The Nation’s Number Two Tight Oil Play After a Year of Low Oil Prices

The Bakken Play, located in North Dakota and Montana, is the birthplace of tight (shale) oil and

in many ways the poster child of the so-called “shale revolution.” Between 2010 and 2014, oil production

in North Dakota grew nearly five-fold, from 236,000 barrels/day in January 2010 to over 1,167,000 barrels/day

in January 2015, according to the U.S. Department of Energy’s

Energy Information Administration (EIA), which every

year publishes its Annual Energy Outlook

(AEO).

The EIA forecast this production growth to continue and — despite thousands of wells having already

been drilled in the most productive areas of the play, and the steep decline in oil prices in 2014 —

even raised its projection in 2015 for the total amount of tight oil produced in the Bakken through

2040 by 85% over the previous year’s forecast.

But a new report throws cold

water on the thinking that U.S. shale production will be around for the long

haul. The Post Carbon Institute

conducted an

analysis of the top seven oil and top seven natural gas plays, which

together account for 89 percent of current shale oil production and 88 percent

of shale gas production.

In Bakken Reality Check, David Hughes, author of Drilling Deeper(which

likely remains the most thorough independent analysis of U.S. shale gas and tight oil production ever

conducted) and a number of other reports on North American shale gas and tight oil production, looks

at how production in the Bakken has changed after a year of low oil prices.

Predicting what oil production will be in 25 years is difficult, to

say the least, but the Post Carbon report projects that oil production from the

Bakken and Eagle Ford will be just

one-tenth of the level that EIA is forecasting. The EIA predicts

that the Bakken and the Eagle Ford will be producing a combined 1 million bpd in

2040. Hughes thinks it will be just a small fraction of that amount – a mere

73,000 bpd.

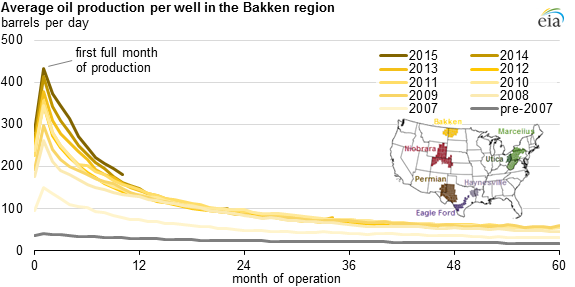

Oil production in the Bakken Play is now falling after more than a year of low oil prices—but it

has proven more resilient than many observers expected. This paper reviews the latest developments in

the Bakken Play and provides an update of the assessment in Drilling Deeper, which was published

in October 2014 just as the turmoil in the oil markets began.

The report found that both shale oil and shale gas production will peak

before 2020. More importantly, the report’s author, David Hughes, says oil

production will decline much more quickly than the EIA has predicted.

That’s largely because of high decline rates at shale wells across

the country. Unlike conventional wells, which can produce relatively

stable rates for a long period of time, shale oil and gas wells experience an

initial burst of production in the first few years, followed by a precipitous

decline thereafter.

Hughes

estimates that the average shale oil well declines at a rate of between 60

and 91 percent over three years. Wells in the Bakken decline by 45 percent per

year, which stands in stark contrast to the 5 percent annual decline for an

average conventional well.

Or put another way, oil and gas companies will have to keep drilling

at a feverish pace just to stand still. This means the industry is on a

“drilling

treadmill” that will be unsustainable over the long-term.

This is not the first time that David Hughes has taken aim at EIA

data. In a

December

2013 report, he skewered the high estimates for the potential of the

Monterrey Shale in California, calling the EIA’s numbers “simplistic and highly

overstated.” Several months later, the EIA was forced to back track on its

figures,

downgrading the recoverable oil estimates in the Monterrey by 96 percent.

Hughes says the implications of getting it wrong are “profound,” since so

many companies are basing very large investments on incorrect projections. He

says rosy estimates have cut into investment for renewables, while steering

capital towards expensive oil and gas export terminals that should now be called

into question.

An article in CleanTechnica points to the possibility of boom towns turning

into “ghost towns” if the pace of drilling drops off. If David Hughes

and The Post Carbon Institute are correct, there could be quite a few ghost

towns popping up in the coming years as the shale revolution begins to fizzle.

HB. I have used leases developed in our field in the past ten years to demonstrate that shale

is high cost. Again, rule of thumb the cost of a conventional well in our field is

approximately 1/100 of a shale oil well ($70K range v $7 million range).

Here are some examples with production through 10/31/19:

8 producers 4 injection wells. Cumulative BO 83,466. YTD BO 2,085. First production

4/2003.

10 producers 4 injection wells. Cumulative BO 116,065. YTD BO 2089. First production

9/2005.

10 producers 4 injection wells. Cumulative Bo 55,595. YTD BO 3,023. First production

3/2006.

4 producers 1 injection well. Cumulative BO 37,418. YTD BO 1,289. First production

8/2008.

8 producers 3 injection wells. Cumulative BO 42,494. YTD BO 2,328. First production

10/2008.

4 producers 1 injection well. Cumulative BO 19,216. YTD BO 1,220. First production

12/2010.

8 producers 3 injection wells. Cumulative BO 46,463. YTD BO 1,877. First production

8/2011.

4 producers 2 injection wells. Cumulative BO 10,700. YTD BO 634. First production

10/2011.

8 producers 3 injection wells. Cumulative 59,592 BO. YTD 4,956 BO. First production

11/2011.

1 producer. Water disposed of in adjoining lease. Cumulative BO 7,872. YTD BO 444 BO.

First production 5/2012.

8 producers 3 injection wells. Cumulative 56,500 BO. YTD 3,858 BO. First production

6/2012.

4 producers 1 injection well. Cumulative BO 11,758. YTD BO 1,457. First production

6/2013.

2 producers. Water disposed of on adjoining lease. Cumulative 3,524 BO. YTD BO 393. First

production 11/2013.

6 producers Two injection wells. Cumulative 25,988 BO. YTD 3,233 BO. First production

9/2014.

Figure in anywhere from $60K-80K to drill, complete and equip each well including

electric, flow and/or injection lines. Figure another $20-30K for a tank battery.

Assume anywhere from 12.5 to 20 percent royalty.

Of course, some projects do better than others. But compare this to shaleprofile.com

wells.

There was very little drilling in our field from 1987 to 2003. There has been very little

since 2015. Century plus year old stripper field.

There have also been many reclamation projects in our field during 2005-2014 of abandoned

wells wherein the producers went bust in the 1990s, with 1998 being a knockout blow.

We took over 2 wells drilled in the 1950s they were abandoned in 1998. We just had to

equip them and build a new tank battery. We also took over three wells also drilled in the

1950s where we had to do the same, plus plug the injection well and convert one producer to

an injector. These work well at $55-65 WTI also.

I can also point to many projects developed in our field in the 1980s where cumulative per

well has topped 40K BO to date.

Conventional oil is a much better deal than shale usually when you can find it. And also

when you aren't trying to pay for 8 figure CEO pay, skyscrapers and jets out of it.

Shale just has the scale. Huge scale. Worldwide game changing size.

Shallow, I can't thank you enough. Alot to digest here. My first glance gave me the feeling

shale drilling dollars are about half as productive. Maybe you have a better number.

When a new field is drilled, is it always under pressure without the cost of lifting it

from the hole? Then once the pressure is exhausted it becomes a stripper?

A lot of the Huntington Beach field lays under the ocean. There is over a mile long row of

wells along the shoreline. I'm assuming they go horizontal under the ocean. Only a few wells

have lift Jacks. Can strippers wells go horizontal?

There isn't enough down hole pressure here for natural flow. Everything goes on pumping unit

immediately and injection wells are also drilled at the same time as production wells.

To put into perspective, the field was originally drilled over 100 years ago. Waterflood

was initiated on a large scale right after WW2. Many wells were plugged in the late

1960s-early 1970s when oil prices were low. The field was redrilled in the late 1970s –

early 1980s. Little activity after 1986, until prices took off during the Iraq War.

For example, we operate a lease that was originally drilled in the 1950s. It was plugged

out in 1972. In 1979-81, all of the plugged wells were drilled out (casing had not been

pulled). New injection wells were drilled.

Cumulative from 9 producing wells since 1979 is over 140K BO with production currently at

5.5 BOPD. It is difficult to tell what these wells produced from 1953-1972, because they were

part of a larger unitized waterflood project. Our guess is around 200-250K BO during that

time frame.

Only a small company would be interested in 9 wells making 5.5 BOPD, but they have been

economic even during the worst part of 2016 (barely during Q1 – 2016).

There haven't been HZ wells drilled in the shallow zones (1,500' and below). However,

there has been some success with 1,800'-5,000' TVD hz wells. Not sure of the economics.

There has been success with slick water fracks in deeper vertical wells also.

If we assume as 10 million per well total cost, then 200K barrel needs to be extracted to

break even. Assuming average life of the well of 5 years you need to produce on average 1000

barrel a day to break even. In the past that were possible (the average was 143), now it is

not

The Monterrey shale estimate was by the EIA not the USGS. The EIA had a private consultant

do the analysis and it was mostly based on investor presentations, very little geological

analysis.

It would be better if the USGS did an economic analysis as they do with coal for the

Powder River Basin. They could develop a supply curve based on current costs, but they

don't.

Do you have any idea of the capital cost of the wells (ballpark guess) for a horizontal

multifracked well in the Wolfcamp? Would $7 million be about right (a WAG by me)?

On ignoring economics, I show my oil price assumptions. Other financial assumptions for

the Bakken are $8 million for capital cost of the well (2016$). OPEX=$9/b, other costs=$5/b,

royalty and taxes=29% of gross revenue, $10/b transport cost, and a real discount rate of 7%

(10% nominal discount rate assuming 3% inflation).

I do a DCF based on my assumed real oil price curve. Brent oil price rises to $77/b

(2016$) by June 2017 and continue to rise at 17% per year until Oct 2020 when the oil price

reaches $130/b, it is assumed that average oil prices remain at that level until Dec 2060.

The last well is drilled in Dec 2035 and stops producing 25 years later in Dec 2060.

EUR of wells today is assumed to be 321 kb and EUR falls to 160 kb by 2035. The

last well drilled only makes $243,000 over the 7% real rate of return, so the 9 Gb scenario

is probably too optimistic, it is assumed that any gas sales are used to offset OPEX and

other costs, though no natural gas price assumptions have been made to simplify the

analysis.

This analysis is based on the analyses that Rune Likvern has done in the past, though his

analyses are far superior to my own.

I think when seismic, land, surface and down hole equipment is included, the number is much

higher. With $20-60K per acre being paid, land definitely has to be factored in. Depending on

spacing, $1-5 million per well?

I am doing the analysis for the Bakken. A lot of the leases are already held and I don't

know that those were the prices paid. Give me a number for total capital cost that makes sense,

are you suggesting $10.5 million per well, rather than $8 million? Not hard to do, but all the

different assumptions you would like to change would be good so I don't redo it 5 times.

Mostly I would like to clear up "the number".

I threw out more than one number, OPEX, other costs, transport costs, royalties and taxes,

real discount rate (adjusted for inflation), well cost.

I think you a re talking about well cost as "the number". I include down hole costs as part

of OPEX (think of it as OPEX plus maintenance maybe).

Dennis. The very high acreage numbers are for recent sales in the Permian Basin. In reading

company reports, it seems they state a cost to drill and case the hole, another to complete the

well, then add the two for well cost.

This does not include costs incurred prior to the well being drilled, which are not

insignificant. Nor does it include costs of down hole and surface equipment, which also are not

insignificant.

Land costs are all over the map, and I think Bakken land costs overall are the lowest,

because much of the leasing occurred prior to US shale production boom. I think a lot of

acreage early on cost in the hundreds per acre. Of course, there was quite a bit of trading

around since, so we have to look project by project, unfortunately. For purposes of a model, I

think $8 million is probably in the ballpark.

I would not include equipment for the well, initially, as OPEX (LOE is what I prefer to

stick with, being US based). The companies do not do that, those costs are included in

depreciation, depletion and amortization expense.

Once the well is in production, and failures occur, I include the cost of repairs, including

replacement equipment, in LOE. I am not sure that the companies do that, however.

I think the Permian is going to be much tougher to estimate, as there are different

producing formations at different depths, whereas the Bakken primarily has two, and the Eagle

Ford has 1 or 2.

An example:

QEP paid roughly $60,000 per acre for land in Martin Co., TX. If we assume one drilling unit

is 1280 acres (two sections), how many two mile laterals will be drilled in the unit?

1280 acres x $60,000 = $76,800,000.

Assume 440′ spacing, 12 wells per unit.

$76,800,000/12 = $6,400,000 per well.

However, there are claims of up to 8 producing zones in the Permian.

So, 12 x 8 = 96 wells.

$76,800,000 / 96 = $800,000 per well.

Even assuming 96 wells, the cost per well is still significant.

If we assume 96 wells x $7 million to drill, complete and equip, total cost to develop is

$.75 BILLION. That is a lot of money for one 1280 acre unit, need to recover a lot of oil and

gas to get that to payout.

I am neither an oil man nor an accountant, so regardless of what we call it I am assuming

natural gas sales (maybe about $3/barrel on average) are used to offset the ongoing costs to

operate the well (LOE, OPEX, financial costs, etc), we could add another million to the cost of

the well for surface and downhole equipment and land costs.

Does an average operating cost over the life of a well of about $17/b ($14/b plus natural

gas sales of $3/b of oil produced)seem reasonable? That would be about $5.4 million spent on

LOE etc. over the life of the well (assuming 320 kbo produced). Also does the 10% nominal rate

of return sound high enough, what number would you use as a cutoff?

You use a different method than a DCF and want the well to pay out in 60 months. This would

correspond to about a 14% nominal rate of return and an 11% real rate of return (assuming a 3%

annual inflation rate.)

"The Monterrey shale estimate was by the EIA not the USGS. The EIA had a private consultant do

the analysis and it was mostly based on investor presentations, very little geological

analysis."

Exactly. USGS' estimate as of October 2015 is very conservative:

"The Monterey Formation in the deepest parts of California's San Joaquin Basin contains an

estimated mean volumes of 21 million barrels of oil, 27 billion cubic feet of gas, and 1

million barrels of natural gas liquids, according to the first USGS assessment of continuous

(unconventional), technically recoverable resources in the Monterey Formation."

"The volume estimated in the new study is small, compared to previous USGS estimates of

conventionally trapped recoverable oil in the Monterey Formation in the San Joaquin Basin.

Those earlier estimates were for oil that could come either from producing more Monterey oil

from existing fields, or from discovering new conventional resources in the Monterey

Formation."

Previous USGS estimates were for conventional oil:

"In 2003, USGS conducted an assessment of conventional oil and gas in the San Joaquin Basin,

estimating a mean of 121 million barrels of oil recoverable from the Monterey. In addition, in

2012, USGS assessed the potential volume of oil that could be added to reserves in the San

Joaquin Basin from increasing recovery in existing fields. The results of that study suggested

that a mean of about 3 billion barrels of oil might eventually be added to reserves from

Monterey reservoirs in conventional traps, mostly from a type of rock in the Monterey called

diatomite, which has recently been producing over 20 million barrels of oil per year."

I am corrected, RE; USGS and Monterrey. I still don't believe there is 20G BO in the Wolfcamp.

Most increases in PB DUC's are not wells awaiting frac's but lower Wolfcamp wells that are TA

and awaiting re-drills; that should tell you something. With acreage, infrastructure and water

costs in W. Texas, wells cost $8.5-9.0M each. The shale industry won't admit that, but that's

what I think. What happens to EUR's and oil prices after April of 2017 is a guess and a waste

of time, sorry.

What most interests me are suggestions that there is so much available oil in Wolfcamp and what

that will do to oil prices and national policy.

Seems like any announcement of more oil will likely keep prices low. And if they stay low,

there's little reason to open up more areas for oil drilling.

"Their assessment method for Bakken was pretty simple – pick a well EUR, pick a well

spacing, pick total acreage, pick a factor for dry holes – multiply a by c by d and

divide by b."

USGS estimates for average well EUR in Wolfcamp shale look reasonable: 167,ooo barrels in the

core areas and much lower in other parts of the formation.

I do not know if the estimated potential production area is too big, or assumed well spacing

is too tight.

The key question is what part of these estimated technically recoverable resources are

economically viable at $50; $60; $70; $80; $90, $100, etc.

Significant part of resources may never be developed, even if they are technically

recoverable.

Keep in mind these USGS estimates are for undiscovered TRR, one needs to add proved reserves

times 1.5 to get 2 P reserves and that should be added to UTRR to get TRR. There are roughly 3

Gb of 2P reserves that have been added to Permian reserves since 2011, if we assume most of

these are from the Wolfcamp shale (not known) then the TRR would be about 23 Gb. Note that

total proved plus probable reserves at the end of 2014 in the Permian was 10.5 Gb (7 Gb proved

plus 3.5 GB probable with the assumption that probable=proved/2). I have assumed about 30% of

total Permian 2P reserves is in the Wolfcamp shale. That is a WAG.

Note the median estimate is a UTRR of 19 Gb with F95=11.4 Gb and F5=31.4 Gb. So a

conservative guess would be a TRR of 13.4 Gb= proved reserves plus F95 estimate. If prices go

to $85/b and remain at that level the F95 estimate may become ERR, at $100/b maybe the median

is potentially ERR. It will depend how long prices can remain at $100/b before an economic

crash, prices are Brent Crude price in 2016$ with various crude spreads assumed to be about

where they are now.

Dennis,

where your number for proven reserves in the Permian comes from?

In November 2015, the EIA estimated proven reserves of tight oil in Wolfcamp and Bone Spring

formations as of end 2014 at just 722 million barrels.

I just looked at Permian Basin crude reserves (Districts 7C, 8 and 8A) and assumed the

change in reserves from 2011 to 2014 was from the Wolfcamp. I didn't know about that page for

reserves. It is surprising it is that low.

In any case the difference is small relative to the UTRR, it will be interesting to see what

the reserves are for year end 2015.

Based on this I would revise my estimate to 20 Gb for URR with a conservative estimate of 12

Gb until we have the data for year end 2015 to be released later this month.

My guess is that the USGS probably already has the 2015 year end reserve data.

The EIA proved reserves estimate for 2015 will be issued this month. I think we will see a

significant increase in the number for the Permian basin LTO.

Also note that USGS TRR estimate is only for Wolfcamp.

I can only guess what could be their estimate for the whole Permian tight oil reserves.

But the share of Wolfcamp in the Permian LTO output is only 24% (according to the

EIA/DrillingInfo report).

That makes sense. I also imagine the USGS focused on the formation with the bulk of the

remaining resources. It is conceivable that the 30 Gb estimate is closer to the remaining oil

in place and that more like 90% of the TRR is in the Wolfcamp, considering that the F5 estimate

is about 30 Gb. That older study from 2005 may be an under estimate of TRR for the Permian,

likewise the USGS might have overestimated the UTRR.

If oil prices go back to $100/b in 2018 as the IEA seems to be concerned about, it could

ramp up at the speed of the Eagle Ford (say 2 to 3 years). It will be oil price dependent and

perhaps they won't over do it like in 2011-2014, but who knows, some people don't learn from

past mistakes. If you or Mike were running things it would be done right, but the LTO guys, I

don't know.

"This estimate is for continuous (unconventional) oil, and consists of undiscovered,

technically recoverable resources.

Undiscovered resources are those that are estimated to exist based on geologic knowledge and

theory, while technically recoverable resources are those that can be produced using currently

available technology and industry practices. Whether or not it is profitable to produce these

resources has not been evaluated."

If it requires slave labor at gunpoint to get the oil out, then that's what will happen

because you MUST have oil, and a day will soon come when that sort of thing is reqd.

Nice apocalyptic vision of the future you've got there!

Whatever happened to the ideals of democracy, capitalism, business, profits, free markets

etc ? Don't worry, no need to answer, that was purely a rhetorical question. I'm quite aware of

the realities of the world!

However, not to pour too much sand on your vision, But I have to wonder? Since your

potential slaves in 21st century America are already armed to the teeth, they might decide not

to just go with the flow. (pun intended)

Anyways slaves don't buy cars or too many consumer goods so that might, in and of itself,

put a bit of a damper on the raison d'etre, excuse my french, of the oil companies and the very

existence of these future slave owners.

because you MUST have oil

Really now?! You know, as time goes by, I'm less and less convinced of that!

This follows on from reserve post above (two a couple of comments). In terms of changes over

the last three years – there really weren't anything much dramatic. We'll see what 2016

brings, especially for ExxonMobil, but it looks like they already knocked a big chunk off of

their Bitumen numbers already in 2015.

Note I went through a lot of 20-F and 10-K reports watching the rain fall this morning and

copied out the numbers, I'm not guaranteeing I got everything 100%, but I think the general

trends are shown.

Note the figures are totals for all nine companies I looked at.

IEA WEO is out: http://www.iea.org/newsroom/news/2016/november/world-energy-outlook-2016.html

presentation slides, fact sheet and summary are available online (report can be purchased). IEA

seems to be _very_ concerned about underinvestment in upstream oil production. Several pages of

the report is devoted to this, the title of that section is "mind the gap". More or less all of

the content has been discussed on this website, including the issue with high levels of debt

and that this can affect suppliers' capacity to rebound, and how much demand can be reduced as

a result of a stringent carbon cap.

From the fact sheet (available free of charge):

"Another year of low upstream oil investment in 2017 would risk a shortfall in oil production

in a few years' time. The conventional crude oil resources (e.g. excluding tight oil and oil

sands) approved for development in 2015 sank to the lowest level since the 1950s, with no sign

of a rebound in 2016. If there is no pick-up in 2017, then it becomes increasingly unlikely

that demand (as projected in our main scenario) and supply can be matched in the early 2020s

without the start of a new boom/bust cycle for the industry"

Presentation 1:09 – Dr. Birol gives his view: "depletion never sleeps"

I wonder who that paragraph is aimed at. As I indicated above the companies that would be

investing in long term conventional projects don't have a very large inventory of undeveloped

reserves (17 Gb as of end of 2015, some of this has gone already this year and more is in

development and will come on stream in 2017 and 2018 (and a small amount in later years for

approved projects). I'd guess there might only be less than 10 Gb (and this the most expensive

to develop) that is currently under appraisal among the major western IOCs and larger

independents; allowing for their partnerships with NOCs in a lot of the available projects that

could represent 20 to 30 Gb total. That really isn't very much new supply available, and a

large proportion is in complex deep water projects that wouldn't be ramped up fully until 6 to

7 years after FID (i.e. already too late for 2020). Really the main players need to find new

fields with easy developments, but they obviously aren't, probably never will, and actually

aren't looking very hard at the moment.

My interpretation is that this is IEAs way of saying that it does not look good. Those who can

read between the lines get the message. Also, a few years from they will be able to say "see we

told you so".

It's impossible for IEA to make statements like: "the end of low cost oil will negatively

affect economic growth", "geology is about to beat human ingenuity" etc.

WEO have become more and more bizarre over the years. On the one hand they contain

quantitative projections which tell the story politicians wants to hear. On the other hand, the

text describes all sorts of reason of why the assumptions are unlikely to hold. Normally, if

you don't believe in your own assumptions you would change them.

Here is the production graph. Not that much has happened. There was a big drop for 2011. 2009

on the other hand saw an increase. Up to the left, which is very hard to see, 2015 continues to

follow 2014 which follows 2013 which follows 2012. Will we see 2013 reach 2007 the next few

months?

Its on purpose both because I wanted to zoom in and because the data for first 18 months or so

for the method I used above is not very usable. Bellow is the production profile which is

better for seeing differences the first 18 months. Above graph is roughly 6 months ahead of the

production profile graph.

And I guess we can all see no technological breakthru. 2014's green line looks superior to

first 3 mos 2015.

2016 looks like it declines to the same level about 2.5 mos later, but is clearly a steeper

decline at that point and is likely going to intersect 2014's line probably within the

year.

There is zero evidence on that compilation of any technological breakthrough surging output

per well in the past 2-3 yrs.

In fact, they damn near all overlay within 2 yrs. No way in hell there is any spectacular

EUR improvement.

And . . . in the context of the moment, nope, no evidence of techno breakthrough. But also

no evidence of sweetspots first.

I suppose you could contort conclusions and say . . . Yes, the sweetspots were first - with

inferior technology, and then as they became less sweet the technological breakthroughs brought

output up to look the same.

clarifying, the techno breakthrus are bogus. They would show in that data if they were real.

And it would be far too much coincidence for techno breakthrus to just happen to increase

flow the exact amount lost from exhausting sweet spots.

This suggests the sweetspot theory is also bogus, unless there are 9 years of them, meaning

it's ALL been sweetspots so far. 9 yrs of sweetspots might as well be called just normal rather

than sweet.

It is pretty much all bogus, yes, Watcher. With any rudimentary understanding of volumetric

calculations of OOIP in a dense shale like the Bakken, there is only X BO along the horizontal

lateral that might be "obtained" from stimulation. More sand along a longer lateral does not

necessarily translate into greater frac growth (an increase in the radius around the horizontal

lateral). Novices in frac technology believe in halo effects, or that more sand equates to

higher UR of OOIP per acre foot of exposed reservoir. That is not the case; longer laterals

simply expose more acre feet of shale that can be recovered. Recovery factors in shale per acre

foot will never exceed 5-6%, IMO, short of any breakthroughs in EOR technology. That will take

much higher oil prices.

Its very simple, actually bigger fracs (that cost lots more money!!) over longer laterals

result in higher IP's and higher ensuing 90 day production results. That generates more cash

flow (imperative at the moment) and allows for higher EUR's that translate into bigger booked

reserve assets. More assets means the shale oil industry can borrow more money against those

assets. Its a game, and a very obvious one at that. Nobody is breaking new ground or making big

strides in greater UR. That's internet dribble. Freddy is right; everyone in the shale biz is

pounding their sweet spots, high grading as they call it, and higher GOR's are a sure sign of

depletion. Moving off those sweet spots into flank areas will be even less economical (if that

is possible) and will result in significantly less UR per well. That is what is ridiculous

about modeling the future based on X wells per month and trying to determine how much

unconventional shale oil can be produced in the US thru 2035. The term, "past performance is

not indicative of future results?" We invented that phrase 120 years ago in the oil

business.

That, sir, is pretty much the point. I see what looks like about 20% IP increase for the extra

stages post 2008/9/10. How could there not be going from 15 stages to 30+?

I see NO magic post peak. They all descend exactly the same way and by 18-20 months every

drill year is lined up. That's actually astounding - given 15 vs 30 stages. There should be

more volume draining on day 1 and year 2, but the flow is the same at month 20+ for all drill

years. This should kill the profitability on those later wells because 30 stages must cost

more.

But profit is not required when you MUST have oil.

Freddy, is there something going on in the data? How can 30 stage long laterals flow the

same at production month 24 as the earlier dated wells at their production month 24

–whose lengths of well were MUCH shorter?

I can only speculate why the curves look like they do. It could be that the newer wells would

have produced more than the older wells, but closer well spacing is causing the UR to go down.

Here is the updated yearly decline rate graph. 2010 has seen increased decline rates as I

suspected. The curves are currently gathering in the 15%-20% range.

2007 only has 161 wells. So it makes the production curve a bit noisy as you can see above.

Current yearly decline rate for 2007 is 7,2% and the average from month 98 to 117 would

translate to a 10,3% yearly decline rate. The 2007 curve look quite different from the other

curves, so thats why I did not include it.

Thanks. The 2008 wells were probably refracked so that curve is messed up. If we ignore

2008, 2007 looks fairly similar to the other curves (if we consider the smoothed slope.) I

guess one way to do it would be to look at the natural log of monthly output vs month for each

year and see where the curve starts to become straight indicating exponential decline. The

decline rates of many of the curves look similar through about month 80 (2007, 2009, 2010,

2011) after 2011 (2012, 2013, 2014) decline rates look steeper, maybe poor well quality or

super fracking (more frack stages and more proppant) has changed the shape of the decline

curve. The shape is definitely different, I am speculating about the possible cause.

2007 had much lower initial production and the long late plateau gives it a low decline rate

also. But yes, initial decline rates look similar to the other curves. If you look at the

individual 2007 wells then you can see that some of them have similar increases to production

as the 2008 wells had during 2014. I have not investigated this in detail, but it could be that

those increases are fewer and distributed over a longer time span than 2008 and it is what has

caused the plateau. If that is the case, then 2007 may not be different from the others at and

we will see increased decline rates in the future.

Regarding natural log plots. Yes it could be good if you want to find a constant exponential

decline. But we are not there yet as you can see in above graph.

One good reason why decline rates are increasing is because of the GOR increase. When they

pump up the oil so fast that GOR is increasing, then it's expected that there are some

production increases first but higher decline rates later. Perhaps completion techniques have

something to do with it also. Well spacing is getting closer and closer also and is definitely

close enough in some areas to cause reductions in UR. But I would expect lower inital

production rather than higher decline rates from that. But maybe I´m wrong.

Ok Enno's data from NDIC shows 73 well completions in North Dakota in Sept 2016, 33 were

confidential wells, if we assume 98% of those were Bakken/TF wells that would be 72 ND

Bakken/TF wells completed in Sept 2016.

I have 75 in my data, so about the same. They have increased the number of new wells quite alot

the last two months. It looks like the addtional ones mainly comes from the DUC backlog as it

increased withouth the rig count going up. But I see that the rig count has gone up now too.

Ron you say " Bakken production continues to decline though I expect it to level off soon."

A few words of wisdom as to the main reasons why it would level off? Price rise?

Even though you asked Ron. He might think that the decline in the number of new wells per

month may have stabilized at around 71 new wells per month. If that rate of new completions per

month stays the same there will still be decline but the rate of decline will be slower.

Scenario below shows what would happen with 71 new wells per month from Sept 2016 to June 2017

and then a 1 well per month increase from July 2017 to Dec 2018 (89 new wells per month in Dec

2018).

I am not so convinced that either Texas or the Bakken is finished declining at the current

level of completions. There was consistent completions of over 1000 wells in Texas until about

October of 2015. Then it dropped to less than half of that. The number of producing wells in

Texas peaked in June of this year. Since then, through October, it has decreased by roughly

1000 wells a month. The Texas RRC reports are indicating that they are still plugging more than

they are completing.

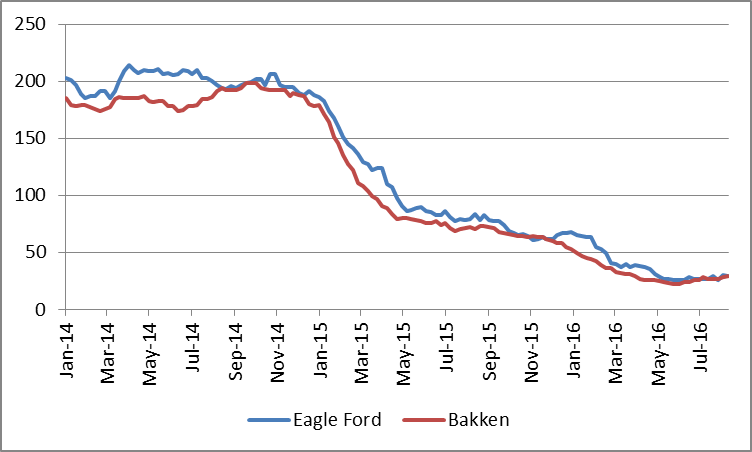

I remember reading one projection recently for what wells will be doing over time in the Eagle

Ford. They ran those projections for a well for over 22 years. Not sure which planet we are

talking about, but in Texas an Eagle Ford does well to survive 6 years. They keep referring to

an Eagle Ford producing half of what they will in the first two years. In most areas, I would

say that it is half in the first year.

The EIA, IEA, Opec, and most pundits have the US shale drilling turning on a dime when the oil

price reaches a certain level. If it was at a hundred now, it would still take about two years

to significantly increase production, if it ever happens. I am not a big believer that US shale

is the new spigot for supply.

The wells being shut in are not nearly as important as the number of wells completed because

the output volume is so different. So the average well in the Eagle Ford in its second month of

production produces about 370 b/d, but the average well at 68 months was producing 10 b/d. So

about 37 average wells need to be shut in to offset one average new well completion.

Point is that total well counts are not so important, it is well completions that drive

output higher.

Output is falling because fewer wells are being completed. When oil prices rise and profits

increase, completions per month will increase and slow the decline rate and eventually raise

output if completions are high enough. For the Bakken at an output level of 863 kb/d in Dec

2017 about 79 new wells per month is enough to cause a slight increase in output. My model

slightly underestimates Bakken output, for Sept 2016 my model has output at 890 kb/d, about 30

kb/d lower than actual output (3% too low), my well profile may be slightly too low, but I

expect eventually new well EUR will start to decrease and my model will start to match actual

output better by mid 2017 as sweet spots run out of room for new wells.

Guess I will remember that for the future. The number of producing wells is not important.

Kinda like I got pooh poohed when I said the production would drop to over 1 million barrels

back in early 2015.

Do you agree that the shut in wells tend to be low output wells? So if I shut down 37 of

those but complete one well the net change in output is zero.

Likewise if I complete 1000 wells in a year, I could shut down 20,000 stripper wells and the

net change in output would be zero, but there would be 19,000 fewer producing wells, if we

assume the average output of the 1000 new wells completed was 200 b/d for the year and the

stripper wells produced 10 b/d on average.

How much do you expect output to fall in the US by Dec 2017?

Hindsight is 20/20 and lots of people can make lucky guesses. Output did indeed fall by

about 1 million barrels per day from April 2015 to July 2016, can you point me to your comment

where you predicted this?

Tell us what it will be in August 2017.

I expected the fall in supply would lead to higher prices, I did not expect World output to

be as resilient as it has been and I also did not realize how oversupplied the market was in

April 2015. In Jan 2015 I expected output would decrease and it increased by 250 kb/d from Jan

to April, so I was too pessimistic, from Jan 2015 (which is early 2015) to August 2016 US

output has decreased by 635 kb/d.

If you were suggesting World output would fall from Jan 2015 levels by 1 Mb/d, you would

also have been incorrect as World C+C output has increased from Feb 2015 to July 2016 by 400

kb/d. If we consider 12 month average output of World C+C, the decline has been 340 kb/d from

the 12 month average peak in August 2015 (centered 12 month average).

The dropping numbers are not as much from the wells that produce less than 10 barrels a day,

but from those producing greater than 10, but less than 100. The ones producing greater than

100 are remaining at a consistent level over 9000 to 9500. The prediction on one million was as

to the US shale only. It is your site, you can search it better than I can,

But then don't take my word for it. You can find the same information under the Texas RRC site

under oil and gas/research and statistics/well distribution tables. Current production for Sep

can be found at online research queries/statewide. It is still dropping, and will long term at

the current activity level. Production drop for oil, only, is a little over 40k per day

barrels, and condensate is lower for September. Proofs in the pudding.

My guess is that you would see a lot more plugging reports, if it were not so expensive to plug

a well. At net income levels where they are, I expect they would put that off as long as they

could.

I trust the NDIC numbers much more than the EIA numbers which are based on a model. Enno

Peters data has 66 completions in August 2016, he has not put up his post for the Sept data yet

so I am using the Director's estimate for now. I agree his estimate is usually off a bit, Enno

tends to be spot on for the Bakken data, for Texas he relies on RRC data which is not very

good.

Dennis. Someone pointed out Whiting's Twin Valley field wells being shut in for August.

It appears this was because another 13 wells in the field were recently completed.

It appears that when all 29 wells are returned to full production, this field will be very

prolific initially. Therefore, on this one field alone, we could see some impact for the entire

state.

Does anyone know if these wells are part of Whiting's JV? Telling if they had to do that on

these strong wells. Bakken just not close to economic.

I also note that average production days per well in for EOG in Parshall was 24. I haven't

looked at some of the other "older" large fields yet, but assume the numbers are similar.

I agree higher prices will be needed in the Bakken, probably $75/b or more. To be honest I

don't know why they continue to complete wells, but maybe it is a matter of ignoring the sunk

costs in wells drilled but not completed and running the numbers based on whether they can pay

back the completion costs. Everyone may be hoping the other guys fail and are just trying to

pay the bills as best they can, not sure if just stopping altogether is the best strategy.

There is the old adage that when your in a hole, more digging doesn't help much.

So my model just assumes continued completions at the August rate for about 12 months with

gradually rising prices as the market starts to balance, then a gradual increase in completions

as prices continue to rise from July 2017($78/b) to Dec 2018 (from 72 completions to about 90

completions per month 18 months later). At that point oil prices have risen to $97/b and LTO

companies are making money. Prices continue to rise to $130/b by Oct 2020 and then remain at

that level for 40 years (not likely, but the model is simplistic).

I could easily do a model with no wells completed, but I doubt that will be correct.

Suggestions?

Dennis. As we have discussed before, tough to model when there is no way to be accurate

regarding the oil price.

I continue to contend that there will be no quick price recovery without an OPEC cut.

Further, the US dollar is very important too, as are interest rates.

At some point OPEC may not be able to increase output much more and overall World supply

will increase less than demand. My guess is that this will occur by mid 2017 and oil prices

will rise. OPEC output from Libya an Nigeria has recovered, but this can only go so far, maybe

another 1 Mb/d at most. I don't expect any big increases from other OPEC nations in the near

term.

A big guess as to oil prices has to be made to do a model.

I believe my guess is conservative, but maybe oil prices will remain where they are now

beyond mid 2017.

I expected World supply to have fallen much more quickly than has been the case at oil

prices of $50/b.

"EIA does this by using a relatively new dataset-FracFocus.org's national fracking chemical

registry-to identify the completion phase, marked by the first fracking. If a well shows up on

the registry, it's considered completed "

There is an unlikely peak oil related editorial writer hiding in the most unlikely place: a

weekly English business paper called Capital Ethiopia. The latest editorial is again putting an

excellent perspective on world events. http://capitalethiopia.com/2016/11/15/system-failure/#.WC1ZCvl9600

For the record, I have no interest or connection to this publication other than that of a

paying reader.

Wouldn't it be nice if mainstream publications would sound a bit more like this.

Thanks all. I thought that the red queen concept meant that there had to be an increase in the

rate of completions. So that 71 year-on-year in north Dakota would only stabilise temporarily.

Perhaps the loss of sweet spots are being counteracted by the improvements in technology? I'm

assuming that even with difficulties of financing there will be a swift increase in completions

should the oil price take off, but not sure how sustainable this would be

Sometimes I think that once the price of oil is up enough that sellers can hedge the their

selling price for two or three years at a profitable level, it will hardly matter what the

banks have to say about financing new wells.

At five to ten million apiece, there will probably be plenty of money coming out of various

deep pockets to get the well drilling ball rolling again, if the profits look good.

Sometimes the folks who think the industry will not be able to raise money forget that it's

not a scratch job anymore. The land surveys, roads, a good bit of pipeline, housing, leases,

etc are already in place, meaning all it takes to get the oil started now is a drill and frack

rig.

I don't know what the price will have to be, but considering that a lot of lease and other

money is a sunk cost that can't be recovered, and will have to be written off, along with the

mountain of debts accumulated so far, the price might be lower than a lot of people

estimate.

Bankruptcy of old owners results in lowering the price at which an old business makes money

for its new owners.

The Red Queen effect is that more and more wells need to be completed to increase

output. As output decreases fewer wells are needed to maintain output. So at 1000 kb/d output

it might require 120 wells to be completed to maintain output (if new well EUR did not

eventually decrease), but at 850 kb/d it might require about 78 new wells per month to maintain

output.

I think your numbers reflect numbers reported from ND DMR but Bloomberg might be closer to

reality for wells that will actually ever be completed (just a guess by me though). How do

Bloomberg get their numbers (e.g. removing Tight Holes, or removing old wells, not counting

non-completed waivers etc.)?

Yes indeed. The difficulty with DUCs is always, which wells do you count. I don't filter old

wells for example, and already include those that were spud last month (even though maybe

casing has not been set). I don't do a lot of filtering, so the actual # wells that really can

be completed is likely quite a bit lower. I see my DUC numbers as the upper bound. I don't know

Bloombergs method exactly, so I can't comment on that.

Concerning Freddy's chart of production profile of wells drilled in various years.

They all line up by about month 18 of production. This should not be possible. The later

wells have many more stages of frack. They are longer, draining more volume of rock. But the

chart says what it says. At month about 18 the 2014 wells are flowing the same rate as 2008

wells. We know stage count has risen over those 6 yrs. 2014 wells should flow a higher rate.

The shape of the curve can be the same, but it should be offset higher.

Explanation?

How about above ground issues . . . older wells get pipelines and can flow more oil . . .

nah, that's absurd.

There needs to be a physical explanation for this.

These new wells have higher IPs, but also higher decline rates.

Closer spacing (see Freddy's comment above) and depletion of the sweet spots may also impact

production curves and EURs.

That doesn't make sense. They are longer. By a factor of 2ish. How can a 6000 foot lateral flow

exactly the same amount 2 yrs into production as a 3000 foot lateral flows 2 yrs into

production?

Look at the lines. At 18 months AND BEYOND, these longer laterals flow the same oil rate as

the shorter laterals did at the same month number of production. Higher IP and higher decline

rate will affect the shape, but There Is Twice The Length..

I don't think we have information on the length of the wells, since 2008 the length of the

lateral has not changed, just the number of frack stages and amount of proppant. This seems to

primarily affect the output in the first 12 to 18 months, and well spacing and room in the

sweet spots no doubt has some effect (offsetting the greater number of frack stages etc.).

The combination of longer lateral lengths and advancements in completion technology has

allowed operators to increase the number of frac stages during completions and space them

closer together. The result has been a higher completion cost per well but with increased

production and more emphasis on profitability.

In the past five years, DTC Energy Group completion supervisors in the Bakken have helped

oversee a dramatic increase from an average of 10 stages in 2008 to 32 stages in 2013. Even

40-stage fracs have been achieved.

One of the main reasons for this is the longer lateral lengths – operators now have

twice as much space to work with (10,000 versus 5,000 feet along the lateral). Frac stages are

also being spaced closer together, roughly 300 feet apart as compared to spacing up to 800 feet

in 2008, as experienced by DTC supervisors.

By placing more fracture stages closer together, over a longer lateral length, operators

have successfully been able to improve initial production (IP) rates, as well as increase EURs

over the life of the well.

blah blah, but they make clear the years have increased length. Freddy was talking about

well spacing, this text is about stage spacing, but that is achieved because of lateral

length.

Freddy can you revisit your graph code? It's just bizarre that different length wells have

the same flow rate 2 yrs out, and later.

Take a look at Enno´s graphs at https://shaleprofile.com/ . They look the same as my graphs and

we have collected and processed the data independently from each other.

If the wells have the same wellbore riser design irrespective of lateral length (i.e. same

depth, which is a given, same bore, same downhole pump) then that section might become the main

bottleneck later in life and not the reservoir rock. With a long fat tail that seems more

likely somehow compared to the faster falling Eagle Ford wells say (but that is just a guess

really). But there may be lots of other nuances, we just don't have enough data in enough

detail especially on the late life performance for all different well designs – it looks

like the early ones are just reaching shut off stage in numbers now. I doubt if the E&Ps

concentrated on later life when the wells were planned – they wanted early production,

and still do, to pay their creditors and company officers bonuses (not necessarily in that

order).

Hmmm. I know it is speculation, but can you flesh that out?

If some bottleneck physically exists that defines a flow rate for all wells from all years

then that does indeed explain the graphs, but what such thing could exist that has a new number

each year past year 2?

We certainly have discussed chokes for reservoir/EUR management, but the same setting to

define flow regardless of length?

The flow depends on the available pressure drop, which is made up of friction through the rock

and up the well bore (plus maybe some through the choke but not much), plus the head of the

well, plus a negative number if there is a pump. The frictional and pump numbers depend on the

flow and all the numbers depend on gas-oil ratio. Initially there is a big pressure drop in the

rock because of the high flow, then not so much. Once the flow drops the pressure at base of

the well bore just falls as a result of depletion over time, the effect of the completion

design is a lot less and lost in the noise, so all the wells behave similarly. That's just a

guess – I have never seen a shale well and never run a well with 10 bpd production,

conventional or anything else.

A question might be if the flow is the same why doesn't the longer well with the bigger

volume deplete more slowly, and I don't know the answer. It may be too small to notice and lost

in the noise, or to do with gas breakout dominating the pressure balance, or just the way the

the physics plays out as the fluids permeate through the rock, or we don't have long enough

history to see the differences yet.

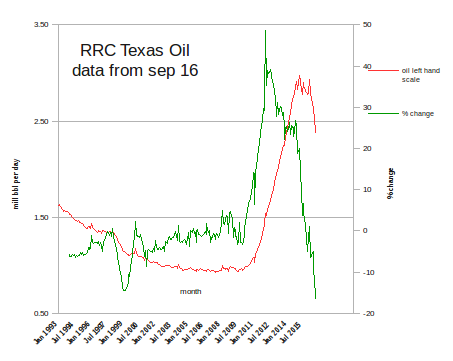

RRC Texas for September came out recently. As others will probably elaborate more on the data,

I just want to show if year over year changes in production could be use as a predictive tool

for future production (see below chart).

It is obvious that year over year changes (green line) beautifully predicted oil production

(red line) at a time lag of about 15 month. Even when production was still growing, the steep

decline of growth rate indicated already the current steep decline.

The interesting thing is that the year over year change is a summary indicator. It does not

tell why production declines or rises. It can be the oil price, interest rates or just

depletion – even seasonal factors are eliminated. It just shows the strength of a

trend.

I am curious myself how this works out. The yoy% indicator predicts that Texas will have

lost another million bbl per day by end next year. That sounds quite like a big plunge. One

explanation could be the fact that we have now low oil prices and high interest rates. In all

other cycles it has been the other way around: low oil prices came hand in hand with low

interest rates. This could be now a major obstacle for companies to grow production.

This concept of following year over year changes works of course just for big trends, yet

for investment timing it seems exactly the right tool. Another huge wave is coming in electric

vehicles which are growing in China by 120% year over year. Here we have the same situation as

for shale 7 years ago: Although current EV sales are barely 1 million per year worldwide, the

growth rate reveals already an huge wave coming. So as an investor it is always necessary to

stay ahead of the trend and I think this can be done by observing the year over year%

change.

Big trouble is brewing in the mighty North Dakota Bakken Oil Field. While oil production in

the Bakken has reversed since it bottomed in 2016 and increased over the past few years, so has

the amount of by-product wastewater. Now, it's not an issue if water production increases along

with oil. However, it's a serious RED FLAG if by-product wastewater rises a great deal more

than oil.

And... unfortunately, that is exactly what has taken place in the Bakken over the past two

years. In the oil industry, they call it, the rising "Water Cut." Furthermore, the rapid

increase in the amount of water to oil from a well or field suggests that peak production is at

hand . So, now the shale companies will have an uphill battle to try to increase or hold

production flat as the water cut rises.

According to the North Dakota Department of Mineral Resources, the Bakken produced 201

million barrels of oil in the first six months of 2018. However, it also produced a stunning

268 million barrels of wastewater:

Thus, the companies producing shale oil in the Bakken had to dispose of 268 million barrels

of by-product wastewater in just the first half of the year. I have spoken to a few people in

the industry, and the estimate is that it cost approximately $4 a barrel to gather, transport

and dispose of this wastewater. Which means, the shale companies will have to pay an estimated

$2.2 billion just to get rid of their wastewater this year.

Now, some companies may be recycling their wastewater, but this isn't free. Actually, I have

seen estimates that it cost more money to recycle wastewater than it does to simply dispose of

it. So, as the volume of wastewater increases while the percentage of oil production declines,

then the shale companies are hit with a double-whammy... less oil revenue and rising wastewater

disposal costs.

To give you an idea just how much more water is being produced versus oil in the Bakken, I

went back to the North Dakota Department of Mineral Resources and looked at their data back to

2015. Unfortunately, the data published in excel only goes back to 2015, even though they have

figures published in PDF form starting in 2003.

Regardless, four years is plenty of time to show just how bad the situation is becoming in

the Bakken. In June 2015, the North Dakota Bakken produced 16% more water than oil. However

June this year, the Bakken field produced 38% more water than oil :

You will notice that overall oil and water production declined in 2016, due to the falling

oil price, but as production grew in 2017 and 2018, the percentage increase of by-product

wastewater surged to 32% and 38% respectively. Here is an interesting comparison:

Bakken Oil & Water Production:

June 2015 Oil = 34.4 million barrels

June 2015 Water = 39.8 million barrels (16% more water)

June 2018 Oil = 33.8 million barrels

June 2018 Water = 46.8 million barrels (38% more water)

As we can see, while overall Bakken oil production in June 2018 was less than it was in June

2015, the volume of waster water increased by an additional 7 million barrels.

I believe there are two negative forces at work in the Bakken as it pertains to the rising

volume of wastewater.

As the wells and field age, more water is produced than oil

Larger Frac Stages, which require more water and sand, are now being utilized to keep

production growing or to keep it from falling

While a rising water cut isn't a surprise to the industry as it is a natural progression of

an aging oil well or field, the use of Larger Frac Stage wells should be a WAKE-UP CALL to

investors. Why? Because Larger Frac Stage wells consume a great deal more water and sand to

produce more oil initially, but the decline rates are even more severe than regular shale

wells.

So, when the Investor Relations are bragging how the companies are using the newer

technology of more complex Large Frac Stage wells, this isn't a good sign. This means that the

company is now desperate to try and grow production, or at worst, to keep it from falling.

Unfortunately, the U.S. Shale Industry is in serious trouble. Most of the shale fields have

reached a peak and when production starts to decline, especially during a collapsing oil price,

I forecast a rapid disintegration of the industry. We must remember, as the oil price and oil

production falls, then company stock and asset values will plummet while the high debt levels

remain. Thus, the shale industry will have increasing difficulty in servicing its debt.

I will continue to monitor the production of oil and wastewater in the Bakken. Please check

back for updates.

The completed around 95 according to my data. The is lag in the data on confidential wells

that will show up next month in the final data. Also if the Bakken was to get and hold 1.4

million barrels a day the would need to complete around 1500 wells per year.

"... I have mentioned this before, but SERIOUS TROUBLE will come down hard on the Bakken. Looks like someone hasn't been honest about its production figures. ..."

"... Fireworks will arrive shortly .. hehehe. ..."

I have mentioned this before, but SERIOUS TROUBLE will come down hard on the Bakken. Looks like someone hasn't been honest

about its production figures.

active wells increased by 158 from August to Sept and output increased by 19 kb/d for the Bakken Three Forks to 1055 kb/d.

Only 77 new wells were completed in the North Dakota in August 2017 and output increased that month by 23 kb/d.

They have added over 1,100 Bakken and/or Three Forks wells to boost production back to where it was in March, 2016.

So, conservatively $8 billion spent just to climb back up.

The amount of capital being burned on energy in the USA is truly remarkable.

Dennis, I have seen data that shows the total cost of all "shale" oil and gas wells from maybe 2003 forward, and then the gross

proceeds from same. Very interesting how far from payout the USA wells are, in aggregate.

"... So perhaps Bakken oil production peaked in 2015. But that depends on how many new wells will be added the coming years. ..."

"... Regarding downspacing, it has been a real crapshoot throughout all the shale plays. Operators had been purposefully drilling closer and closer and monitoring results. The biggest influencing factors (among many) seems to be the permeability and brittleness of the rock. ..."

"... Utica operators are back to 1,000 foot spacing while Marcellus operators continue to drill 500′ or less. Again, the thickness of these formations plays a big role as 3 dimension, not 2, come into play. 80% production in offset wells is the commonly quoted figure from several operators, and they seem to be okay with that. ..."

"... Be advised, Bakken operators have recently changed their flowback procedures and early month produced water numbers have skyrocketed. New wells now show 150/200 thousand barrels produced water their first few months online. ..."

Thanks that is really interesting. As most wells in Bakken are 10000 feet long, 500 feet well

spacing would translate into about 5 wells per section in Bakken. As I mentioned some time

ago, the Grail area in McKensey has close to 5 wells per section now. The 2016 wells there

had worse production than previous years and they have almost stopped drilling new wells

there. As there are maybe 1500 well locations left in the sweet spot area of McKensey

(assuming 5 wells per section) and they are adding perhaps 40 wells per month now, it means

that there are only some 3 years of new wells left. But it's not like they will add 40 wells

per month and then suddenly stop.

So more and more wells need to come from outside the sweet spots the coming years. Because

of the red queen phenomena, if new wells start to produce less, then more wells are needed

just to keep total production flat. So perhaps Bakken oil production peaked in 2015. But

that depends on how many new wells will be added the coming years.

One needs to remember the Three Forks formation when doing those kind of calculations.

Some of the higher producing wells in North Dakota these past 2 years targeted the second

bench of the TF.

There have been very few third bench TF wells and, I believe, only a couple targeting the

fourth bench so far.

Regarding downspacing, it has been a real crapshoot throughout all the shale plays.

Operators had been purposefully drilling closer and closer and monitoring results. The

biggest influencing factors (among many) seems to be the permeability and brittleness of the

rock.

Utica operators are back to 1,000 foot spacing while Marcellus operators continue to

drill 500′ or less. Again, the thickness of these formations plays a big role as 3

dimension, not 2, come into play. 80% production in offset wells is the commonly quoted

figure from several operators, and they seem to be okay with that.

BTW, I appreciate the charts you regularly post here.

Be advised, Bakken operators have recently changed their flowback procedures and early

month produced water numbers have skyrocketed. New wells now show 150/200 thousand barrels

produced water their first few months online.

"... Hopefully everyone involved in defending Bakken production upswings will not disappear into the woodwork next month, or the month after, when production drops again. ..."

"... Of course marginal shale oil wells that are at or below economic limits get shut in during winter, or get shut in and stay shut in because workover costs to restore production simply do not make economic sense. ..."

"... Re-frac's cost more money. At $20.00 per barrel net back prices a $2.5-3.0M re-frac requires ANOTHER 137,000 BO to payout. Productivity should never be confused with profitability (or lack thereof); in the end the latter always wins out. ..."

"... A little more time and realized production data will prove that downsizing actually reduced UR per incremental well and was yet another economic disaster in a string of economic disasters for the shale oil industry, the biggest being oversupply and an ensuing 70% drop in product prices. ..."

Hopefully everyone involved in defending Bakken production upswings will not disappear into

the woodwork next month, or the month after, when production drops again.

Of course marginal shale oil wells that are at or below economic limits get shut in during

winter, or get shut in and stay shut in because workover costs to restore production simply do

not make economic sense. There are gazillions of those kinds of well in all three of America's

shale oil basins. There need not be a flush 'uptick' of production when those wells come back

on line (that's investor presentation dribble), in fact it can be just the opposite because of

bubble point/higher water saturations.

Re-frac's cost more money. At $20.00 per barrel net back prices a $2.5-3.0M re-frac requires

ANOTHER 137,000 BO to payout. Productivity should never be confused with profitability (or lack

thereof); in the end the latter always wins out.

Imagine a situation where you are drilling these $6.5M wells so close together (Marathon at

330 feet, toe to toe) that you have to "protect" them by shutting them in for prolonged periods

of time while you frac a new well 3000 feet away. That makes a lot of sense, doesn't it?

A little more time and realized production data will prove that downsizing actually reduced

UR per incremental well and was yet another economic disaster in a string of economic disasters

for the shale oil industry, the biggest being oversupply and an ensuing 70% drop in product prices.

The actual reserve that is being produced in the Bakken was "discovered, undeveloped and developed"

in 2013, and not covered by the USGS. It's difficult to find break out information for individual

areas in most companies reports but I don't think there was more than about 5 Gb developed and

undeveloped reserves in 2013, and it might have declined a bit since then, even including actual

production.

Bakken production down 86,150 barrels per day to 895,330 bpd. North Dakota production

down

92,029 bpd

to 942,455 bpd. It was noted that this the largest decline ever in North Dakota

production. But it should not be overlooked that the October in crease in production was also the

largest ever increase in North Dakota production.

EIA wildly optimistic in Bakken, Gulf and Texas. Their current numbers have

to be way high in relation to what is actually happening. Even Texas RRC

site is not predicting an upturn until current permits and completions get a

lot higher. At $53 oil, it is not happening, or going to happen.

In my view there is simply a cost issue here. If a

well goes from 100 barrels to 20 barrels per day, the mainenance,

operating and transport costs go up fivefold per barrel, even if

they are the same for the well. So, it might not pay off to send a

crew there and pay for transport. Unless, the oil price does not go

up, these wells and many more wells are likely to shut down for a

while.

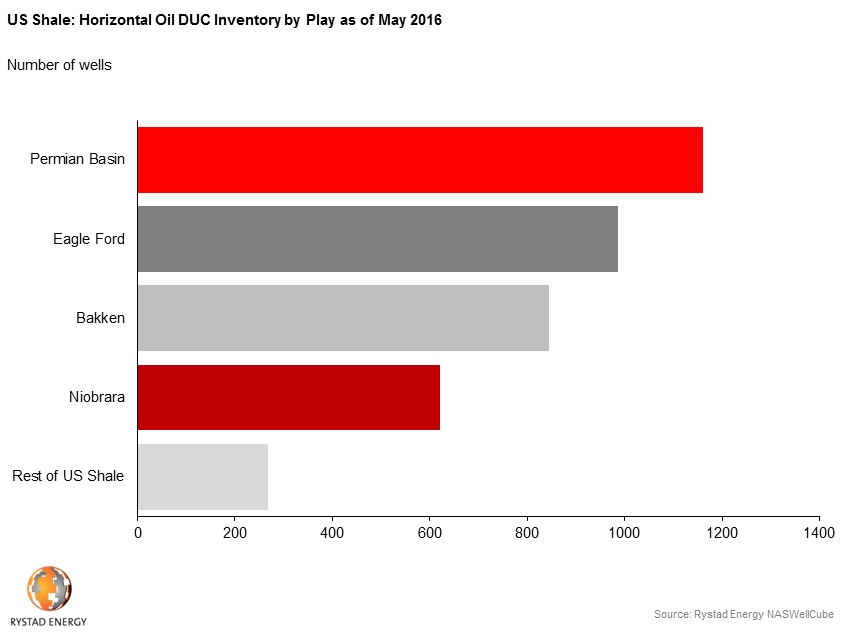

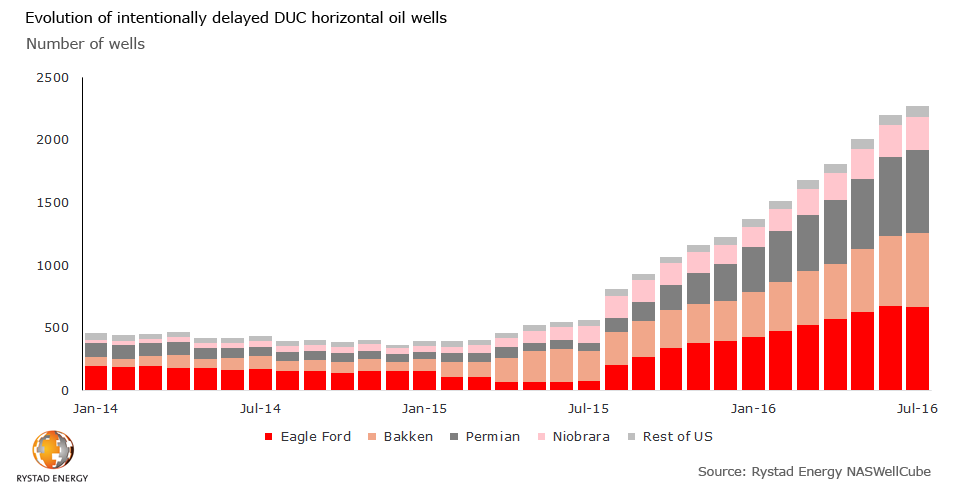

I saw a recent story about the rise in the cost of fracking to completion

for these DUC wells. Costs are said to have risen to something like $3.2

million in some of the areas where wells need completion. I believe the

Director's Cut said last month there were 86o wells awaiting completion.

If the story I read was true, then it will be around $2.8 billion to

frack those 860 wells. I don't know what the cost of getting a well to

the DUC stage is, but it sure seems a lot of money to have sunk in the

ground for wells that will be outputting just 100 barrel a day after

their first 24 months.

Bruno Verwimp wrote back in 2016, September 16th, " .Hold your breath for

the next winter. It might bring severe decline in oil production in ND

Bakken ."

I wrote at the same time: " FWIW my 'money' is on Verwimp's observation

and model for the Bakken. I for one will be interested to see your chart

next spring!"

Another 3 months will be interesting. By the look of it, it might well be

down to 700,000 bpd in a year if the uncanny accuracy continues. As I

understand it, his chart has nothing in it derived from price.

That is correct. Verwimp's model has no oil price input. This is a

serious problem since everybody recognizes that oil price has been

determinant in the current oil situation. Therefore one can only conclude

that Verwimp's model is accurate due to chance, and therefore has no

predicting capability. It will continue to be accurate until it doesn't.

It probably represents oil production decay in the absence of sufficient

economical incentive.

Geology absolutely plays a role, especially when oil

prices are relatively high it is clear which fields are constrained by

geology. When oil prices fall by a factor of 3 or 4 fields that are

not constrained by geology will decline due to economic constraints

(poor profitability.) The Bakken only increased in output due to high

oil prices and a high well completion rate. Eventually geology will be

the reason for Bakken decline, low oil prices clearly are the reason

at present.

In Jan 2018 your model predicts about 680 kb/d for ND Bakken/TF

output. My 61 well model predicts about 818 kb/d in Jan 2018 and the

85 well model predicts 900 kb/d in Jan 2018, I expect ND Bakken/Three

Forks output will be around 825 to 900 kb/d in Jan 2018, with a best

guess of 866 kb/d (847 kb/d in Dec 2018). This corresponds to a 75

well model, chart below.

A big contributor to the legacy oil decline is the unrelenting physics of

fluid phase behavior, with gas becoming more prevalent in the production

stream. Statewide GOR increased from 1200 to 1500:1 cuft/bo in 2015. The

legacy wells will be worse (i.e. the newer wells dampen the effect, which

have an initial GOR of ~ 1000:1). For reference, generally a GOR> 2000:1 is

considered a "gas" well or field.

Most of these LTO fields will eventually be abandoned as gas fields.

note – I tried to post a *.png graph, but the reply tool failed.

Is the 2000 GOR a North Dakota convention? There's no reservoir

engineering reason to designate a depleted well as a gas well when GOR

increases to 2000 scf/bo. Depleted oil wells under depletion drive do

experience very high GORs, but they remain oil wells.

My recall is there's a regulation in Texas that classifies liquids

from a gas well as condensate vs oil from an oil well. Almost

certainly has some tax consequence.

Munger would have us import oil and gas now from OPEC so that we can save

our oil and gas for the future when the world is going to have major

shortages."

The day comes when a firebrand is in control and dares to rock the

societal systemic boat by declaring the price of oil will be non

monetary. You want oil from Russia, America? Disarm. You want oil from

KSA, America? Convert to Islam.

"We have enough of your dollars created from thin air. Let's have

something of real value to us before we send you oil. The price is

described above."

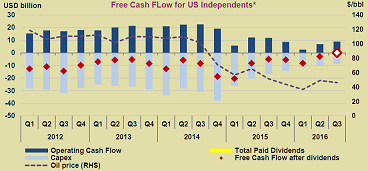

"... Looking at Bakken(ND) as one big project, it has now spent an estimated total of about $36Billion more than generated from net operational cash flows (Jan-09 – Dec-16). To reach pay out for the wells started in 2009-2016 requires an estimated oil price of $65/bo (WTI) starting Jan-17. To get a return of 2.5% (which is, call it, an inflation hedge) on the $36B requires an estimated oil price of $77/bo (WTI). ..."

"... To enable a debt reduction requires a net positive cash flow from operations and the longer it takes before positive cash flow happens, the higher the required oil price becomes to earn some return. ..."

"... Some of this $36B debt has already been written down (also through bankruptcies (Chapter 11s), the business model is not sustainable with low oil prices!), which means that the companies now needs to recover less than the $36B. ..."

"... Write downs/impairments shrinks the affected companies' assets/equities and thus debt carrying capacities. Some make forecasts about future developments without considering the companies' balance sheets. ..."

"... At present oil pries (low/mid 50's) the companies may add an average of 60-70 wells/month from cash from operations, this will likely be a mixture of DUCs and "new" wells. ..."

"... For 2017 I expect companies in Bakken(ND) will continue to spend above what is generated from operations. ..."

To keep the Dec-15 output level from Bakken(ND) through 2016, I estimated this would require

the addition of an average of about 95 wells/month (61 wells/month were added through 2016).

In 2016 an estimated $2.0 – $2.5Billion more than (net) cash flow from operations was spent.

This is about 300 – 350 new wells (spud to flow).

Without this external capital infusion fewer wells would have been brought to flow and thus

a steeper decline in production.

Looking at Bakken(ND) as one big project, it has now spent an estimated total of about

$36Billion more than generated from net operational cash flows (Jan-09 – Dec-16). To reach

pay out for the wells started in 2009-2016 requires an estimated oil price of $65/bo (WTI)

starting Jan-17. To get a return of 2.5% (which is, call it, an inflation hedge) on the $36B

requires an estimated oil price of $77/bo (WTI).

To enable a debt reduction requires a net positive cash flow from operations and the

longer it takes before positive cash flow happens, the higher the required oil price becomes

to earn some return.

Some of this $36B debt has already been written down (also through bankruptcies (Chapter

11s), the business model is not sustainable with low oil prices!), which means that the companies

now needs to recover less than the $36B.

Write downs/impairments shrinks the affected companies' assets/equities and thus debt

carrying capacities. Some make forecasts about future developments without considering the

companies' balance sheets.

At present oil pries (low/mid 50's) the companies may add an average of 60-70 wells/month

from cash from operations, this will likely be a mixture of DUCs and "new" wells.

For 2017 I expect companies in Bakken(ND) will continue to spend above what is generated

from operations.