|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

| Jan | Feb | Mar | Apr | May | June | July | Aug | Sep | Oct | Nov | Dec |

|

|

|

|

Zero Hedge

Last week, Bill Gross did not mince his words when he said that he now "sees bubbles everywhere" and that "when that stops there will be repercussions" but for now Benny and the Inkjets, not to mention his band of merry statist men, who take from the poor and give to the wealthy, are playing the music on Max, and so one must dance and dance and dance. And after one legacy bond king, it was the turn of that other, ascendant one - Jeff Gundlach - to share his perspectives Bernanke's amazing bubble machine. His response, to nobody's surprise: "there is a bubble in central banking. We are drowning in central banking and quantitative easing.... And it's not ending until there are some negative consequences."

What are those negative consequences? This too should be perfectly expected for regular readers: currency devaluation leads to trade wars (as either is a zero sum game, and in a zero sum game it is very easy to blame someone else for one nation's suffering and economic malaise), trade wars lead to real wars (see the 1930s), and so on. We are not there just yet: quote Gundlach "With global growth slowing not everyone can increase their imports [indeed: observe just how it was that Spain managed to post its first "trade surplus" since 1971 - hint: not by boosting exports] you're playing a market share game." But it is rapidly approaching: "We are looking at competitive currency devaluations, which causes rancor, causes unhappiness, and fingerpointing and god-forbid tariffs and things that cause even slower economic growth a la the 1930s." Good choice of words, considering it was just a week ago that none other than stagnating metals magnate Lakshmi Mittal, head of ArcelorMittal, who was urging Europe to just go ahead already and declare trade on China asap. For his own selfish reasons of course.

On May 16 we are two weeks from the start of bond bubble collapse and it looks like nobody understand that danger. Kind of weak warning was famous Bill Gross: "We See Bubbles Everywhere " (and BTW he did withdraw some of his family fund money in May). Here is ZH write-up (Bill Gross We See Bubbles Everywhere Zero Hedge). But if you read attentively, it is clear that he iether does not understand the gravity of the situation or is trying to deceive the listeners:

It is only logical that when one of the smarter people in finance warns that he "sees bubbles everywhere" that he should be roundly ignored by those who have no choice but to dance. Because Bernanke and company are still playing the music with the volume on Max, and if not for POMO there is always FOMO. However, if there is any doubt why this "rally is the most hated ever", here are some insights from the Bond King from an interview with Bloomberg TV earlier today: "We see bubbles everywhere, and that is not to be dramatic and not to suggest they will pop immediately. I just suggested in the bond market with a bubble in treasuries and bubble in narrow credit spreads and high-yield prices, that perhaps there is a significant distortion there. Having said that, it suggests that as long as the FED and Bank of Japan and other Central Banks keep writing checks and do not withdraw, then the bubble can be supported as in blowing bubbles. They are blowing bubbles. When that stops there will be repercussions. It doesn't mean something like 2008 but the potential end of the bull markets everywhere. Not just in the bond market but in the stock market as well and a developing one in the house market as well."

As a gentle reminder, the reason why nobody anywhere trusts this particular bubble - the biggest in history - is not because speculators are not greedy (they are), or because everyone knows the market is always one central planner wrong move away from a collapse which would make the 2009 lows seem like amateur hour (it is), but because, as Seth Klarman explained two weeks ago, it is the Fed itself which by pushing on a string and the economy constantly deteriorating, proves it has no idea how to make things better:

"When you tell the populace that we can all enjoy a free lunch of extremely low interest rates, massive Fed purchases of mounting treasury issuance, trillions of dollars of expansion in the Fed's balance sheet, and huge deficits far into the future, they are highly skeptical not because they know precisely what will happen but because they are sure that no one else--even, or perhaps especially, the policymakers-does either."

And today from Bill, on the reason why QE is not working as intended, and why the Fed's channels are not only clogged but never worked as intended in the past four years: "Does it mean it is a good thing that capitalism should thrive under this quantitative easing posture on the part of central banks that distorts markets and this court's capitalism and promotes a zombie corporations and lowers net interest margins and destroys business model? All of that is the negative aspects of quantitative easing. Can we live with? I do not think this will be with us for a long time."

One can hope.

Some other observations from Gross:

On how distorted the bond marker is:

"It is easy on the bond side. We speak to an epical bond/bull market, not the beginning of a bear market but the ending of an epical bond/bull market show it in terms of a smiley face. It has been the investment committee.

The bright [left?] side of the smile is the thirty year bull market in which prices rise exceeded what rationally could have been expected. We are at the bottom basically of this smiley face and [in] our opinion on a long-term basis.

That means with treasury yields and credit spreads, importantly and here is the key to the bond market statement: treasuries are [overvalued?] 80 basis points, credit spreads are 70 basis points, put them together, 150 basis points in combination.

In our opinion, absent of an additional amount of quantitative easing treasuries will go down in yield because of slowing economy, but that will make spreads go up. This suggests a 20-Month time ahead in which treasury, corporate, and high yields do not move much. --[I wish this would be true ;-)]

[At] The end [right side?] of the smiley face all market run in terms of higher yields and lower prices is over[coming?].

On whether the conditions today are reminiscent of what we saw in 1992 and 1993:

"I do not think so, because in 1994 the FED raised funds dramatically to 200 basis points to basically slow things down. If the FED did that this time, I think they know with this amount of leverage there is two to three times more leverage in this economy this time than in 1994, the FED does not dare move in 200 basis point increments. That kind of market to our way of thinking is not in store for us. Does it mean it is a good thing that capitalism should thrive under this quantitative easing posture on the part of central banks that distorts markets and this court's capitalism and promotes a zombie corporations and lowers net interest margins and destroys business model? All of that is the negative aspects of quantitative easing. Can we live with? I do not think this will be with us for a long time. For the next 12-24, perhaps.

On when the Federal Reserve will start to taper the billions of dollars in bond purchases:

"It is almost a day-to-day thing in terms of the market but certainly not in the terms of the FED. They had objectives in terms of 6.5% unemployment and importantly, 2.5% inflation. We're down to 1 percent inflation in terms of the PCE which is their target for inflationary measure. To think the fed would begin to pull back in terms of tapering when inflation is approaching the Japanese levels of the lost decade is a big stretch. I do not think they change much. I think they have to be concerned about what happens in asset markets. Up until this point the chairman has done an Alan Greenspan and said cannot really relieve him as such but will monitor them in terms of potential regulation. However, having said that, I think the FED basically is on hold for a long time until unemployment and more certainly, inflation moves higher to the 2.5% target.

On the implications of the end of the 30-year bull market in treasury:

"It is not just treasuries. Treasuries, corporates, high-yield. We actually saw the end of the treasury market about six months ago. I think only a few weeks ago when you put the whole enchilada together, what does it mean going forward? It means as interest rates eventually go up, we do not think they are going up for 12 months or so, that the cost of interest for them move forward. And the portly, households will increase as well. Because of the lag effect in terms of the average cost of debt for corporations, and even government, there is a fair amount of room in terms of timing, even as interest rates move back up. Treasury yields on average are above 2%.

In terms of what they're issuing it is closer to 1%. Same thing in terms of relative magnitude on the front of corporatations and households. It will be a while until this "smiley face" where higher interest rates begin to affect corporations and the credit sector as well as the government sector in terms of the cost of leverage in the cost of borrowing. Eventually, a net interest margins narrow on the part of corporations because they will hire in terms of interest. Same things for households they pay higher for mortgage loans. That is two to three, four years out. We don't have to worry about it yet, but we have to worry about it.

On the great experiment and what is happening in Japan right now in the shift:

"We want to be able to monitor in the Tokyo office. They are in touch with the institutions in Tokyo. We want to be able to monitor where the money is going. Our sense is not much of it, some of it, is going outside the country. The metaphor for the Japanese small investor, Mr or Mrs. Watanabe, when she or he begins to sense there are more attractive yields outside of Japan and the Japanese Yen moving lower in the yields and lower in price that they can capture a higher total return by moving outside that is where they will go. We want to get in front of them so to speak. Where will they go? Typically they went to the Euro and bought a lot of France and Germany. Those markets we think our extended close to zero. Italy and Spain perhaps at the periphery. And back to the good ol' United States. We think it will buy treasury bonds at 80 basis points above the five-year and close to 1.90 or so for the 10-year treasury. It does not sound like a deal, but a much better field in Japan.

* * *

So to summarize: the great bond bull market is over, but Japan will buy everything about 1.90% on the 10 Year. Perhaps this is why, somewhat counterinuitively, Pimco has been buying up every Treasury it could find in the past 6 months, or around the time Pimco "saw the end of the treasury market about six months ago." Just in case someone takes Bill a little too literally.

As we can see not much insight. Here is some sarcastic comments from ZH

madbraz:Gross: "I closed my eyes during 30 years and was proclaimed the king of bonds just because I happened to be at the right place at the right time when yields were above 10% and have gone down since. Now that half a brain is required to figure out how things will turn out, I endlessly put out garbage in the media frightening people and making the worst calls one can make - after all, I sell bonds and now a bit of stocks and whatever happens I will be way fine - it's my clients that suffer.

I'm going out the Buffett way, idiotically proclaiming to know what is going to happen when I have absolutely no clue or if I do I just want you to keep buying my products."

ghostfaceinvestah

The malinvestment the Fed is fostering is enormous, I see it every day. When this turns, and it will turn, the crash is going to be epic.

buzzsaw99

Even Gross can't be this naive: When that stops there will be... When it stops? LMAO! And today from Bill, on the reason why QE is not working as intended... Come on Bill, it is working exactly as intended, making Buffett et al wealthier. The transmission is clogged? Please mutha fugga. Stopped reading right there. Bill is disingenuous at best.

Dr. Engali

Bill If I were you I would just retire. You had a good run, hang it up before you look any more ridiculous than you currently do. You're trying to prognisticate in an environment where everthing is manipulated and eventually there is only one way to go. I would love it if one of these big shots when asked the question " what do we doi?" ..would just say..the fed is printing buy the fucking dip! End of interview.

Actually Bill Gross also said:

"We see bubbles everywhere, and that is not to be dramatic and not to suggest they will pop immediately. I just suggested in the bond market with a bubble in treasuries and bubble in narrow credit spreads and high-yield prices, that perhaps there is a significant distortion there.

Having said that, it suggests that as long as the FED and Bank of Japan and other Central Banks keep writing checks and do not withdraw, then the bubble can be supported as in blowing bubbles. They are blowing bubbles. When that stops there will be repercussions. It doesn't mean something like 2008 but the potential end of the bull markets everywhere.

Not just in the bond market but in the stock market as well and a developing one in the house market as well."

|

|

Switchboard | ||||

| Latest | |||||

| Past week | |||||

| Past month | |||||

As evidence mounts that a mid-year slowdown is taking place in the world economy, the next few days will offer a clearer glimpse of how that will impinge on policymaking and buoyant financial markets.

... ... ...

Some poor business surveys from China have also had an impact, suggesting the world's No.2 economy is struggling for momentum.

... ... ...

"The underlying momentum in the global economy is weaker than it should be at this point of the economic cycle, five years after the global crisis," said Lena Komileva, director of G+ Economics consultancy in London.

"We have yet to see evidence of a convincing, self-sustained positive feedback loop between real growth and market value inflation."

... ... ...

Growth is still proving to be elusive for the euro zone economy, largely thanks to the extent of the budget austerity taking place across the continent.

... ... ...

Reuters

The average 401(k) retirement balance for U.S. workers hit a record high of $80,900 in the first quarter, a growth spurt of 75 percent since the stock market's nadir in March 2009, Fidelity Investments said on Thursday based on a survey of its accounts.

Most of the recovery is linked to a stock market rally that has lifted the broad S&P 500 Index 145 percent since the close of trading on March 9, 2009.

The 401(k) recovery looks even better for workers 55 and older, according to Boston-based Fidelity, the largest U.S. administrator of 401(k) retirement plans. Those pre-retirement workers have seen their average balance nearly double to $255,000 since the first quarter of 2009 when the average balance was $130,700. The analysis covers people who have been with their current employer 10 or more years, Fidelity said.

But a small percentage (1.6 percent) of pre-retirees have not seen as much of a rebound because they abandoned stocks during the tumult of the financial crisis. Their average balance grew only 26 percent to $101,000 over the same period, Fidelity said.

(Reporting by Tim McLaughlin; Editing by Bob Burgdorfer)

Reuters

The average 401(k) retirement balance for U.S. workers hit a record high of $80,900 in the first quarter, a growth spurt of 75 percent since the stock market's nadir in March 2009, Fidelity Investments said on Thursday based on a survey of its accounts.

Most of the recovery is linked to a stock market rally that has lifted the broad S&P 500 Index 145% since the close of trading on March 9, 2009.

The 401(k) recovery looks even better for workers 55 and older, according to Boston-based Fidelity, the largest U.S. administrator of 401(k) retirement plans. Those pre-retirement workers have seen their average balance nearly double to $255,000 since the first quarter of 2009 when the average balance was $130,700. The analysis covers people who have been with their current employer 10 or more years, Fidelity said.

But a small percentage (1.6 percent) of pre-retirees have not seen as much of a rebound because they abandoned stocks during the tumult of the financial crisis. Their average balance grew only 26 percent to $101,000 over the same period, Fidelity said.

(Reporting by Tim McLaughlin; Editing by Bob Burgdorfer)

Zero Hedge

Last week, Bill Gross did not mince his words when he said that he now "sees bubbles everywhere" and that "when that stops there will be repercussions" but for now Benny and the Inkjets, not to mention his band of merry statist men, who take from the poor and give to the wealthy, are playing the music on Max, and so one must dance and dance and dance. And after one legacy bond king, it was the turn of that other, ascendant one - Jeff Gundlach - to share his perspectives Bernanke's amazing bubble machine. His response, to nobody's surprise: "there is a bubble in central banking. We are drowning in central banking and quantitative easing.... And it's not ending until there are some negative consequences."

What are those negative consequences? This too should be perfectly expected for regular readers: currency devaluation leads to trade wars (as either is a zero sum game, and in a zero sum game it is very easy to blame someone else for one nation's suffering and economic malaise), trade wars lead to real wars (see the 1930s), and so on. We are not there just yet: quote Gundlach "With global growth slowing not everyone can increase their imports [indeed: observe just how it was that Spain managed to post its first "trade surplus" since 1971 - hint: not by boosting exports] you're playing a market share game." But it is rapidly approaching: "We are looking at competitive currency devaluations, which causes rancor, causes unhappiness, and fingerpointing and god-forbid tariffs and things that cause even slower economic growth a la the 1930s." Good choice of words, considering it was just a week ago that none other than stagnating metals magnate Lakshmi Mittal, head of ArcelorMittal, who was urging Europe to just go ahead already and declare trade on China asap. For his own selfish reasons of course.

Submitted by Lance Roberts of Street Talk Live blog,In Part III of Lance's series of reports from the 10th annual Strategic Investment Conference, presented Altegris Investments and John Mauldin, the question of how to invest during a deleveraging cycle is addressed by A. Gary Shilling, Ph.D. Dr. Shilling is the President of A. Gary Shilling & Co., an investment manager, Forbes and Bloomberg columnist and author - Mr. Shilling's list of credentials is long and impressive. His most recent book "The Age Of Deleveraging: Investment Strategies In A Slow Growth Economy" is a must read.

Here are his views on what to watch out for and how to invest in our current economic cycle.

Six Fundamental Realities

- Private Sector Deleveraging And Government Policy Responses

- Rising Protectionism

- Grand Disconnect Between Markets And Economy

- Zeal For Yield

- End Of Export Driven Economies

- Equities Are Vulnerable

Private Sector Deleveraging And Government Policy Responses

Household deleveraging is far from over. There is most likely at least 5 more years to go. However, it could be longer given the magnitude of the debt bubble. The offset of the household deleveraging has been the leveraging up of the Federal government.

The flip side of household leverage is the personal saving rates. The decline in the savings rate from the 1980's to 2000 was a major boost to economic growth. That has now changed as savings rate are now slowly increasing and acting as a drag on growth.

However, American's are not saving voluntarily. American's have been trained to spend as long as credit is readily available. However, credit is no longer available. Furthermore, there is an implicit mistrust of stocks which is a huge change from the 90's when stocks were believed to be a source of wealth creation limiting the need to save.

My forecast for GDP growth going forward is that it will remain mired around 2%.

The response to the stalled economic environment and deleveraging cycle has been massive government interventions. The Fed's original program of zero interest rates have failed to promote borrowing. The next step was unprecedented Quantitative Easing.

The Fed's dual mandate is full employment, currently targeted at 6.5%, and price stability (inflation) around 2%. The Fed has been very clear that the current QE programs are directly tied to these targets. However, monetary policy is a very blunt instrument, but the Fed believes that it will work within a 5 step process.

- The Fed buys treasuries and mortgage bonds out of the market.

- The increase in liquidity is then reinvested into the equity market.

- The rise in asset prices creates a wealth effect for consumers.

- With stronger confidence consumers spend more which creates demand on businesses.

- The increase in demand leads to job creation.

The problem is that there is little evidence that Q.E. programs are fulfilling their intended role.History is not a controlled experiment. There is no way to tell what would have really happened had the Fed not intervened after the financial crisis.

However, what we can absolutely measure, is the impact of the Fed's activities on the economy. If we measure the increase in real GDP for each dollar of increase in debt we find that it has been close to nil. From 2001 through the end of Q2-2012 – we find that there has been only a 0.08% increase in real GDP per dollar of increase in debt.

While the economy has failed to ignite - there has been a sharp surge in market capitalization as a percentage of nominal GDP. Currently at levels well above the long term average it is unlikely that this is the beginning of the next great secular bull market.

The bottom line is that despite trillions of dollars of Federal Reserve interventions there has been very little impact on the real economy. This is because there has been very little follow on effect from the massive increases in excess reserves. Historically required reserves have remained fairly close to the level of excess reserves. However, today, excess reserves are running roughly $1.7 trillion above the level of required reserves. Liquidity remains trapped which is why there is no velocity of money in the economy.

Growing Protectionism

The problem today is that everybody wants to increase exports to boost their respective economies - but no one wants to, or is able to, buy. This has pushed countries into the need to take more drastic actions to stabilize and boost their economies. This has led to currency devaluation schemes.

Japan is the poster child to currency devaluation. They have gone "all in" to debase their currency in hopes that they will create some inflation. For Japan it is "go big or go home."

It is important to note that NO ONE ever initiates currency devaluation – they are just trying to get back to even.

Currently, the head of the central bank in Japan, has the backing of the country. This will allow him to operate and continue his stimulative actions. The tipping point will be when he loses this approval.

However, while Japan is currently happy with their direction, other countries are not. Eventually there will be a reprisal.

The Great Disconnect

"Don't worry about a thing as long as the Fed is inflating assets and the economy is in the tank."

Nobody wants to end the current Q.E. programs. What it will take is an economic shock of some magnitude. What type of shock it will be, and when it will occur, are the only questions?

Here is the simple truth: Stocks will eventually revert to the fundamentals of the economy. Such a reversion will devastate most investors that are unhedged for that eventuality.

Zeal For Yield

The chase for yield has reached excessive levels. Despite the rising risks individuals continue to ignore the fundamentals and reach for ever increasing levels of yield.

Junk bonds, emerging market debt and bank loans are at record low levels in yield. The yield on stocks and bonds are equal for the first time in decades. This is an indication of a late stage bull market. It is also one that has historically ended badly for investors.

End of Export Driven Growth In Developing Countries.

The demand for exports is slowing as the major developed countries are weak and demand slackens.

(Note: This was seen in the latest trade deficit report as imports for the U.S. plunged sharply last month. In other words the demand for products from other exporters is slowing which negatively impacts their economies.)

As Jeff Gundlach discussed earlier – China's growth rate is slowing. However, no one really trusts the data coming out of China. It takes China 18 days from the end of the quarter to report GDP. It takes the U.S. 28 days. China never revises their data subsequent to that first report while the U.S. revises its data two more times over a 90 day period. The data is extremely unreliable. For instance, how do you have a flat manufacturing report coming out of China, as measured by Markit PMI, when they supposedly have a 7.7% GDP growth? That simply does not add up.

Going forward emerging economies are focused on creating internal growth to offset the drag from slowing export growth. This will likely lead to problems.

Equities Are Vulnerable

We are still within a secular BEAR market that begin in 2000 with P/E ratios still contained within a declining trend. Despite media commentary to the contrary - this time is likely not different.

In order for valuations just to return to the long term average they would have to decline by 27.5% from current levels. However, the reality is that valuation reversions always exceed the long term mean.

Furthermore, corporate profits have only soared due to declining labor costs and increased productivity. The problem now is that there is an inability to slash costs and increase productivity at levels that can offset the decline in operating earnings and revenue.

This makes equities susceptible to a large reversion at some point in the future.

2013 Investment Themes

"Economists are like lookouts at the house of ill-repute. They are kept away from the action but good to have when the cops arrive."

The risk on trade is alive and well - but will not last forever. Therefore, the following is what I find attractive and unattractive in the current environment.

Attractive.

- Treasury Bonds

- Quality Bonds And Dividend Stocks.

- Small Luxuries

- Staples And Food.

- Dollar Vs Yen, Long Nikkei

- Selected Healthcare Providers And Medical Office Buildings

- Productivity Enhancers – Things That Help Businesses Lower Costs

- North American Energy Producers Excluding Renewables

Unattractive

- Developed Country Stocks

- Homebuilders And Related Companies

- Your House

- Big Ticket Consumer Discretionary Stocks

- Consumer Lenders

- Selected Banks

- Junk Securities

- Developing Country Bonds And Stocks

- Commodities

- Old-Tech Capital Equipment Producers

Q&A

Austerity Or Stimulus – What Should We Be Doing?

If you don't get austerity when things are tough you will never get it. This is the problem in Germany.

In the U.S. – Congress has it completely backwards. They should be working on structural deficits rather than fiscal deficits. Change retirement ages, etc. rather than trying to inflate assets.

GDP less inventories is much weaker. Inventories are a residual of activity and small changes on either end have a big impact on the economic figure.

What Happens?

The great disconnect will reconnect over the next couple of years which will negatively impact long only investors.

The Fed Reserve – Does The Fed Have To Exit?

That is an interesting point. With slow growth, which will continue due to the ongoing deleveraging cycle for another 5 years, it is likely that the Fed will not try any exit. However, when the economy begins to reach higher levels of growth in the future the excess reserves will begin to flow into the system. If the Fed doesn't exit from their policies when that occurs the impact of inflation could be severe.

May 18, 2013 | Zero Hedge

We feel that now there is a Bermuda Triangle of economics - a space where everything tends to disappear without radar contact, a black hole in which rationality and science is replaced by hope, superstition and nonsense pundits pretending to understand the real drivers of the economy.

The Bermuda Triangle in real life runs from Bermuda to Puerto Rico to Miami. The Economic Bermuda Triangle (EBT) one runs from high stock market valuations to high unemployment to low growth/productivity. There is a myth that the sunken Atlantis could be in the middle of this triangle. It has been renamed Modern Monetary Theory (MMT) to make it suit the black hole's main premise of ensuring there is a fancy name for what is essentially the same economic recipe: print and spend money, then wait and pray for better weather.

The EBT is getting harder and harder to justify - if for nothing else because the constant reminders of crisis keep us all defensive and non-committed to investing beyond the next quarter. We all naively think we can exit the "risk-on" trade before anyone else.

We are due for a new crisis. We have governments and central banks proactively pursuing bubbles. A long time ago, policymakers entered a one-way street where reversing is, if not illegal, then impossible.

Jesse's Café Américain

In my opinion Bernanke is literally fighting a new kind financial crisis, of the Fed's own making, with the last war's tactics and weapons, in the manner of the French generals at the beginning of the Second World War. Therefore the next crisis could be quite impressive and pervasive, affecting sovereign debt and currencies to an even great degree than the last two or three bubble/crises, depending how one is keeping score.

The failure points, or limits if you will, are the valuation of the bonds and the US dollar. And Bernanke looks to be giving those limits, and the theories of risk and valuation therein, a rather rigorous stress test.

"At 85 Billion a month, massive amounts of liquidity are driving the markets higher each day. While we are closely watching the FED for signs of an exit strategy, I heard a very interesting piece from David Tepper at Appaloosa Management this morning that put todays markets in a much better perspective. According to David, The FED will have a 368 Billion dollar surplus this year! That is 368 Billion in more liquidity that "has to go somewhere".

With the Dow and the S&P 500 trading at or near all time highs and 10yr paper trading at historic lows, you would think that we have run our course and we may want to pull some money off the table. Think again? Do you fight the FED? Do you create the MOAS? (Mother of all shorts)….Or do you stay long?

In this chart, we look at the Equity Risk Premium Index versus the DJIA, S&P 500 and the US 10yr to 1885. The red line represents the Equity Risk Premium Index and by all accounts, looks like it is ready to breakout and make a move to new highs.

Provided that the FED follows through to 2014 with the QE program, one would have to assume that the respective equity indices will all move higher with the massive amounts of liquidity that are in the pipeline. That has proven wise, as long as the FED stays your partner.""

Posted by Jesse at 2:01 PM

Zero Hedge via Cyniconomics blog

Benefits and risks of extreme monetary stimulus

Firstly, the benefits of existing policies are well understood. Monetary stimulus has certainly contributed to the meager growth of recent years. And jobs that are preserved in the near-term have helped to mitigate the rise in long-term unemployment, which can weigh on the economy for years to come. These are the primary benefits of monetary stimulus, and I don't recall any hedge fund managers disputing them.

But the ultimate success or failure of today's policies won't be determined by these benefits alone – there are many delayed effects and unintended consequences. I'll describe seven long-term risks that aren't mentioned in DeLong's article, replacing his made-up world with messages from professional investors (h/t ZeroHedge for many of the links).

Risk #1 – Inequality and social injustice. The Fed's current stance continues an entrenched pattern of public policies that favor the wealthy, in general, and bankers, in particular. I've always been puzzled as to why DeLong and other economists who revere John Maynard Keynes are so often silent on this basic issue of fairness. Keynes called for policies to lower interest rates and squeeze out the "rentier" class – those who live off their wealth. But today's situation is totally different to the interwar period during which Keynes produced his most famous work. The effects of interest rate changes on the distribution of wealth have completely reversed.

Wealthy classes are best characterized today as risk-takers and have profited immensely from both low rates and QE. But we now have a vast middle class that relies on adequate bond yields to fund retirement. And current policies are disastrous for these middle class retirees (and near retirees). If Keynes were alive today, he would have surely adjusted his message to account for the fact that low rates are no longer an egalitarian policy. His followers, on the other hand, seem happy to stick to the old script.

And not only do recent policies have insidious social effects, but they also have dangerous economic effects. Lawrence Fuller of Fuller Asset Management recently discussed these effects and summarized them like this: "The real economy is horrid for the vast majority of Americans. The Fed's deluge of credit has disproportionately benefited those who didn't need assistance in the first place. As a result, the cracks in the foundation of our economy are beginning to show up in the macro-economic data."

Risk #2 – Banking crises. Did DeLong consider the impetus for JP Morgan's London Whale trades before writing his article? If so, he would have recognized that funding costs for JPM's CIO office (where the Whale worked) are at record lows, thanks to the Fed. Moreover, JPM knows from its Bernanke (and Greenspan) experiences that whenever anything goes wrong in the financial sector, the Fed saves the day.

These facts surely had something to do with Jamie Dimon's encouragement of hugely risky bets in credit derivatives, which showed that the last decade's excessive risk-taking remains alive and well. And as long as risk-taking persists, so does the possibility of a brand new crisis. There's more than a little irony in DeLong's decision to link JPM's ill-fated derivatives bets to his defense of monetary policy. Presumably, it was unintentional.

What's more, it's possible that the next banking crisis will be more sudden and damaging than the last, especially as a portion of the private sector's leverage has been transferred to the public sector rather than being extinguished. Paul Singer links the risk of a more severe crisis to the lessons learned in 2008, Dodd-Frank provisions that reward creditors who bail out early, and the continued impossibility of extracting accurate risk information from bank balance sheets. Here's an excerpt from a speech that Singer delivered last year:

… if you are observing a large company getting into trouble, what you know is that you have to pull your assets because those assets can be transferred … You don't know how your claim will be treated, so you have to sell the bonds that you own … So the whole thing militates toward stepping away abruptly from any company that is designated as systemically important. So I think that the opacity, the lessons of '08, the vicissitudes and thoughtlessness of Dodd-Frank, militate in favor of a very, very abrupt resolution.

Risk #3 – Public debt-related risks. Skyrocketing public debt can have a variety of unwelcome consequences, contrary to what you may hear from exuberant Reinhart-Rogoff smear campaigners, whom I wrote about here and here. Nor will you hear about these unwanted effects from DeLong, who ignores fiscal policy risks just as studiously as he ignores monetary policy risks. His academic work on fiscal policy is based on the assumptions that debt can rise without limit (trillions, quadrillions, quintillions, you name the number and it's achievable according to DeLong's model) and stimulus can be applied without ever needing to counterbalance it later with restraint. (Read here for more detail.)

The connection to monetary policy is that there's little incentive today for politicians to take serious action on the debt. In the current political calculus, deficits don't matter as long as they can be funded for a pittance, and Fed policies have reduced funding costs to exactly that – a pittance. Kyle Bass said it clearly last year, noting that when he challenges congressional leaders on their poor fiscal habits, they tell him to look at the 10-year.

People may forget that we once had a central bank that fought hard for fiscal discipline. While he was busy crushing inflation and ushering in a multi-decade period of stability, Fed Chairman Paul Volcker essentially told Congress and the Reagan Administration (while publicly denying it): No deficit reduction, no changes in monetary policy.

Consider these accounts from William Greider's Secrets of the Temple:

Reagan's OMB Director David Stockman: "Volcker was telling everyone, 'If you give us some relief on the deficits, it will take some pressure off … Our hands are tied unless you give us some relief on the fiscal side."

Influential Congressman and Reagan tax cut champion Jack Kemp: "Monetary policy is deliberately being kept unnecessarily tight and the economic expansion held hostage to a tax increase … Mr. Volcker would offer a quid pro quo of monetary ease and lower interest rates in return for a fiscal policy of higher taxes which is more to his liking."

Notably, these discussions occurred during and after a deep recession. But Bernanke's Fed has chosen to abet rather than limit our soaring national debt, rejecting Volcker's approach. Bernanke's methods lessen the immediate debt burden, while likely increasing the costs that we'll have to bear in the future. And history has shown again and again that these costs can be devastating.

Risk #4 – Extreme economic volatility. It shouldn't be surprising that the investment community is intently focused on the eventual "exit" from extreme monetary stimulus. Just as history has proven the risks of excessive public debt, it also shows that bad things tend to happen when policy swings from stimulus to restraint. When you remove stimulus, expansions have been more likely to end than continue, as I showed here.

In the case of monetary stimulus, the Fed could eventually find itself between a rock and a hard place. Zero interest rates and strong growth aren't compatible with the price stability portion of its mandate, whereas rising rates usually tip economies back into recession. At some point in the future, the Fed may be confronted with only those two options. And the longer it chooses to "beat a donkey (a 1% growing economy) for not being a horse (a 3% growing economy)," to quote Jeremy Grantham, the likelihood of such a lose-lose scenario increases.

Grantham's grasp of economic reality contrasts sharply with DeLong's advice, which is rooted in recession-free economic projections such as those of the Congressional Budget Office (CBO). DeLong's approach helps to preserve a long academic tradition of ignoring the economy's natural cyclicality, assuming instead that economies revert to a "full employment equilibrium" and then stay there. With this assumption, the case for stimulus during recessions is usually stronger than it would otherwise be. But unfortunately, such a world doesn't exist outside the economics profession.

Risk #5 – Credit crises. When you choose to fight a debt crisis with more debt, insolvency risks are unlikely to normalize for very long. And if these risks aren't priced properly because, say, markets are manipulated by public officials, a fresh crisis could be closer than you may have thought. This was essentially the threat discussed in February in a speech by Fed Governor Jeremy Stein, who created a stir with his analysis of incipient credit risks. DeLong makes a cryptic reference to Stein in his whale of a tale article, perhaps to hint that he doesn't share Stein's concerns. If that's indeed the case, DeLong must have decided that insolvency risks are too insignificant to discuss.

What could possibly go wrong with such complacency?

To pick just two sectors: Does he realize that today's volumes and delinquency rates for student loans aren't that different to the figures for sub-prime bonds as of 2006/07? Has he looked at the high yield bond risks discussed by Stein, especially as the Barclay's high yield index shattered records this month by yielding less than 5%? As far as I can tell, DeLong's analysis extends no deeper than his cryptic references (if I'm wrong about this, please send me the research), and these aren't especially helpful.

Risk #6 – Asset price bubbles. One way to approach asset valuation is to break it into three pieces:

- What are the expected cash flows?

- How much are you paying for those cash flows?

- How does the IRR implied by #1 and #2 compare to an appropriate benchmark interest rate?

Applying this approach to U.S. stocks, the market peak in 2000 was explained mostly by changing perceptions about question #2 – investors finally accepted that they were paying too much. The peak in 2007 was explained mostly by changing perceptions about question #1 – investors were reminded that corporate earnings tend to mean revert (with especially big adjustments in the financial sector). At the next peak, we may find that changes in the answer to question #3 are the driving force. The trigger would be an increase in benchmark interest rates.

In fact, this risk is baked into the Fed's argument that its policies stimulate the economy through the portfolio balance channel – their jargon for buying so much of a few assets (Treasuries and mortgages, in this instance) that you push up the prices of all assets. It goes without saying that the portfolio balance channel works in both directions. When the benchmark assets turn around, so does everything else. Stanley Druckenmiller memorably described these asset pricing risks in a recent interview with an incredulous expression and this pair of rhetorical questions:

The thought that you can exit by wherever the balance sheet will be at that time – $4 trillion or wherever it is – in an orderly manner … Do you know what guys like me are going to do when they sell the first bond out of $4 trillion? And don't think that letting the bonds run off isn't selling. That debt has to be refinanced. If you just let all the bonds run off, that is still $4 trillion in selling … What do you think the markets are going to do when they figure out the exit?

And by the way, projected cash flows and prices (questions #1 and #2 above) are also showing some signs of froth. Maybe in the same way that froth was apparent in 1997 or 2006, several years before the respective peaks, but froth nonetheless.

Risk #7 – Real economy distortions. You'll rarely find Keynesian economists such as DeLong discussing the unintended effects of public policies on private decision-making. But just like the other risks listed above, these effects should never be glossed over. In the case of the Fed's extreme stimulus, one of the most obvious consequences is that business people are incented to exploit artificially low interest rates through purely financial strategies. These are typically short-term strategies that lock in a yield difference.

On the other hand, the Fed may be discouraging capital spending on tangible, long-term investments. Unlike many yield-based strategies, capital spending decisions are subject to the additional uncertainties of the eventual exit from extreme stimulus. Bloggers popular in the investment community, such as Tyler Durden, have long written about this risk. Here are Bill Gross's thoughts, lifted from a client letter that was published on ZeroHedge in January:

Zero-bound interest rates, QE maneuvering, and "essentially costless" check writing destroy financial business models and stunt investment decisions which offer increasingly lower ROIs and ROEs.

Purchases of "paper" shares as opposed to investments in tangible productive investment assets become the likely preferred corporate choice. Those purchases may be initially supportive of stock prices, but ultimately constraining of true wealth creation and real economic growth. At some future point, risk assets – stocks, corporate and high yield bonds – must recognize the difference. Bernanke's dreams of economic revival, which would then lead to the day that investors can earn higher returns, may be an unattainable theoretical hope, in contrast to a future reality.

Spotting the real villain in DeLong's article

Getting back to DeLong's article, his "Bernanke-haters" really don't have to share their fiscal and monetary policy concerns with the general public. They certainly haven't done this out of frustration with losing trades. At least two of the three managers whom he cites (in the separate post that refers to Druckenmiller, Bass and Singer) have been on the record with accurate predictions that Fed-fueled market rallies were likely to continue for some time. DeLong's claim that these managers have probably "spent years shorting Treasuries" is preposterous.

The real reason that we hear from these hedge fund managers is their exceptional track records. The media realizes that they've shown a remarkable understanding of economic risks, and therefore, their opinions are widely reported. They haven't necessarily sought an audience, but they've certainly earned one.

DeLong, on the other hand, epitomizes an academic community that regularly gets blindsided by real life events. It's a shame that they claim authority on economic issues, because we all suffer when their abstract theories blow up in their faces as happens time and again. This is yet another reason that we should call foul when we see an irresponsible piece of fantasy like DeLong's article.

Now sure, I can understand why he wrote it the way that he did. Is there a better way to fire up your acolytes than by wrapping a clever little rant around a popular villain? According to DeLong's crowd, hedge funds are about as villainous as they come. And this crowd was beside itself with glee as they spread the word about the whale of a tale. Check out the tweets noted above and you'll see that the comments following them were full of giddy, backslapping fun and many happy contributions from DeLong himself.

But to me, the shoddy quality of DeLong's work buries his wit. It's nice to have camaraderie, but we all know that people are capable of some pretty ugly camaraderie.

In my opinion, DeLong and his joyful followers are once again behaving like a pack of fools. And he once again made a mockery of the header for his website. Beneath the simple title, "Brad DeLong," his tagline reads "Grasping Reality with Both Invisible Hands: Fair, Balanced, and Reality-based."

As I said, DeLong may have been grasping for some Twitter love with his whale of a tale, but he certainly wasn't delivering reality, fairness or balance.

Economist's View

One thing I learned from the recent crisis is that despite my indifference to the day to day gyrations in asset markets, I need to pay more attention to them. For example, is there presently a bubble in stock market prices?

Antonio Fatás argues that it's a difficult to find evidence for this:

Let's get real about the stock market: As reported by the financial press, the stock market continues to hit fresh record-high levels in many advanced economies. The Dow Jones passed the 15,000 mark, the Nikkei just went over 14,000, and the DAX just went above its previous record. It seems to be the time to talk about bubbles in asset prices - an important issue given how these bubbles have dominated the last business cycles in these economies.Except that we are looking at the wrong numbers. It is remarkable that the discussion on the value that these indices are reaching ignores two fundamental issues:

- These are nominal values and as we were told in the first economics lesson, we need to look at real variables and not nominal ones.

- Asset prices are not supposed to stay constant (in real terms). In many cases its appreciation will reflect real growth in the economy, earnings and/or the expected return that these assets should provide in equilibrium.

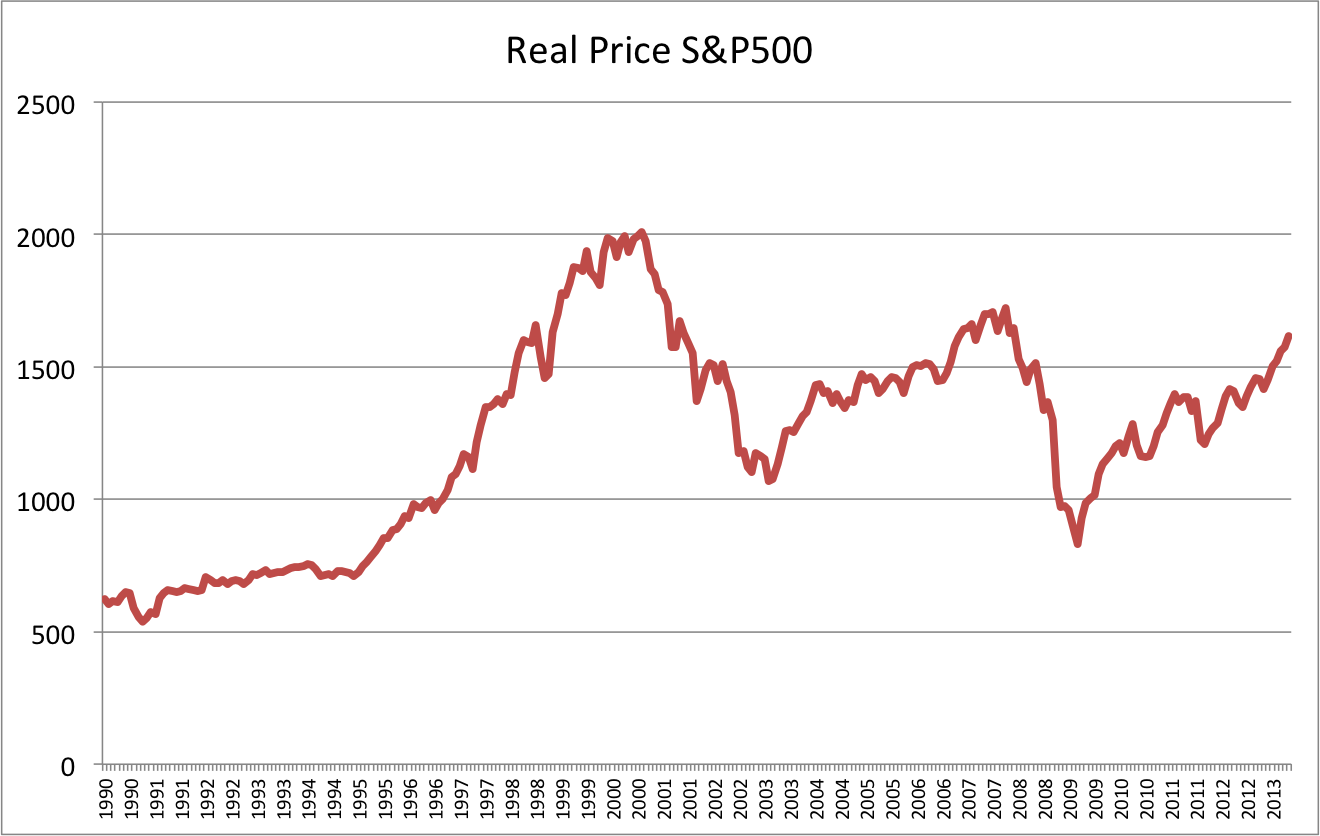

No need to look for data that provides a better benchmark than just nominal indices. Robert Shiller provides all the necessary data in his web site. Adjusting for inflation is easy and below is a chart with the real price of the S&P500 index where the CPI has been used to convert nominal into real variables.

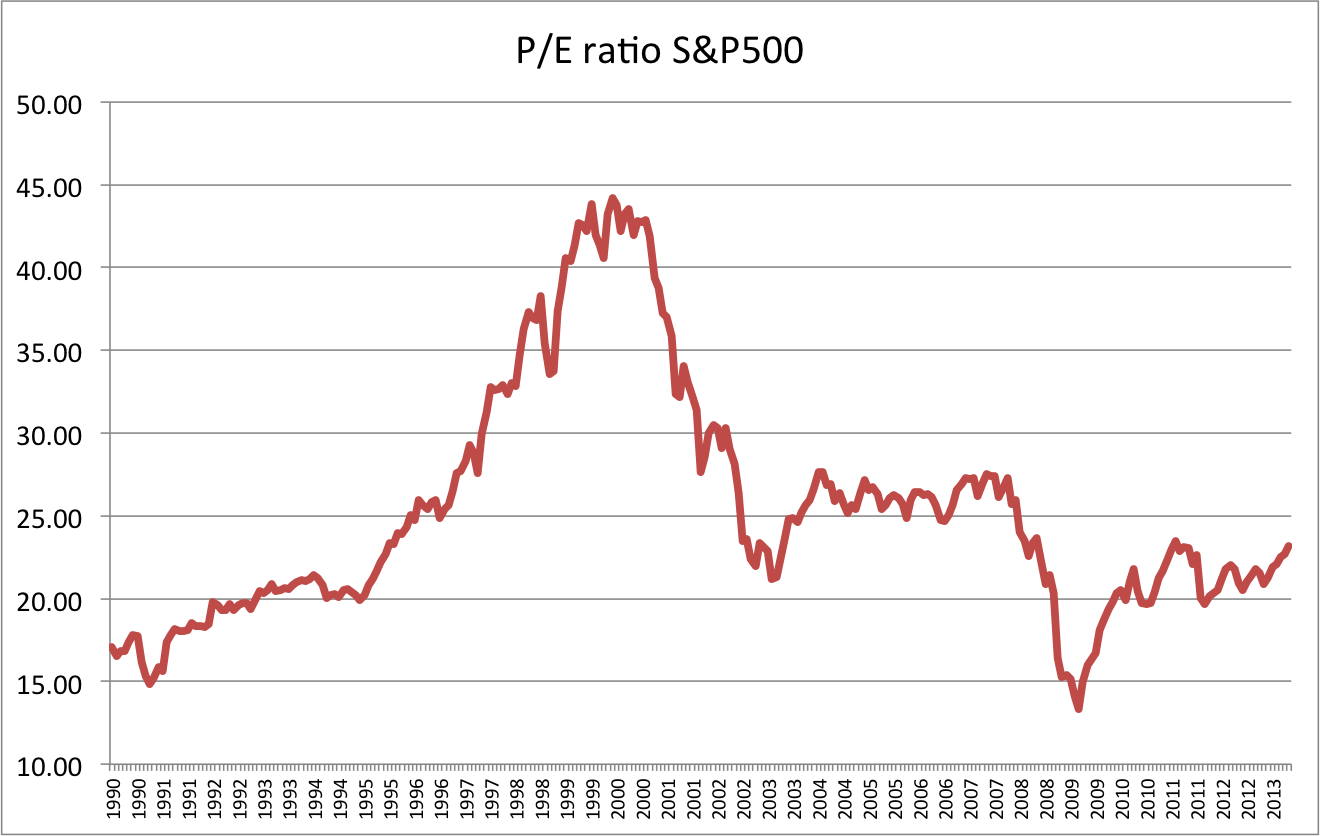

After adjusting for inflation we can see that the index is far from its peak in 2000 and it is even below the peak in 2007. No sign of a record level yet.Adjusting for inflation is not enough as the fundamentals (earnings) also grow because of real growth. The price-to-earnings ratio takes care of this adjustment (it also takes care of inflation because earnings are measures in nominal terms). Making this adjustment is more difficult but I will reply on Shiller's numbers again (his book and writings provide a lot of detailed analysis on his data).

Once we adjust for nominal as well as real growth, the current levels look even less impressive. Very low compared to the bubble built in the 90s and significantly lower than the ratio observed in most of the years during the 2002-2007 expansion. We are very far from record-high levels if we use this indicator.Of course, to do a proper analysis we need to bring a lot of other factors: expected earnings growth, interest rates, risk appetite,.... And there will be room there to debate whether the current valuation of the stock market is reasonable, too high or too low. But starting the analysis with a statement of record-high levels when measured in nominal terms and ignoring real growth in earnings is clearly the wrong place to start the debate.

For more on stock prices, see Fernando Duarte and Carlo Rosa of the NY Fed: Are Stocks Cheap? A Review of the Evidence:

We surveyed banks, we combed the academic literature, we asked economists at central banks. It turns out that most of their models predict that we will enjoy historically high excess returns for the S&P 500 for the next five years. But how do they reach this conclusion? Why is it that the equity premium is so high? And more importantly: Can we trust their models? ...SUTM said...Why is the equity premium so high right now? And why is it high at all horizons? There are two possible reasons: low discount rates (that is, low Treasury yields) and/or high current or future expected dividends. ... We find that the equity risk premium is high mainly due to exceptionally low Treasury yields at all foreseeable horizons. In contrast, the current level of dividends is roughly at its historical average and future dividends are expected to grow only modestly above average in the coming years. ...

Patrick said in reply to SUTM...The question is really whether QE is creating investment bubbles or a platform to launch the economy.

This is a diagram of the S&P index versus QE.

http://moneymorning.com/images2/Fed-Folly-3-425.jpg

It appears when QE stops then the market falls.

The question is whether QE will be allowed to stop and if it runs for too long then there could be an asset crash.

---------------------------------------------------------

Using inflation moderation along with PE multiples etc etc etc... Negates the whole concept of the marketplace. The market is neither under or over valued if the information is reasonably perfect.

What will happen is sophisticated investors will start cashing out and looking for other investments. So, in some ways the best indicator of whether the market is overvalued is to watch the changing portfolio mixes of institutional investors. (I.e. If too many private investors pile into the market).

anne said in reply to SUTM..."The market is neither under or over valued if the information is reasonably perfect."

You're subscribing to the strong efficient market hypothesis here. The evidence for this is pretty slim.

"Using inflation moderation along with PE multiples etc etc etc... Negates the whole concept of the marketplace."

Even in a world of the strong EMH we would need to correct for inflation. Even though the market would be constant, the value of our dollars may increase or decrease, so when we evaluate the market price in dollars(or indices based on dollar prices) we need to apply this correction.

Mark A. Sadowski said in reply to SUTM...So, in some ways the best indicator of whether the market is overvalued is to watch the changing portfolio mixes of institutional investors....

[ There is no evidence I know of that institutional investors can effectively time the stock market or that institutional managers are more successful than than index fund investors. All the evidence I know of is that institutional returns trail index returns by management cost.

As for watching changing portfolio mixes of even fine institutional managers, how? ]

anne said in reply to Mark A. Sadowski..."The question is really whether QE is creating investment bubbles or a platform to launch the economy."

One way of quantifying large scale asset purchases, or "QE", is to look at the size of the monetary base. Since 2009 the correlation in levels between the the monetary base and stock market indicies has been exceptionally strong:

http://research.stlouisfed.org/fred2/graph/?graph_id=120227&category_id=0

If there's any comfort there is a historical precedent for this.

During the Great Depression interest rates and the velocity of money also dropped (what some call a "liquidity trap"). Shortly after FDR took office as President in March 1933 he abandoned the gold standard, eventually devaluing the dollar. This led to gold inflows and an extraordinary increase in the monetary base. This was essentially the "QE" of its day.

The stock market soared and the correlation in levels between the monetary base and stock market indicies became unusually strong, and lasted at least until the recession of 1937-38:

http://research.stlouisfed.org/fred2/graph/?graph_id=120229&category_id=0

After the 1937-38 recession the monetary base continued to increase to enormous levels relative to GDP during the 1940s, before declining to more normal levels in the post WW II era:

http://research.stlouisfed.org/fred2/graph/?graph_id=112896&category_id=0

However, the correlation between the monetary base and the stock market had weakened, and eventually disappeared altogether as the economy fully recovered.

acerimusdux said...Dean Baker, who I always pay attention to, thinks that the difference between actual and potential GDP that presently exists will allow for significant increases in corporate earnings from here so that stocks can be expected to return about the long term average even though the Shiller valuations are historically high at present:

May 7, 2013

Moody's Get Faddish on Public Pensions

By Dean BakerIt's not a bubble from a value perspective, but I think there may be one forming from a psychological perspective.

I think we have been in a secular bear since 2000, and previous such bears have tended to run for 15-20 years. I'm not convinced we're ready to break out from this one after only 12. I don't think the volume will be there to support that. Also, previous secular bears have resulted in exceptional buying opportunities before breaking free. I don't think we're quite there yet. In addition, after a 4 year bull run, I think the market is going to run out of steam. The market made new highs at the end of 2007 as well, before dropping through 2008.

Very tough to call this with certainty, though. I really like it when a value analysis and technical analysis point in the same direction. Much harder call here when the valuation says buy and the technicals say it's due for a drop. It could be better to follow Buffet and not try to time it. But I will anyway.

Recent economic news has been positive, helping to extend the run. But two things can go wrong now. One, the economic news could turn. The other, continued economic strengthening could lead to an end to quantative easing, which obviously has functioned through supporting asset prices.

On Saturday, Buffett said he stood by the actions taken by the U.S. Federal Reserve, even as he cautioned the Fed's program could be "very inflationary."

"This is like watching a good movie, and I do not know the end," said Buffett. "We have benefited significantly, and the country has benefited significantly, by what the Fed has done."

Earlier Saturday, one of Buffett's top lieutenants said things were picking up but could improve further.

"It feels like a 2 percent economy. If we want to see GDP click up to 3.5 percent, 4 percent, you need to see more consumption," said Rose, CEO of the railroad Burlington Northern, in an interview.

Rose said BNSF was seeing "across the board" increases in demand to ship things like concrete, roofing tiles and cars.

Shiller says the housing market is operating in an "abnormal economy" where the Federal Reserve is buying $40 billion worth of mortgage securities and $45 billion worth of Treasury notes each month. This has driven mortgage rates to record lows.According to Freddie Mac's weekly survey out last Thursday, the average rate for a 30-year fixed rate mortgage is a record low 3;4%;

The Fed will eventually stop buying these securities, says Shiller, and mortgage rates will rise.

Shiller, also an economics professor at Yale University, says the biggest home price increases now are seen in multifamily rather than single family homes which reflects a shift from home ownership to renting. The buyers are investors who rent their properties.

"Most of the increase in households in this country has been met by an increase in renting," says Shiller. "My own survey data with Chip Case confirms that people feel more positive about renting." He suggests that those investing in real estate buy homes that are most suitable to convert to rentals.

Another shift that Shiller observes in the housing market is the growing popularity of urban areas and suburbs near those areas.

Shiller says people don't want to commute long distances because of relatively high gasoline prices and in the current "ideas economy," many want to live in close proximity to others.

There are also demographic shifts: aging baby boomers who no longer enjoy working on the upkeep of their homes and the increase in single-person households.

When asked where this all leaves the housing market 10 years from now, Shiller says home prices will be "about where they are now" after adjusting for inflation.

The Fed dispelled any illusions about ending QE early in their statement today. The chill passing over the economy has quite a bit to do with it. But the Fed will keep doing what they are doing until something improves or breaks, because they are locked into an obsessive compulsive box by the credibility trap of their own past policy failures and conflicts of interests. So expect another bubble and crisis.

ADP employment numbers came up short, and that impinges on expectations for the Non-Farm Payrolls report on Friday.

National ISM was aenemic, but not quite a contraction. But it was enough to show that 'The Recovery' is no recovery.

Intraday commentary about the Fed statement here and the bubble environment caused in part by the Fed here. Please be sure to listen to Jeff Sachs entire speech and the Q&A session here, and recall that he was speaking to a conference at the Philadelphia Fed. Every time I listen to it I am astonished that it did not get a wider exposure, and nary a mention in the mainstream media. Sachs is no outsider, and hardly a starry eyed reformer. The venal stupidity of those in command is frightening even to longer term stalwarts.

I think it will take another financial crisis, and even more scandals and revelations. And I will be surprised if there are any lack of any of them, despite the war on whistleblowers and the muzzling of the media.

Many market strategists credit the Federal Reserve with the rally that has pushed the Dow and the S&P 500 to record highs.

The near-zero interest rate policy of the U.S. central bank coupled with millions of dollars worth of asset purchases monthly has essentially swelled liquidity in the market, and those funds have to find a home.

With the 10-year Treasury yield well under 2% and an economy in (a sluggish) recovery, investors have been pouring money into the U.S. stock market.

The Fed may have been the catalyst for the start of the stock rally but, according to Mohamed El-Erian, CEO of Pimco which runs the world's largest mutual fund, "the latest surge is really not on the back of the Fed but the Bank of Japan."

In early April Japan's central bank announced a massive program of monetary easing that would double the country's money supply and target a 2% inflation rate-all in an effort to once and for all slay the deflation dragon that has plagued Japan for at least a decade.

Fed officials are meeting today but no change is expected in Fed policy when the bank issues its latest policy statement at 2pm ET.

J

The rally is not unloved! We ALL THINK the MARKET is full of CHEATS who manipulate pps, create fake volume and colluded with market analyst and brokers.

You know that already and fail to mention the TRUTH about market sentiment towards it.

RacerX

It's called ZOMBIE economics... the real economy is dead and lives only via endless QE.

NN

Fed Is Artificially Inflating Asset Prices in "Most Unloved Market Rally" It is nothing more than a house of straw, almost anything could cause the entire thing to come tumbling down. And, with all the Federal 'Administrations' attention on growing the Government, the Private Sector is literally being robbed, with dollars (trillions) being syphoned into the Federal Government.

Todd

"The near-zero interest rate policy of the U.S. central bank coupled with millions of dollars worth of asset purchases monthly has essentially swelled liquidity in the market, and those funds have to find a home."

The monthly number is 85 BILLION not millions BILLIONS!

Harry

In other words when the MUSIC STOPS don't be the SMUCK without a CHAIR!!!! Oy Vey!!!!

sierrawave_92007

What do I think? I think Japan is headed to taking much of the wealth from the older generation and transferring it to the younger generation with continued deflation. My Reason? Japan is trying to lower their export prices by printing Japanese currency and will be met by lower wages by their export competitors across Asia. Result? Lower prices for Japanese exports, and even lower prices for exports by Japanese competitors.

joe

Bil Gross from Pimco said money from Japan was going to be flowing into US treasuries. I like El-Erian but he has been wrong more times than he has been right. In May of 2011 he said to stay away from treasuries. The best performing asset class that year was long treasuries.

March 27, 2013

Declining Wealth Brings a Rising Retirement Risk, by Bruce Bartlett, Commentary, NY Times: ...[In] defined-benefit ... pension plans..., workers are promised a specific income at retirement, which the employer provides. The employer bears all the risk of market fluctuations. Under a defined contribution scheme, such as a 401(k) plan, the worker and the employer jointly contribute to a tax-deductible and tax-deferred account from which the worker will finance retirement. ...Now the first generation of workers who have virtually all their pension saving in defined-contribution plans is nearing retirement, and the news isn't good. According to a March 19 report from the Employee Benefit Research Institute, only about half of workers nearing retirement have confidence that they have enough money saved for an adequate retirement.Not surprisingly, retirement saving has taken a back seat to more pressing concerns – coping with unemployment, maintaining standards of living during an era of slow wage growth, putting children through increasingly expensive colleges and so on. ...This problem is much more severe for black Americans. ... The wealth gap isn't only racial, it's generational...What's really depressing about these studies is the lack of solutions and the likelihood that the problem will only get worse.Republicans in Congress have pressed for years to convert Social Security, a classic defined-benefit pension, into a defined contribution plan, and also to convert Medicare into a voucher program. These changes would shift even more of the financial risk in retirement onto families that have yet to adapt to fundamental changes in employer pensions and the economy over the last 30 years. The future doesn't look pretty.Members of Congress appear to be eager to cut retirement benefits even further to show they can make the hard choices (and the president seems to be on board). They should raise the payroll cap instead, but the "hard choice" that would hit the people who can afford it isn't under consideration. It's not hard to imagine why.

Darryl FKA Ron :save_the_rustbelt said in reply to paine ...The "news isn't good" about the shift from defined-benefit to defined-contribution pension plans:

[The new is great for corporations and investors, just not for retirees from ordinary wage and salary jobs. It's great news for the rich and great news for the poor. The rich will have even higher profits and income and the poor will have a LOT more company pretty soon.]

Now the first generation of workers who have virtually all their pension saving in defined-contribution plans is nearing retirement, and the news isn't good.

[Don't worry it will get a lot worse over the next decade or so. The more equities that are cashed in by pension funds and 401Ks to draw down savings for income, then the lower equity prices will fall. After decades of pumping up equity prices with demand for savings, now things will begin to turn the other way. Why do you think that equities have rebounded after economics shocks so quickly in recessions past? It was not just corporate profits driving prices back up. It was also demand. Retirees draw down savings a lot faster than they saved. We save for forty or more years in order to have roughly fifteen to twenty years of retirement income, if that. Our savings rate is dependent upone our earnings. So, high income old boomers will stop saving and start retiring. The demand for equities from lower payed younger workers will not be able to pick up the slack. Hedge funds will run short sells to the floor. Then all the wealthy investors will pick up bargains off the floor. This price slump will help younger savers for as long as it lasts. Eventually, enough boomers will die off that equity price inflation will return.]

save_the_rustbelt said in reply to save_the_rustbelt...This is old but ugly news.

In the few spare moments I have away from obamacare I tinker with redesigning def con plans, no brilliant solutions yet.

Ah, there is a new law prof paper on SSRN, really good analysis, now where did I put the darn thing......

ken melvin :found it

Lawrence A. Frolik (Pittsburgh), Rethinking ERISA's Promise of Income Security in a World of 401(k) Plans

Cynthia said in reply to ken melvin...The whole model is problematic: an investor class, CALPERS and the workers, price of housing, asset inflation, ...

ken melvin said in reply to Cynthia...The market is not the economy and can stay irrational longer than you can stay liquid. At some point, corporations will reach the law of diminishing returns in employment reduction and will NOT be able to continue pushing through price increases without the bottom line being affected. When that happens, and it will at some point in time if the economy continues to contract to where the market will more accurately reflect the economy, and it won't be pretty.

I hope the market is "forward looking" and foretelling a better economy, but I think it's safe to view that with a jaundiced eye. It is fun while it last though, no doubt, unless you're one of the poor bastards that got reduced out of a job.

When in doubt follow the copper market. What is that canary doing?

save_the_rustbelt :Yeah, I think that we're beginning to see the end of the WalMart model; I'm not sure what will follow. The race to the bottom means at some point the workers can no longer afford to buy and there goes the whole of it, the middle class, all of it.

Ellen1910 said in reply to anne...A finance prof I work with, a guy really grounded in reality, has named the past ten years the

Decade of 0% Returns

Not exactly the 8% we were promised.

Barry :VFINX 7/31/2000-7/31/2010 AAR -0.86%

VWESX 7/31/2000-7/31/2010 AAR 7.81%I guess it depends on what you're looking at and when you look.

Mark: "Members of Congress appear to be eager to cut retirement benefits even further to show they can make the hard choices (and the president seems to be on board). "

No, because the members of Congress don't make hard choices - or at least, hard for them. The financial elites lust after Social Security money, and would love to have it transferred over to them for 'safekeeping'.

D Surber :

Don't forget the billions in wealth stolen when defined benefit plans were converted to 401ks. Twice in my career I have sat in meetings and watched my employer rape my coworkers through such a conversion.

Employees who were literally months from being fully vested in the defined benefit plan had their retirements wiped out. Both companies valued the accrued but not vested benefits at some pathetic dollar amount while vested employees received several times as much for only a few months more service.

Because there were so many more unvested employees, the company reaped a huge windfall by pocketing the "excess". Both companies chose to make the conversion during big stock runups when there were large "excess" savings in the pension plan.

Of course the "excess" was a financial fiction but that didn't stop corporate execs from pocketing the cash through outsize bonuses.

Perspective said in reply to Perspective...

I wish everyone with strong opinions about taxation/spending had the opportunity to live as a broke family and as a $300k+ family in LA/SF/NY/CHI. I think that perspective would change these "absolutes" that are so easily thrown-around (that a household making $250k should be paying tens of thousands more in taxes). The answers aren't easy. Life is hard and complicated.

Reply Wednesday, March 27, 2013 at 10:26 AM

paine said in reply to Perspective...

i've seen that range

i've live that range

i'm more absolute

its about economic class struggleabout people as classes not as "personhoods"

ya each of us has a unique identity more or less

each of us deserves equal respect and compassion

as individualsand so ....????

i see no modification of the class struggle

D Surber

I'm in both ranges and I would gladly pay tens of thousands more in taxes to fund education for the workers whose payroll taxes will be funding my Social Security and Medicare. To pay for firefighters who will stop the next Oakland Hills Fire before it destroys my home. To pay for bridges and dams that won't collapse. Et cetera.

Notice I'm not willing to pay yet more trillions to Haliburton, Blackwater, Lockheed, etc for wars of aggression. Nor am I willing to pay trillions to imprison millions in the failed War On Drugs. Or trillions to pay bonuses to bankers who destroyed the world economy. I guess that makes me a taker.

Perspective:

Ah, and there's the rub. You're willing to pay more, but you don't want it directed in the trillions of directions it's wasted. So why pay more? Why not demand the military industrial complex be reduced billions?

Before you demand I pay a dollar more, I demand that you stop building war machines the military has publicly stated they don't want or need. Talk to me then...

Darryl FKA Ron :

that a household making $250k should be paying tens of thousands more in taxes

[Given you arithmetic skills then it is difficult to imagine the payroll tax cap would affect you.]

anne said in reply to Perspective...

I love the unchallenged judgment from the Left. If someone from the Right suggests that maybe, someone receiving welfare or Food Stamp benefits shouldn't be spending $40 on their nails every two weeks, that's not only insensitive but racist.

[ Not necessarily racist unless that is the intent, but a sickening stereotype and I realize now how typical the comment is. Would such a comment be sickening from the left or sickening from the right? I have no idea.

Where is my nail polish, Jeeves? ]

paine said in reply to Perspective...

an extra 10 k ?

its less then a 7% tax

to hit ten k in extra payroll taxeswhat

230 k income

and that's just one earner

most households have two now eh ?

or can have twowhere are u coming from here ?

paine said in reply to paine ...

a little non computive there

don't you think

Perspective ?Perspective said in reply to paine ...

I was throwing a round figure in there with some assumptions to make a point. If we're talking about two married people each making $150k for a total of $300k, it would be more than $10k due to the Pease phase-down of their itemized deductions, .9% Obamacare Tax on $50k of their AGI, the 3.8% ObamaCare Tax on their investment income, and now 6.2% on another ~$100k of income for SSI.

Let's not forget, that the Senate Democrats' budget includes more taxes for these households too, not least of which is dramatically limiting the mortgage interest deduction (which I support BTW).

Darryl FKA Ron said in reply to Perspective...

But when someone on the Left suggests that people making $113k+ "can afford to pay much more in taxes," nobody questions this assumption. That person/family has bills and obligations too. This is America, so they're likely living paycheck-to-paycheck as well.

[OK, so I did the math considering a single earner making enough to pay $10K more in SSA payroll tax from lifting the cap and got $274,290. I will give you this much. In certain zip codes in NYCity, parts of Mass and CA, then a household could be living paycheck to paycheck. Of course, you might suppose that someone anywhere in the country might be living paycheck to paycheck on over a quarter million per year, but then you would have to question what someone that stupid did to make that much money? Ok, a family with more than five children would not be just overflowing with disposable income at that income. But a normal size family at that income should not be so cash flow strapped that the cap lift will kill them. It has been done before to levels higher than just inflation parity. Remember this is more than five times average household income and some of those households have five kids as well.]

Perspective said in reply to Darryl FKA Ron...

It won't kill them. I fully agree. However, the same argument could be said for raising the Medicare Tax or SSI tax 1%-2% as each is currently constructed. This won't kill middle class families.

EMIchael said in reply to Perspective...

Exactly how many people do you know that are receiving "welfare or foodstamp benefits" that pay $40 every two weeks to have their nails done?

Perspective said in reply to EMIchael...

Ah, that is where my perspective colors my political viewpoints (and makes me party-less). I was born and raised in South Los Angeles in a broken low-working class home. I know the people and especially the culture very well.

Perspective said in reply to EMIchael...

I often wonder if academics on the Left have ever been around low-income families and communities. The Right absurdly thinks that everyone has the opportunity to pick themselves up by their bootstraps regardless of the terrible family/community into which they were born.

But the Left equally absurdly thinks that every under-privileged family is doing everything possible to improve their lot in life, or at least the children's lot. They're both patently wrong.

Matt Young :

Benefits are defined by the ability of the middle class taxpayer to make the payments. So do not tell us that you deplore the destruction of the middle class, then demand the middle class start making more payments, that it seems is a contradiction way beyond anything normal.

Also, the middle class has discovered the magic theories of economics, and we do not buy it. At the end of the magic the middle class still ends up with the bill, as we all know.

Economist.com