They also own a small RV and are able to sometimes work out of it, stay in state parks near a work site (they're self-employed).

A few other people in that general age group have downsized via new jobs, i.e., they moved for job, first rented an apartment then bought smaller than previous home.

A few other friends in that age group have 1 or more adult children living w/them for awhile (all working full time) and are renting out part of their home. Possibly not legally, but it works for them and no complaints from neighbors. They live in good public school districts and the people renting have small children & apparently couldn't afford to live in the school district otherwise.

Of the adult children, one is out of the country for long periods of time (1-2 years) for work so she's never bothered to buy/rent, the other is working full time but previous rental was sold.

barfly

arthur_dent wrote:

Since their is no new corresponding productive capacity to justify that new money

that money is increasing the reserve ratios mandated by Dodd-Frank

Finance_Fan

"The math is not difficult. The US has an annual GDP of $14 trillion, and the nation's current $1 trillion in annual deficit spending is seven percent of its GDP. Growth in GDP has recently been running at about two percent annually (though in the last quarter of 2012 the economy actually contracted slightly). The relationship between deficit spending and GDP growth may not be exactly 1:1 but it's probably quite close. The conclusion is therefore inescapable: doing away with a substantial portion of deficit spending would reduce GDP by a roughly corresponding amount, almost certainly causing the economy to tip over into recession."

-RHi'm afraid this is mostly true. We are living in a debt trap. lower the deficits to avoid default and you get a deeper recession and higher debt/GDP ratios. hence it's politically more palatable to just keep on going with the $1T deficits and reach default through that "less painful" way.

default is unavoidable anyway given that the developed world headwinds are structural (aging demographics).

arthur_dent wrote on Tue, 2/26/2013 - 11:17 am (in reply to...)

Finance_Fan wrote on Tue, 2/26/2013 - 11:18 ambarfly wrote:

that money is increasing the reserve ratios mandated by Dodd-Frank

don't see how that matters, new money without corresponding real growth is debasement. Of course a more traditional way to increase reserves would be through lower profits.

ResistanceIsFeudalUncle wants to sell, can't get the price, is shadow inventory. Other Uncle already downsized. Father is looking to sell and downsize.In fact, not a single one of older generation want to stay in large house.

then you get the other issue, with younger people having fewer kids or none, large homes are not even needed. they are seing as a drag, not as something desirable.

azurite wrote:

They live in good public school districts and the people renting have small children & apparently couldn't afford to live in the school district otherwise.

Tough to dispute that "good public school districts" and also 'not being a warground for gang warfare, crack dealers and meth-heads' have value to most people. Wherever value exists, it will eventually be monetized.

sum luk:

arthur_dent wrote:

new money without corresponding real growth is debasement

... if all Ben is doing is preventing mbs price discovery, there's no debasement; except, possibly, from what you think shudda happened on some ideal plane.

shill:

sum luk:CR has a very reasonable expectation that the future will be like the past -- young generations will want to own their own single-family home. What if the future is different from the past? At these prices, the future does not look like that past to me.

$50 dollar an hour Mc-jobs should cover it.

meanwhile, back at the ranch, from: Bernanke on Sequester Cuts: Too Much, Too Soon - ABC News

Ben said:

"Congress and the administration should consider replacing the sharp, frontloaded spending cuts required by the sequestration with policies that reduce the federal deficit more gradually in the near term but more substantially in the longer run," Ben Bernanke said today. "Such an approach could lessen the near-term fiscal headwinds facing the recovery while more effectively addressing the longer-term imbalances in the federal budget."

.... I think Mr. Mkt hears "lets make a deal"

Finance_Fan:

CR has a very reasonable expectation that the future will be like the past -- young generations will want to own their own single-family home. What if the future is different from the past? At these prices, the future does not look like that past to me.the future in terms of demographics and living arrangements is Europe already on the coastal areas. the young get along with their parents it seems better than the boomers that wanted out desperately at 18. they value mobility and flexibility. free housing adds to their ability to be picky in terms of jobs, ability to travel and the like. it's not looked down either, i know youngsters who even envy those who don't need to pay rent. i think a decade or so ago it was looked down on for some reason. younger people burdened with student debt (or even knowing a friend who is) get financially savvy fast.

the middle of the country is dealing with a meth epidemics of big proportions, reminds me of the crack epidemic in inner cities 20-35 years ago. we'll see if meth doesn't take over the coastal areas too. that shouldn't be taken for granted.

ResistanceIsFeudal:

can you imagine our society in the event the rentiers (elite, bourgeois, and proletariat alike) had to experience the evaporation of untoward profits and the collapse of speculative premia on leveraged asset holdings?

sum luksum luk wrote:

except, possibly, from what you think shudda happened on some ideal plane.

support of inflated prices may not be viewed by everyone as a view from an ideal plane.

ResistanceIsFeudal wrote:

can you imagine our society in the event the rentiers (elite, bourgeois, and proletariat alike) had to experience the evaporation of untoward profits and the collapse of speculative premia on leveraged asset holdings?

... I think they call that scenario, "not having an economy"

barfly

arthur_dentone man's opinion

inflation tied to wages, which are flat since the 70's

we are very near going into a deflationary spiral, which Ben has so far prevented

sum luk wrote:

I'm not understanding why Ben's fiat is an insufficient replacement for the "pre-recession money" that set those asset prices

my own view is that if you continually reward psychotics you will have an economic system dominated by psychotics who continually push the system toward an undamped response, creating higher highs and lower lows until the whole thing tears itself apart. The natural healing of a depression is that the psychotics are replaced by those who practiced sound money management and is a necessary part of system stability.

Yahoo! Finance

The "Great Rotation" from bonds to stocks is underway, or is it?

There is no doubt the investment world is confident we are still in a bond "bubble" that is sure to pop, but that opinion is now a few years old and has largely been incorrect.

Regardless of what the mainstream thinks, we remain skeptical of any bond bubble and are actually looking at a bond buying opportunity. Let's analyze some of the reasons.

A Phony Rotation

Once the money flow data was released for January showing decade high Mutual Fund (VFINX - News) and ETF (VTI - News) inflows, Wall Street went crazy with reports that the "great rotation" was in full swing as it justified buying equities (VT - News) at the expense of selling bonds (BOND - News).

- "Have we entered the Great Rotation" - Charles Schwab 2/6/13

- "Are we watching a Great Rotation into Stocks - Time Magazine 1/28/13

- "Trading the Market's 'Great Rotation" - MarketWatch 2/7/13

The great rotation argument implies a zero sum game where money is either in stocks (SPY - News) or it is in bonds (TIP - News) and the two asset classes jockey for investors' dollars. When investors put money into stocks, it must come from bonds. When money is put into bonds, it is at the expense of stocks.

But, the facts simply don't support such a scenario of recent rotation.

In order to justify January's equity fund inflows as part of the great rotation, the money that flowed into equity funds should have come out of bonds. But, bonds also had inflows of $30B. Not exactly a rotation out of bonds.

In reality the Great Rotation, was a "fake" as most of the money flowing into equities (EEM - News) came from savings and money market accounts that were ballooned by the accelerated pay that occurred in December as a result of the non-recurring "fiscal cliff" episode.

Times like these it often helps to step back from the day to day headlines and see what is really going on in the bigger picture. One of the best ways to do this is by examining the charts.

Seeing the Big Picture

One simple question: Does this chart of the iShares Barclays 20+ Year Treasury (TLT - News) look bullish or bearish?

The long term trend in bonds has been up in price and down in yield. Although long term Treasury prices have recently pulled back from their highs (what all the fuss is about), it barely even shows up in the chart above. Bonds are firmly in a bullish uptrend.

When Sentiment Gets Out of Whack

On 7/1/12 bonds also were experiencing a plethora of bearish sentiment as prices dipped to $125 on the TLT. Along with the shorter-term technical picture, the sentiment background helped us stay long treasuries.

In a post to our readers we wrote:

"Continue to disregard the media and talking heads that say bonds are overvalued and inflation is around the corner. Until we see it in price, it is not happening. Price is the only true leading indicator, and we will rely on it to tell us when inflation is here. Until then, we continue to stay long the longer duration treasury bonds. We are set up for all three time frames pointing in the same direction (up)".

As we alerted, U.S. Treasuries continued to rally and we swiftly exited on 7/20/12 when TLT was $130 and sentiment flipped to extremely bullish levels.

Are Treasuries a Buy?

The technical setup for TLT is intriguing right now for a few reasons. With price around $116, the recent pullback is now at a level near numerous support zones, which should keep the downside risk minimal.

Some of these support levels surround Fibonacci retracement levels, last year's $107-$113 support zone, as well as a long term uptrend support line.

A sizable decline in the equities (IWM - News) market also would only help increase bond prices as investors flee to bond safety. Couple this with the pessimistic sentiment surrounding bonds and the recipe is in place for another Treasury bond rally.

The ETF Profit Strategy Newsletter and Technical Forecast provide comprehensive analysis and formulate profit strategies based on fundamental, technical, and sentiment research including locations for stop losses and targets for profit taking.

Feb 26, 2013 | Yahoo! Finance

"In general, the good news is that people ages 75 and older are much less likely to have debt, and generally carry far less debt, than other older Americans. But Craig Copeland, a senior research associate with EBRI and the report's author, said it was still troubling to see that the trend for that group was toward increasing, rather than decreasing, debt burdens."

"But in general, she said the really troubling finding she's seeing is that younger Americans appear to be taking on more debt than previous generations, and paying it off at slower rates.

That could mean that today's young people have even bigger problems than their parents and grandparents when they reach age 75 and older."

..But I see BennyBoy today says that continued ZIRP has few risks, in his opinion, like asset bubbles or inflation. Of course a lack of assets among the elderly or the young might not be considered a bubble...hmmmmmm...

...Could Bernanke be economic antimatter? An anti-bubble?

Feb 26, 2013 | Yahoo! Finance

"In general, the good news is that people ages 75 and older are much less likely to have debt, and generally carry far less debt, than other older Americans. But Craig Copeland, a senior research associate with EBRI and the report's author, said it was still troubling to see that the trend for that group was toward increasing, rather than decreasing, debt burdens."

"But in general, she said the really troubling finding she's seeing is that younger Americans appear to be taking on more debt than previous generations, and paying it off at slower rates.

That could mean that today's young people have even bigger problems than their parents and grandparents when they reach age 75 and older."

..But I see BennyBoy today says that continued ZIRP has few risks, in his opinion, like asset bubbles or inflation. Of course a lack of assets among the elderly or the young might not be considered a bubble...hmmmmmm...

...Could Bernanke be economic antimatter? An anti-bubble?

February 25, 2013 | The Big Picture

rd:

The graph is a perception/opinion graph about what risk people are thinking they are willing to take. It does not provide any information on how much risk they are actually taking. Probably many of the people they are asking, don't really understand risk statistics in the context of the stock market or bond market. It appears that the people writing the article are using 80% equities as an acceptable risk threshold:

" There are other indications of lingering caution, though not outright fear. The share of fund investors who have 80 percent or more of their portfolios in the stock market is far lower than it was a decade ago, and fund investors are also diversifying more.

Again, this is most pronounced among 401(k) investors and older investors approaching or in retirement. Since 2000, the share of baby boomers investing more than 80 percent in stocks in their retirement plans has dropped in half, to about 25 percent for 50-somethings and 21 percent for 60-somethings in 2011, the most recent data available."

These authors somehow seem to be thinking that the portfolio asset allocations many people had in the dot.com boom are optimum. Is anybody in the financial sector seriously thinking most baby boomers should have 80%+ equities in their portfolio at this time? Their data point indicating that over 20% of 50+ and 60+ people have more than 80% equities in their portfolio should be concerning us at this point, especially considering that markets have doubled over the past 4 years and several fairly reliable valuation indicators (CAPE, Q etc.) are indicating that we are in the upper range of historic valuations. these people may really be taking on too much risk.

If they were presenting data indicating that more than 25% of 50+ people had less than 40% equities in their portfolio, then I could see an argument for being over-cautious but that data is not provided. At this time, it appears that the authors are simply pushing for the small investor to return to the fully invested profiles they had in 2000 and 2007, presumably so they can suffer the same fate as then.

USSofA:

How many boomers got burned in the dot com bubble and said they were done with the stock market. They turned to something more concrete to save for retirement…housing. Ouch again. There is only one safe place left, good old US Treasuries. Ouch again to the Bernank. From now on when a boomer dies, check the mattress first.

DisciplinedInvesting:

Nice post. :)

http://www.disciplinedinvesting.blogspot.com/2013/02/most-investors-remain-cautious-on-stocks.html

Just pulling your chain Barry.

David

~~~

BR: What is the original source of the chart? I thought that was what I was linking to . . .

techy:

smartass: Most people who are in their 50s that I know, will be dependent on SS for most of their living expense, but I know one another plan they are counting on, work till death.

Another thing, I dont think it is unfair to pay better benefits to SS recipients, otherwise they will starve because of ZIRP. They planned for min 5% return from safe investment, not 1%.

The inequality caused by offshoring and automation can be fought only with massive stimulus spending or zirp QE(inflation to remove inequality).

smartass:

@BennyProfane

The way SS works is they only count 1/2 of your benefits, so that married couple getting 35k in benefits only has 17.5k in income subtract standard deduction and personal exemptions and you have no income left. If you itemize then you can earn more with no tax.

Like everything there are many catches..they will tax your benefits @ 85% if your income is over 44k joint 34k single

A particular couple I work with retired last year. While they were working we were withholding 10% from her IRA distributions. In dec I phoned their CPA let them know they are both retired 36k per year in SS combined another 8k per year from the IRA. I wanted all of us to be on the same page and he confirmed this couple could earn roughly 51-52k per year before any tax would kick in.

Needless to say if you are a high income earner then your income will not be tax free but it will still help lower your marginal tax rate.

DeDude:

@smartass;

The average monthly SS check is $1230 – with the 50% spousal benefits it gets to $1845 for a couple (with one being home-maker). That can cover a low living standard, although if anybody gets sick (and old people do) it will be a struggle. Many people are (by definition) below the average and if they are alone it can be extremely difficult to live and get health care on their SS alone. Now that is not the type of people who belong to your clientele since they simply cannot afford professional services (even if they need them).

However, the people you are dealing with have paid close to maximum into the SS system for prolonged periods of time – and when you calculate what they paid and what they get back out they are not getting such a hot deal (often would have gotten more back if the money had been placed in regular treasuries). That is why we, in all fairness, need to fix SS by putting a 1% SS tax on all income (including investment and inheritance income) in excess of the limit for normal SS taxes.

PS: The sad part about this discussion of SS benefit cuts is that the system will turn out to be fully funded for everybody if we just leave it alone for the next decade. We have had an epidemic of obesity for more than a decade now and it is getting worse. Obesity causes diabetes, hypertension and dyslipidemia. Those are all things that drastically cut life expectancy. So the average lifespan is about to drop. However, the SS administration builds its projections on current trends in lifespan not on the drop that we all know is about to begin. Even with the current projections they tell us that the system will suffer a few decades of 70-99% payments of promised benefits, then it will be back in black and produce a surplus. What do you think would happen if they used the lifespan predictions that include our knowledge of the effects of obesity. No, cannot do that – because then we would have no excuse for punishing the poor – and cutting taxes on the rich after surpluses magically appears (you know in a "nobody could have predicted" kind of way).

evelyn:

As retirement savings have turned away from pensions and toward 401K type investments, surely it is with widespread understanding among the financial elite that former pensioners don't know how to manage their own investments. What an opportunity to make money! We are ready marks waiting to be trolled, and annoying doesn't begin to express the problem with the setup.

slowkarma:

A lot of people who "did the right thing" - saved money, kept track of what they would have in retirement with conservative projections - are being screwed by the artificially low-interest environment being forced by the Fed; and will probably be screwed again on the back end of this thing, when the washout comes. In any case, if you're 73 years old and retired at 67, before the crash, having spent your life doing the right thing, buying equities is not really a risk - it's a requirement. For many of these people, retirement was carefully calculated: x amount from social security, y amount from a company pension, z amount from investments. But even the most conservative projections ten years ago didn't foresee a half-decade or more of virtually no returns on government bonds; and these carefully constructed retirements are going in the toilet, with people spending savings instead of interest. So, with the need for some return, and with the idea that an inflation washout is probably coming, people go to large companies with substantial dividends, trying to get both a bit of return and a bit of cover if inflation moves up. You have to ask: is 3M really more risky than government bonds that return nothing?

constantnormal

"Are Boomers Too Cautious About Stocks?"

If we are using history as our guide, then yes. But then consider these nuggets of experience …

The boomers were pitched IRAs and then 401-Ks, with the story that "in retirement you will spend less, so the money that comes out of these plans will be taxed less" … along with the fable of using their homes as their "investments" …

And indeed, the trend in tax rates has been ever-lower, but now no thinking person believes they can continue to decline … meanwhile health care costs have exploded, and employers have abandoned pensions, using 401-Ks as an excuse for doing so, and housing has punctured the myth of ever-increasing home values, leaving the typical boomer radically out of their depth, with their only real expectation being that every aspect of their existence is going to get incredibly expensive, and that the "system" is out to get them, with corruption throughout our society, and the top of the economic food chain merrily feeding on the shrimp struggling to hang on.

This is perception, and may or may not represent actual reality. But it does serve to crank uncertainty 'way up there, and make boomers leery of assuming any risk that they don't have to … they think that there is already to much uncertainty and risk in their lives, why take on more?

And truth be told, it is VERY difficult to see much of a rosy future ahead, with no evidence whatsoever of any corrective actions being taken in our society, some good evidence that things are going to get even more uncertain, and emerging nations elbow their way into the developed nation club, and putting immense pressure on resources and the environment (the Grantham argument).

History is a pretty poor guide at this point, for the formation of any expectations of the future, and the boomers have run outa time … their future is just about upon them … being paralyzed with conservative fears is a quite understandable thing for them to be experiencing …

Moopheus:

I agree with Julia–in Ye Olde Dayes of pensions and interest on savings, the idea was to back off risk as you got to the end of your prime earning years. Why risk a big loss when you couldn't make it up? The fact that many have insufficient savings and can no longer no longer count on safe investments to produce income is not a failing of boomers (well, not entirely), but of the crooks who swindled us out of these things.

danm:

One can always move into trailer parks and other small scale housing. Condos will be out of the question because of the upkeep fees -- If you don't have access to health care… why stay close to the city… the boodocks are way cheaper.

wally:

"Too" cautious?

The Cult of Equities continues.

skier5150:

So Boomer me turns 50 for Dot Bomb and the Bush offshoring & collapse, worked 4 years of his 8, none with benefits, started having medical issues, I did hold onto my house (oops), then back to a real job since 2009 (private mfg, not govt at all).

But wages have stalled since 1980 (cept for the 90′s) and we are called Communist for noticing you get less pay than your parents got when the GDP percapita was half what it is now. My big decade for saving $ is gone.

I am hanging OK, mainly due to not having a family, but retirement will only mean getting off the 50+hr treadmill, and working contracts. I think it'll calm down one way or another in 5 years or so, but I'll live under a bridge before I give the crooked bastards running the Big Rigged Casino a godamn nickel.

Stocks managed to totter into the weekend while holding support.Excelsior!

And yes, a pun.

In watching the video below, Galton and Eugenics, I am reminded of some of the recent things which I have read, and the general current of policy talk, about the natural supremacy of the elite in Europe and America, and their entitlement to the spoils in return for their leadership through crisis.

See you Sunday evening.

Calculated Risk

Bad Dawg Bobby wrote on Sat, 2/23/2013 - 5:40 pm (in reply to...)

Rob Dawg wrote:

If we could get Chinese construction prices I'd say go for it.

"Chinese Construction prices" But quality of product, espescially high speed rail, I woul want union. American Union.

Ever notice that when it can to Republicans TAKING Taxpayer dollars ( What 4-6Trillion) to save TBTF Bankster or Corporations.

NO PROBLEM. Ben and Timmy just help themselves (With the permision of our Congress) to Tax money from the US Treasury

BUT 1.4 Trillion to Feed people with food stamps, or medical care or Disabilities they screem like stuck PIGS GEEEEEEK, GEEEEEEK (!)"I want that money"

They have really made no bones about being the party that represents the top 20%. It is sad being a former Republican and stand here and watch it self destruct, Time to bring back the WIG party Smile I say Tax the Corporations, Banks,People 90% that making over 1 Million a year. I'm Kidding but I really have had enough of this greed, instead of leaders our top 20% have become wealth spunges.

Tyler Durden's picture The Spending Crunch Is Official: "We Are Confident There Is An Issue With The Consumer" Submitted by Tyler Durden on 02/20/2013 - 10:42 Think the Walmart "disastrous" sales memo was a one-off event, which net of Walmart's damage should be completely ignored (something the market has been perfectly happy to oblige with)? Then listen to a separate perspective on the US consumer, this time from a very different angle: that of Town Sports International which operates such gyms as New York Sports Club, and specifically its CEO David Gallagher, who in last night's conference call just confirmed what everyone knows: "As we moved into January membership trends were tracking to expectations in the first half of the month, but fell off track and did not meet our expectations in the second half of the month. We believe the driver of this was the rapid decline in consumer sentiment that has been reported and is connected to the reduction in net pay consumers earn given the changes in tax rates that went into effect in January."

"Several participants emphasized that the Committee should be prepared to vary the pace of asset purchases, either in response to changes in the economic outlook or as its evaluation of the efficacy and costs of such purchases evolved. For example, one participant argued that purchases should vary incrementally from meeting to meeting in response to incoming information about the economy.A number of participants stated that an ongoing evaluation of the efficacy, costs, and risks of asset purchases might well lead the Committee to taper or end its purchases before it judged that a substantial improvement in the outlook for the labor market had occurred.

Several others argued that the potential costs of reducing or ending asset purchases too soon were also significant, or that asset purchases should continue until a substantial improvement in the labor market outlook had occurred.

A few participants noted examples of past instances in which policymakers had prematurely removed accommodation, with adverse effects on economic growth, employment, and price stability; they also stressed the importance of communicating the Committee's commitment to maintaining a highly accommodative stance of policy as long as warranted by economic conditions.

In this regard, a number of participants discussed the possibility of providing monetary accommodation by holding securities for a longer period than envisioned in the Committee's exit principles, either as a supplement to, or a replacement for, asset purchases...

Similarly, one member raised a question about whether the statement language adequately captured the importance of the Committee's assessment of the likely efficacy and costs in its asset purchase decisions, but the Committee decided to

maintain the current language pending a review, planned for the March meeting, of its asset purchases...Ms. George [Kansas City Fed] dissented out of concern that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in inflation expectations.

In her view, the potential costs and risks posed by the Committee's asset purchases outweighed their uncertain benefits. Although she noted that monetary policy needed to remain supportive of the economy, Ms. George believed that policy had become too accommodative and that possible unintended side effects of ongoing asset purchases, posing risks to financial stability and complicating future monetary policy, argued against continuing on the Committee's current path."

FOMC, Fed Minutes, January 2013

Stocks dropped hard today, albeit from a lofty height reached with few corrections. The trend is not yet broken.The cause was said to be the release of the January Fed minutes, which suggested that QE will not be everlasting.

I think the correction was as much concerned about the lack of serious work being done in Washington about the sequester, and in particular to address a broken economy.

But in reality the stock market was reaching into bubble territory, with complacency at an extreme. And the economy has simply not caught up with pricing. And it may not for some time.

Forecasters keep reaching for the ever receding recovery. And I think it will keep receding, because of the policy error of the Federal Reserve and the Treasury in supplying stimulus to rescue bankers and traders from their own mismanagement and speculation, without performing their most imporatant obligations to the public and the real economy.

The cynical nature of Washington these days is hard for most people to understand. Those political denizens of the Beltway just do not care, judging by their servile attention to special interests, and preoccupation with personal enrichments and power. It is probably the tail end of a long running trend, culminating in the rise of a generation which has suckled on the gospel of greed.

WSJ.com

Americans had good reason to be disgusted by politicians arguing over the so-called fiscal cliff. But do they recognize such behavior in themselves?

Retirement is your own fiscal cliff. I mean ... it you one of those is going to ... retire by age sixty five ... but you're not saving and pushed into retirement and you standard of living dramatically drops.

You are pushed into the situation when you need as much as you can. Maximize you match, use Roth IRA (which gives you tremendous flexibility).

And working several extra years might be not under you control. Health issues or job market can decided against it.

Millennial investors have emerged from two boom-and-bust cycles more conservative about investing and more skeptical of financial advice than older generations who were hit hardest by the market, according to an Accenture survey released Wednesday.The survey of some 1,000 high-income, digitally savvy U.S. investors also showed that millennials were the most determined to learn how to invest and pass along wealth to their families.

"This poses a fundamental challenge for financial advisors who will see the greatest transfer of wealth in history from boomers to their heirs over the next several decades," Alex Pigliucci, global managing director of Accenture Wealth and Asset Management Services, said in a statement.

"But counter to prevailing wisdom, our research suggests millennials are a highly viable target for advisors."

According to the survey, 43% of millennial respondents (age 21-30) described themselves as "conservative" investors, compared with 31% of baby-boom respondents (age 46-70). Millennials were also significantly more likely than baby boomers to say they preferred "tried and true" investment options.

They were four times more likely than baby boomers to say they were unwilling to act on the advice of a financial advisor without first consulting other sources. Forty-four percent said they "spend a lot of time researching alternatives before making a major purchase decision," compared with 33% of baby boomers.

Forty percent millennial respondents said they were "determined" to pass along wealth to their families, compared with 25% of baby boomers and Gen Xers (aged 31-45). Forty-four percent described themselves as "extremely" interested in improving their understanding of investing, compared with 38% of older respondents.

Accenture said the survey pointed to unmet demand for online investor education and advisor-interaction tools that could increase millennial investing and help bridge the "trust gap" with financial advisors. Presented with concepts for new online educational resources, it said, millennial respondents showed overwhelming interest.

"The behaviors and attitudes of millennials are not just a matter of long-term strategy for wealth managers; they are a leading indicator of the need for change today," Pigliucci said.

"With half of all baby-boom investors currently active in social media and a vast majority active online, the innovations that will capture the millennial generation also will help capture the most coveted demographics among Gen Xers and baby boomers."

Accenture's research has found more than 75 million digitally savvy investors in the U.S. with high income, assets and education, and refers to as "Generation D" or "Gen D." This investor demographic, on which Accenture's survey focused, comprises 44% of the online U.S. population, age 18-65, and represents a staggering $27 trillion in total assets.

The survey found that Gen D members saw investing as a viable path to building and passing wealth to future generations. They also recognized the need for financial advice, but were less and less likely to view financial advisors as trusted sources.

For example, 59% of respondents across all generations said they had actively sought financial advice recently, but only 40% had turned to a financial advisor.

Yahoo! Finance

There's an old saying that poses the question: Do you want to hear the good news or bad news first? The thinking is that the order in which you are given information will somehow impact your reaction to it. But what if the bad news was actually good news - or at least presented a good opportunity?

Such is the mindset of Rob Arnott, chairman of Research Affiliates and manager of the five-star rated PIMCO All Asset Fund (PAAIX) and the All Asset All Authority Fund (PAUIX), who is troubled by a market that "shrugs off" everything yet is still closing in on all-time highs. "I'm concerned. I think we're definitely in a slowdown relative to last year - which was anemic enough - and quite possibly already in recession," he says in the attached video.

That's not to say he is out of ideas. On the contrary, he clearly states that no matter what the economy is doing, "there's always something interesting to invest in." For him, there are far too many bulls and far too few bears out there right now, and that presents an opportunity.

"If you look at advisor sentiment surveys, you find that right now there are fewer bears than have been seen in these surveys except at extreme major market tops, such as in early 2000," he says. "When it gets to be downright embarrassing to be a bear, doesn't that make for a wonderful time to take some risk off the table?"

Part of his concern that the economy has stalled comes from the fact that fourth-quarter GDP plunged to a three-and-a-half-year low of -0.1%, despite the fact that companies accelerated dividends and bonuses ahead of the tax increase. Since that activity was supposed to have happened in the first quarter, but was clawed back into 2012 instead, Arnott is understandably concerned about what this quarter is going to look like without it.