In recent years Americans have been hearing that the United States is poised to regain

its role as the world’s premier oil and natural gas producer, thanks to the widespread use

of horizontal drilling and hydraulic fracturing (“fracking”). This “shale revolution,”

we’re told, will fundamentally change the U.S. energy picture for decades to come—leading

to energy independence, a rebirth of U.S. manufacturing, and a surplus supply of both oil

and natural gas that can be exported to allies around the world. This promise of oil and

natural gas abundance is influencing climate policy, foreign policy, and investments in

alternative energy sources.

The term "shale bubble" is about the idea that the United States is poised to regain "energy

independence" becoming again net exporter instead of major importer of oil and natural gas.

The primary driver of the propaganda campaign was the U.S. Department of Energy’s Energy

Information Administration (EIA). The key technologies that were enabler of shell boom were:

Oil and gas outfit Fieldwood Energy is now in the market with a $2.63 billion

covenant-lite first- and second-lien acquisition loan.

...As lending to lower-rated companies has increased generally, more of them

are also opting for covenant-lite financings.

That trend is evident particularly in the B3 ratings category. Around 18 percent of covenant-lite

loans are for B3 rated companies so far this year, versus 8 percent in 2012 and 3.7 percent in

2011

...Loan portfolio managers said that new institutional clients are also seeking to invest.

More than $57 billion of CLOs have been issued this year, topping 2012 volume.

This refinancing bulge in 2016 became more compressed in time and more imminent.

Most of the defaults, debt restructurings, and bankruptcies so far this year and last year

were triggered when over-indebted cash-flow negative companies could not make interest

payments on their debts.

During the crazy days of the peak of the credit bubble two years ago, they would have been

able to borrow even more money at 8% or 9% and go on as if nothing happened. But those days

are gone. Now the riskiest companies face interest costs of 20% or higher – if they’re able to

get new money at all. Hence, the wave of debt restructurings and bankruptcies.

But that’s small fry. Now comes the wave of companies whose debts mature. They will have to

borrow new money not only to fund their interest payments, cash-flow-negative operations, and

capital expenditures, but also to pay off maturing debt.

That “refinancing cliff” is going to be the biggest, steepest ever, after the greatest credit

bubble in US history when companies took on record amounts of debt, and it comes at the worst

possible time, warned Moody’s in its annual report.

In its report a year ago, Moody’s had already warned that the refinancing cliff for junk-rated

US companies over the next five years – at the time, from 2015 through 2019 – would hit $791

billion. Of that, $349 billion would mature in 2019, the largest amount ever to mature in a

single year.

...Among the other macroeconomic factors, Moody’s lists the slowdown in China and

volatility in oil prices. And there’s another factor that will “make it more difficult for

lower-rated companies to refinance”: worried regulators have been cracking down on banks’

exposure to leveraged loans, which are so risky that even the Fed has been fingering them

publicly.

Banks sell these leveraged loans to loan mutual funds or repackage them into collateralized

loan obligations (CLOs) which they then sell in tranches to institutional investors. When

leveraged loans mature, companies have to come up with the money, but Moody’s warns that

“rising defaults and the impact of the Dodd-Frank Act’s risk retention rule will make it more

difficult for existing CLOs to supply corporate financing.”

The widespread use of horizontal drilling and hydraulic fracturing, the technologies

that while expensive (and unable compete with conventiona oil production price wise) , continue

to evolve and improve.

Spike of oil prices in 2011-2014

This fake promise of oil and natural gas abundance affected both domestic government priorities

and foreign policy. Domestically it slowed down rising of private car fleet efficiency d as well as

investments in alternative energy sources. The implications of this are profound. If the “shale

revolution” is nothing more than a temporary respite from the inevitable decline in US oil and gas

production (not a revolution but a retirement party), then why are there is such a rush to rewrite our

domestic and foreign policy as if we’re going to be “Saudi America” for the rest of the century?

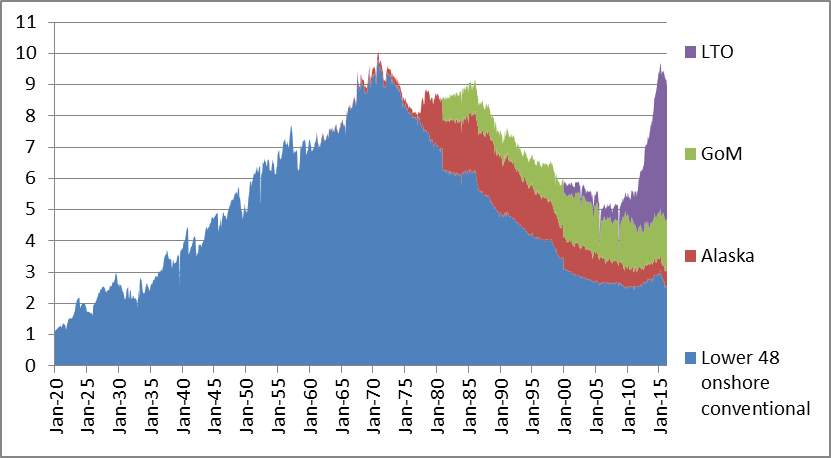

In 2015 U.S. shale oil production has peaked, productivity gains have flatlined and the cheap

money has all but disappeared. Has the U.S. shale game finally blown over? (Alberta

Oil Magazine, Jan 7, 2016):

To summarize the damage: output has peaked, the cheap money and easy private equity are gone,

the gains in per-rig productivity have slowed and the 20 to 30 per cent break that E&P companies

were getting from contractors for labor costs won’t go on much longer. By all metrics, the shale

party is nearly over. The question now is whether the 2015 production peak will forever be the

high-water mark for this uniquely North American industry.

There are three major sources of "subprime" oil: tight oil, shale oil and tar sands.

The term oil shale generally refers to any sedimentary rock that contains solid

bituminous materials (called kerogen) that are released as petroleum-like liquids

when the rock is heated in the chemical process of pyrolysis. Oil shale was formed millions of years

ago by deposition of silt and organic debris on lake beds and sea bottoms. Over long periods of time,

heat and pressure transformed the materials into oil shale in a process similar to the process that

forms oil; however, the heat and pressure were not as great. Oil shale generally contains enough

oil that it will burn without any additional processing, and it is known as "the rock that burns".

Oil shale can be mined and processed to generate oil similar to oil pumped from conventional oil

wells; however, extracting oil from oil shale is more complex than conventional oil recovery and

currently is more expensive. The oil substances in oil shale are solid and cannot be pumped directly

out of the ground. The oil shale must first be mined and then heated to a high temperature (a process

called retorting); the resultant liquid must then be separated and collected. An

alternative but currently experimental process referred to as in situ retorting

involves heating the oil shale while it is still underground, and then pumping the resulting liquid

to the surface.

What bother many observers is the amount of unprofitable (supported by junk bonds) shale oil that

come to the market in the relatively short period of time.

“There is this huge myth propagated by the MSM as well as several of the well-known names in the

alternative analyst community about the wonders of SHALE ENERGY. I can’t tell you how many readers

send me articles from some of these analysts stating how the United States will become energy independent

while pumping some of these shale energy stocks. Nothing has changed in America….. there’s always

another sucker born every minute.

It is extremely frustrating to see the continued GARBAGE called analysis on the SHALE ENERGY INDUSTRY.

I have written several articles listing the energy analysts that I believe truly understand what

is taking place in U.S. energy industry. They are, Art Berman, Bill Powers, David Hughes, Jeffrey

Brown and Rune Likvern.”

While this conversion of junk bonds into oil has features of classic bubble (excessive greed) but

it was also different in some major aspects.

We know that bankers like bubbles because they always make money on swings, either going up or down.

We can accept that that is how things work on this planet under neoliberalism but that does not turn

them less crazy.

At the beginning this was about shale gas, only later it became about shale and tight oil production.

But shale oil production did has major elements of a bubble. And greed was present in large qualities.

Special financial instruments like ETN were created to exploit this greed. MSM staged a compaign of

how the wonders of technology, specifically horizontal drilling and hydraulic fracturing, have unleashed

a new era for energy supplies. Without mentioning that for each dollar shale industry recovered 1.5

dollar of junk bonds was created.

If we think about it in bubble terms that the key selling point of this bubble was that it will lead

to America’s energy independence, a manufacturing renaissance, and will lower gas bills for everyone.

The estimates (based on past reservoir dynamics) were grossly over represented. The factor that is present is bubbles is that they create excess production that at some point far outpace

the demand.

North American crude oil producers are not cash flow positive, and they haven’t been since the beginning

of the shale boom. Capital expenses of shale companies has consistently exceeded cash flow even at $100

per barrel oil price. So essentially this was a risky gamble that oil will go higher, and this gamble failed.

At least for now.

Most experts and analysts agree that, at current oil prices, the shale oil sector will need to

dramatically reduce per-barrel costs in order to make the vast majority of North American plays

viable. “The minimum price I’ve seen [to make production worthwhile] is $50 a barrel in the

very best possible scenarios and with the very best technology,” says Farouq Ali, a chemical and

petroleum engineer at the University of Calgary. “But most of the time they need $65 oil. So the

5.5 million shale barrels we see right now will all decline, but they will decline over time

because there are still thousands of wells. Even if oil prices go to $60 they will still decline

because that’s just not enough profit to operate.”

Of course, those returns aren’t just diminishing on the production side, but in the

pocketbooks of investors, too. Wunderlich Securities senior vice-president Jason Wangler

describes the rise of U.S. shales as a “perfect storm” of cheap money, seemingly limitless

production potential and rapidly advancing technologies. “Now the money is hard to come by,”

Wangler says over the phone from the firm’s Houston office. “With oil at $90 or $100 it was

pretty hard not to be economic.” But that old high-price environment, he says, caused significant

overinvestment in shale assets, including in risky bets on barely marginal plays like the

Tuscaloosa Marine Shale formation that spans parts of Louisiana and Mississippi. “But if you look

at the last year or so, you’ve seen a lot of folks really focus on the Permian and on the

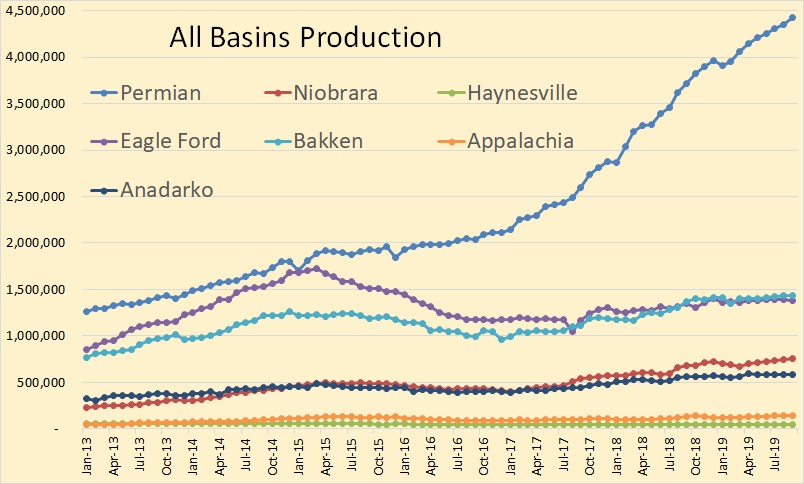

Niobrara,” Wangler says. “Meanwhile you’ve seen the Bakken really fall off very, very hard, as

well as the Eagle Ford and the mid-continent area.”

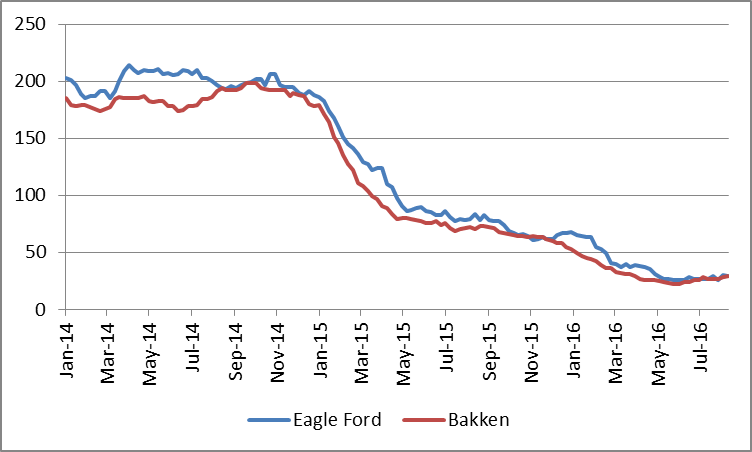

The decreasing viability of the Bakken region is especially significant. Houston-based shale

expert and petroleum geologist Arthur Berman estimates that with West Texas oil trading at $46, a

mere one per cent of the massive Bakken shale play is profitable. At those prices, just four per

cent of the horizontal wells that have been drilled in the Bakken since 2000 would recover their

costs for drilling, completion and operations, according to Berman. Add to that the competition

from Western Canadian crude oil, which continues to travel down through the U.S. Midwest via rail

and pipeline, and one can assume that a lot of Bakken production will remain economically

underwater without a significant price correction or some breakthrough in cost savings. “In the

Bakken, you’ve got a long way to transport to get that oil to market,” Wangler says. “Obviously

you’re fighting with all that Canadian crude coming down, which makes the price more difficult.

It’s also expensive to [transport oil out of] North Dakota, whether you’re going to the Gulf

Coast or you’re going east or west.”

Due to the dramatic drop of oil prices shale bubble start deflation. Several bankruptcies occurred

in 2015. More expected in 2016 if the price not recover.

Some critics to argue the business model of shale production is fundamentally unsustainable. Before

the oil rice collapse, which started at mid 2014, immediately after signing Iran deal (strange coincidence)

it was expected that producers would have positive returns for the first time in 2015”

“Only 1% of the Bakken Play area is commercial at current oil prices based on my analysis

that follows.

Only 4% of horizontal wells drilled since 2000 meet the EUR (estimated ultimate recovery)

threshold needed to break even at current oil prices, drilling and completion, and operating costs.

The leading producing companies evaluated in this study are losing $11 to $38 on each barrel

of oil that they produce, the very definition of waste. …”

While oil shale is found in many places worldwide, by far the largest deposits in the world are

found in the United States in the Green River Formation, which covers portions of

Colorado, Utah, and Wyoming. Estimates of the oil resource in place within the Green River Formation

range from 1.2 to 1.8 trillion barrels. Not all resources in place are recoverable; however, even

a moderate estimate of 800 billion barrels of recoverable oil from oil shale in

the Green River Formation is three times greater than the proven oil reserves of Saudi Arabia. Present

U.S. demand for petroleum products is about 20 million barrels per day. If oil shale could be used

to meet a quarter of that demand, the estimated 800 billion barrels of recoverable oil from the Green

River Formation would last for more than 400 years1.

More than 70% of the total oil shale acreage in the Green River Formation, including

the richest and thickest oil shale deposits, is under federally owned and managed lands.

Thus, the federal government directly controls access to the most commercially attractive portions

of the oil shale resource base.

See the Maps page for

additional maps of oil shale resources in the Green River Formation.

The Oil Shale Industry

While oil shale has been used as fuel and as a source of oil in small quantities for many years,

few countries currently produce oil from oil shale on a significant commercial level. Many countries

do not have significant oil shale resources, but in those countries that do have significant oil

shale resources, the oil shale industry has not developed because historically, the cost of oil derived

from oil shale has been significantly higher than conventional pumped oil. The lack of commercial

viability of oil shale-derived oil has in turn inhibited the development of better technologies that

might reduce its cost.

Relatively high prices for conventional oil in the 1970s and 1980s stimulated interest and some

development of better oil shale technology, but oil prices eventually fell, and major research and

development activities largely ceased. More recently, prices for crude oil have again risen to levels

that may make oil shale-based oil production commercially viable, and both governments and industry

are interested in pursuing the development of oil shale as an alternative to conventional

oil.

Oil Shale Mining and Processing

Oil shale can be mined using one of two methods: underground mining using the

room-and-pillar method or surface mining. After mining, the oil shale is transported

to a facility for retorting, a heating process that separates the oil fractions of oil shale from

the mineral fraction.. The vessel in which retorting takes place is known as a retort.

After retorting, the oil must be upgraded by further processing before it can be sent to a refinery,

and the spent shale must be disposed of. Spent shale may be disposed of in surface impoundments,

or as fill in graded areas; it may also be disposed of in previously mined areas. Eventually, the

mined land is reclaimed. Both mining and processing of oil shale involve a variety of environmental

impacts, such as global warming and greenhouse gas emissions, disturbance of mined land,

disposal of spent shale, use of water resources, and impacts on air and water quality. The development

of a commercial oil shale industry in the United States would also have significant social

and economic impacts on local communities. Other impediments to development of the oil shale

industry in the United States include the relatively high cost of producing oil from oil shale (currently

greater than $60 per barrel), and the lack of regulations to lease oil shale.

Surface Retorting

While current technologies are adequate for oil shale mining, the technology for surface retorting

has not been successfully applied at a commercially viable level in the United States, although technical

viability has been demonstrated. Further development and testing of surface retorting technology

is needed before the method is likely to succeed on a commercial scale.

In Situ Retorting

Shell Oil is currently developing an in situ conversion process (ICP). The process

involves heating underground oil shale, using electric heaters placed in deep vertical holes drilled

through a section of oil shale. The volume of oil shale is heated over a period of two to three years,

until it reaches 650–700 °F, at which point oil is released from the shale. The released product

is gathered in collection wells positioned within the heated zone.

Shell's current plan involves use of ground-freezing technology to establish an underground barrier

called a "freeze wall" around the perimeter of the extraction zone. The freeze wall

is created by pumping refrigerated fluid through a series of wells drilled around the extraction zone.

The freeze wall prevents groundwater from entering the extraction zone, and keeps hydrocarbons and

other products generated by the in-situ retorting from leaving the project perimeter.

Shell's process is currently unproven at a commercial scale, but is regarded by the U.S. Department

of Energy as a very promising technology. Confirmation of the technical feasibility of the concept,

however, hinges on the resolution of two major technical issues: controlling groundwater during production

and preventing subsurface environmental problems, including groundwater impacts.1

Both mining and processing of oil shale involve a variety of environmental impacts,

such as global warming and greenhouse gas emissions, disturbance of mined land; impacts on wildlife

and air and water quality. The development of a commercial oil shale industry in the U.S. would also

have significant social and economic impacts on local communities. Of special concern

in the relatively arid western United States is the large amount of water required for oil shale processing;

currently, oil shale extraction and processing require several barrels of water for

each barrel of oil produced, though some of the water can be recycled.

1RAND Corporation Oil Shale Development in the United

States Prospects and Policy Issues. J. T. Bartis, T. LaTourrette, L. Dixon, D.J. Peterson, and

G. Cecchine, MG-414-NETL, 2005.

For More Information

Additional information on oil shale is available through the Web. Visit the

Links page to access sites

with more information.

Two years ago, Wall Street banks were on their way out of a long-term relationship with the

oil industry. Now, with oil prices over $70 for the first time in three years, big bond buyers

are snapping up oil bonds once again.

Only there is a condition this time.

The Wall Street Journal's Joe Wallace and Collin Eaton

wrote this week that Wall Street was buying bonds from non-investment-grade U.S. energy

companies, which took advantage of record low interest rates to raise some $34 billion in fresh

debt in the first half of the year.

That's twice as much as the industry raised over the same period last year. But investors

don't want borrowers to use the cash to drill new wells. They want them to use it to pay off

older debt and shore up balance sheets.

It makes sense, really, although it is a marked departure from how banks normally react to

oil industry crises. The 2014 oil price collapse, in hindsight, may have been the last "normal"

crisis. Oil prices fell, funding dried up, supply tightened, prices went up, banks were willing

to lend again, and producers poured the money into boosting production.

Since then, however, the energy transition push has really gathered pace and banks have more

than one reason to not be so willing to lend to the oil industry. With the world's biggest

asset managers setting up net-zero groups to effectively force their institutional clients to

reduce their carbon footprint and with the Biden administration throwing its weight behind the

push for lower emissions, banks really have little choice but to follow the current. Their own

shareholders are increasingly concerned about the environment, too.

https://www.youtube.com/embed/aQXqMVeoOPs

Yet business is business, and nowhere is this clearer than in banks' dealings with the oil

industry. Bank shareholders may be concerned about the environment, but they certainly would be

more concerned about their dividend""and part of that comes from income made from lending to

oil. And the higher oil prices go, the more willing banks will be to lend to those that produce

it.

When they were unwilling to lend to the oil industry, other lenders

stepped in . Last year, alternative investment firms scooped up hundreds of millions in oil

industry debt from banks that were cutting their exposure to the politically incorrect

industry. Hedge funds and other so-called shadow lenders don't seem to have banks' misgivings

about profiting from oil and gas.

Now banks have mellowed towards oil somewhat, but it is an interesting twist that the

current loans come with the condition of not boosting output. Again, it makes sense. For years,

the shareholders of U.S. shale oil companies have been complaining about poor returns as the

companies put everything into output growth. Now it's payback time, and shareholders want their

returns.

So do lenders, apparently.

Per the WSJ article, this year, bond buyers "want to see companies repairing their

balance sheets and delivering to creditors and shareholders rather than plowing money into new

wells."

We have owned rigs. We could never keep an operator around long enough to make it

worthwhile. We had a double drum and a single drum. Mud pump. Power swivel. Power tongs on

both. Testing truck. The whole enchilada.

We sold them all to a man who had worked for someone else and then went out on his own. We

gave him a good deal, and he did a lot of work for us. He still does work for us, but he can't

find help that will stay.

We also owned a tank truck. Sold it also. It is currently parked, the man we sold it to

cannot find a driver. He is a one horse tank truck driver. He turns down work all the time. We

had to shut down a lease we haul water on for a few days when he got COVID. Thankfully he

recovered.

All of us around here just cannot quite believe what is going on with the oilfield labor

force. It is a perfect storm.

Meanwhile, most recently we paid $5.63 per foot for 2 3/8" steel tubing, which was under $3

a year ago. We priced a 115 fiberglass tank for $6,800, would have been $3,900 a year ago.

We had a couple wells down for a few weeks because we could neither get new nor rewound

motors for them.

The man who owns the backhoes, trackhoes and cranes that does contract work for us is in his

70's and has great grandkids. He works in the field daily beside his son and grandson.

One of the last rig hands we had broke into our shop last winter. He got out of jail after a

few weeks and immediately got a job in a local factory. Hope he stays clean. He was a good hand

when he was, and had learned to operate a single drum also.

The prosecutor in our county announced the first six months of 2021 that 162 felony cases

had been filed in our small county, that in 2019 the total for the year was 204 felonies, and

that 33 of the 34 jail inmates were addicted to meth.

We do have one pumper now under 50. The rest are from 51 to 63. REPLYINGRAHAMMARK7 IGNORED07/20/2021 at 1:34

am

How much land do you have left? At one well per section how many can you drill and how long

it takes? That's when your business wraps up. REPLYRASPUTIN IGNORED07/20/2021 at 2:40

am

Holy Moly SS

I guess the days of vertical doing things in house are gone. That labor mess is unreal.

However, here in nowhere USA it is hard to find good help but you can usually find help. I was

so surprised at some of the job turnover even during peak covid when some businesses were

restricted and some essential. How are people living that have no jobs? Over the years I hired

relatives that never got it, didn't stay sober and didn't see the long term upside. Maybe it's

all about today for the younger generation.

Over the past year and a half I've been following your posts including labor issues. Were

they so dreadful before covid and helicopter money? It might appear to the uninformed that

training rig help. pumpers and the like is easy, but it's not. One small oops for man is one

huge oops for you.

Perhaps, as we move away from the false narrative that you must have a college degree to get

a good or high paying job, things will improve in the trades and the oilfield.

About 20 years ago I was visiting with a substantial independent stimulation company that

was having labor issues. The head honcho lamented that they had already poached all of the

young guys that grew up on farms and knew machinery, getting up early and how to work. Having

known a few guys and what they earned they most likely didn't point their kids at basket

weaving degrees.

Sure wish I had an answer for you. Personally, I'm shrinking down to a few wells close to

the house/shop/yard, one of which I could walk to for daily exercise. However, I'll run my

equipment myself as long as possible.

The number of basically "homeless" people living here in my part of very rural USA is

startling. People aren't generally sleeping in the parks. They have duffle bags and backpacks

and crash place to place.

We have the tremendous labor shortage, yet the public defender and conflicts public defender

have over 400 clients combined. This in a county of a little less than 20K people. That right

there is the labor force for a decent sized factory around here.

To qualify for the PD you must have income below 125% of federal poverty guidelines, which

is very low. During the height of COVID, nothing got done with their cases because the PD's

couldn't get ahold of them. Few have cell phones that are permanent (track phones) and few have

permanent addresses. The jail is full so there aren't a lot of warrants being issued for the

lower level crimes. So people haven't been showing up for their court cases for months/ over a

year. Our county is going to send close to 100 people to prison this year, almost all for meth

delivery. This is the situation all over rural USA. People who live here and aren't in the

court system are oblivious to it until they get broken into or robbed (or have an addicted

relative, which many do).

The primary reason for the labor shortage here is a combination of young people moving to

larger towns/cities, a very large percentage of the working age population being addicted to

meth (which is now being cut with heroin, fentanyl, etc) and the significant benefits that have

been paid to not work. I hate to think of how many billions of borrowed money stimulus our

future generations are now indebted with that went directly into the pockets of the foreign

drug cartels.

As for the oilfield, add to that the hard work, not the greatest pay in the world at the

bottom end (rig hands) the need to find people who can work unsupervised outdoors, and the

young people being told the industry is dead and a job in that field will soon be gone.

Finally, a ton of "old timers" simply retired during COVID.

Our country has no idea how dependent we are on labor from Mexico and Central America that

keeps us alive. The only farm workers are Hispanic. However, most don't want to work in the

oilfield either, it seems. We just harvested green beans, and all the crew were Hispanic. The

same will be the case here shortly as we harvest watermelons and cabbage. If Trump were

successful and closed the borders and sent everyone back, we would starve.

The largest oil company here shut in everything it owned when oil went negative.

Unfortunately for them they laid off a lot of people. Many of their wells are still idle.

Maybe we are an outlier. But I doubt it. A decent amount people at the lower end of the

labor force seem to have decided they aren't going to work, and offering a lot more $$ won't

bring them back. Maybe they will come back when the government benefits end.

Even the prisons can't find employees. They pay $70K+ plus great benefits. Mentally

difficult work though. Also, can't have a criminal record and cannot use drugs, even pot.

Keep in mind a large percentage of the USA population now smokes or ingests pot. That

doesn't work well in a lot of industries where sobriety is mandatory.

The gas station I fill up at is offering a $300 signing bonus which is paid after 30 days of

no unexcused absences. $13 and hour to start at the cash register. They can't find people to

take that.

I'm rambling now, and I'll stop.

Surely there are some shale basin people reading this. Could any of you comment about

whether there is a labor shortage in your shale basin? If there isn't, maybe we could persuade

a few of them to come to our neck of the woods and work on the simple, shallow wells. Not a lot

of traveling, no weekends unless you pump, and work is daytime only. KANSAS OIL IGNORED07/20/2021 at 9:10

am

Shallow Sand –

I echo all of your sentiments. We are a small operator in Kansas, producing about 300

bbl/day in 13 various counties. We have approximately 50-60 bbl/day offline pushing 3 weeks.

We're talking 8/8ths approximately $75,000 in revenue. Pre-Covid you could count on getting a

pulling unit sometimes next day if you had a mechanical failure. Now it's 3-4 weeks. $20/hour

for green rig hands evidently isn't enough to move the needle, whether it's because the work is

too difficult, or it's easier to keep cashing the government checks. And by my count we are in

a similar situation with oil field pumpers. We have 13 of them. 2 are 50s, and the rest are all

over 60. I'm in my early 40s and my field superintendent is 56. He loves to work and will

probably do so until he's 70-75. When he checks out will probably be when I check out.

REPLYSHALLOW SAND IGNORED07/20/2021 at 9:55

am

Kansas Oil.

Great to hear from you.

Thanks for confirming what we are experiencing.

The big question is whether this is also going on in the shale basins, primarily Permian. If

it is, don't see how USA production grows much.

I drive across Kansas on both I 70 and the South Route through Wichita to the OK panhandle

quite a bit. Always keep my eyes open for whether pumping units are moving or not.

I worry about whether the huge feed lots, hog facilities and packing plants out there can

find enough help. People have no clue how much of the USA is fed from the TX, OK panhandles on

up through Western KS and NE.

Two years ago, Wall Street banks were on their way out of a long-term relationship with the

oil industry. Now, with oil prices over $70 for the first time in three years, big bond buyers

are snapping up oil bonds once again.

Only there is a condition this time.

The Wall Street Journal's Joe Wallace and Collin Eaton

wrote this week that Wall Street was buying bonds from non-investment-grade U.S. energy

companies, which took advantage of record low interest rates to raise some $34 billion in fresh

debt in the first half of the year.

That's twice as much as the industry raised over the same period last year. But investors

don't want borrowers to use the cash to drill new wells. They want them to use it to pay off

older debt and shore up balance sheets.

It makes sense, really, although it is a marked departure from how banks normally react to

oil industry crises. The 2014 oil price collapse, in hindsight, may have been the last "normal"

crisis. Oil prices fell, funding dried up, supply tightened, prices went up, banks were willing

to lend again, and producers poured the money into boosting production.

Since then, however, the energy transition push has really gathered pace and banks have more

than one reason to not be so willing to lend to the oil industry. With the world's biggest

asset managers setting up net-zero groups to effectively force their institutional clients to

reduce their carbon footprint and with the Biden administration throwing its weight behind the

push for lower emissions, banks really have little choice but to follow the current. Their own

shareholders are increasingly concerned about the environment, too.

https://www.youtube.com/embed/aQXqMVeoOPs

Yet business is business, and nowhere is this clearer than in banks' dealings with the oil

industry. Bank shareholders may be concerned about the environment, but they certainly would be

more concerned about their dividend""and part of that comes from income made from lending to

oil. And the higher oil prices go, the more willing banks will be to lend to those that produce

it.

When they were unwilling to lend to the oil industry, other lenders

stepped in . Last year, alternative investment firms scooped up hundreds of millions in oil

industry debt from banks that were cutting their exposure to the politically incorrect

industry. Hedge funds and other so-called shadow lenders don't seem to have banks' misgivings

about profiting from oil and gas.

Now banks have mellowed towards oil somewhat, but it is an interesting twist that the

current loans come with the condition of not boosting output. Again, it makes sense. For years,

the shareholders of U.S. shale oil companies have been complaining about poor returns as the

companies put everything into output growth. Now it's payback time, and shareholders want their

returns.

So do lenders, apparently.

Per the WSJ article, this year, bond buyers "want to see companies repairing their

balance sheets and delivering to creditors and shareholders rather than plowing money into new

wells."

No. Not true and badly misleading. Remaining EIA PDP from the Permian will not generate sufficient net cash flow to self fund

123,000 wells (your estimate) costing nearly $1T, much less do that AND pay down over $100 B of existing debt in the Permian. That's

using EIA PDP estimates; whack those by 30%. It is not possible to drill $9MM wells for a 135% ROI over 15 years and be financially

self-sufficient, service and pay down debt, provide returns to investors and maintain a 100% RRR. The US shale oil model does not

work without credit. $70 "assumptions" do NOT solve the issue of where the money is going to come from for your miracle of abundance

to actually occur. ANCIENTARCHER IGNORED07/05/2021 at 6:01 am

EIA is expecting excess supply in 2022.

Are they smoking some really good stuff to come up with this? I'd like to smoke that too

As I see it, demand will slowly go back up to previous level of 100mmbpd and then resume its slow march upwards. Where is it that

EIA are seeing that extra production from that will lead to oversupply 6-7 months down the line? All I see is that various regions

of the world are slowly declining in production due to a combination of worsening asset quality and a paucity of capex over the last

several years, especially in 2020/21. US Shale, Russia, Offshore, conventional onshore, small members of OPEC and even Saudi"¦ all

are experiencing pressure on production.

OPEC seems to be concerned about the possibility of excess supply next year, probably due to this report by EIA. The Saudis are

especially concerned and therefore are pushing to extend the supply cut to the end of 2022 which UAE is opposing.

So, am I missing a crucial element or are the EIA on to something here?

The U.S. is producing roughly 2 million barrels a day less than it was before the pandemic.

In the USA shale patch many "sweet spots" are now gone and what remains is less proficableto drill and thus requres higher prices.

In this sense the currentoil price might be not enough to spur additional activity.

Frackers have been forced to rein in spending and

live

within their means

after many investors lost faith in the companies following years of poor returns, lenders reduced their

credit lines and capital markets showed little interest in funding expansive new drilling campaigns.

The result is that shale drillers, which in the past have played the role of the oil world's swing producer by quickly increasing

output to meet demand, are largely standing pat for now, as the reopening of Western economies leads to a resurgence of global

oil

and

gas prices

.

The companies are raking in more cash than ever. Public shale companies that drill primarily for oil collectively generated a

record $4.1 billion in free cash flow in the first quarter of 2021 and are poised to take in almost $15 billion for the year if

prices remain higher, according to consulting firm Rystad Energy.

U.S. shale producers generated more free cash

flow in the first quarter than any time

in the

industry's history, analysts said.

Free

cash flow

Source:

Rystad Energy

billion

2014

'15

'16

'17

'18

'19

'20

'21

-12.5

-10.0

-7.5

-5.0

-2.5

0

.0

2.5

$5.0

But instead of pumping that money back into drilling as they have historically done, large producers such as

Occidental

Petroleum

Corp.

OXY

+2.09%

and

Ovintiv

Inc.,

the

company formerly known as Encana Corp., have said they plan to

focus

on reducing debt

, keeping U.S. output flat. Other sizable shale drillers such as

Pioneer

Natural Resources

Co.

PXD

+0.66%

and

Devon

Energy

Corp.

DVN

+3.40%

are

socking away money to return to investors in the form of variable dividends, one of the enticements they want to use to lure more

investors back.

"We're producing all this free cash flow, but it's not going out to investors yet," said Scott Sheffield, chief executive of

Pioneer, noting that many companies are focusing on debt before they return cash to investors. "There's no reason for them to buy

into this sector at this point in time."

... ... ...

In the heyday of the shale boom, publicly traded oil producers typically reinvested more than 100% of the cash flow they made

from operations back into drilling campaigns. Now they are using about half of the income they generate on new drilling and are

only growing output slightly, if at all.

... ... ...

Shale companies had about $148.6 billion in debt coming into the year, according to energy consulting firm Wood Mackenzie, and

much of the cash they are collecting is going toward that debt pile. Securing new capital is increasingly difficult for many.

Many large U.S. banks have cut their energy lending, and some European ones such as

Deutsche

Bank

AG

and

Société

Générale

SA

SCGLY

5.48%

have

exited fossil fuel financing altogether...

Callon said it would cut its 2021 capital expenditures to $430 million, a 12% reduction from its 2020 budget. In 2019, it spent

$515 million. As a result, the company said it would produce about 90,000 barrels of oil and gas a day in 2021, down from more

than 101,000 barrels a day in 2020. Callon said it is focused on reducing its roughly $3 billion in debt. The company declined to

comment.

Many frackers made bad bets early this year, hedging their production with oil in the forties and low fifties -

especially Pioneer and Devon. This article, for some reason, fails to mention that fact and it's impact on their

current production.

PAUL HUNT

After 38years in O&G E&P I filtered out of the industry due to changing industry. The loss of expertise and technology

in the energy industry over the last 5 years has been huge. USA has given the energy industry to China. Look for

overall energy prices to triple in less than 10 years.

DAVID LAWRENCE

What is left out in this article are the returns of the 600lb gorilla of frackers in the room.

XOM alone generated almost $7 billion in free cash flow last quarter. With oil prices where they are that figure is

likely to rise to $10 billion next quarter. The company has only $53 billion in debt outstanding having already pared

down $6 billion during the pandemic.

They are going to gobble up even more weaker little guys shortly.

Peter Sullivan

I don't see XOM significantly increasing production in US shale anytime soon. They are focusing CAPEX on deepwater

assets that present a better ROI than shale. Who would of thought we have reached a time where it is less risky for a

US based company to drill in a small South American country than within our own borders?

DAVID LAWRENCE

XOM CAPEX is greatly reduced (1/2) in 2021 across the board. This is because they spent nearly $20 billion in 2020 using

piles of borrowed money that so many junior analysts obsessed over.. The plan is to pay that pile down with the

windfall those investments are generating.

XOM is far from a pure play fracker and have always developed the largest offshore assets of any company and Guyana is a

hot prospect!

Edward Cotterell

The oil market has always been boom and bust. When the pandemic hit people stopped driving and the oil market went

bust. Prices fell and drillers went bankrupt. Now the economy is reviving, people are driving again and oil is

booming. To those who think otherwise, get a grip. The price of gasoline today is about where it was in 2018 and 2019

pre-pandemic. You know, when Trump was president.

This article points out a longer term change in the market. The hype over fracking is over. The lenders want their

principal back plus interest and they are not taking exaggerations from drillers any more. So oil prices may have to go

a bit higher until the lenders are satisfied that they will get their money. Then they will lend to drillers and

fracking will crank up.

Trash that 12 mpg pickup. Get a vehicle that gets better mileage. Some hybrids get over 50 miles a gallon. Electrics

get the energy equivalent of 100 miles a gallon.

Ben Griffith

How is the electricity produced ? Coal, oil, natural gas produced by fracking, nuclear, hydroelectric dam, harnessing

the hot air of Climate Change speech ?

ROBERT STUPP

Many don't realize how many older, experienced energy professionals took retirement over the last few years. Similar to

the 1980's energy bloodbath, it will take a while to establish teams able to stabilize the companies, let alone grow

them from survival mode. You can't turn on production like your kitchen faucet.

Jerome Abernathy

Fracking wells deplete so fast that the capex expenditures needed to maintain and grow production result in a low ROI

for the industry. Worse yet, given the volatility of oil prices and the precarious state of their balance sheets,

frackers are unattractive borrowers. The industry needs a new, creative financing model.

Matthew Oatway

An interesting article, but the authors should have acknowledged (a) the impact of consolidation in the sector on

production discipline and (b) the fact that many shale producers have a large portion of their production hedged at

lower crude prices. Both factors point to a more restrained return to production growth that we have seen in the past.

Banks have started to cut their exposure to the U.S. shale patch, seeing more than 100

producers and oilfield services firms go bust last year and feeling the environmental, social,

and governance (ESG) pressure to reduce credits to fossil fuels. While traditional lenders are

cutting their losses and de-risking energy loan portfolios, alternative capital providers are

stepping up to scoop up U.S. energy debt at a discount and take part in debt or equity

transactions that could give them returns sooner than a loan would for a bank.

Since the oil price crash in 2020 and the downturn in the U.S. shale industry, banks have

been wary of their exposure to the sector. The commodity price slump last year dramatically cut

the value of the assets of oil and gas firms, against which they have traditionally obtained

loans from banks.

Running for the Exit

Lenders slashed the amounts of reserve-based loans to the U.S. shale firms in the middle

of last year.

But it is not only purely financial considerations that are driving reduced bank exposure

to the oil and gas industry. ESG lending and aligning loan portfolios to the Paris Agreement

goals are now more prominent than ever.

For example, asset manager Schroders, which holds many bonds in the banking sector, is

engaging with banks to understand their fossil fuel exposure.

"Banks that are highly exposed to the fossil fuel industry face significant financial,

regulatory and reputational risks as a result of the transition to a low-carbon economy,"

Schroders said, explaining its rationale to identify the exposure of the banks to oil, gas, and

coal.

Increased pressure from the ESG universe, coupled with years of poor returns of U.S.

shale firms, have prompted several major transactions in which banks have sold energy debt to

hedge funds and private equity firms.

Hancock Whitney, for example, agreed last year to sell $497 million worth of energy loans

to certain funds and accounts managed by alternative investment provider Oaktree Capital

Management. Hancock Whitney expected to receive $257.5 million from the sale of the

reserve-based loans (RBL), midstream, and non-drilling service credits.

Hancock Whitney's main reason to sell the energy loans was to minimize the risks to its

loan portfolio.

"The primary objective of this sale is to continue de-risking our loan portfolio by

accelerating the disposition of assets that have been impacted by ongoing issues within the

energy industry, and have now been further complicated by COVID-19," Hancock Whitney's

President and CEO John M. Hairston said.

At the end of 2020, Bank of Montreal decided it would wind down its non-Canadian

investment and corporate banking energy business.

Most recently, ABN AMRO announced last week it would sell a $1.5 billion portfolio of

energy loans to funds managed by Oaktree Capital Management and affiliates of Sixth Street

Partners. The portfolio consists of loans to around 75 companies active in the North American

energy markets.

With this sale, ABN AMRO is withdrawing from oil and gas related lending in North America

as part of a process to wind down its non-core activities and significantly reducing the

non-core loan book.

"On a daily basis, loadings will decline by 22% in July compared to the current month,

Reuters calculations showed."

REPLYPOLLUX IGNORED06/28/2021

at 1:37 pm

"Russian oil production has declined so far in June from average levels in May despite a

price rally in oil market and OPEC+ output cuts easing, two sources familiar with the data told

Reuters on Monday.

Russia's compliance with the OPEC+ oil output deal was at close to 100% in May, which

means the state is about to exceed its target in June.

Two industry sources said that lower output levels may be due to technical issues some

Russian oil producers are experiencing with output at older oilfields."RON PATTERSON IGNORED

06/28/2021 at 2:38 pm

Yes, they are definitely experiencing issues with their older oilfields, it's called

depletion. But that decline is only 33,000 bpd or .3%. But your post above that one says

exports in the third quarter will decline by 22%. What gives there?

I just checked the Russia site and they have revised up their original May estimate. It is

one week later than the original. Production is now down 9,000 b/d. RON PATTERSON IGNORED06/28/2021

at 4:50 pm

Yeah, they revised it up by 14,000 pbd. A pittance. Now they are down only 9,000 bpd instead

of 23,000. Nothing to get excited about. Basically, they were flat in May.

JEAN-FRANÇOIS FLEURY IGNORED06/28/2021

at 4:09 pm

"Russia plans to decrease oil loadings from its Western ports to 6.22 million tonnes for

July compared to 7.75 million tonnes planned for loading in June, the preliminary schedule

showed." 7,75 x 10^6 – 6,62 x 10^6 = 1130000 t. 1130000×7,3/30 = 274966 b/d.

Therefore, these decrease of oil export suggests a decrease of production of 274966 b/d.

Precedently, it was announced that oil exports of Russia would decrease of 7,2 % for the period

July-September or a decrease of 308222 b/d. Therefore, it's coherent.

https://www.zawya.com/mena/en/markets/story/Russias_quarterly_crude_oil_exports_to_drop_72_schedule-TR20210617nL5N2NY2IQX8/?fbclid=IwAR0ZjvwzjVS427CbUAzTL1vJfqog7R8CDwaJAvI3uUdaw_0z5S5l_57SGFY

I notice that it concerns the "Western ports", therefore the exports toward EU and USA. Well,

EU is also the main customer of Russia with 59% of the oil exports of Russia. RON PATTERSON IGNORED

06/28/2021 at 4:59 pm

Western Syberia is where all the very old supergiant fields are. They produce 60% of Russian

crude oil. Or at least they used to. LIGHTSOUT IGNORED06/29/2021

at 2:11 am

Ron

If one of the West Siberian giants is rolling over in the same way as Daquing did, things could

get very interesting very quickly. RON

PATTERSON IGNORED06/29/2021

at 7:24 am

Four of Russia's five giant fields are in Western Siberia. The fifth is in the Urals, on the

European side. All five have been creamed with infill horizontal drilling for almost 20 years.

All five are on the verge of a steep decline. Obviously, one and possibly more have already hit

that point.

This linked article below is 18 months old but there is a chart here that shows where

Russia's oil is coming from. Notice only a tiny part is coming from Eastern Siberia, the hope

for Russia's oil future. Those hopes are fading fast.

As I have written a few months ago: When you reduce output voluntarily for a longer time,

all the nickel nursers from accounting and controlling will cut you any investing in over

capacity you can't use at the moment. That works like this in any industry.

So you have to drill these additional infills and extensions after the cut is liftet. And

this will take time, while fighting against the ever lasting decline.

"Abu Dhabi's state-owned Adnoc has informed customers that it will implement cuts of

around 15pc to client nominations of all its crude exports loading in September, even as the

Opec+ coalition considers further relaxing production quotas.

It was unclear why Adnoc is deepening reductions for its September-loading term crude

exports, with the decision coming ahead of the next meeting of Opec+ ministers scheduled for 1

July when the group is expected to decide on its production strategy for at least one

month"

As oil price stays above $70/barrel, most shale will come back. However the max reached by

USA was 13,100 million b/d. So whether World will hit 75 million b/d is doubtful. But NGL keeps

increasing because of increase in natgas output. Besides nearly 6 million b/d that comes from

CTL, GTL and bio-fuels will keep overall oil consumption above 100 million b/d.

Despite rapid increase in electric vehicles, oil will hold above 100 minion b/d mark.

REPLYHOLE IN HEAD IGNORED06/20/2021

at 1:34 pm

Ted , demand is governed by price and availability . Demand of 100 mbpd is immaterial if the

supply is only 80mbpd . Shale is not coming back . USA has peaked . Period . The peak in shale

was (is) the peak of oil production in USA . I have commented earlier that " all liquids " is

BS . The 6mbpd of NGPL ,CTL , GTL etc. are just " fill in the blanks " . These are not

transportation fuels and have 65% of the BTU of crude . HICKORY IGNORED 06/20/2021

at 2:30 pm

Hole- Hydrocarbon Gas Liquids are nothing to belittle. It is a lot of energy-

"HGLs accounted for over a quarter of total U.S. petroleum products output in 2018"

NGL has about 70% of the energy content of a barrel of crude. In addition most uses for HGLs

are not for transportation which is the the main use for crude plus condensate.

As Ron has said we don't count bottled gas. I would say NGL should be put in a basket with

natural gas.

Or we could define liquid petroleum as that which is a liquid at 1 atmosphere pressure and

25C aka STP.

By that standard only pentanes plus would qualify, which makes sense as it is essentially

condensate, the proportion of pentanes plus in the US NGL mix is less than 12% by volume, 2020

data (582

kbpd). RON PATTERSON IGNORED06/21/2021

at 4:01 pm

I am expecting prices a lot higher in 2022. An average of $85 would not shock me at all.

They will be higher because oil production will not fully recover to the 2019 level as everyone

expects it to.

The EIA Short Term Outlook has production fully recovered by the end of 2022 and total

liquids about one million barrels per day higher for non-OPEC.

OPEC officials heard from industry experts that US oil output growth will likely remain

limited in 2021 despite rising prices,

While there was general agreement on limited US supply growth this year, an industry source

said for 2022 forecasts ranged from growth of 500,000 bpd to 1.3 million bpd

The forecasts for 2021 were for average output to be close to 200 kb/d. The 1.3 Mb/d

prediction for 2022 is out to lunch. The 500 kb/d has a chance but I think the average will be

closer to 350 kb/d.

I think WTI will be $85 plus/minus $5 in mid 2022. This will push the average price of

gasoline slightly above $3/gal. As for output, the US will add somewhere close to 300 kb/d

average in 2022 over 2021. I am betting on some restraint on the part of the drillers. The

Permian is the pivotal basin and I see that the early results for 2021 wells are not as good as

2020.

The big unknown for me is: What is a sustainable price for WTI, $100? At what point does

gasoline suck too much money out of the economy. Once the economy starts to slow, oil demand

will slow. We can all remember 2008.

If WTI crosses $90, OPEC might start to worry. However will they have the spare capacity to

try to control it? Six months from now we can revise our estimates.

What do you mean by confirmation? Do you mean they will confirm that the peak was 2018-2019?

If so, I cannot agree. No, there will be deniers all the way down. There is something about the

human psyche that just cannot accept reality... MATT MUSHALIK IGNORED06/19/2021

at 8:57 pm

Thanks for continuing to monitor crude oil production. As of now, we are back to 2005

levels!

Frac Sand Baroness @sand_frac · Jun 16 There is

currently a @chevron well

uncontrollably blowing out on my land that I live and raise cattle on in West Texas. It is

injecting super concentrated brine and benzene into my water supply. The casing (metal pipe) is

so corroded that Chevron literally cannot re plug it. 5.7K views 0:01 / 0:06 3 60 117

Frac Sand Baroness @sand_frac

· Jun 16 More concerningly, this

well was plugged and abandoned (P&A) in 1995. For those not in the oil industry, a P&A

blowout is extremely rare. A plugged well is exactly that: plugged. It is filled with concrete

plugs, and considered to be permanently deactivated and safe. 2 7 67 Frac Sand Baroness @sand_frac · Jun 16 We've had

issues with Chevron before. In 2002, we flushed a toilet at the ranch house (approximately 1.5

miles south of the blowout) and crude oil bubbled up. The leak source was never fully

identified, and we shut in that water well. 2 6 66 Frac Sand Baroness @sand_frac · Jun 16 Chevron had

operations nearby, so drilled water monitoring wells. These monitoring wells identified a crude

oil plume in the groundwater, and also found a large salt water plume. See Texas Railroad

Commission OCP #08-2423. Again, we never found the source. 1 5 57 Frac Sand Baroness @sand_frac · Jun 16 This

required Chevron to provide an annual water test result to the landowners (me). Of course, they

didn't comply from 2007 through 2013. We never heard about this, and thought our water was safe

again.

One of the biggest pieces of news for Royal Dutch Shell recently has been the Dutch court

ruling that forces them to make a larger 45% emissions reduction by 2030.

Despite this sounding very transformation, considering the geological and economic

reality of their current situation, it actually does not significantly change their underlying

future.

Their reserve life is only sitting at just above seven years and thus even if they wished

to maintain their fossil fuel production, they already required significant investments before

2030.

SNIP You Cannot Fight Geology

Upon reviewing their reserves, it may initially sound very impressive to hear that their

oil and gas reserves currently stand at slightly over nine billion barrels of oil equivalent.

Although in reality this actually sits rather low when compared to their annual production

during 2020 of 1.239b barrels of oil equivalent. This effectively only leaves their reserve

life at just above seven years, which is not particularly long and thus means that their fossil

fuel production would already begin shrinking dramatically by the latter half of this decade.

Admittedly they would likely continue replacing a portion of their oil and gas reserves in the

future but their current production rate would still see them running very low by 2030 if

approximately half were replaced per annum, as the graph included below displays.

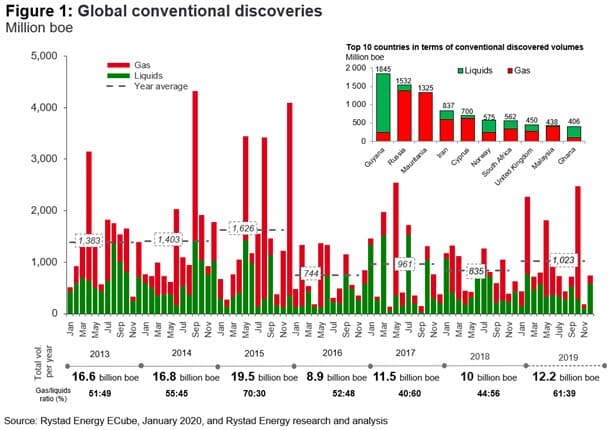

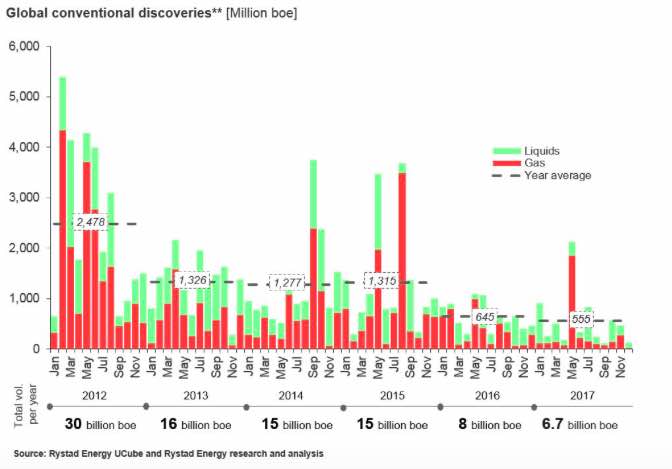

There are two charts in this article. The second on titled: Oil Discoveries Lowest Since

1847 is alarming. STEPHEN HREN IGNORED06/17/2021 at 8:25 am

Hi Ron, any thoughts on why Shell would bag their operations in the Permian while they are

also running low on reserves everywhere else? Seems like they would be holding on to every

scrap of producing land they could. Unless one of two things: 1) they are making a serious

attempt to transition to a low carbon energy company; and/or 2) their holdings in the Permian

are worth squat REPLYRON PATTERSON IGNORED06/17/2021 at

9:22 am

NEW YORK/HOUSTON, June 15 (Reuters) – A cadre of oil companies, seeing continued

profits in shale, are mulling Royal Dutch Shell's (RDSa.L) holdings in the largest U.S. oil

field as the European giant considers an exit from the Permian Basin, according to market

experts.

The potential sale of Shell's Permian holdings, located in Texas, would be a litmus test

of whether rivals are willing to bet on shale's profitability through the energy transition to

reduce carbon emissions.

Shell would follow in the footsteps of other producers, including Equinor (EQNR.OL)

and Occidental Petroleum (OXY.N) that have shed shale assets this year, looking to cut debt and

reduce carbon output in the face of investor pressure.

Shell, like a lot of other companies, sees shale assets as a very low profit, or even a

losing proposition. They can take the money from the sale, reduce their debt, and reduce carbon

emissions of their company in one fell swoop. More from the article:

Against this backdrop, estimates for Shell's acreage run from $7 billion to over $10

billion, the latter implying a valuation of almost $40,000 an acre.

That would be in line with the per-acre price Pioneer Natural Resources (PXD.N) paid for

DoublePoint Energy in April, the most costly deal since a 2014-2016 rush by producers to grab

positions in the Permian.

Most Permian deals this year have closed between $7,000 and $12,000 per acre, said

Andrew Dittmar, senior mergers and acquisitions analyst at data provider Enverus.

If they can get $40,000 per acre they have found a greater fool to offload their acreage on.

HICKORY IGNORED06/17/2021 at 9:44 am

Something about that doesn't make sense. The need or desire to downsize is likely due to an

inability to project making profit on the shale assets rather than any concern over a carbon

footprint- I don't believe they are in business to win any kind of beauty contest. REPLYROGER

IGNORED06/17/2021 at 8:17 pm

"Shell's position as a major European enterprise has become untenable. The Spar had gained a

symbolic significance out of all proportion to its environmental effect. In consequence, Shell

companies were faced with increasingly intense public criticism, mostly in Continental northern

Europe. Many politicians and ministers were openly hostile and several called for consumer

boycotts. There was violence against Shell service stations, accompanied by threats to Shell

staff."

Things are a little different for European companies I recall "Greenpeace sympathizers"

fire-bombed a gas station back then; in light of what has transpired in the US recently who is

to say it couldn't happen again?

Shell is well aware of peak oil, and can't solve the problem. So, what would you have them

do? REPLYKOLBEINIH IGNORED06/17/2021 at 1:26 pm

"Shell would follow in the footsteps of other producers, including Equinor (EQNR.OL) and

Occidental Petroleum (OXY.N) that have shed shale assets this year, looking to cut debt and

reduce carbon output in the face of investor pressure."

I don't think it has anything to do with shale oil specifically. For Equinor it has to do

with that it can draw on competence in Norway in the harsh offshore environment in the North

Sea. Floating offshore wind power is where Equinor is world leading with technology and know

how; now about to be utilised in the North Sea, Japan, US East coast and California. It is not

more economical than ground based offshore wind mills, but has some advantages when it comes to

lifecycle costs. For one, the wind mills can be placed in optimal wind condition areas not in

the way of fishing resources. The big size of wind mills will not cause problems (the height

and diameter of the blades are necessary to capture enough wind energy). And also the wind

mills can be more easily moved to land and recycled, e.g. the steel. Wear and tear offshore is

on the minus side.

Usually the blades are made of carbon fiber to make it lighter, but it can also be made of

aluminum in the future with lower efficiency.

Shell is just now investing in North Sea South II in Norway for ground based offshore mill

farms together with BP. To make the North Sea work with the enormous amount of wind power

coming online and connection cables everywhere is very serious business and just a priority.

Shale oil is too much of a distraction for Shell and Equinor, not even within their core

competence area. REPLYJAY

WOODS IGNORED06/18/2021 at 7:50 am

Shell was ordered by a Dutch court to cut by 45%. Of course, they will cut their "losers"

first.

The chart is old and was published in 2016 by Wood Mackenzie and there is no data for 2016.

It also leaves out the discovery of Ghawar in 1948, first bar/spike. I have not seen any

updates since then. Not sure if Guyana had been discovered in 2016. The original is

attached.

Ironically, the wave of ESG investing in global energy markets may lead to much higher

oil prices as a serious lack of capital expenditure on new fossil fuels dries up just as demand

for crude continues to grow

Pressure from investors, tighter emissions regulation from governments, and public

protests against their business have become more or less the new normal for oil companies. What

the world -- or at least the most affluent parts of it -- seem to want from the oil industry is

to stop being the oil industry.

Many investors are buying into this pressure. ESG investing is all the rage, and

sustainable ETFs are popping up like mushrooms after a rain. But some investors are taking a

different approach. They are betting on oil. Because what many in the pressure camp seem to

underestimate is the fact that the supply of oil is not the only element of the oil

equation.

"Imagine Shell decided to stop selling petrol and diesel today," the supermajor's CEO Ben

van Beurden wrote in a LinkedIn post earlier this month. "This would certainly cut Shell's

carbon emissions. But it would not help the world one bit. Demand for fuel would not change.

People would fill up their cars and delivery trucks at other service stations."

Van Beurden was commenting on a Dutch court's ruling that environmentalists hailed as a

landmark decision, ordering Shell to reduce its emissions footprint by 45 percent from 2019

levels by 2030.

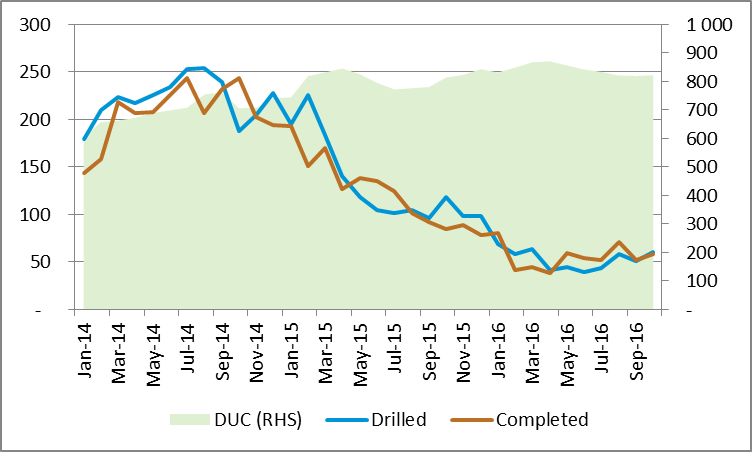

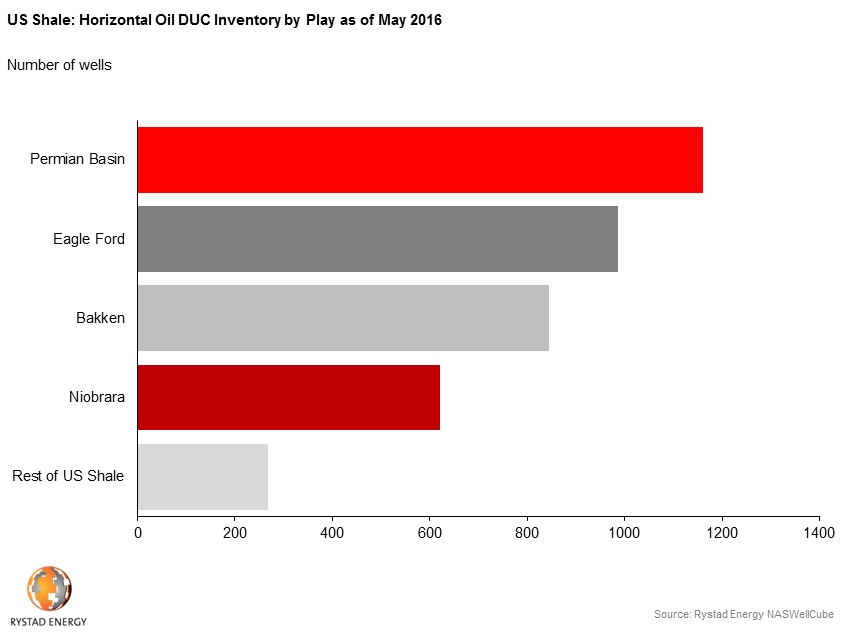

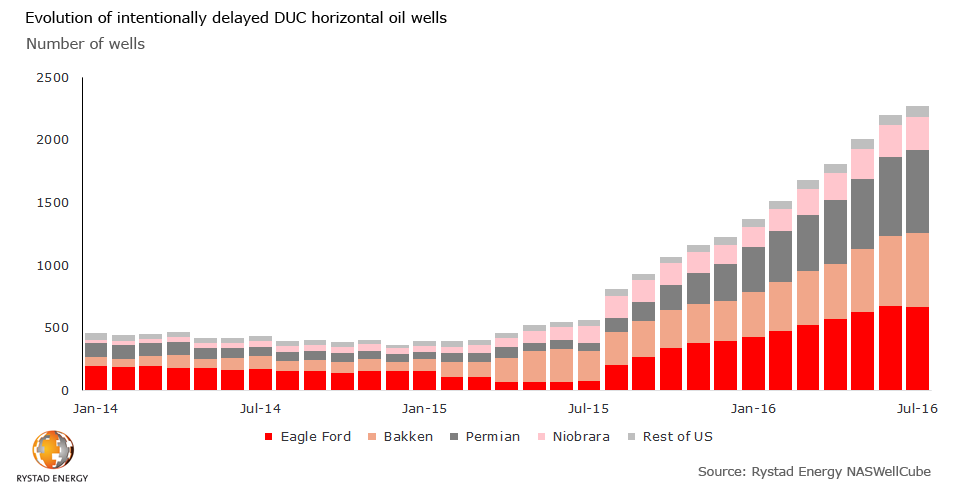

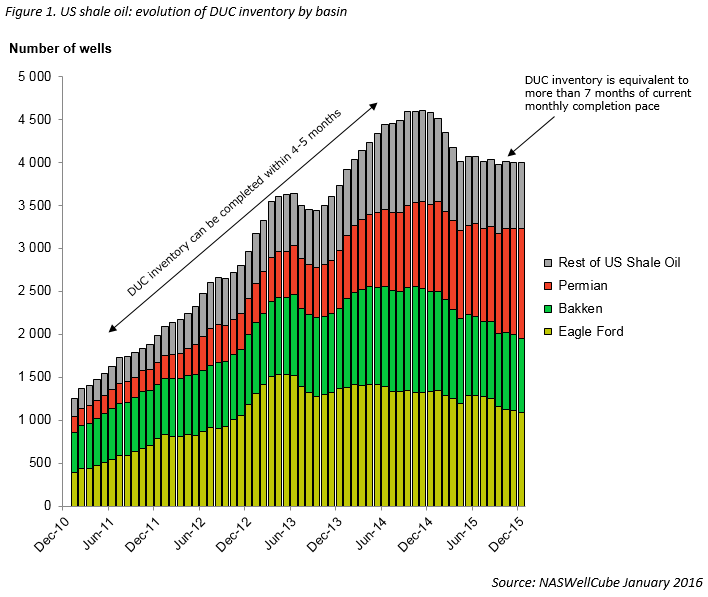

Total DUCs in shale basins are falling at the rate of about 250 per month. I don't know how long this can continue. I have been

told by some experts in the field that there are some DUCs that will never be completed because they would not produce enough oil

to pay the completion cost. So we just cannot count the DUCs and divide by 250. The decline in DUCs will have to stop sooner or

later.

Frugal, I am not an oilman, and an oilman could obviously give a better answer than I. But I will give it a shot, and hopefully,

I will be corrected for any mistakes I make.

Drillers are not frackers and frackers are not drillers. That is an entirely different operation requiring different crews, different

equipment, and different CAPEX. But the driller leaves behind samples from the well, indicating just how productive the well should

be. The best wells will obviously be fracked first. The less promising wells will be left for times when the price is high enough

to justify the fracking cost.

But"¦. the total cost of the well is the drilling cost plus the fracking cost. And in a DUC, the drilling cost has already been

spent. So when times get hard, and you can get a well, though it might not be the best well, you have already paid the drilling

cost, so you can get it for only the fracking cost now. So you pay the fracking cost and recover what you can. And this would

be the case especially if the new wells that are coming in are less promising than the poor wells already drilled.

But then, that's just my opinion, for what it's worth.

Exxon Mobil Corporation XOM has been generating fewer barrels of oil from the prolific

shale fields of the United States since 2019, per Reuters.

According to a latest report, the company's oil wells, which are involved in some of the

most promising shale fields, produced fewer barrels of oil per well despite an increase in

overall expenditure and production.

In 2017, Exxon, which is one of the largest shale oil producers, acquired $6.6 billion of

net acres in New Mexico, which doubled the company's assets in the Permian basin that spans

west Texas and New Mexico. Notably, the company intends to boost shale output in the New Mexico

portion of the Permian basin to 700,000 barrels per day (bpd) by 2025.

Per data released by the Institute for Energy Economics and Financial Analysis ("IEEFA"),

Exxon's average liquid output for the first 12 months of a well dropped to 521 bpd in 2019

from an average of 635 bpd in 2018 in its Delaware basin assets of New Mexico.

That's an 18% drop in production per well. And this was before the pandemic

Another scenario is that some exporting nations realize they will need this oil as the world

stares into a scarcity of oil. They might say: "Shit, why are we selling this stuff when we

will desperately need it for ourselves in a few years?" And as they cut back, or stop exporting

altogether, the problem gets a lot worse, and prices spike even higher. REPLYDOUG LEIGHTON IGNORED06/13/2021 at 3:34 pm

L.O.L. The decision concerning the proportion of a domestic resource that should be

preserved for domestic needs, and how much to export, is interesting. China's REE deposits come

to mind. Also, the impact of the immediate use of a resource versus a lower level of

exploitation over time might come into play in some (perhaps unrealistic) scenarios as well.

Not many examples of countries that have exhaustible natural resources saving some for future

generations I'm aware of; probably would result in an unwelcome war or another ugly result!

John Kilduff of Again Capital has predicted Brent to hit $80 a barrel and WTI to trade

between $75 and $80 in the summer, thanks to robust gasoline demand. Brent is currently trading

at $71.63 per barrel, while WTI is changing hands at $69.13.

On 05/07/21 the US 10year chart formed a hammer candlestick on daily chart within a consolidation pattern. Which suggested higher

yields coming. Well little over a month later price broke below the bottom of that candlestick which suggest that the bond market

doesn't believe the inflation we have seen is here to stay. Yield headed lower.

The inflation we have had seems to be supply side due to covid. If inflation is at peak which bond market is suggesting. Oil price

might not have much more room to run higher. And I'd take it a step further and say price inflation due to a weaker dollar is starting

to real hurt places like China and they are going to act by tightening monetary policy. You think this would be positive for the

yuan and push the dollar even lower. But when you tightening monetary policy credit contracts and economic activity contracts.

I do expect oil price to rollover and head back to $50-$55 might happen from a slightly higher price from here because of lag

time between when bond market signals rollover in inflation back into deflation and when prices start reacting to this.

REPLYEULENSPIEGEL IGNORED06/11/2021

at 10:07 am

This isn't your history bond market.

Inflation doesn't really matters, what only matters is the one big question: "How much bonds does the one market member with unlimited

funds buy?".

And the time the FED was able to rise more than .25% is in the rear mirror "" when they hike now, inflation or not, all these

zombie companies and zombie banks will fail and no lawyer in the world will be able to clean up the chaos after all these insolvency

filings.

They have to talk the way out of this inflation. They have to talk until it stops, or longer. They can't hike. They can perhaps

hike again when most of the debt is inflated away "" a period with 10+% inflation and 1% bond interrest.

And yes, they can buy litterally any bond dumped onto the market "" shown this in March last year when they stopped the corona

crash in an action of one week.

I think most non-investment-banks are zombies at the moment, and more than 20% of all companies. They all will fail in less than

1 year when we would have realistic interrest rates. On the dirty end, this would mean 10%+ for all this junk out there "" even mighty

EXXON will be downgraded to B fast.

In old times the FED rates would be more than 5% now with these inflation numbers. Nobody can pay this these days.

And now in the USA "" look for how much social justice and social security laws you'll get. The FED has to provide cover for all

of them.

We in Europe will do this, too. New green deal, new CO2 taxes, better social security "" the ECB already has said they will swallow

everything dumped on the market.

So, oil 100$ the next years "" but some kind of strange dollars buying less then they used to.

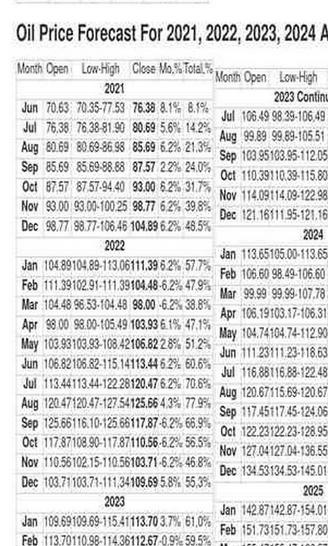

This is nonsense. They have Brent crude oil prices peaking, so far, in March 2025 at $164.11. And they have WTI peaking the same

month at $132.55, $32.56 lower. There is no way the spread could be that large. Also, they have natural gas prices dropping over

the same period. Just who the hell are these "Longforcast.com" people?

Disregard anything with "forecast" in the title. They don't have a time machine, and extrapolation is a horrible metric with dynamic

markets as complex as the energy ones.

Might as well show me the tea leaves or goat entrails and tell me the price on 11 June 2027.

REPLYSHALLOW SAND IGNORED06/11/2021

at 3:58 pm

Dennis Gartman is still considered a commodities expert.

He infamously said in 2016 that WTI would never be above $44 again in his lifetime. He is still alive last I knew.

Since I have owned working interests in oil wells (1997) I have sold oil for a low of $8 and a high of $140 per barrel. 6/14 oil

sold for $99.25 per barrel. 4/20 oil sold for $15.40 per barrel.

Predicting oil prices is impossible.

About the only oil price prediction I have had right so far is that if Biden won, oil prices would rebound. Of course, we can

argue about why that is, and if there is even any connection.

There are still no drilling rigs running in the field we operate in. There are still hundreds of production wells shut in. There

are still less than 10 workover rigs running in our field. The largest operator still has a help wanted sign up in front of its office.

We finally found one summer worker, he is still in high school, but thankfully covered by our workers comp. He cannot drive our trucks,

and is limited to painting, mowing, weed control, digging with a shovel, cleaning the shops and pump houses and other tasks like

those. That's ok, because we need that, but not being able to drive is a pain. But auto ins won't allow anyone under 21 to be covered.

REPLYIRON MIKE IGNORED06/11/2021

at 11:53 am

Yea Ron i agree with Kleiber, I wouldn't take anything on that site too seriously.

REPLYOVI IGNORED06/11/2021

at 1:34 pm

The IEA is now starting to sound warnings about supply. Last week they were telling the oil companies to stop exploring and to

move toward a renewable energy future.

IEA: OPEC needs to increase supply to keep global oil markets adequately supplied

In its monthly oil report, the International Energy Agency (IEA) has said that global oil demand is set to return to pre-pandemic

levels by the end of 2022, rising by 5.4 million bpd in 2021 and by a further 3.1 million bpd next year. The OECD accounts for 1.3

million bpd of 2022 growth while non-OECD countries contribute 1.8 million bpd. Jet and kerosene demand will see the largest increase

( 1.5 million bpd year-on-year), followed by gasoline ( 660 000 bpd year-on-year) and gasoil/diesel ( 520 000 bpd year-on-year).

World oil supply is expected to grow at a faster rate in 2022, with the US driving gains of 1.6 million bpd from producers outside

the OPEC alliance. That leaves room for OPEC to boost crude oil production by 1.4 million bpd above its July 2021-March 2022 target

to meet demand growth. In 2021, oil output from non-OPEC is set to rise 710 000 bpd, while total oil supply from OPEC could increase

by 800 000 bpd if the bloc sticks with its existing policy.